“So, if the housing market isn’t going to affect the economy, and

low interest rates are now a permanent fixture in our society, and

there is NO risk in doing anything because we can financially engineer

our way out it – then why are all these companies building up

departments betting on what could be the biggest crash the world has

ever seen? What is more evident is what isn’t being said. Banks

aren’t saying “we are gearing up just in case something bad happens.”

Quite the contrary – they are gearing up for WHEN it happens. When the turn does come, it will be unlike anything we

have ever seen before. The scale of it could be considerable because of

the size of some of these leveraged deals.” – Lance Roberts, June 2007

It is often said that no one saw the crash coming. Many did, but since it was “bearish” to discuss such things, the warnings were readily dismissed.

Of course, what came next was the worst financial crisis since the “Great Depression.” よく言われることだがだれも暴落が来るとは思っていない。多くの場合そうだった、しかそういう議論をすること自身が「弱気」だからこそ、そういう警告は無視された。当然のことながら、これから来る最悪の金融危機は「大恐慌」以来のものだ。

But that was a decade ago, the pain is a relic of history, and the

surging asset prices due to monetary policies has once again lured both

Wall Street and Main Street into the warm bath of complacency.

It should not be surprising warnings are once again falling on “deaf ears.”

The latest warning came from the Federal Reserve who identified rising sales of risky corporate debt as a top vulnerability facing the U.S. financial system in their latest financial stability report. Via WSJ:

“Officials, for the second time in six months, cited

potential risks tied to nonfinancial corporate borrowing, particularly

leveraged loans—a $1.1 trillion market that the Fed said grew by 20%

last year amid declining credit standards. They also flagged possible concerns in elevated asset prices and historically high debt owned by U.S. businesses. Monday’s report also identified potential economic shocks that could test the stability of the U.S. financial system, including

trade tensions, potential spillover effects to the U.S. from a messy

exit of Britain from the European Union and slowing economic growth

globally. Specifically, the Fed warned a downturn could expose

vulnerabilities in U.S. corporate debt markets, ‘including the rapid

growth of less-regulated private credit and a weakening of underwriting

standards for leveraged loans.’”

It has become quite commonplace to dismiss the current environment under the thesis of “this time is different.”This was also the case in 2007 where the general beliefs were exactly the same:

現在の環境を「this time is different.」として無視するのが一般的だ。この状況は2007年とよく似ている、当時多くの人は同様に感じていた:

Low interest rates are expected to persist indefinitely into the future, 低金利がずっと続くと信じていた。

A pervasive belief that Central Banks have everything under control, and; 中央銀行がすべてを制御できると広く信じられていた;

The economy is strong and there is “no recession” in sight. 経済は強く、「景気後退など全く視野になかった」。

Remember, even though no one knew it at the time, the recessions officially started just 5-months later.

The issue of “zombie corporations,” or companies that would

be bankrupt already if not for ongoing low interest rates and loose

lending standards, is not a recent issue. Via Zerohedge:

“As Bloomberg reports, in a particularly striking sign,

the Fed said the businesses with the biggest existing debt loads are

also the ones taking on the riskiest loans. And protections that lenders include in loan documents in case borrowers default are eroding, the

U.S. central bank said in its twice-a-year financial stability report.

The Fed board voted unanimously to approve the document. ‘Credit standards for new leveraged loans appear to have deteriorated further over the past six months,’ the Fed said, adding that the loans to firms with especially high debt now exceed earlier peaks in 2007 and 2014.

‘The historically high level of business debt and the recent

concentration of debt growth among the riskiest firms could pose a risk

to those firms and, potentially, their creditors.’

Leveraged loans are routinely packaged into collateralized loan obligations, or CLOs. Investors

in those securities — including insurance companies and banks — face a

risk that strains in the underlying loans will deliver ‘unexpected

losses,’ the Fed said Monday, adding that the secondary market isn’t very liquid, “even in normal times.”

And it was the Central Bank’s largesse that led to the latest bubble. As noted by WSJ:

そしてこれは中央銀行の気前良さで膨らんだバブルだ。WSJはこう記す:

“Financial stability has remained a central focus at the Fed

because of the easy-money policies employed to nurse the economy back to

health in the years following the financial crisis. Critics have warned

that the Fed’s large bond-buying campaigns and years of near-zero

interest rates risked new bubbles.”

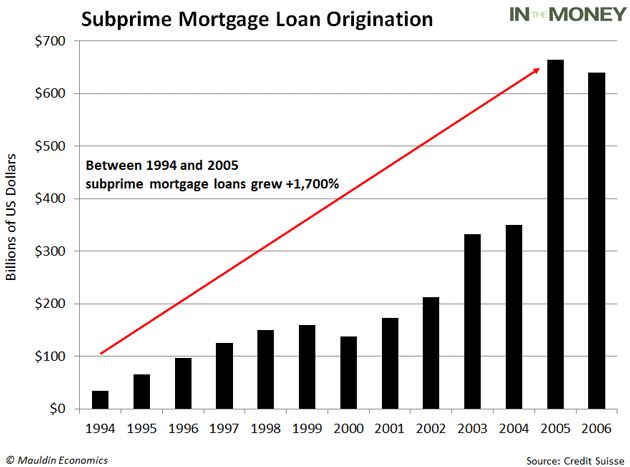

One of the common misconceptions in the market currently, is that the

“subprime mortgage” issue was vastly larger than what we are talking

about currently.

Not by a long shot. 決してそうではない。

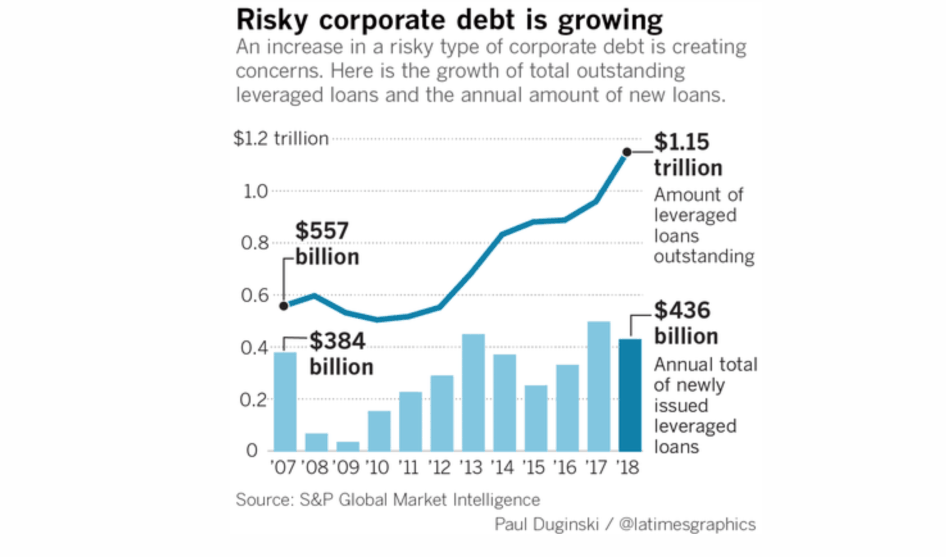

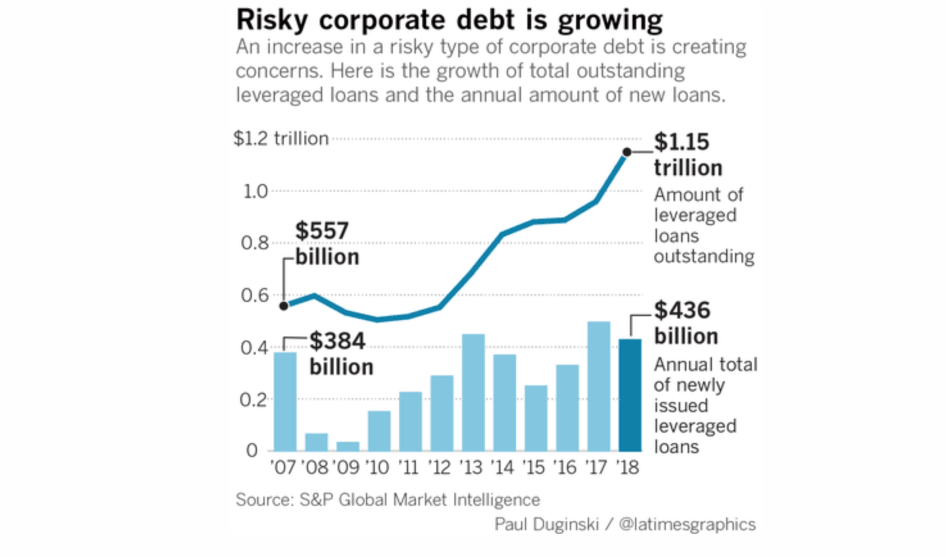

Combined, there is about $1.15 trillion in outstanding U.S. leveraged loans — a record that is double the level five years ago — and, as noted, these loans increasingly are being made with less protection for lenders and investors.

Just to put this into some context, the amount of sub-prime mortgages peaked slightly above $600 billion or about 50% less than the current leveraged loan market. この状況をこういう視点で見てみよう、サブプライムローンはその絶頂期には$600Bを少し超えていた、これは現在のレバレッジドローン市場の50%にも満たない。

Of course, that didn’t end so well.

当然のことながら、サブプライムローンの結末は不味いものだった。

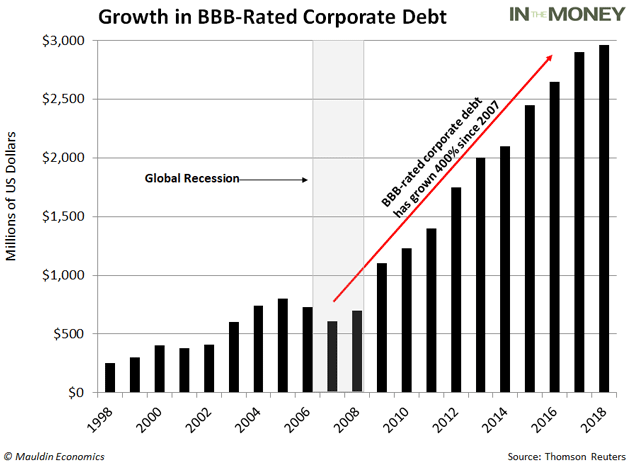

Currently, the same explosion in low-quality debt is happening in another corner of the US debt market as well. 現在のところ、低格付け債務が前回同様に爆発的に増えており、前回と同様に米国債務市場が曲がり角に到達している。

As noted by John Mauldin:

John Mauldinに言わせるとこういう具合だ:

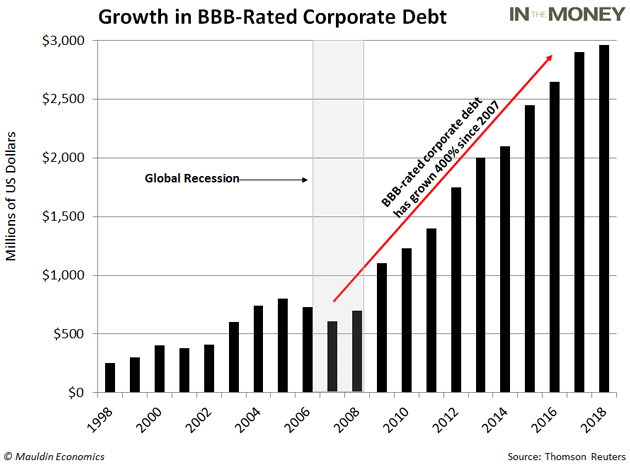

“In just the last 10 years, the triple-B bond market has exploded from $686 billion to $2.5 trillion—an all-time high.

「わずか過去10年で、BBB債券市場は$686Bから$2.5Tへと爆発的に増えーー今過去最高だ。

To put that in perspective, 50% of the investment-grade bond market now sits on the lowest rung of the quality ladder.

これを見通してみると、投資適格債券市場の50%が今や最低格付けBBBとなっている。

And there’s a reason BBB-rated debt is so plentiful. Ultra-low

interest rates have seduced companies to pile into the bond market and

corporate debt has surged to heights not seen since the global financial

crisis.”

As the Fed noted a downturn in the economy, signs of which we are

already seeing, a significant correction in the stock market, or a rise

in interest rates could quickly cause problems in the corporate bond

market. The biggest risk currently is refinancing the debt. As Frank

Holmes noted in a recent Forbes article, the outlook is rather grim.

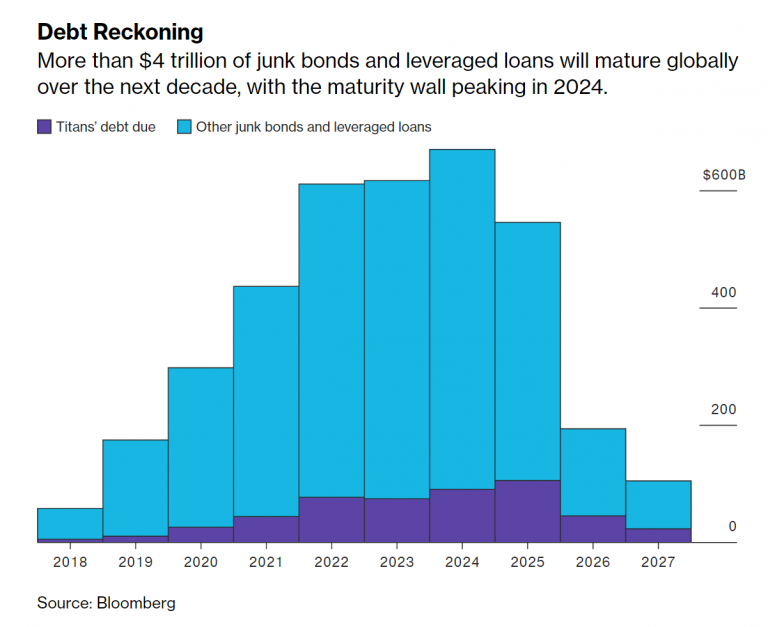

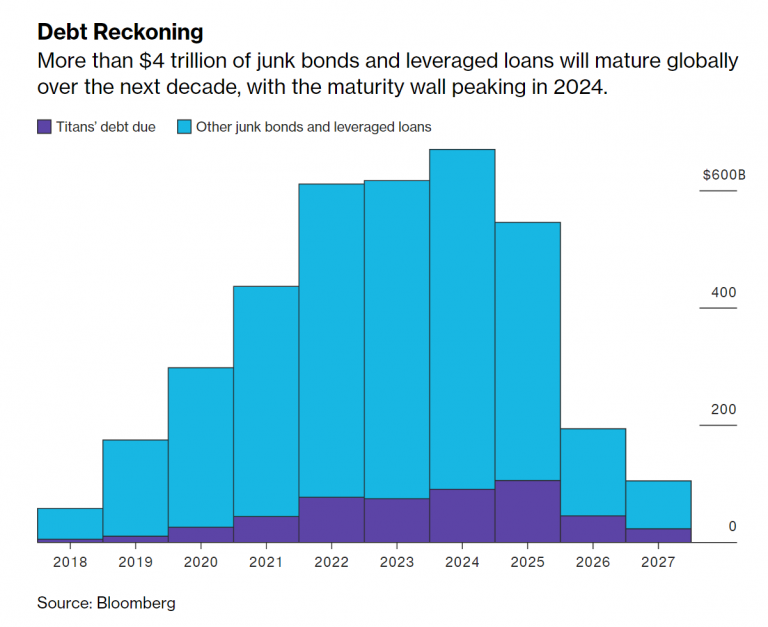

“Through 2023, as much as $4.88 trillion of this debt is

scheduled to mature. And because of higher rates, many companies are

increasingly having difficulty making interest payments on their debt,

which is growing faster than the U.S. economy, according to the

Institute of International Finance (IIF).

“On top of that, the very fastest-growing type of debt is riskier

BBB-rated bonds — just one step up from ‘junk.’ This is literally the

junkiest corporate bond environment we’ve ever seen. Combine this with

tighter monetary policy, and it could be a recipe for trouble in the

coming months.”

「これに加えて、急激に増えている債権はBBB格付けだーー位置段階下がると「ジャンク」となる。これは文字通り紙くず企業債権だ。金融引き締め政策と重なり、今後数ヶ月で問題を引き起こすだろう。」

Let that sink in for a minute.

詳しく分析してみよう。

Over the next 5-years, more than 50% of the debt is maturing. As noted, a weaker economy, recession risk, falling asset

prices, or rising rates could well lock many corporations out of

refinancing their share of this $4.88 trillion debt. Defaults will move

significantly higher, and much of this debt will be downgraded to junk. 今後5年で債務の50%は満期を迎える。 上にも書いたが、弱い経済、景気後退リスク、株価下落、もしくは金利上昇が多くの企業の借り換えを難しくするだろう、債務は$4.88Tもあるのだ。倒産が目に見えて増えるだろう、そしてこれらの債務の多くはジャンクに格下げされることだろう。

As noted by James Grant in a recent interview:

James Grantは最近のインタビューでこう述べた:

“Many companies will get into trouble if the real interest rate

on ten-year treasuries rises over 1%. These businesses are so leveraged

that they can’t cover their debt payments at levels even as humble and

as low as a 1% real interest rate on ten-year treasuries as it

translates into corporate borrowing. Just look at the growth in

the herd of listed zombies; companies whose average operating income has

fallen short of covering the average interest rate expense over three

consecutive years. As it turns out, the corporate living dead,

as a share of the broad S&P 1500 index, are close to 14%. Former

Fed-Chairman Ben Bernanke once tried to reassure everyone that the Fed

could raise rates in 15 minutes if it wanted to. Well, it turns out the

Fed cannot do that. So, it’s a brave new world we’re living in.”

Nonbank lending, an industry that played a central role

in the financial crisis, has been expanding rapidly and is still posing

risks should credit conditions deteriorate.

Often called ‘shadow banking’ — a term the industry does not

embrace — these institutions helped fuel the crisis by providing lending

to underqualified borrowers and by financing some of the exotic

investment instruments that collapsed when subprime mortgages fell

apart.

This kind of lending has absolutely exploded all over the globe since the last recession, and it has now become a $52 trillion dollar bubble. 前回の景気後退以来世界中でこの手の貸出が爆発的に増えている、今やその規模は$52Tのバブルに膨れ上がっている。

In the years since the crisis, global shadow banks have seen

their assets grow to $52 trillion, a 75% jump from the level in 2010,

the year after the crisis ended. The asset level is through 2017,

according to bond ratings agency DBRS, citing data from the Financial

Stability Board.

The real crisis comes when there is a “run on pensions.” With

a large number of pensioners already eligible for their pension, and a

$5 trillion dollar funding gap, the next decline in the markets will

likely spur the “fear” that benefits will be lost entirely. 本当の危機がやって来るのは「年金基金枯渇」のときだ。多くの年金受給者が年金基金に頼っている、しかしそこには$5Tの資金不足がある、次の相場下落では年金受給が全くなくなるのではという「恐怖」に拍車を掛けるだろう。

The combined run on the system, which is grossly underfunded, at a

time when asset prices are dropping, credit is collapsing, and

shadow-banking freezes, the ensuing debacle will make 2008 look like mild recession.

It is unlikely Central Banks are prepared for, or have the monetary capacity, to substantially deal with the fallout.

“There is no way you ever emerge from eight years of free money

without a debt bubble. If it’s not a LatAm cycle, then it’s energy the

next, commercial real estate after that, a tech mania years after, and

then the mother of all of them, housing over a decade ago. This time there is a huge bubble on corporate balance sheets and a price will be paid. It’s just a matter of when, not if.”

Never before in human history have we seen so much debt. Government

debt, corporate debt, shadow-banking debt, and consumer debt are all at

record levels. Not just in the U.S., but all over the world.

If you are thinking this is a “Goldilocks economy,” “there is no recession in sight,” “Central Banks have this under control,” and that “I am just being bearish,” you would be right.

Class 8 Heavy Truck Orders Crash 68% in January by Tyler Durden Wed, 02/06/2019 - 17:25 Among the latest dismal news about the strength of the US economy, on Tuesday ACT Research released preliminary truck orders for January 2019 which showed that Class 8 truck orders collapsed an astounding 68% for January. The decline is being attributed to a 300,000+ vehicle backlog potentially prompting fleets to halt purchases in the near term. 米国経済に関し最近憂鬱なニュースが多い中で、火曜にACT researchが2019年1月のトラック発注を開示した、1月にClass 8のトラック発注がなんと68%も急落した。この発注減は短期的に300,000台超の潜在在庫を生み出す。 Specifically, in January Class 8 net orders were 15,800 units (14,700 SA; 176,400 SAAR), down 68% YoY and down 26% MoM. Class 5- 7 January net orders were 23,400...

Amazonで買物をしてContrarianJを応援しよう Silver Outperforming Gold 2 Adam Hamilton July 26, 2019 3232 Words Silver has blasted higher in the last couple weeks, far outperforming gold. This is certainly noteworthy, as silver has stunk up the precious-metals joint for years. This deeply-out-of-favor metal may be embarking on a sea-change sentiment shift, finally returning to amplifying gold’s upside. Silver is not only radically undervalued relative to gold, but investors are aggressively buying. Silver’s upside potential is massive. ここ2週シルバーは急騰した、ゴールドを遥かに凌ぐものだ。これは注目すべきことだ、もう何年もシルバーはひどいものだった。この極端に嫌われた金属が大きく心理を買えている、とうとうゴールド上昇を増幅するに至った。シルバーは対ゴールドで極端に過小評価されているだけでなく、投資家は積極的に買い進んでいる。シルバーの潜在上昇力は巨大なものだ。 Silver’s performance in recent years has been brutally bad, repelling all but the most fanatical contrarians. Historically silver prices have been mostly ...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...

中国が債務増加していることはたしかです。ただ日本の例を日銀資金循環報告でみると家計、320兆円、民間非金融機関1,785兆円、一般政府 1,284兆円となります。合算すると3,300兆円にもなり、GDPの600%を超えています。 https://www.boj.or.jp/statistics/sj/sjexp.pdf この記事の統計と同じ考え方で数値を採用しているのかどうか気になります。 加えて、この資金循環報告に書かれている海外資産というのが内数なのか外数なのか?私にはよくわかりません。当然海外債務も結構な額になります。一度日銀資金循環 図表1を見てください。詳しい方に教えていただければ。 この中国のたどる道は昔のソ連とかMMTと同様で、自国通貨ならいくら発行しても倒産はしない、というか為政者が痛みに耐えることができず緩和を続けるというものです。でも最終的には限界点に達します。ソ連は建国から崩壊まで70年かかりました。 自由主義経済なら立ち行かなくなった企業は退場してもらうというのが減速なのですが、これがうまくゆかないわけです。 でも日本は中国のはるか先を言っているように見えます。ちょっと検索したのですが、日本の債務に関しては政府債務に言及したものばかりで、この記事のように民間、個人まで総合的に記載しているのは日銀の資金循環統計しか見つけることができませんでした。 China Continues To Pile Debt On Top Of More Debt Written by Jesse Colombo | Feb, 27, 2019 Like many countries, China attempted to rein in its debt growth over the past couple years, but ultimately gave up and is now back to piling on even more debt. Bloomberg reports – 多くの国と同様に、中国もここ2年ほど債務増加を抑えようとしてきた、しかし結局の所諦めてしまい、今や更に債務を積み上げている。ブルームバーグ記事ーー For almost two years,...