生産性:これはどういうものか&どうしてこれが問題か

Productivity: What It Is & Why It Matters

Written by Michael Lebowitz | Jan, 16, 2019

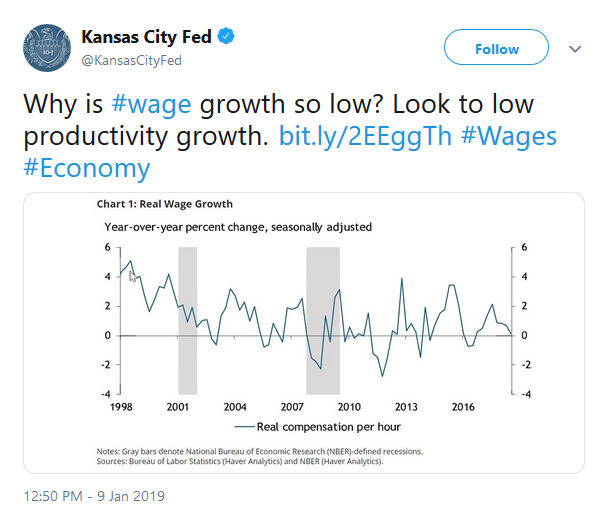

The Kansas City Federal Reserve posted the Twitter

comment and graph below highlighting a very important economic theme.

Although productivity is a basic building block of economic analysis, it

is one that few economists and even fewer investors seem to appreciate.

Kansas 市FEDがツイッターにコメントを投稿した、そのグラフを下に示す、とても重要な経済テーマだ。経済分析においては生産性というのはとても重要な要素だが、ほとんどのエコノミストがこの件に言及しない、投資家は更にこのことを忘れ去っている。

The Kansas City Fed’s tweet is 100% correct in that wages are stagnating in large part due to low productivity growth. As the second chart shows, it is not only wages. The post financial-crisis economic expansion, despite being within months of a record for duration, is by far the weakest since WWII.

Kansas City FEDのツイートは100%正しい、給与が停滞している原因の主要因は生産性成長が低いからだ。二番目のチャートを見ても判るように、成長鈍化は給与だけではない。あの金融危機後の経済拡大は、第二次世界大戦後で記録的長期の拡大期間だが、とても弱い拡大だ。

Productivity growth over the last 350+ years is what allowed America to grow from a colonial outpost into the world’s largest and most prosperous economic power. Productivity is the chief long-term driver of corporate profitability and economic growth. Productivity drives investment returns whether we recognize it or not.

過去350年超の生産性成長で米国は植民地から世界最大の繁栄経済を生み出してきた。長期的に見れば生産性こそが企業収益や経済成長の駆動力だ。生産性こそが投資リターンを生み出すものだ、我々がこれを認めようが認めまいが。

Despite its foundational importance to the economy, productivity is not well understood. There is no greater proof than the hordes of Ivy League trained PhD’s at the Federal Reserve who have promoted extremely easy monetary policy for decades. It is this policy which has sacrificed productivity at the altar of consumption and short-term economic gains.

経済に対してとても重要なことなのだが、生産性は十分に理解されていない。アイビーリーグでPh.DをとりFEDで働く人達も理解が十分でない、彼らは何十年に渡り極端な金融緩和策を推進してきた。消費や短期的な経済成長のために彼らは生産性を犠牲にしてきた。

For more on the interaction between monetary policy and economic growth please read Wicksell’s Elegant Model.

金融政策と経済成長の関係にもっと起用味があるならこの記事を読むが良い、Wicksell's Elegant Model。

Economic growth is a direct function of productivity which measures

the amount of leverage an economy can generate from its two primary

inputs, labor and capital. Without productivity, an economy is solely

reliant on the two inputs. Due to the limited nature of both labor and

capital, they cannot be depended upon to produce durable economic growth

over long periods of time.

経済成長は生産性を直接反映するものだ、この生産性は2つのインプトットから生み出される、労働と資本だ、これが結果として経済をレバレッジ成長させる。生産性無くしても、経済はこの2つの入力に依存している。労働、資本ともに限度があるために、長期に渡り十分な経済成長をすることはできない。

Leveraging labor and capital, or becoming more productive, provides the dynamism to an economy. Unfortunately, productivity requires work, time, and sacrifice. It’s a function of countless factors including innovation, education, government policies, and financial incentives.

労働と資本をレバレッジ、もしくはさらなる生産物を得るために、経済にダイナミクスを与える。残念なことに、生産性には、労働、時間そして犠牲が必要だ。そこには無数の要因がある、革新、教育、政策、そして金融インセンティブ。

Labor 労働

Labor, or human capital, is largely a function of the demographic makeup of an economy and its employees’ skillset and knowledge base. In the short run, increasing labor productivity is difficult. Realizing changes to skills training and education take time but they do have meaningful effect. Similarly, changes in birth rate patterns require decades to influence an economy.

労働、もしくは人的資本、これは経済を支える人工動体によるところが大きい、さらには労働者の熟練度と知識ベースだ。短期的に労働生産性を向上するのは難しい。労働習熟訓練や教育変革を実現するには時間を要し、しかもかなりな努力を要する。同様に経済に影響するほどに出生率を改善するには何十年とかかる。

Within the labor force, the biggest trend affecting current and future economic activity, both domestic and globally, is the so called “silver tsunami”, or the aging of the baby boomers. This outsized cohort of the population, ages 55 to 73 are beginning to retire at ever greater rates. As this occurs, they tend to consume less, rely more on financial support from the rest of the population, and withdraw valuable skills and knowledge from the workforce. The vast number of people in this demographic cohort makes this occurrence more economically damaging than usual. As an example, the old age dependency ratio, which measures the ratio of people aged greater than 65 to the working population ages 18-64, is expected to nearly double by the year 2035 (Census Bureau).

現在と将来の経済に影響する世界的トレンドは、いわゆる「高齢化の津波」だ、もしくは団塊の世代の高齢化。この人口分布の中でとても大きな割合を占める、55歳から73歳の人たちの引退速度がかつてない速さですすんでいる。これにともない、消費は落ち込み、他の世代の人の資金援助を必要としている、そして労働力から貴重なスキルや知識が失われている。人口動態のなかでのこのとても大きな割合の世代がいつも以上に経済にダメージを与えている。たとえば、高齢化率が高まると、18−64人口に対する65以上以上人口が2035年には倍になると見られている(統計局調べ)。

While the implications of changes in demographics and the workforce composition are numerous, they only require one vital point of emphasis: the significant economic contributions attributable to the baby boomers from the last 30+ years will diminish from here forward. As they contribute less, they will also require a higher allotment of financial support, becoming more dependent on younger workers.

人口動態変化や労働力構成は大きいものの、強調すべきことが一つ在る:過去30年超経済成長に大きく寄与してきた団塊の世代が今後は消えてゆくだろう。彼らの寄与は小さくなり、より大きな金融支援が必要となるだろう、より若い労働力への依存度が高くなる。

Finally, immigration is also an important component in the labor force equation. Changes in immigration policies and laws are easier to amend to foster more immediate growth but political dynamics argue that pro-immigration policies and laws are not likely within the next few years.

最後に、労働力問題では移民は重要な構成要素だ。移民を多く受け入れるには政策や法整備が必要だ、しかし政策転換や法整備が今後数年で実現しそうにない。

資本とは当然ながら、人工的なもので金融資源だ。過去30年超にわたり、米国経済は資本増加の恩恵を受けてきた、特に債務だ。債務増加、これが資本の大きな割合を占めるが、これをセクター別に示している。この増加は全くすごいもので、経済活動の増加はこれに比べると穏やかなものだ(黒線)

This divergence in debt and economic growth is a result of many consecutive years of borrowing funds for consumptive purposes and the misallocation of capital, both of which are largely unproductive endeavors. In hindsight we know these actions were unproductive as highlighted by the steadily rising ratio of debt to GDP shown above. The graph below tells the same story in a different manner, plotting the amount of debt required to generate $1 of economic growth. Simply, if debt were used for productive activities, economic growth would have risen faster than debt outstanding.Data Courtesy: Bloomberg, St. louis Federal Reserve

この債務と経済成長の乖離は消費のための多額の借金と資本の誤配分が長年続いたためだ、どちらも生産的ではない努力だ。後知恵だが、対GDPの債務割合が増えていることで、これは生産的でないことが解る。下のグラフは同じ状況を別の視点で示している、$1の経済成長に必要な債務の量だ。簡単に言うと、債務が生産的活動に使われるなら、経済成長は債務残高よりも経済成長のほうが大きいはずだ。

Data Courtesy: Bloomberg, St. Louis Federal Reserve

1980年以来、長期的な生産性の平均成長率は年率0−2%と停滞している、第二次世界大戦後30年間の生産性成長率4−6%だが、これから急速に後退している。生産性の明確な定義は無いが、total factore productivity(TFP)は最良の指標の一つと見られている。TFPはサンフランシスコFEDが算出している。

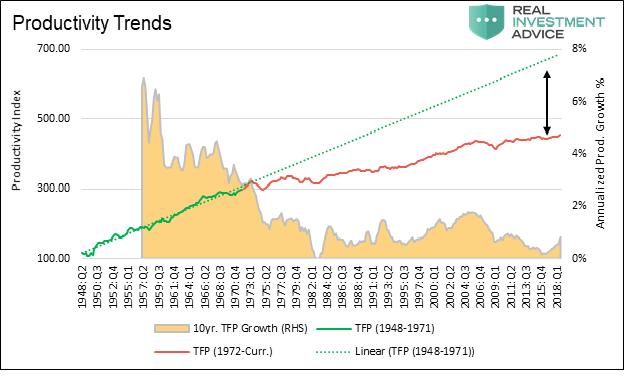

The graph below plots a simple index we created based on total factor productivity (TFP) versus the ten year average growth rate of TFP. The TFP index line is separated into green and red segments to highlight that change in the trend of productivity growth rate that occurred in the early 1970’s. The green dotted line extrapolates the trend of the pre-1972 era forward.

下のグラフはTFPとTFPの10年平均成長率を示している。TFPは赤線と緑線で色分けしている、1970年代初頭に生じた生産性成長率の変化を強調するためだ。緑の点線は1972年以前のトレンドを外挿したものだ。

Data Courtesy: San Francisco Federal Reserve

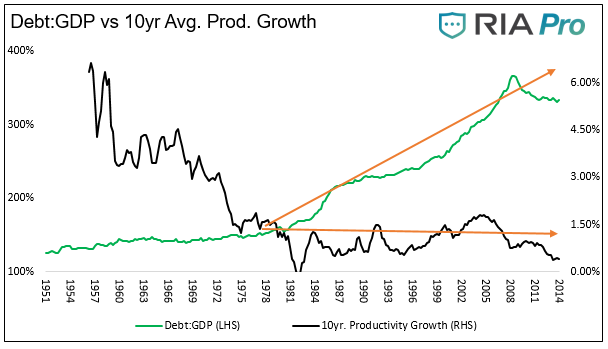

The graph below plots 10 year average productivity growth (black line) against the ratio of total U.S. credit outstanding to GDP (green line).

下のグラフは10年平均生産性成長率(黒線)と対GDP米国債務残高割合(緑線)を示す。

The stagnation of productivity growth started in the early 1970’s. To be precise it was the result, in part, of the removal of the gold standard and the resulting freedom the Fed was granted to foster more debt. For more information on this please read our article: The Fifteenth of August. The graph above reinforces the message from the other debt related graphs – over the last 30 years the economy has relied more upon debt growth and less on productivity to generate economic activity.Data Courtesy: Bloomberg, St. Louis and San Francisco Federal Reserve

生産性成長の低迷は1970年代初頭に始まった。正確に言うとこれは結果であり、部分的には、金本位制を放棄しFEDがさらなる債務を許した結果だ。この件に関してもっと詳しく知りたければ、私どもの記事を読むと良い:The Fifteenth of August。上のグラフを見れば、債務に関連する他のグラフの主張を売れ付けているーー過去30年以上、経済活動は債務増加に依存しており、生産性向上への依存度が低い。

政府の赤字歳出は民間部門に渡され、これが経済的な効果を出していると思われている。しかしながら、明らかに対GDPでの債務債務は増える一方だ、というわけでこれは嘘だ。更に言うと、赤字を生み出す金融コストだけでなく、機会費用が過小評価もしくは無視されている。政府部門に誤配分されている資金のために経済的な有益な生産性を引き起こすかもしれないベンチャー企業への資金が削られている。

The government is not solely to blame. The Federal Reserve has used monetary policy to prod economic growth and deprive the economy of full economic recessions that clean up mal-investment. They have bailed out the largest enablers of unproductive debt. Their policies encourage public and private debt expansion, much of which has been unproductive as shown in this article.

政府だけが責められるべきでもない。FEDは金融政策で経済成長を駆り立てる一方で完全な景気後退も引き起こし誤投資を一掃している。彼らは非生産的な債務を引き起こす巨大組織を補助している。彼らの政策は政府・民間部門の債務拡大を推奨しており、この記事で解説してきたように多くは非生産的なものだ。

We the people, also play a role. We drive bigger cars and live in bigger houses for example. We tend to spend more lavishly than generations past. Too much of this unproductive consumption is done with borrowed money and not savings. While these luxuries are nice, the economic benefits are very short-term in nature and come at the expense of the long-term benefits of more productive investment.

我々も生身の人間で、これに一翼を担っている。親の世代よりも大きな車に乗り大きな家に住みたいと思う。前の世代よりも贅沢な消費をする傾向にある。これが過剰になると非生産的な消費を引き起こし、貯蓄ではなく借金で賄うことになる。こういう贅沢は素晴らしいことだが、経済的恩恵は当然のことながらとても短期的なもので、もっと生産的な投資による長期的な恩恵を引き去ってしまう。

既存の債務への対処能力には限界があり、上に述べたように人口動態は難しくなってきている、となると将来の経済成長にはおもに生産性増加に重きを置かざるを得ない。現在の経済環境を見ると経済成長は湿っぽく、そして明らかに生産性が弱められている、債務の処理に資金が投じれれており生産的な目的への資金は減じられている。その場しのぎの誤政策は過剰に債務に依存しており、人口動態は成り行きに任せっきりだ。

The change required will be neither easy nor painless but it is necessary. Policy-makers will either need to become immediately responsive and take action to address these issues or discipline will be imposed by other involuntary means.

This is not just an economics story. Importantly, as investors in assets whose value and cash flows are dependent on these economic forces, we urge caution when the valuation of those assets is high as it is today amid such a challenging economic backdrop.

求められる変革は簡単でもなく痛みを伴うものだ、しかしこれが必要だ。為政者は直ちに責任を取りこれらの問題に取り組む行動を始めるべきだ、もしくは何らかの規律を見せるべきだ。こうなるともう経済の議論の範疇ではない。大切なことは、投資家としては投資する資産の価値とキャッシュフローがこの経済力学に依存しているわけで、これらの資産のバリュエーションが高くなったときには注意深くなるべきで、現在の経済環境はとても挑戦的なものだ。

Kansas 市FEDがツイッターにコメントを投稿した、そのグラフを下に示す、とても重要な経済テーマだ。経済分析においては生産性というのはとても重要な要素だが、ほとんどのエコノミストがこの件に言及しない、投資家は更にこのことを忘れ去っている。

The Kansas City Fed’s tweet is 100% correct in that wages are stagnating in large part due to low productivity growth. As the second chart shows, it is not only wages. The post financial-crisis economic expansion, despite being within months of a record for duration, is by far the weakest since WWII.

Kansas City FEDのツイートは100%正しい、給与が停滞している原因の主要因は生産性成長が低いからだ。二番目のチャートを見ても判るように、成長鈍化は給与だけではない。あの金融危機後の経済拡大は、第二次世界大戦後で記録的長期の拡大期間だが、とても弱い拡大だ。

Productivity growth over the last 350+ years is what allowed America to grow from a colonial outpost into the world’s largest and most prosperous economic power. Productivity is the chief long-term driver of corporate profitability and economic growth. Productivity drives investment returns whether we recognize it or not.

過去350年超の生産性成長で米国は植民地から世界最大の繁栄経済を生み出してきた。長期的に見れば生産性こそが企業収益や経済成長の駆動力だ。生産性こそが投資リターンを生み出すものだ、我々がこれを認めようが認めまいが。

Despite its foundational importance to the economy, productivity is not well understood. There is no greater proof than the hordes of Ivy League trained PhD’s at the Federal Reserve who have promoted extremely easy monetary policy for decades. It is this policy which has sacrificed productivity at the altar of consumption and short-term economic gains.

経済に対してとても重要なことなのだが、生産性は十分に理解されていない。アイビーリーグでPh.DをとりFEDで働く人達も理解が十分でない、彼らは何十年に渡り極端な金融緩和策を推進してきた。消費や短期的な経済成長のために彼らは生産性を犠牲にしてきた。

For more on the interaction between monetary policy and economic growth please read Wicksell’s Elegant Model.

金融政策と経済成長の関係にもっと起用味があるならこの記事を読むが良い、Wicksell's Elegant Model。

What Drives Economic Activity

経済活動を推進するものはなにか

経済成長は生産性を直接反映するものだ、この生産性は2つのインプトットから生み出される、労働と資本だ、これが結果として経済をレバレッジ成長させる。生産性無くしても、経済はこの2つの入力に依存している。労働、資本ともに限度があるために、長期に渡り十分な経済成長をすることはできない。

Leveraging labor and capital, or becoming more productive, provides the dynamism to an economy. Unfortunately, productivity requires work, time, and sacrifice. It’s a function of countless factors including innovation, education, government policies, and financial incentives.

労働と資本をレバレッジ、もしくはさらなる生産物を得るために、経済にダイナミクスを与える。残念なことに、生産性には、労働、時間そして犠牲が必要だ。そこには無数の要因がある、革新、教育、政策、そして金融インセンティブ。

Labor 労働

Labor, or human capital, is largely a function of the demographic makeup of an economy and its employees’ skillset and knowledge base. In the short run, increasing labor productivity is difficult. Realizing changes to skills training and education take time but they do have meaningful effect. Similarly, changes in birth rate patterns require decades to influence an economy.

労働、もしくは人的資本、これは経済を支える人工動体によるところが大きい、さらには労働者の熟練度と知識ベースだ。短期的に労働生産性を向上するのは難しい。労働習熟訓練や教育変革を実現するには時間を要し、しかもかなりな努力を要する。同様に経済に影響するほどに出生率を改善するには何十年とかかる。

Within the labor force, the biggest trend affecting current and future economic activity, both domestic and globally, is the so called “silver tsunami”, or the aging of the baby boomers. This outsized cohort of the population, ages 55 to 73 are beginning to retire at ever greater rates. As this occurs, they tend to consume less, rely more on financial support from the rest of the population, and withdraw valuable skills and knowledge from the workforce. The vast number of people in this demographic cohort makes this occurrence more economically damaging than usual. As an example, the old age dependency ratio, which measures the ratio of people aged greater than 65 to the working population ages 18-64, is expected to nearly double by the year 2035 (Census Bureau).

現在と将来の経済に影響する世界的トレンドは、いわゆる「高齢化の津波」だ、もしくは団塊の世代の高齢化。この人口分布の中でとても大きな割合を占める、55歳から73歳の人たちの引退速度がかつてない速さですすんでいる。これにともない、消費は落ち込み、他の世代の人の資金援助を必要としている、そして労働力から貴重なスキルや知識が失われている。人口動態のなかでのこのとても大きな割合の世代がいつも以上に経済にダメージを与えている。たとえば、高齢化率が高まると、18−64人口に対する65以上以上人口が2035年には倍になると見られている(統計局調べ)。

While the implications of changes in demographics and the workforce composition are numerous, they only require one vital point of emphasis: the significant economic contributions attributable to the baby boomers from the last 30+ years will diminish from here forward. As they contribute less, they will also require a higher allotment of financial support, becoming more dependent on younger workers.

人口動態変化や労働力構成は大きいものの、強調すべきことが一つ在る:過去30年超経済成長に大きく寄与してきた団塊の世代が今後は消えてゆくだろう。彼らの寄与は小さくなり、より大きな金融支援が必要となるだろう、より若い労働力への依存度が高くなる。

Finally, immigration is also an important component in the labor force equation. Changes in immigration policies and laws are easier to amend to foster more immediate growth but political dynamics argue that pro-immigration policies and laws are not likely within the next few years.

最後に、労働力問題では移民は重要な構成要素だ。移民を多く受け入れるには政策や法整備が必要だ、しかし政策転換や法整備が今後数年で実現しそうにない。

Capital 資本

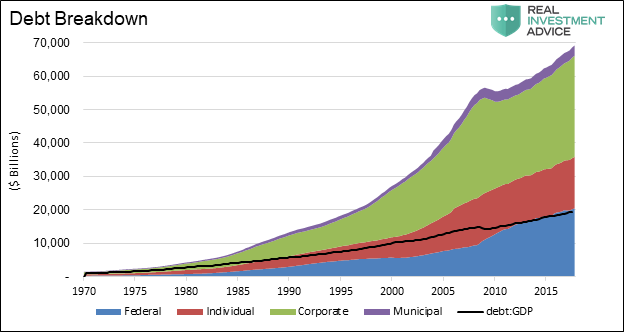

Capital includes natural, man-made and financial resources. Over the past 30+ years, the U.S. economy benefited from significant capital growth, in particular debt. The growth in debt outstanding, a big component of capital, is shown broken out by sector in the graph below. The increase is stark when compared to the relatively modest level of economic activity that accompanied it (black line).資本とは当然ながら、人工的なもので金融資源だ。過去30年超にわたり、米国経済は資本増加の恩恵を受けてきた、特に債務だ。債務増加、これが資本の大きな割合を占めるが、これをセクター別に示している。この増加は全くすごいもので、経済活動の増加はこれに比べると穏やかなものだ(黒線)

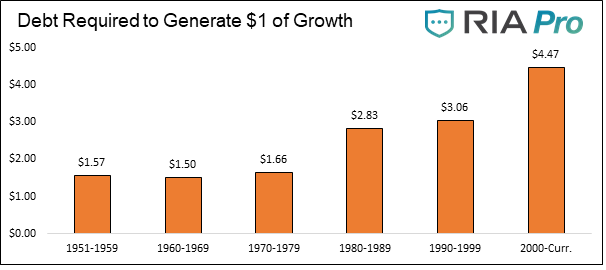

This divergence in debt and economic growth is a result of many consecutive years of borrowing funds for consumptive purposes and the misallocation of capital, both of which are largely unproductive endeavors. In hindsight we know these actions were unproductive as highlighted by the steadily rising ratio of debt to GDP shown above. The graph below tells the same story in a different manner, plotting the amount of debt required to generate $1 of economic growth. Simply, if debt were used for productive activities, economic growth would have risen faster than debt outstanding.Data Courtesy: Bloomberg, St. louis Federal Reserve

この債務と経済成長の乖離は消費のための多額の借金と資本の誤配分が長年続いたためだ、どちらも生産的ではない努力だ。後知恵だが、対GDPの債務割合が増えていることで、これは生産的でないことが解る。下のグラフは同じ状況を別の視点で示している、$1の経済成長に必要な債務の量だ。簡単に言うと、債務が生産的活動に使われるなら、経済成長は債務残高よりも経済成長のほうが大きいはずだ。

Data Courtesy: Bloomberg, St. Louis Federal Reserve

Productivity 生産性

Since 1980, the long term average growth rate of productivity has stagnated in a range of 0 to 2% annually, a sharp decline from the 30 years following WWII when productivity growth averaged 4 to 6%. While there is no exact measure of productivity, total factor productivity (TFP) is considered one of the best measures. Data for TFP can found at the San Francisco Federal Reserve- (http://www.frbsf.org/economic-research/indicators-data/total-factor-productivity-tfp/)1980年以来、長期的な生産性の平均成長率は年率0−2%と停滞している、第二次世界大戦後30年間の生産性成長率4−6%だが、これから急速に後退している。生産性の明確な定義は無いが、total factore productivity(TFP)は最良の指標の一つと見られている。TFPはサンフランシスコFEDが算出している。

The graph below plots a simple index we created based on total factor productivity (TFP) versus the ten year average growth rate of TFP. The TFP index line is separated into green and red segments to highlight that change in the trend of productivity growth rate that occurred in the early 1970’s. The green dotted line extrapolates the trend of the pre-1972 era forward.

下のグラフはTFPとTFPの10年平均成長率を示している。TFPは赤線と緑線で色分けしている、1970年代初頭に生じた生産性成長率の変化を強調するためだ。緑の点線は1972年以前のトレンドを外挿したものだ。

Data Courtesy: San Francisco Federal Reserve

The graph below plots 10 year average productivity growth (black line) against the ratio of total U.S. credit outstanding to GDP (green line).

下のグラフは10年平均生産性成長率(黒線)と対GDP米国債務残高割合(緑線)を示す。

The stagnation of productivity growth started in the early 1970’s. To be precise it was the result, in part, of the removal of the gold standard and the resulting freedom the Fed was granted to foster more debt. For more information on this please read our article: The Fifteenth of August. The graph above reinforces the message from the other debt related graphs – over the last 30 years the economy has relied more upon debt growth and less on productivity to generate economic activity.Data Courtesy: Bloomberg, St. Louis and San Francisco Federal Reserve

生産性成長の低迷は1970年代初頭に始まった。正確に言うとこれは結果であり、部分的には、金本位制を放棄しFEDがさらなる債務を許した結果だ。この件に関してもっと詳しく知りたければ、私どもの記事を読むと良い:The Fifteenth of August。上のグラフを見れば、債務に関連する他のグラフの主張を売れ付けているーー過去30年以上、経済活動は債務増加に依存しており、生産性向上への依存度が低い。

Demoting Productivity 生産性の低下

Government deficit spending is sold to the public as economically beneficial. However, the simple fact that government debt as a ratio of GDP has continually grown, tells you this is a lie. Further, there is not just a financial cost to running deficits but an opportunity cost that is underappreciated or ignored altogether. The capital misallocated towards the government was not employed for ventures that may have resulted in economically beneficial productivity gains.政府の赤字歳出は民間部門に渡され、これが経済的な効果を出していると思われている。しかしながら、明らかに対GDPでの債務債務は増える一方だ、というわけでこれは嘘だ。更に言うと、赤字を生み出す金融コストだけでなく、機会費用が過小評価もしくは無視されている。政府部門に誤配分されている資金のために経済的な有益な生産性を引き起こすかもしれないベンチャー企業への資金が削られている。

The government is not solely to blame. The Federal Reserve has used monetary policy to prod economic growth and deprive the economy of full economic recessions that clean up mal-investment. They have bailed out the largest enablers of unproductive debt. Their policies encourage public and private debt expansion, much of which has been unproductive as shown in this article.

政府だけが責められるべきでもない。FEDは金融政策で経済成長を駆り立てる一方で完全な景気後退も引き起こし誤投資を一掃している。彼らは非生産的な債務を引き起こす巨大組織を補助している。彼らの政策は政府・民間部門の債務拡大を推奨しており、この記事で解説してきたように多くは非生産的なものだ。

We the people, also play a role. We drive bigger cars and live in bigger houses for example. We tend to spend more lavishly than generations past. Too much of this unproductive consumption is done with borrowed money and not savings. While these luxuries are nice, the economic benefits are very short-term in nature and come at the expense of the long-term benefits of more productive investment.

我々も生身の人間で、これに一翼を担っている。親の世代よりも大きな車に乗り大きな家に住みたいと思う。前の世代よりも贅沢な消費をする傾向にある。これが過剰になると非生産的な消費を引き起こし、貯蓄ではなく借金で賄うことになる。こういう贅沢は素晴らしいことだが、経済的恩恵は当然のことながらとても短期的なもので、もっと生産的な投資による長期的な恩恵を引き去ってしまう。

Summary 要約

Given the finite ability to service debt outstanding and aforementioned demographic challenges, future economic growth, if we are to have it, will need to be based largely on gains in productivity. Current economic circumstances serve as both a wet blanket on economic growth and are clearly weighing on productivity by diverting capital away from productive uses in order to service that debt. Ill-conceived policies that impose an over-reliance on debt and demographics have largely run their course.既存の債務への対処能力には限界があり、上に述べたように人口動態は難しくなってきている、となると将来の経済成長にはおもに生産性増加に重きを置かざるを得ない。現在の経済環境を見ると経済成長は湿っぽく、そして明らかに生産性が弱められている、債務の処理に資金が投じれれており生産的な目的への資金は減じられている。その場しのぎの誤政策は過剰に債務に依存しており、人口動態は成り行きに任せっきりだ。

The change required will be neither easy nor painless but it is necessary. Policy-makers will either need to become immediately responsive and take action to address these issues or discipline will be imposed by other involuntary means.

This is not just an economics story. Importantly, as investors in assets whose value and cash flows are dependent on these economic forces, we urge caution when the valuation of those assets is high as it is today amid such a challenging economic backdrop.

求められる変革は簡単でもなく痛みを伴うものだ、しかしこれが必要だ。為政者は直ちに責任を取りこれらの問題に取り組む行動を始めるべきだ、もしくは何らかの規律を見せるべきだ。こうなるともう経済の議論の範疇ではない。大切なことは、投資家としては投資する資産の価値とキャッシュフローがこの経済力学に依存しているわけで、これらの資産のバリュエーションが高くなったときには注意深くなるべきで、現在の経済環境はとても挑戦的なものだ。

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for Clarity Financial, LLC. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

2019/01/16