Like many countries, China attempted to rein in its debt growth over

the past couple years, but ultimately gave up and is now back to piling

on even more debt. Bloomberg reports –

For almost two years, the question

has lingered over China’s market-roiling crackdown on financial

leverage: How much pain can the country’s policy makers stomach?

Evidence

is mounting that their limit has been reached. From bank loans to

trust-product issuance to margin-trading accounts at stock brokerages,

leverage in China is rising nearly everywhere you look.

While

seasonal effects explain some of the gains, analysts say the trend has

staying power as authorities shift their focus from containing the

nation’s $34 trillion debt pile to shoring up the weakest economic

expansion since 2009. The government’s evolving stance was underscored

by President Xi Jinping’s call for stable growth late last week, while

on Monday the banking regulator said the deleveraging push had reached

its target.

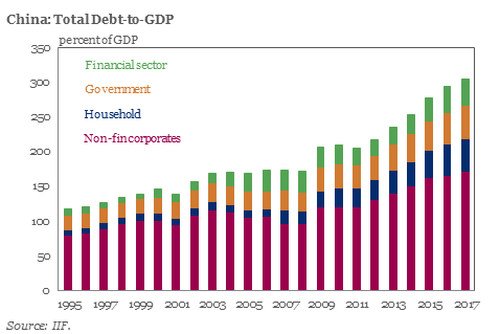

As I’ve been warning,

China has been experiencing a powerful credit bubble over the past

decade (see the chart below). China’s leaders inflated the credit bubble

in order to supercharge economic growth during and after the global

financial crisis in 2008/2009. China’s credit-driven economy has become

one of the main growth engines of the global economy, which has scary

implications because it’s even more evidence that the global economic

recovery is predicated on debt.

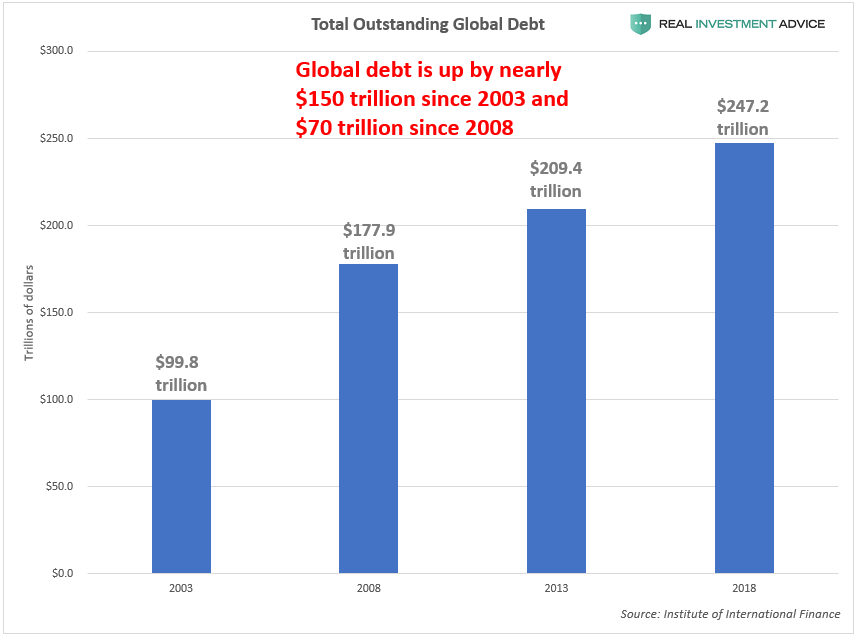

China’s aggressive credit expansion is a major contributor to the

global debt explosion over the past couple decades. Global debt has

increased by $150 trillion since 2003 and $70 trillion since 2008:

China’s credit bubble is very similar to Japan’s economic bubble

in the late-1980s. For many years, Japan’s economic growth seemed

unstoppable and many people believed that Japan would overtake Western

economies in short order. Of course, Japan’s growth miracle came to a

screeching halt in the early-1990s when the country’s bubble burst. By

ramping up debt so aggressively (which borrows economic growth from the

future), China is following in the same footsteps as Japan and will soon

experience the downsides of debt-fueled growth.

Please follow me on LinkedIn and Twitter to keep up with my updates. Please click here to sign up for our free weekly newsletter to learn how to navigate the investment world in these risky times.

多量のオピオイドを米国に送り込み、米国で深刻な麻薬中毒問題を引き起こしています。現代版「阿片戦争」です。あのトヨタ初の女性取締役もオピオイド中毒で逮捕解任されましたよね。 US Is Dependent On China For Almost 80% Of Its Medicine by Tyler Durden Fri, 05/31/2019 - 12:55 Experts are warning that the U.S. has become way too reliant on China for all our medicine , our pain killers, antibiotics, vitamins, aspirin and many cancer treatment medicine. 専門家はこう警告する、米国はすべての医薬品、痛み止め、抗生物質、ビタミン、アスピリン、各種抗がん剤で、中国依存度が高すぎる。 Fox Business reports that according to FDA estimates at least 80 percent of active ingredients found in all of America’s medicine come from abroad, primarily from China . And it’s not just the ingredients, China wants to become the world’s dominant generic drug maker. So far Chinese companies are making generic for everything from high blood pressure to chemotherapy drugs. 90 percent of America’s prescriptions a...

米国はよく理解してませんが、日本の場合では量的緩和で日銀が国債買い上げした資金は日銀当座預金にそのままです、市中には流れていません。でもNHKのニュース等では「ジャブジャブ」という表現をアナウンサーが使い、さらに丁寧に水道の蛇口からお金が吐き出される画像まで示してくれます。これって心理効果が大きいですよね。量的緩和とは何かを7時のニュースや新聞でこれ以上丁寧に解説するのはそう簡単ではありません。一般の人も株式をやっている人も「イメージ」で捉える以上はそう簡単にできません。多くの人は量的緩和とはなにか、を理解していないと私は想像しています。 ただし、国債を買い上げるので長期金利が低下し住宅ローン金利等が下がったのは確実な効果です。一方で長短金利差が少なくなると銀行のビジネスモデルが成り立たなくなりますが。 This Is The One Chart Every Trader Should Have "Taped To Their Screen" by Tyler Durden Sat, 01/19/2019 - 18:55 After a year of tapering, the Fed’s balance sheet finally captured the market’s attention during the last three months of 2018. 一年間のテーパリング後、FEDバランスシートがとうとう市場の注目をあびることになった、2018年の最後の3ヶ月だ。 By the start of the fourth quarter, the Fed had finished raising the caps on monthly roll-off of its balance sheet to the full $50bn per month (peaking at $30bn USTs, $20bn MBS...

後講釈なんですが、6月option(5月28日 expire)の$2400 Call Optionが out of the moneyになりました。6月optionは特にOpen Interest が大きい。きっかけはFED高官の発言のようですが、Option Writerにはまちかまえていたものでしょう。 ただ、これも今月末のexpireをすぎれば圧力は無くなると思います。