“Importantly, the previous deep ‘oversold’ condition which was

supportive of the rally following Christmas Eve has now been fully

reversed back into extreme ‘overbought’ territory. While

this doesn’t mean the current rally will immediately reverse, it does

suggest that upside from current levels is likely limited.”

As I discussed previously, what was needed for the bulls to gain control of the narrative were several important issues:

私は以前にも議論したが、ブル相場が継続するためにはいくつかの重要なできごとが必要だ:

Central bank activity reverse from restrictive to accommodative,

中央銀行の政策が引き締め的から緩和的に転換する、

Washington to back off of “tariffs” and “trade war” rhetoric, and;

ワシントン政府が「関税」や「貿易戦争」方針を後退させる、そして;

The Federal Reserve to continue its more “dovish” stance.

FEDがさらに「ハト派」の姿勢を保つ。

Last weekend, we noted evidence of those changes. This week, the

markets were given the clearest sign yet that the Fed, and Central Banks

globally, were all too ready to come to the markets rescue.

It started with a WSJ article

suggesting that the Fed would not only stop hiking interest rates but

also cease the balance sheet reduction which has been extracting

liquidity from the market. This was quite the change as noted in an

early morning tweet.

WSJの記事によると、FEDは金利引き上げを停止するだけでなくバランスシート縮小を弱める、これまで市場の流動性を引き去ってきた縮小だ。朝早くのツイートに書かれていた変化だ。

In mid-2018, the Federal Reserve was adamant that a strong economy

and rising inflationary pressures required tighter monetary conditions.

At that time they were discussing additional rate hikes and a continued

reduction of their $4 Trillion balance sheet.

China has launched their own version of “Quantitative Easing” to help prop up their slowing economy.

中国は彼ら独自の「量的緩和」を実行し低迷する経済を元気づけようとした。

Lastly, the ECB downgraded Eurozone growth and there is a likelihood

that not only will they not raise rates this year, they will also extend

the TLTRO program.

Good question. It is the Targeted Longer-Term Refinancing Operations scheme which gives cheap loans to struggling Eurozone banks.

良い質問だ。これはTargeted Longer-Term Refinnacing Operationsと呼ばれるもので、不調の欧州銀行に安価なローンを提供するものだ。

Think about this for a moment.

こういう状況をちょっと考えてほしい。

For a decade the global economy has been growing. Market participants

are crowing about the massive surge in asset prices as clear evidence

of the strength of the economy. As noted last week:

“We’re the hottest economy in the world. Trillions of dollars are flowing here and building new plants and equipment. Almost

every other data point suggests, that the economy is very strong. We

will beat 3% economic growth in the fourth quarter when the Commerce

Department reopens.

We are seeing very strong chain sales. We don’t get the retail

sales report right now and we see very strong manufacturing production.

And in particular, this is my favorite with our corporate tax cuts and

deregulation, we’re seeing a seven-month run-up of the production of

business equipment, which is, you know, one way of saying business

investment, which is another way of saying the kind of competitive

business boom we expected to happen is happening.” – Larry Kudlow, Jan 24, 2019.

強い売上を目の当たりにしている。まだ小売データを見ていないが、強い生産高を目にした。そして特に、法人減税と規制緩和で7か月連続でビジネス機器製造が増えている、これはみなさんもご存知のとおりだ、ビジネス投資が活発だ、言い換えれば競争的なビジネスブームが起きており、期待通りになっている。」ーーLarry Kudlow, Lan 24,2019。

But yet, these “emergency measures” are STILL in place. Eurozone banks, global economies, and markets are still needing massive levels of support to stay afloat.

Yes, Kudlow is certainly “spinning the yarn” for the media to try and keep markets complacent. However, the Fed is clearly signaling their concern about “reality,” which as the data through the end of December shows, the U.S. economy is beginning to slow.

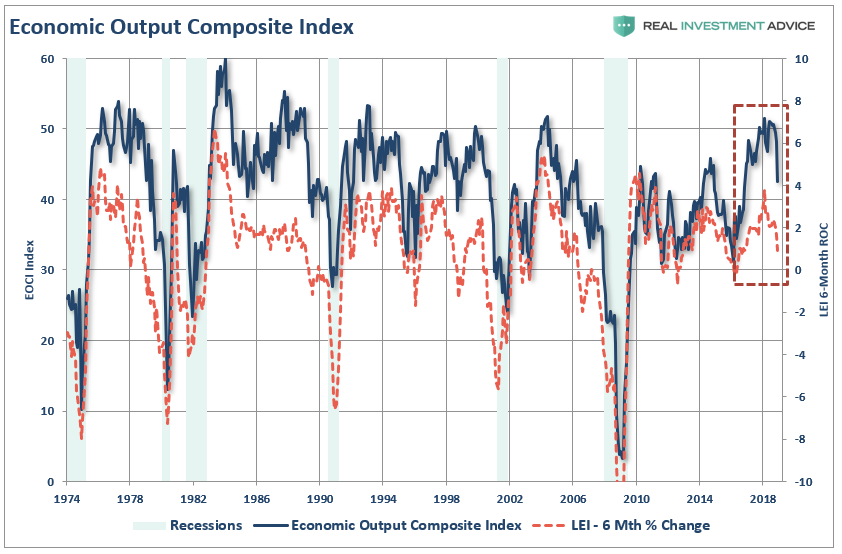

“As shown, over the last six months, the decline in the LEI has

actually been sharper than originally anticipated. Importantly, there is

a strong historical correlation between the 6-month rate of change in

the LEI and the EOCI

index. As shown, the downturn in the LEI predicted the current economic

weakness and suggests the data is likely to continue to weaken in the

months ahead.”

However, while the markets did respond bullishly to the news that the “Fed Put” was alive and well, the biggest issue facing the Fed, will be the ongoing effectiveness of “Quantitative Easing” programs. As previously discussed:

“Of course, after a decade of Central Bank interventions, it has

become a commonly held belief the Fed will quickly jump in to forestall a

market decline at every turn. While such may have indeed been the case

previously, the problem for the Fed is their ability to ‘bail

out’ markets in the event of a ‘credit-related’ crisis.”

“In 2008, when the Fed launched into their “accommodative

policy” emergency strategy to bail out the financial markets, the Fed’s

balance sheet was only about $915 Billion. The Fed Funds rate was at

4.2%.

If the market fell into a recession tomorrow, the Fed would be starting with roughly a $4 Trillion dollar

balance sheet with interest rates 2% lower than they were in 2009. In

other words, the ability of the Fed to ‘bail out’ the markets today, is

much more limited than it was in 2008.”

As an investor what you should be most concerned that it only a

slight slowing in economic growth and just a 4.4% decline in the S&P

500 last year to send the Fed into “panic mode.”

The question you should be asking is what do they know that you don’t. 疑問を持つべきことはこうだ、みなさんが知らない何かを彼らは知っているのだろうか。

Bull In A Bear’s Den

ベアの巣窟のなかのブル

Michael Lebowitz and I recently discussed the market in a broader sense for our subscribers at RIA PRO.

Michael Labowitzと私は最近購読者向けに幅広く市場に関して議論した、RIA PROでだ。

Use code“Bear Market” for a 1-MONTH free trial to RIA PRO. You get access to our exclusive commentary, portfolios, and a ton of research data to help improve your investing.

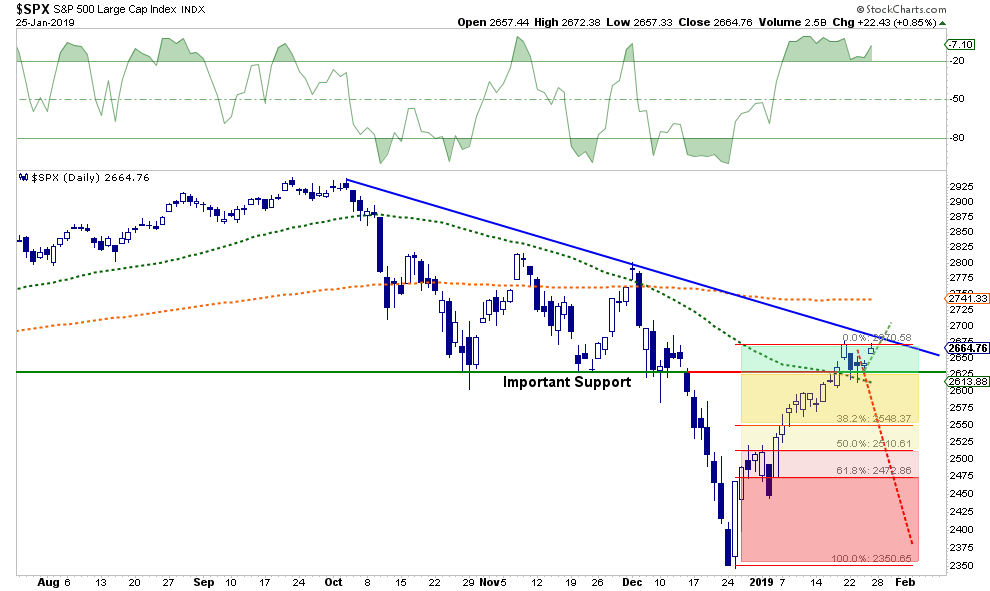

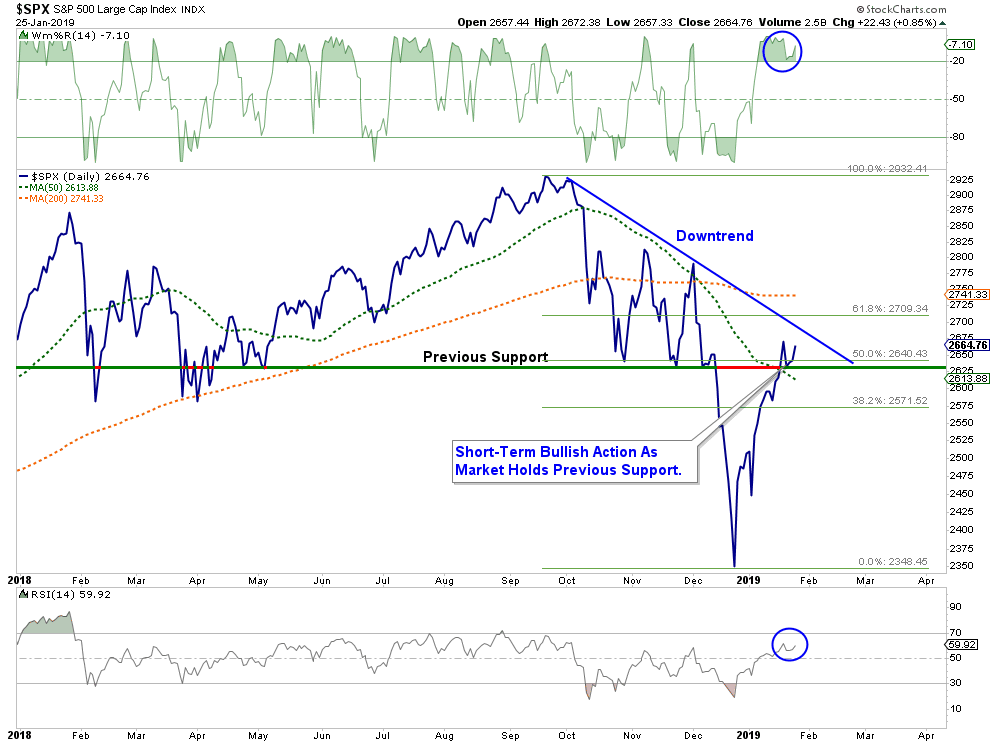

From a technical short-term perspective, the recent bullish market action remains confined to a “bearish” trend currently. This keeps the risk/reward ratio unbalanced for aggressive equity exposure.

As shown, this past week, the market tested both its previous support

of the October and November lows while maintaining above the 50-dma.

However, despite the news on Friday which pushed prices sharply higher,

the market failed to break above it previous highs and still remains

trapped below the downtrend line from the 2018 highs.

“Importantly, while the market did break above the first level of

resistance, it is currently NOT confirming the change to a bear market

just yet. As shown in the chart below, the 2015-2016 correction ended

when the market broke above, and successfully retested the 200-dma. That

put the market back on a bullish price trend above that running moving

average.”

The rally on Friday was based on the Fed will turn exceedingly “dovish” in their meeting next week. This could well wind up disappointing the markets. Last week, we added equity exposure to our portfolios with the acquisition of some companies that we like the fundamentals of.However,

we also swept a large portion of our trading cash into 1-3 month

Treasury bills as the risk/reward for equities remains negative. 金曜のラリーは、来週のFOMCでFEDが極端に「ハト派的」になるだろうという期待に基づいている。これが市場の失望を巻き戻した。先週、私どもは株式露出を増やした、ファンダメンタルズが良好と思え企業買収をした銘柄だ。しかしながら、私どもは手元現金のかなりな部分を1−3か月の短期国債にした、というのも株式のリスク/リターンはまだマイナスだからだ。

Even if you are exuberantly bullish, you should consider Mark Hulbert’s analysis from this past week:

たとえあなたが極端な強気でも、Mark Hulvertの先週の分析を考慮すべきだ:

The Dow Theory is still flashing a “sell” signal. Before this

indicator can turn bullish again, the rally that has taken the Dow Jones

Industrial Average almost straight up since its Dec. 24 low must end. That’s why bullishly predisposed Dow Theorists should be hoping for a market pullback.

Though individual Dow Theorists disagree on the specifics of how

to apply the Dow Theory in any particular situation, there is a broad

consensus on what it takes to generate a buy signal:

1. Both the Dow Jones Industrial Average and the Dow Jones

Transportation Average must undergo a “significant” rally after hitting

new lows — “significant” both in terms of time and magnitude. This step

has been satisfied by the market’s rally from the Dec. 24 lows.

2. Both of these Dow averages must subsequently undergo a

“significant” correction of the rally referred to in step #1, and in

this correction either one or both of these Dow averages must hold above

their previous lows (Dec. 24). We are waiting for this step.

3. Both averages must rise then rise above their highs registered at the top of the rally referred to in step #1. One of the lesser-appreciated aspects of this three-step process

is that, without a “significant” pullback (step #2), a buy signal will

never occur.

中国が債務増加していることはたしかです。ただ日本の例を日銀資金循環報告でみると家計、320兆円、民間非金融機関1,785兆円、一般政府 1,284兆円となります。合算すると3,300兆円にもなり、GDPの600%を超えています。 https://www.boj.or.jp/statistics/sj/sjexp.pdf この記事の統計と同じ考え方で数値を採用しているのかどうか気になります。 加えて、この資金循環報告に書かれている海外資産というのが内数なのか外数なのか?私にはよくわかりません。当然海外債務も結構な額になります。一度日銀資金循環 図表1を見てください。詳しい方に教えていただければ。 この中国のたどる道は昔のソ連とかMMTと同様で、自国通貨ならいくら発行しても倒産はしない、というか為政者が痛みに耐えることができず緩和を続けるというものです。でも最終的には限界点に達します。ソ連は建国から崩壊まで70年かかりました。 自由主義経済なら立ち行かなくなった企業は退場してもらうというのが減速なのですが、これがうまくゆかないわけです。 でも日本は中国のはるか先を言っているように見えます。ちょっと検索したのですが、日本の債務に関しては政府債務に言及したものばかりで、この記事のように民間、個人まで総合的に記載しているのは日銀の資金循環統計しか見つけることができませんでした。 China Continues To Pile Debt On Top Of More Debt Written by Jesse Colombo | Feb, 27, 2019 Like many countries, China attempted to rein in its debt growth over the past couple years, but ultimately gave up and is now back to piling on even more debt. Bloomberg reports – 多くの国と同様に、中国もここ2年ほど債務増加を抑えようとしてきた、しかし結局の所諦めてしまい、今や更に債務を積み上げている。ブルームバーグ記事ーー For almost two years,...

Class 8 Heavy Truck Orders Crash 68% in January by Tyler Durden Wed, 02/06/2019 - 17:25 Among the latest dismal news about the strength of the US economy, on Tuesday ACT Research released preliminary truck orders for January 2019 which showed that Class 8 truck orders collapsed an astounding 68% for January. The decline is being attributed to a 300,000+ vehicle backlog potentially prompting fleets to halt purchases in the near term. 米国経済に関し最近憂鬱なニュースが多い中で、火曜にACT researchが2019年1月のトラック発注を開示した、1月にClass 8のトラック発注がなんと68%も急落した。この発注減は短期的に300,000台超の潜在在庫を生み出す。 Specifically, in January Class 8 net orders were 15,800 units (14,700 SA; 176,400 SAAR), down 68% YoY and down 26% MoM. Class 5- 7 January net orders were 23,400...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...