どのトレーダも「自らのモニターにコピー」しておくべき一枚のチャート

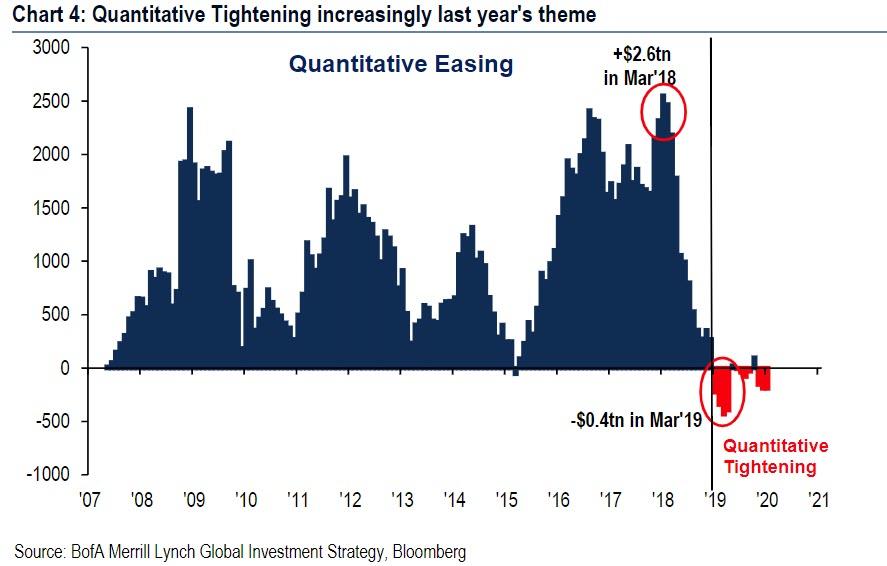

米国はよく理解してませんが、日本の場合では量的緩和で日銀が国債買い上げした資金は日銀当座預金にそのままです、市中には流れていません。でもNHKのニュース等では「ジャブジャブ」という表現をアナウンサーが使い、さらに丁寧に水道の蛇口からお金が吐き出される画像まで示してくれます。これって心理効果が大きいですよね。量的緩和とは何かを7時のニュースや新聞でこれ以上丁寧に解説するのはそう簡単ではありません。一般の人も株式をやっている人も「イメージ」で捉える以上はそう簡単にできません。多くの人は量的緩和とはなにか、を理解していないと私は想像しています。

ただし、国債を買い上げるので長期金利が低下し住宅ローン金利等が下がったのは確実な効果です。一方で長短金利差が少なくなると銀行のビジネスモデルが成り立たなくなりますが。

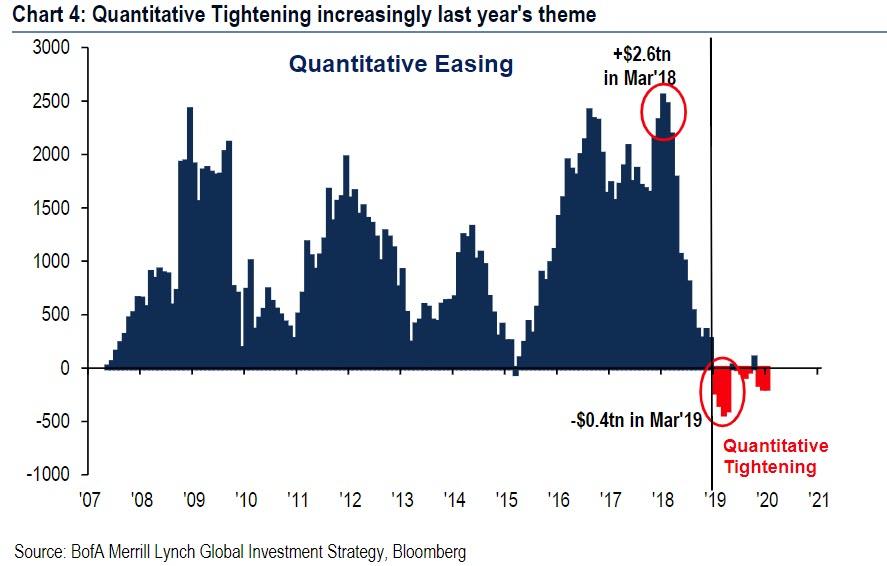

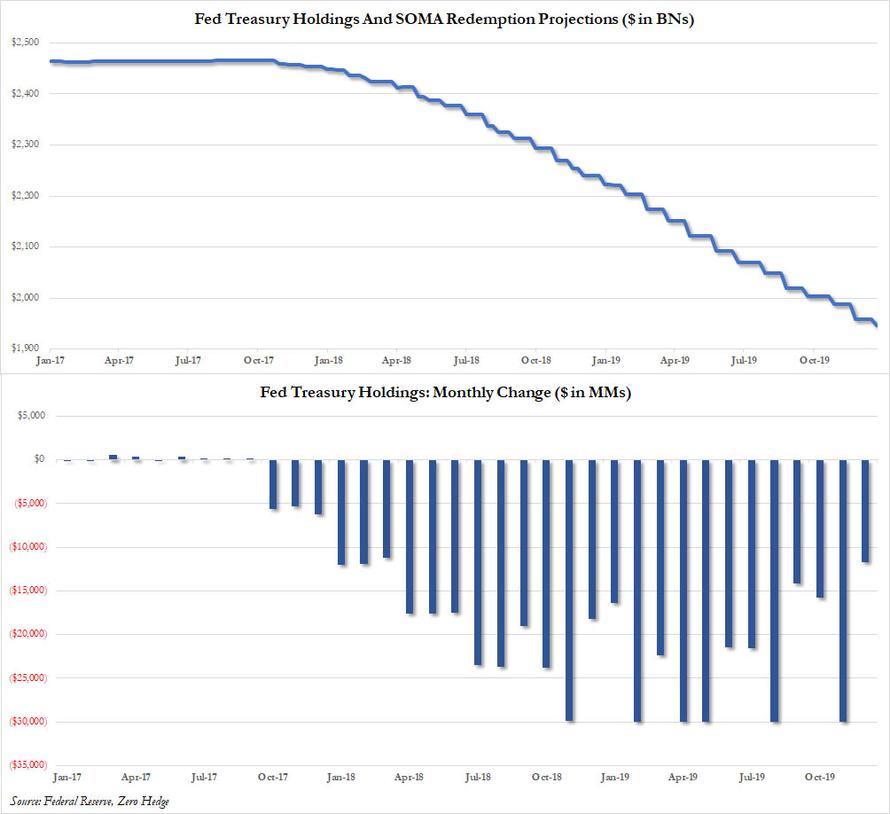

After a year of tapering, the Fed’s balance sheet finally captured the market’s attention during the last three months of 2018.

一年間のテーパリング後、FEDバランスシートがとうとう市場の注目をあびることになった、2018年の最後の3ヶ月だ。

By the start of the fourth quarter, the Fed had finished raising the caps on monthly roll-off of its balance sheet to the full $50bn per month (peaking at $30bn USTs, $20bn MBS, although on many months the B/S does not actually shrink by this full amount which depends on the redemption schedule) and by end-Q4 markets also experienced some of the largest volatility and drawdowns in nearly a decade.

第4四半期が始まり、FEDはとうとうバランスシート縮小を最大の$50B/月とした(米国債を$30B、MBSを$20Bだ)そしてQ4末には市場は最大のボラティリティと10年ぶりの下落を経験した。

As Nomura's George Concalves writes in a Friday letter, whether it was a coincidence or not, broader markets questioned the Fed’s original view that B/S roll-off was going to be like “watching paint dry.” Indeed, recent Fedspeak has shifted to being more open-minded, with Fed policy makers suggesting that they are prepared to be “flexible” in implementing their balance sheet policy.

NomuraのGeorge Concalvesが金曜に書いたことだが、市場参加者の多くがFEDの当初の目論見ようにB/S縮小は「ペンキが乾くように」行われているか疑問をいだいている。たしかに最近のFED言動をみるとより柔軟になっている、FEDの政策立案者が示唆するところでは、バランスシート政策を「柔軟」にする準備をした。

The reason for that is that as both the market and the Fed (and especially Chicago Fed president Charles Evans) were violently reminded, just as QE added liquidity and boosted all asset prices, so QT is draining liquidity from the system. Worse, as Marko Kolanovic wrote in his latest report from Jan 16, given the recent collapse in liquidity and the toxic feedback loop of flows- liquidity-volatility which we discussed last week, "investors are very attentive to monetary policy measures that may affect liquidity."

その理由とは市場とFED双方にある、強烈に覚えているだろうが、QEによる流動性追加ですべての資産を持ち上げた、その後QTでシステムから流動性を取り去りつつある。悪いことに、Marko Kolanovicが書いた1月16日の最新報告書では、最近の流動性急減で悪影響が出ており、これは先週議論した、「投資家は流動性に影響する金融政策に敏感になっている」。

And since the most closely watched metric of systemic liquidity is once again the pace of the Fed’s balance sheet change, and specifically, reduction, Kolanovic notes the recent example of a sharply negative market reaction to the comment that balance sheet reduction (Quantitative Tightening or QT) will be on autopilot (and positive reaction when this statement was later modified). Additionally, even casual remarks on the balance sheet has dramatic and "significantly negative intraday impacts on markets" (such as Powell's recent remarks that the balance sheet should be "substantially smaller").

そして最も注目されている流動性指標はFEDのバランスシート変化だ、特に削減、Kolanovicが言うには、バランスシート縮小(QT)が自動運転だと言われたことが市場にマイナス効果だった(そして後にこの発言を修正したときはプラス効果になった)。更に加えると、なにげないバランスシートに関する発言が劇的にそして「毎日の相場にとても大きなマイナス効果」を与える(たとえば最近のPowellの発言にあったが、バランスシートは「基本的にもっと小さくなるべきだ」というような発言だ)。

But why, Kolanovic asks rhetorically, is there such a focus on the Fed’s balance sheet from investors?

Kolanovicが文字面を追いかけるわけで、どうして投資家はここまでFEDバランスシートに注目するのだろう?

The answer is obvious: by now only clueless hacks will deny that adding liquidity in the form of QE was the single, most important factor driving asset classes higher over the past decade. According to JPMorgan, the impact of QE was ~20% of equity prices (see the bank's report here).

答えは明らかだ:今の所、その場しのぎのQEによる流動性追加は無いと思われている、この10年相場を持ち上げる最重要要因はQEだった。JPMorganによると、QEのインパクトは株価の約20%にもなるという(当行の報告書をここで見るが良い)。

Yet while qualitatively the answer is simple, complications arise when one tries to quantify the impact of the balance sheet shrinkage. Specifically, as the JPM quant notes, the questions investors struggle with are how negative was/will be the impact of the QT, to wit: "It is plausible that dollar for dollar, QT has a significantly larger impact than QE."

ただ、定性的には答えはシンプルだが、バランスシート縮小の効果を定量的に捉えようとすると問題は複雑だ。特に、JPMのアナリストが言うことだが、QTのマイナス効果を定量的に捉えようと投資家は格闘している、見てみよう:「もっともらしく語られるのは、QEよりもQTの方が影響が遥かに大きい」。

The reason for that, according to Kolanovic, has to do that may be the previously discussed fragility feedback loop. During QE, both central banks and investors, and certainly HFTs and algos, would broadly buy assets in an environment of low volatility/ increased liquidity when the impact is small, while during QT "assets are typically sold while liquidity is removed, compounding the negative impact of other outflows."

この理由は、Kolanovicによると、これまでにもこのフィードバックループの脆弱性について議論された。QEの期間には、中央銀行も投資家も、そしてHFTもアルゴリズム売買も、低ボラティリティの中で幅広く資産が買われる、流動性増加のためでインパクトは緩やかだ、一方でQTの期間には「流動性が取り除かれ資産は売られるものだ、これが他の資産にマイナスインパクトを与える。」

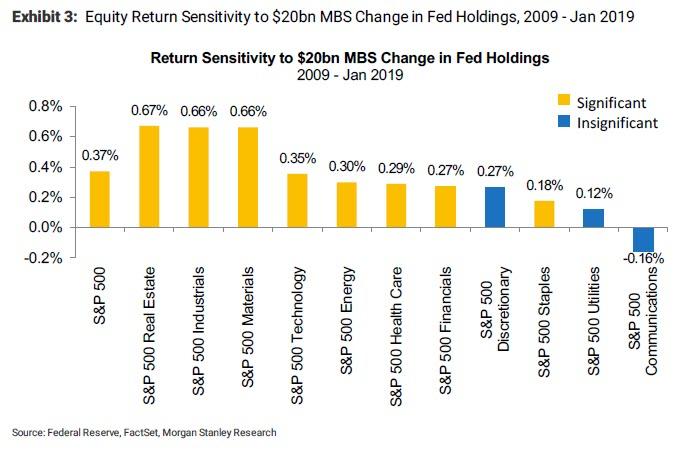

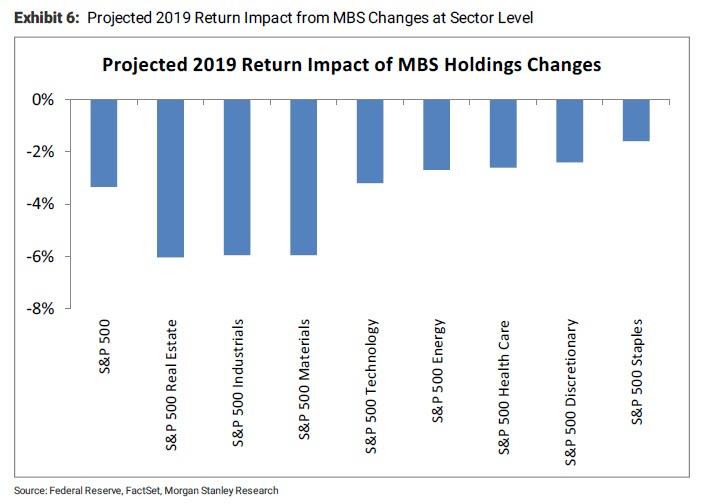

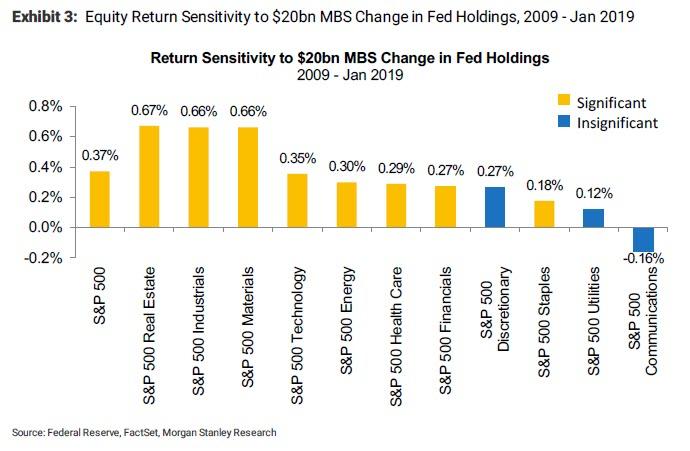

Others have also tried to quantify the impact of QT on risk assets, most recently Morgan Stanley, which last week calculated that every $20 billion decline in Mortgage Backed Securities held by the Fed leads to a 0.37% drop in the S&P (curiously, MS found that S&P 500 returns are not significantly correlated with changes in the Fed's Treasury holdings, although that observations will surely be retested soon).

他にもリスク資産に対するQTのインパクトを量的に捉えようとする人がいる、直近のMorgan Stanleyの報告だ、先週の計算ではFEDが持つMBSが$20B減るごとにS&Pga0.37%下落するという(奇妙なことにMSが言うところではFEDのもつ米国債減少ではS&P500に顕著な影響はないという、ただこの見解もすぐに再検討されるのは確実だ)。

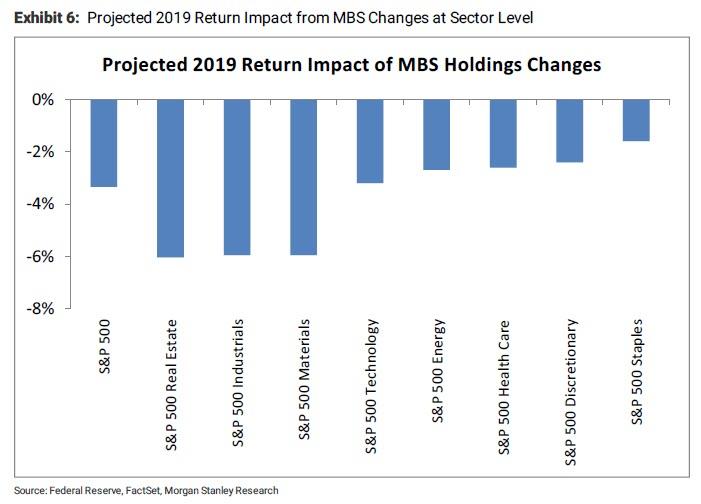

As a result, Morgan Stanley calculates that based on the recent MBS runoff of $15bn per month, the projected S&P 500 return impact is -3.3% for 2019, with the real estate sector hit the hardest.

結果として、Morgan Stanleyの計算は最近の毎月$15BのMBS放出に基づいている、ここから推測されるのは2019年にはS&P500への影響は−3.3%、不動産部門への影響が最も大きい。

Yet while Morgan Stanley believes it may have found the causality link between the Fed's B/S size and its impact on the market, JPM disagrees, and in his note Kolanovic assets that to his knowledge, "there is no broadly accepted understanding of the exact mechanics and magnitude of QT’s impact (e.g., how much it is a signal to the market, vs. mechanical supply/demand and price impact)."

ただ、Morgan StanleyはFEDバランスシートと相場の間の因果関係を見つけたと信じているが、JPMは同意しない、そしてKolanovicによると、「QTのインパクトに関して幅広く受け入れらているメカニズムはない(すなわち、単に市場にシグナルを発しているだけか,

vs. 機械的に需給を通じて価格に影響を与えるか)」。

Instead, he suggests that while there is a significant relationship between the Fed’s balance sheet changes and the market, the big drivers of this relationship are points when the large QE programs were announced such as March 2009 (e.g., when this point is taken out, the relationship no longer appears statistically significant).

そうではなく、彼が示唆するのは、FEDバランスシートと相場に強い相関は在るが、この大きな駆動力は2009年3月にQEプログラムを開始したときにこれを声高に主張したことだ(すなわち、もうこういうことないために相関はそれほど大きくないと)。

In other words, unlike Morgan Stanley's attempt to extrapolate correlation into causation, JPMorgan is more intellectually honest, stating that "whatever the real mechanical impact of QT is, the indirect impact on market sentiment is likely much larger", in other words stocks drop as traders expect QT to drain liquidity and impair stocks, selling in the process and resulting in a self-fulfilling prophecy.

言い換えると、Morgan Stanleyと異なり相関を因果関係と解釈している、JPMorganはもう少し丁寧に主張する、「QTのインパクトに関するメカニズムがどうであれ、間接的に市場心理に影響を与えているわけで、そのこうかはもっと大きなものだ」、言い換えるとQTで流動性がなくなるとトレーダーが予想することで株価は下落する、このプロセスでの売りが自己実現的(下落すると思うから下落する)に機能する。

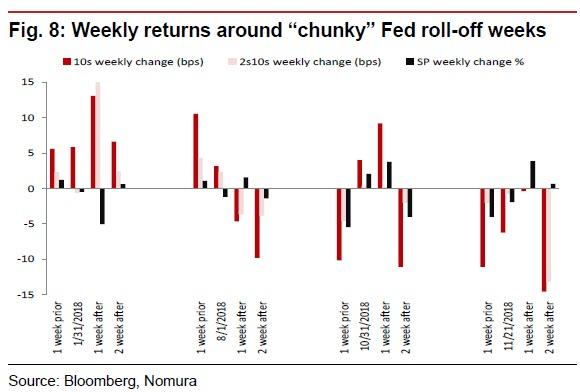

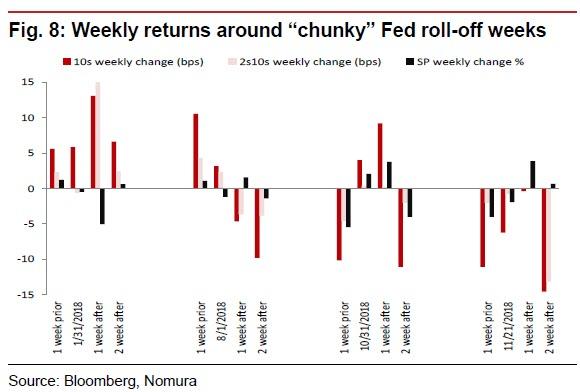

In a somewhat similar analysis, Nomura fixed income strategist George Concalves suggests a compromise option, noting that while his own analysis found little correlation of the smaller balance sheet to the SP500 ("unlike what was seen during the QE days where stocks had an eerie visual relationship to the actual size of the B/S") he did notice weekly B/S changes could be impacting markets.

As an example, he notes that the weeks where MBS holdings were paying down and/or weeks around the time the total size of the roll-off for both UST and MBS exceeded $20bn, markets would come under pressure with the most striking of those periods at the time being the February VIX shock.

これと同様の分析として、Nomuraの金利商品ストラテジストGeorge Concalvesは妥協的な考えを述べる、彼自身の観測ではバランスシート総額が小さいときにSP500との相関は殆ど無い(”QEが始まった当時株式とB/S規模の目に見える相関はあまりなかった”)彼は実際毎週のB/S変化が相場に影響を与えていることに気づいた。その例として彼が主張するのは、MBS保持高が減る週 and / or USTとMBSの満期学が$20Bを超える週には、相場は下落圧力を受ける、これが最も顕著だったのが2月のVIXショックだった。

Additionally, in 2018 there were some “chunky” roll-off and around those weeks there was market volatility and drawdowns (especially in late October and November). To fine tune its analysis, Nomura looked at market performance for a few weeks after large roll-off weeks. It found that while in Feb 2018 it looks like the higher 10yr rates impulse was just as easily the driver of the SP500 declines a couple weeks later, by end-2018 the QT narrative was well entrenched and even then stocks would decline either before or after the larger rolloff periods.

更に加えると、2018年には満期額が「大きな塊」となることが何度かあった、これらの週の前後では市場はボラティリティが大きく相場が下落した(特に10月遅くと11月に顕著だった)。この分析をさらに突き進めると、Nomuraは大きな満期額のあった数週後のパフォーマンスに注目した。この結果わかったのは2018年仁木には10年債の金利が急上昇しその二週後にSP500の下落要因となったが、2018年末にはQTの話が広く知れ渡り、大きな満期額期間であろうとなかろうと株式は下落した。

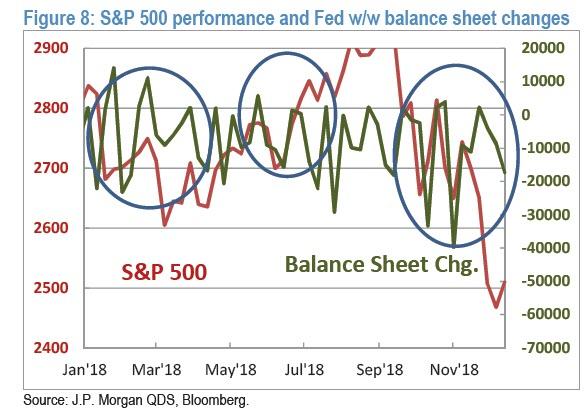

So confirming Kolanovic's view that QT is a self-fulfilling prophecy, Goncalves muses that perhaps "markets were anticipating these moves and discounted them. Meanwhile, going back to Kolanovic's reflexive take on QT and the market, the JPM strategist notes recent intraday movements on balance sheet mentions, as well as the price action of the S&P 500 during Q4 shown in the chart below.

というわけでQTが自己実現的であるというKolanovicの見立てを知った上で、Goncalvesはこういうふうに考える「市場はこういう値動きを懸念しそれを割り引いていた」と。同時に、QTや相場に対するKolanovicの考えを繰り返すと、JPMのストラテジストは最近の値動きをバランスシートの変動と関連付けて見ている、下に示すのはQ4のS&P500のチャートだ。

So what does all this mean for markets?

でこれで相場との関連は?

The answer remains generally unclear, with Nomura concluding that while it believes that "QT is tightening", it is not "straight forward and seems to come in rolling aftershocks of liquidity draining and markets adjusting positions." Meanwhile, the more actue impact of MBS QT on markets "makes sense as those securities are not zero-risk weight (as are USTs) and take up capital and/or need to be a substitutes for other credit products (which impacts FCI)."

答えは、よくわからないままだ、Nomuraは「QTは引き締めだ」と信じる一方で、「債権満期による流動性引き去りと市場調整とのアイアに直接の関連は見られない」。同時に、MBS QTは市場への影響が顕著で「これらの債権はゼロリスクではなく他の与信商品へ置き換えられる必要がある。

Going back to Kolanovic, the JPM quant generally agrees with Nomura, and writes that while there may be little or no mechanical impact on equity prices, most macro traders will not "fight the Fed", meaning when liquidity is added they are buying assets, and when liquidity is removed they are selling assets. Finally, to justify his thesis that QT, for now at least, impacts markets largely as a result of feedback loops and quirks in behavioral finance, Kolanovic also notes that over the past months, "we have heard a large number of anecdotes where investors avoid buying risky assets during (or actively sell into) weeks when there is a significant balance sheet reduction, e.g., traders taping the schedule to their screens, blogs and email chains, etc.."

Kolanovicの主張に戻ると、JPMアナリストはNomuraに同意する、そしてこう主張する、株価にほとんどインパクトはないが、多くのマクロ重視トレーダーは「FEDに逆らう」ことはしないだろう、ということは流動性が加わるとアセットを買い、流動性が引き去られるとアセットを売っている。最終的には、彼の主張を正当化するには、今の所QTの市場へのインパクトは行動金融学におけるフィードバックループの結果だ、Kolanovicもまたすヶ月前にこう書いている、「巨額のバランスシート縮小があると投資家はリスク資産購入を控えるという話は数多く聞かれる、すなわち、トレーダーは自らのPCスクリーン状、ブログ、email等々で目にすることを追いかけている・・・」

JPMorgan's conclusion: whatever the mechanism or sequence of events by which QT affects markets, there is no denying that the shrinking of the Fed's balance sheet does affect the S&P in an adverse way: "balance sheet reductions put significant strain on market sentiment, on flows and on the weakest link in the market – the liquidity-volatility-flow feedback loop. If the balance sheet reduction is a signal to sell, volatility increases, liquidity decreases, and additional systematic flows are triggered." As a result, Kolanovic warns that "balance sheet driven market fragility is thus increasing the risk of market disruptions and ultimately the risk of a recession – which is in contrast to policy makers’ intentions."

JPMorganの結論は:QTが相場に影響するメカニズムや手順がどうであれ、FEDバランスシート縮小がS&Pにマイナス効果を及ぼす:「バランスシート縮小は市場心理におおきな緊張を生み出す、資金移動と相場の最も弱い部分に対してーー流動性ーーボラティリティー資金フローフィードバックループにおいて。もしバランスシート縮小が売りシグナルなら、ボラティリティが増え、流動性が減り、そしてこれらが相乗的に機能してトリガーになる。」その結果、Kolanovicはこう警告する「バランスシートの影響を受ける市場の脆弱性は市場下落リスクを増し、景気後退の大きなリスクだーーこれは政策立案車の意図とは異なる。」

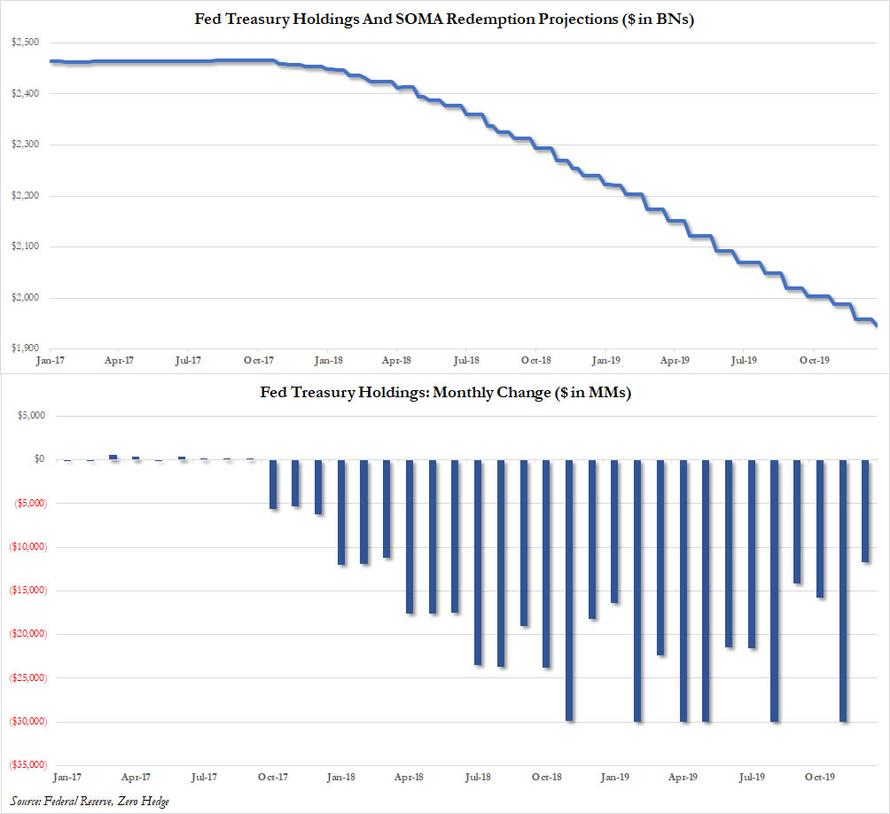

Naturally one can argue this point very easily, and note that if true, then Kolanovic's assessment suggests that absent the Fed's balance sheet, the world would be in a singular depression right now if indeed the modest shrinkage of the Fed's balance sheet from $4.5TN to $3.9TN risked a recession. Consider that there is still another almost $2 trillion to go before the Balance sheet is "renormalized" and one can see why the Fed is not only trapped, but will never be able to renormalize without jeopardizing both the fake market and global economy erected over the past decade on the back of $16 trillion in central bank balance sheet expansion, i.e. liquidity.

当然のことながら、だれでもこのポイントを簡単に指摘できる、そしてこれが正しいなら、Kolanovicの見立てが示唆するのは、FEDバランスシートの議論は抜きにしてもそうななに、FEDバランスシートが$4.5Tから$3.9Tに緩やかに縮小し景気後退リスクにさらされるなら、世界はとても強烈な下落に直面している。バランスシート「正常化」までにはまだ$2Tを縮小するわけで、誰でも解ることだが、FEDは罠に陥っているだけでなく、フェイクマーケットと世界経済を危険に晒すこと無く正常化はできないだろう、過去10年、世界の中央銀行が協力して$16Tものバランスシート拡大・流動性注入で経済を膨れ上がらせたのだから。

But that's a problem for another day.

でも、いつかは問題になる、(今すぐではない)。

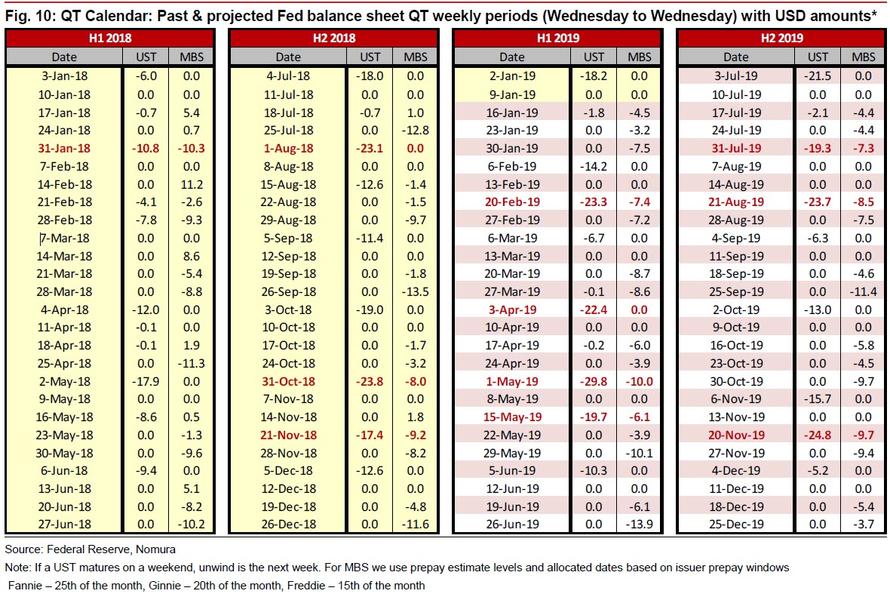

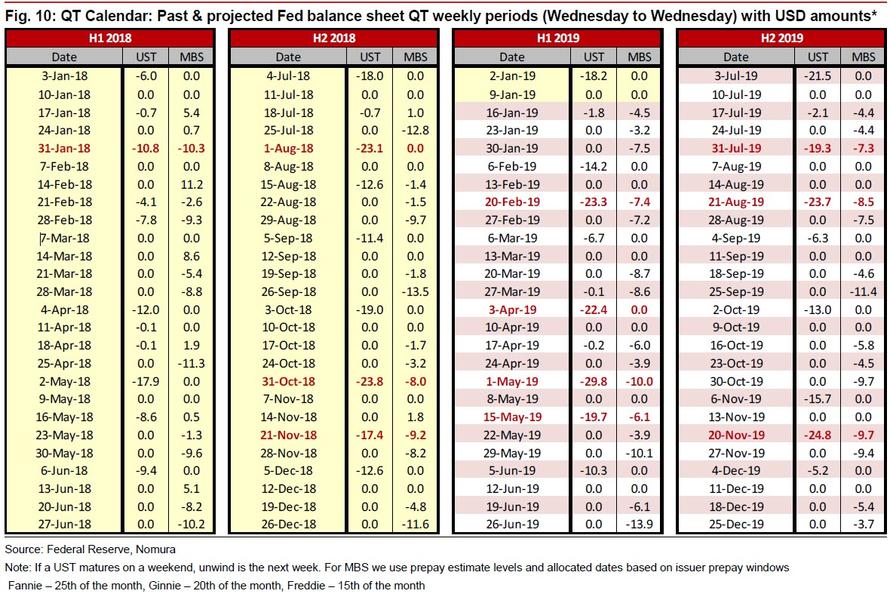

For now, we'll conclude with the schedule that JPMorgan says "traders tape to their screens, blogs and email chains" - the complete QT calendar consisting of past and projected Fed Balance sheet QT periods, courtesy of Nomura's George Goncalves. Needless to say, self-fulfilling prophecy is most likely to be validated during the "dangerous" QT weeks which are highlighted in red, when the Fed's balance sheet shrinks especially aggressively,such as Feb 20, April 3, and May 1 and 15.

今の所、ZeroHedgeの結論としてはJPMorganの言う通り「トレーダーは自らのPCやブログ、多数のeMailでスケジュールを見ている」ーーこれまでそしてこれからのQTに関する完全QTカレンダーを提供しよう、NomuraのGeorge Goncalvesの好意によるものだ。言うまでもないが、self-fulfilling prophecy 自己予言的実現(皆が下がると思うから下がる)が最も起きそうなのは「危険な」QT週間だ、これを赤で強調している。この週にはFEDバランスシート縮小が特に顕著になる、Feb 20, April 3そしてMay 1と15だ。

一年間のテーパリング後、FEDバランスシートがとうとう市場の注目をあびることになった、2018年の最後の3ヶ月だ。

By the start of the fourth quarter, the Fed had finished raising the caps on monthly roll-off of its balance sheet to the full $50bn per month (peaking at $30bn USTs, $20bn MBS, although on many months the B/S does not actually shrink by this full amount which depends on the redemption schedule) and by end-Q4 markets also experienced some of the largest volatility and drawdowns in nearly a decade.

第4四半期が始まり、FEDはとうとうバランスシート縮小を最大の$50B/月とした(米国債を$30B、MBSを$20Bだ)そしてQ4末には市場は最大のボラティリティと10年ぶりの下落を経験した。

As Nomura's George Concalves writes in a Friday letter, whether it was a coincidence or not, broader markets questioned the Fed’s original view that B/S roll-off was going to be like “watching paint dry.” Indeed, recent Fedspeak has shifted to being more open-minded, with Fed policy makers suggesting that they are prepared to be “flexible” in implementing their balance sheet policy.

NomuraのGeorge Concalvesが金曜に書いたことだが、市場参加者の多くがFEDの当初の目論見ようにB/S縮小は「ペンキが乾くように」行われているか疑問をいだいている。たしかに最近のFED言動をみるとより柔軟になっている、FEDの政策立案者が示唆するところでは、バランスシート政策を「柔軟」にする準備をした。

The reason for that is that as both the market and the Fed (and especially Chicago Fed president Charles Evans) were violently reminded, just as QE added liquidity and boosted all asset prices, so QT is draining liquidity from the system. Worse, as Marko Kolanovic wrote in his latest report from Jan 16, given the recent collapse in liquidity and the toxic feedback loop of flows- liquidity-volatility which we discussed last week, "investors are very attentive to monetary policy measures that may affect liquidity."

その理由とは市場とFED双方にある、強烈に覚えているだろうが、QEによる流動性追加ですべての資産を持ち上げた、その後QTでシステムから流動性を取り去りつつある。悪いことに、Marko Kolanovicが書いた1月16日の最新報告書では、最近の流動性急減で悪影響が出ており、これは先週議論した、「投資家は流動性に影響する金融政策に敏感になっている」。

And since the most closely watched metric of systemic liquidity is once again the pace of the Fed’s balance sheet change, and specifically, reduction, Kolanovic notes the recent example of a sharply negative market reaction to the comment that balance sheet reduction (Quantitative Tightening or QT) will be on autopilot (and positive reaction when this statement was later modified). Additionally, even casual remarks on the balance sheet has dramatic and "significantly negative intraday impacts on markets" (such as Powell's recent remarks that the balance sheet should be "substantially smaller").

そして最も注目されている流動性指標はFEDのバランスシート変化だ、特に削減、Kolanovicが言うには、バランスシート縮小(QT)が自動運転だと言われたことが市場にマイナス効果だった(そして後にこの発言を修正したときはプラス効果になった)。更に加えると、なにげないバランスシートに関する発言が劇的にそして「毎日の相場にとても大きなマイナス効果」を与える(たとえば最近のPowellの発言にあったが、バランスシートは「基本的にもっと小さくなるべきだ」というような発言だ)。

But why, Kolanovic asks rhetorically, is there such a focus on the Fed’s balance sheet from investors?

Kolanovicが文字面を追いかけるわけで、どうして投資家はここまでFEDバランスシートに注目するのだろう?

The answer is obvious: by now only clueless hacks will deny that adding liquidity in the form of QE was the single, most important factor driving asset classes higher over the past decade. According to JPMorgan, the impact of QE was ~20% of equity prices (see the bank's report here).

答えは明らかだ:今の所、その場しのぎのQEによる流動性追加は無いと思われている、この10年相場を持ち上げる最重要要因はQEだった。JPMorganによると、QEのインパクトは株価の約20%にもなるという(当行の報告書をここで見るが良い)。

Yet while qualitatively the answer is simple, complications arise when one tries to quantify the impact of the balance sheet shrinkage. Specifically, as the JPM quant notes, the questions investors struggle with are how negative was/will be the impact of the QT, to wit: "It is plausible that dollar for dollar, QT has a significantly larger impact than QE."

ただ、定性的には答えはシンプルだが、バランスシート縮小の効果を定量的に捉えようとすると問題は複雑だ。特に、JPMのアナリストが言うことだが、QTのマイナス効果を定量的に捉えようと投資家は格闘している、見てみよう:「もっともらしく語られるのは、QEよりもQTの方が影響が遥かに大きい」。

The reason for that, according to Kolanovic, has to do that may be the previously discussed fragility feedback loop. During QE, both central banks and investors, and certainly HFTs and algos, would broadly buy assets in an environment of low volatility/ increased liquidity when the impact is small, while during QT "assets are typically sold while liquidity is removed, compounding the negative impact of other outflows."

この理由は、Kolanovicによると、これまでにもこのフィードバックループの脆弱性について議論された。QEの期間には、中央銀行も投資家も、そしてHFTもアルゴリズム売買も、低ボラティリティの中で幅広く資産が買われる、流動性増加のためでインパクトは緩やかだ、一方でQTの期間には「流動性が取り除かれ資産は売られるものだ、これが他の資産にマイナスインパクトを与える。」

Others have also tried to quantify the impact of QT on risk assets, most recently Morgan Stanley, which last week calculated that every $20 billion decline in Mortgage Backed Securities held by the Fed leads to a 0.37% drop in the S&P (curiously, MS found that S&P 500 returns are not significantly correlated with changes in the Fed's Treasury holdings, although that observations will surely be retested soon).

他にもリスク資産に対するQTのインパクトを量的に捉えようとする人がいる、直近のMorgan Stanleyの報告だ、先週の計算ではFEDが持つMBSが$20B減るごとにS&Pga0.37%下落するという(奇妙なことにMSが言うところではFEDのもつ米国債減少ではS&P500に顕著な影響はないという、ただこの見解もすぐに再検討されるのは確実だ)。

As a result, Morgan Stanley calculates that based on the recent MBS runoff of $15bn per month, the projected S&P 500 return impact is -3.3% for 2019, with the real estate sector hit the hardest.

結果として、Morgan Stanleyの計算は最近の毎月$15BのMBS放出に基づいている、ここから推測されるのは2019年にはS&P500への影響は−3.3%、不動産部門への影響が最も大きい。

Yet while Morgan Stanley believes it may have found the causality link between the Fed's B/S size and its impact on the market, JPM disagrees, and in his note Kolanovic assets that to his knowledge, "there is no broadly accepted understanding of the exact mechanics and magnitude of QT’s impact (e.g., how much it is a signal to the market, vs. mechanical supply/demand and price impact)."

ただ、Morgan StanleyはFEDバランスシートと相場の間の因果関係を見つけたと信じているが、JPMは同意しない、そしてKolanovicによると、「QTのインパクトに関して幅広く受け入れらているメカニズムはない(すなわち、単に市場にシグナルを発しているだけか,

vs. 機械的に需給を通じて価格に影響を与えるか)」。

Instead, he suggests that while there is a significant relationship between the Fed’s balance sheet changes and the market, the big drivers of this relationship are points when the large QE programs were announced such as March 2009 (e.g., when this point is taken out, the relationship no longer appears statistically significant).

そうではなく、彼が示唆するのは、FEDバランスシートと相場に強い相関は在るが、この大きな駆動力は2009年3月にQEプログラムを開始したときにこれを声高に主張したことだ(すなわち、もうこういうことないために相関はそれほど大きくないと)。

In other words, unlike Morgan Stanley's attempt to extrapolate correlation into causation, JPMorgan is more intellectually honest, stating that "whatever the real mechanical impact of QT is, the indirect impact on market sentiment is likely much larger", in other words stocks drop as traders expect QT to drain liquidity and impair stocks, selling in the process and resulting in a self-fulfilling prophecy.

言い換えると、Morgan Stanleyと異なり相関を因果関係と解釈している、JPMorganはもう少し丁寧に主張する、「QTのインパクトに関するメカニズムがどうであれ、間接的に市場心理に影響を与えているわけで、そのこうかはもっと大きなものだ」、言い換えるとQTで流動性がなくなるとトレーダーが予想することで株価は下落する、このプロセスでの売りが自己実現的(下落すると思うから下落する)に機能する。

In a somewhat similar analysis, Nomura fixed income strategist George Concalves suggests a compromise option, noting that while his own analysis found little correlation of the smaller balance sheet to the SP500 ("unlike what was seen during the QE days where stocks had an eerie visual relationship to the actual size of the B/S") he did notice weekly B/S changes could be impacting markets.

As an example, he notes that the weeks where MBS holdings were paying down and/or weeks around the time the total size of the roll-off for both UST and MBS exceeded $20bn, markets would come under pressure with the most striking of those periods at the time being the February VIX shock.

これと同様の分析として、Nomuraの金利商品ストラテジストGeorge Concalvesは妥協的な考えを述べる、彼自身の観測ではバランスシート総額が小さいときにSP500との相関は殆ど無い(”QEが始まった当時株式とB/S規模の目に見える相関はあまりなかった”)彼は実際毎週のB/S変化が相場に影響を与えていることに気づいた。その例として彼が主張するのは、MBS保持高が減る週 and / or USTとMBSの満期学が$20Bを超える週には、相場は下落圧力を受ける、これが最も顕著だったのが2月のVIXショックだった。

Additionally, in 2018 there were some “chunky” roll-off and around those weeks there was market volatility and drawdowns (especially in late October and November). To fine tune its analysis, Nomura looked at market performance for a few weeks after large roll-off weeks. It found that while in Feb 2018 it looks like the higher 10yr rates impulse was just as easily the driver of the SP500 declines a couple weeks later, by end-2018 the QT narrative was well entrenched and even then stocks would decline either before or after the larger rolloff periods.

更に加えると、2018年には満期額が「大きな塊」となることが何度かあった、これらの週の前後では市場はボラティリティが大きく相場が下落した(特に10月遅くと11月に顕著だった)。この分析をさらに突き進めると、Nomuraは大きな満期額のあった数週後のパフォーマンスに注目した。この結果わかったのは2018年仁木には10年債の金利が急上昇しその二週後にSP500の下落要因となったが、2018年末にはQTの話が広く知れ渡り、大きな満期額期間であろうとなかろうと株式は下落した。

So confirming Kolanovic's view that QT is a self-fulfilling prophecy, Goncalves muses that perhaps "markets were anticipating these moves and discounted them. Meanwhile, going back to Kolanovic's reflexive take on QT and the market, the JPM strategist notes recent intraday movements on balance sheet mentions, as well as the price action of the S&P 500 during Q4 shown in the chart below.

というわけでQTが自己実現的であるというKolanovicの見立てを知った上で、Goncalvesはこういうふうに考える「市場はこういう値動きを懸念しそれを割り引いていた」と。同時に、QTや相場に対するKolanovicの考えを繰り返すと、JPMのストラテジストは最近の値動きをバランスシートの変動と関連付けて見ている、下に示すのはQ4のS&P500のチャートだ。

So what does all this mean for markets?

でこれで相場との関連は?

The answer remains generally unclear, with Nomura concluding that while it believes that "QT is tightening", it is not "straight forward and seems to come in rolling aftershocks of liquidity draining and markets adjusting positions." Meanwhile, the more actue impact of MBS QT on markets "makes sense as those securities are not zero-risk weight (as are USTs) and take up capital and/or need to be a substitutes for other credit products (which impacts FCI)."

答えは、よくわからないままだ、Nomuraは「QTは引き締めだ」と信じる一方で、「債権満期による流動性引き去りと市場調整とのアイアに直接の関連は見られない」。同時に、MBS QTは市場への影響が顕著で「これらの債権はゼロリスクではなく他の与信商品へ置き換えられる必要がある。

Going back to Kolanovic, the JPM quant generally agrees with Nomura, and writes that while there may be little or no mechanical impact on equity prices, most macro traders will not "fight the Fed", meaning when liquidity is added they are buying assets, and when liquidity is removed they are selling assets. Finally, to justify his thesis that QT, for now at least, impacts markets largely as a result of feedback loops and quirks in behavioral finance, Kolanovic also notes that over the past months, "we have heard a large number of anecdotes where investors avoid buying risky assets during (or actively sell into) weeks when there is a significant balance sheet reduction, e.g., traders taping the schedule to their screens, blogs and email chains, etc.."

Kolanovicの主張に戻ると、JPMアナリストはNomuraに同意する、そしてこう主張する、株価にほとんどインパクトはないが、多くのマクロ重視トレーダーは「FEDに逆らう」ことはしないだろう、ということは流動性が加わるとアセットを買い、流動性が引き去られるとアセットを売っている。最終的には、彼の主張を正当化するには、今の所QTの市場へのインパクトは行動金融学におけるフィードバックループの結果だ、Kolanovicもまたすヶ月前にこう書いている、「巨額のバランスシート縮小があると投資家はリスク資産購入を控えるという話は数多く聞かれる、すなわち、トレーダーは自らのPCスクリーン状、ブログ、email等々で目にすることを追いかけている・・・」

JPMorgan's conclusion: whatever the mechanism or sequence of events by which QT affects markets, there is no denying that the shrinking of the Fed's balance sheet does affect the S&P in an adverse way: "balance sheet reductions put significant strain on market sentiment, on flows and on the weakest link in the market – the liquidity-volatility-flow feedback loop. If the balance sheet reduction is a signal to sell, volatility increases, liquidity decreases, and additional systematic flows are triggered." As a result, Kolanovic warns that "balance sheet driven market fragility is thus increasing the risk of market disruptions and ultimately the risk of a recession – which is in contrast to policy makers’ intentions."

JPMorganの結論は:QTが相場に影響するメカニズムや手順がどうであれ、FEDバランスシート縮小がS&Pにマイナス効果を及ぼす:「バランスシート縮小は市場心理におおきな緊張を生み出す、資金移動と相場の最も弱い部分に対してーー流動性ーーボラティリティー資金フローフィードバックループにおいて。もしバランスシート縮小が売りシグナルなら、ボラティリティが増え、流動性が減り、そしてこれらが相乗的に機能してトリガーになる。」その結果、Kolanovicはこう警告する「バランスシートの影響を受ける市場の脆弱性は市場下落リスクを増し、景気後退の大きなリスクだーーこれは政策立案車の意図とは異なる。」

Naturally one can argue this point very easily, and note that if true, then Kolanovic's assessment suggests that absent the Fed's balance sheet, the world would be in a singular depression right now if indeed the modest shrinkage of the Fed's balance sheet from $4.5TN to $3.9TN risked a recession. Consider that there is still another almost $2 trillion to go before the Balance sheet is "renormalized" and one can see why the Fed is not only trapped, but will never be able to renormalize without jeopardizing both the fake market and global economy erected over the past decade on the back of $16 trillion in central bank balance sheet expansion, i.e. liquidity.

当然のことながら、だれでもこのポイントを簡単に指摘できる、そしてこれが正しいなら、Kolanovicの見立てが示唆するのは、FEDバランスシートの議論は抜きにしてもそうななに、FEDバランスシートが$4.5Tから$3.9Tに緩やかに縮小し景気後退リスクにさらされるなら、世界はとても強烈な下落に直面している。バランスシート「正常化」までにはまだ$2Tを縮小するわけで、誰でも解ることだが、FEDは罠に陥っているだけでなく、フェイクマーケットと世界経済を危険に晒すこと無く正常化はできないだろう、過去10年、世界の中央銀行が協力して$16Tものバランスシート拡大・流動性注入で経済を膨れ上がらせたのだから。

But that's a problem for another day.

でも、いつかは問題になる、(今すぐではない)。

For now, we'll conclude with the schedule that JPMorgan says "traders tape to their screens, blogs and email chains" - the complete QT calendar consisting of past and projected Fed Balance sheet QT periods, courtesy of Nomura's George Goncalves. Needless to say, self-fulfilling prophecy is most likely to be validated during the "dangerous" QT weeks which are highlighted in red, when the Fed's balance sheet shrinks especially aggressively,such as Feb 20, April 3, and May 1 and 15.

今の所、ZeroHedgeの結論としてはJPMorganの言う通り「トレーダーは自らのPCやブログ、多数のeMailでスケジュールを見ている」ーーこれまでそしてこれからのQTに関する完全QTカレンダーを提供しよう、NomuraのGeorge Goncalvesの好意によるものだ。言うまでもないが、self-fulfilling prophecy 自己予言的実現(皆が下がると思うから下がる)が最も起きそうなのは「危険な」QT週間だ、これを赤で強調している。この週にはFEDバランスシート縮小が特に顕著になる、Feb 20, April 3そしてMay 1と15だ。