「状況は急速に劣化している」:欧州が世界で「最も弱い」

Last

week, when looking at the latest regional Industrial Production figures

out of European nations, we made a simple observation: while GDP has

yet to confirm, Europe is now in a recession.

先週に、欧州での各国工業生産指数を確認したとき、ZeroHedgeはシンプルなことを見つけた:GDPの観点では、すでに欧州は景気後退入りしている。

そしてブルームバーグによると、その数日後、欧州は確かに世界の中で最も弱いリンクだ、そしてこれは米中貿易戦争よりも深刻だ、「世界経済成長に対する最大の懸念は欧州のように見える」。

As evidence, Bloomberg cites the same data that we highlighted last week, namely that industrial production across the 19-nation euro area is "falling at the fastest pace since the financial crisis, and deteriorating demand is evident as the region finds itself squeezed between international and domestic drags." According to Wednesday data, industrial output for the Euro area slumped 0.9% in December from November, double the forecast, while the annual decline was the steepest since 2009.

ブルームバーグが指摘するのと同じ証拠を先週示したが、欧州19か国の工業生産は「金融危機以来最速で下落している、そして需要が悪化しているのは明らかだ、この地域をみると地域内そして国際経済を引きずっている」。水曜のデータによると、欧州の工業生産は12月には前月から0.9%下落した、予想の倍の悪化だ、一方前年比で見ると2009年以来の下落となる。

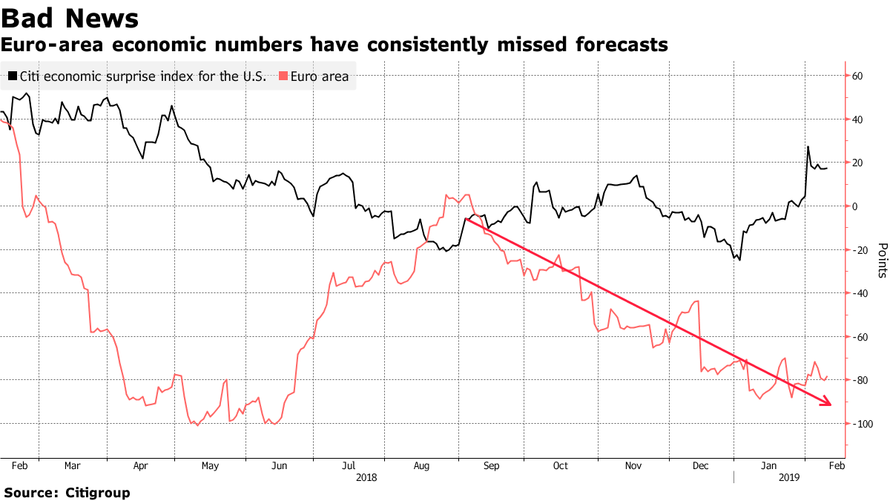

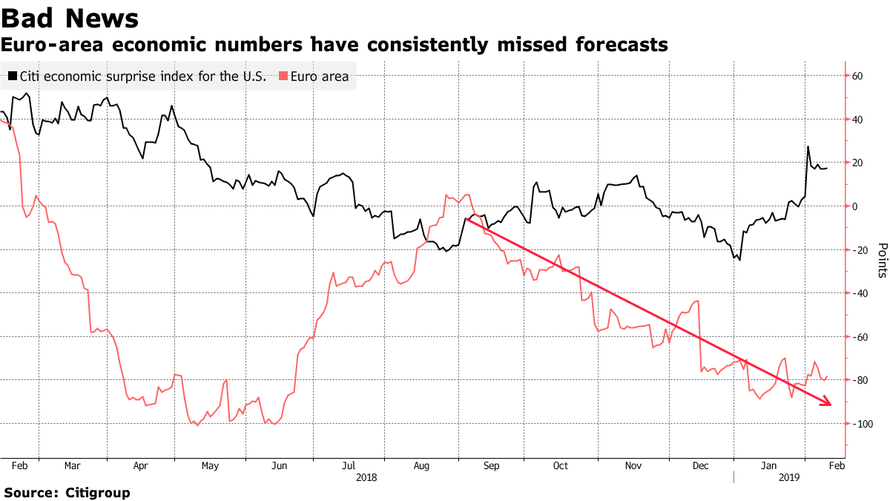

That leaves Europe's GDP at risk of barely reaching 1% in 2019, a sharp slowdown from 2018, with even continental powerhouse Germany in trouble. That, of course, is a polite way of saying that Europe is on the verge of a recession, if not already in one - as we claimed previously - and as seen in the following chart showing the recent series of disappointments in European economic data relative to expectations.

このレベルなら、欧州GDPは2019年に1%にもならないだろう、2018年から急激に鈍化している、最も強力なドイツがトラブルに見舞われている。当然、欧州が景気後退の崖っぷちにいるというのは丁寧な表現だが、ZeroHedgeが以前にも書いたがこれだけではない、下のチャートに示すが欧州経済を示す一連のデータは予想を下回り失望するものだ。

Making matters worse, Europe is sliding into contraction at the worst possible time: just as the ECB has ended its QE, although the silver lining is that any speculation for a rate hike by Mario Draghi have been permanently crushed, and like in the US, the only question now is when will QE return.

更に悪いことに、欧州は最悪のときに収斂を迎えている:ECBがQEを終了した、Mario Draghiが金利引き上げなどしようものなら急落だ、そして米国と同様に問題はいつQEを再開するかだ。

As a result, the Bloomberg euro index is near its lowest since mid-2017 and European stocks have never been cheaper relative to bonds in terms of yield gap. And investors are not happy.

結果として、ブルームバーグのユーロ指数は2017年半ば以来で最低だ、そして欧州株価はイールドギャップを考えると債権より割安では決して無い。そして投資家はハッピーではない。

“The concern I have right now is in Europe,” said Salman Ahmed, chief investment strategist at Lombard Odier. “It’s

clear China is going through a slowdown, but there’s also a strong

amount of stimulus in the pipeline. However, in Europe, things are

deteriorating quite fast.”

「私が今懸念しているのは欧州だ」とSalman Ahmedは言う、彼はLombard Odierの主任投資ストラテジストだ。「中国が減速しているのは明らかだ、しかし強い刺激作が順次実行されている。しかしながら、欧州では状況が急速に悪化している。」

While Europe is no stranger to sluggish growth, the extent and suddenness of the latest bout of weakness is different, as unlike previous episodes, it "reflects that the slowdown is hitting the core of the region."

欧州では成長鈍化でも驚かないが、最近の弱さへの急変はちょっとこれまでのものとは異なる、「景気減速がこの地域の中核を襲っている」。

As Bloomberg notes, while the likes of Greece were at the root of past sluggishness, this time Germany’s prospects are crumbling after a protracted slump in manufacturing. Household spending has also ground to a halt in France, which is beset by the Yellow Vest protests.

ブルームバーグによると、前回はギリシャが震源だったが、今回はドイツの製造業で後退が続いている。フランスでは家計支出が低迷し、これがイエローベストの抗議を引き起こした。

"Together those two countries account for about half the euro-area economy", and any coordinated contraction in the two assures a Eurozone recession, best summarized by the following quote from Ludovic Subran, deputy chief economist at Allianz.: "If France stops consuming and Germany stops producing you have a major problem in the euro zone."

「この2国を合わせると欧州経済の半分になる」、そして2国同時に収斂すると欧州景気後退は確実だ、Ludovic Subranがこの状況をうまくまとめている、彼はAllianzの主任代理エコノミストだ:「もしフランスが消費を止めドイツが生産を止めるなら、欧州の大問題となる。」

It's not just the economy, however, as Europe's demons that were

previously stuffed under the rug, are once again starting to re-emerged:

Italian bond yields, after a torrid burst of buying in the past few

months, have once again started to creep higher amid doubts over fiscal

management, the health of banks is questionable and Brexit remains

unresolved. Yesterday's decision by Santander not to call a contingent

convertible note only adds to the woes plaguing Europe's banks. Oh, and

just one more observation: Deutsche Bank. Nuff said.

問題は経済だけではない、以前とよく似た欧州の悪魔が潜んでいる、これがまた出現し始めた:イタリアの債権利率だ、ここ数ヶ月は積極的に買われていたが、財政懸念、銀行の健全性懸念、Brexitが解決されない懸念で金利があがりはじめた。昨日にはSantander銀行がココ債のコールを実行しなかったばかりか欧州銀行の苦悩が続く。さらにもう一つ:ドイツ銀行だ。

And speaking of the devil, Deutsche Bank's chief economist David Folkerts-Landau said this month that “downside risks have risen sharply in Europe” (he did not discuss his employer's key role therein).

そして悪魔といえば、ドイツ銀行のチーフエコノミストDavid Folkerts-Laundauがこういった、「欧州では下落リスクが急増している」(彼は自らの勤め先については議論しなかった)。

As for the reasons behind Europe's collapsing economy, they have been widely discussed previously, and revolve mostly around China's economic slowdown, with automakers such as Fiat citing weaker demand in the world’s second-largest economy. That’s filtering through to other companies, "with Brussels-based Umicore saying last week that profit will be held back by the global automotive slowdown."

欧州経済急落の背景にあるのは、これまで広く議論されてきたが、中国経済減速の議論もあり、Fiatのような自動車メーカも需要が弱い。これが他の企業にも影響し、「ブリュッセルを拠点とするUmicoreの先週の話では、世界的自動車産業の減速で利益が減ると見られている。」

All of this is known; what is not known is what Europe can or will do if its slowdown fails to reverse: "If it does get worse, there’s a question over how authorities could respond, and the European Central Bank has little left in the tank."

これらはすでに知られたことだ、わからないことは低迷が反転に失敗するなら欧州はどうなるかだ:「更に悪くなるなら、当局がどう対処するかが疑問だ、そしてECBにはもう弾があまり残っていない。」

Yet another unprecedented central bank intervention may still be needed. According to Bloomberg, Germany’s downside may be limited by "record-low unemployment along with modest fiscal stimulus. And Bloomberg Economics research suggests that spillovers from Germany to other euro nations is usually containable. That’s partly because it has a different structure and its shocks are country-specific."

さらなる前代未聞の中央銀行介入が必要かもしれない。ブルームバーグによると、ドイツの下落に関しては記録的な低失業率もあり、穏やかな財政刺激で対処できるかもしれない。ブルームバーグエコノミストの調査では、ドイツから他のユーロ諸国への影響は限られるかもしれないと示唆する。国により構造が異なりショックはそれぞれの国特有だからだ。

Unless, of course, this time is different, with it is because even with a slumping Euro, Germany's export powerhouse is unable to capitalize on this export subsidy.

Meanwhile, like Deutsche Bank, Goldman recently downgraded its near-term euro-area expectations, although it remains optimistic on the longer-term outlook, and sees an improvement later this year, thanks to a boost from lower oil prices and fiscal policy. ABN Amro economist Aline Schuling shares the view: "The domestic economy is quite resilient. You could very well have a negative first quarter and a weakish second, but after that it should pick up again. I don’t expect a deep or prolonged recession."

今回が例外でない限り、欧州景気後退となれば、ドイツの輸出は芳しくない。同時に、ドイツ銀行と同様に、ゴールドマン・サックスは最近欧州の短期予想を格下げした、ただし長期的には楽観している、そして今年遅くには回復すると見ている、原油価格低下と財政政策の後押しでだ。ABN AmroのエコノミストAline Schulingはこう見ている:「国内経済は弾力がある。Q1はマイナスQ2は弱いかもしれない、しかしその後持ち直すはずだ。私は深く長い景気後退になるとは予想していない。」

Which is bad news for traders, now that the world is back in a global race to the rates bottom, because the deeper and more prolonged the recession, the more assured yet another major intervention by the ECB.

これはトレーダーに取っては悪い話だ、今の所世界中で金利は底値になっている、景気後退が長引きもっと深刻になると、さらなるECBの介入となろう。

先週に、欧州での各国工業生産指数を確認したとき、ZeroHedgeはシンプルなことを見つけた:GDPの観点では、すでに欧州は景気後退入りしている。

そしてブルームバーグによると、その数日後、欧州は確かに世界の中で最も弱いリンクだ、そしてこれは米中貿易戦争よりも深刻だ、「世界経済成長に対する最大の懸念は欧州のように見える」。

As evidence, Bloomberg cites the same data that we highlighted last week, namely that industrial production across the 19-nation euro area is "falling at the fastest pace since the financial crisis, and deteriorating demand is evident as the region finds itself squeezed between international and domestic drags." According to Wednesday data, industrial output for the Euro area slumped 0.9% in December from November, double the forecast, while the annual decline was the steepest since 2009.

ブルームバーグが指摘するのと同じ証拠を先週示したが、欧州19か国の工業生産は「金融危機以来最速で下落している、そして需要が悪化しているのは明らかだ、この地域をみると地域内そして国際経済を引きずっている」。水曜のデータによると、欧州の工業生産は12月には前月から0.9%下落した、予想の倍の悪化だ、一方前年比で見ると2009年以来の下落となる。

That leaves Europe's GDP at risk of barely reaching 1% in 2019, a sharp slowdown from 2018, with even continental powerhouse Germany in trouble. That, of course, is a polite way of saying that Europe is on the verge of a recession, if not already in one - as we claimed previously - and as seen in the following chart showing the recent series of disappointments in European economic data relative to expectations.

このレベルなら、欧州GDPは2019年に1%にもならないだろう、2018年から急激に鈍化している、最も強力なドイツがトラブルに見舞われている。当然、欧州が景気後退の崖っぷちにいるというのは丁寧な表現だが、ZeroHedgeが以前にも書いたがこれだけではない、下のチャートに示すが欧州経済を示す一連のデータは予想を下回り失望するものだ。

Making matters worse, Europe is sliding into contraction at the worst possible time: just as the ECB has ended its QE, although the silver lining is that any speculation for a rate hike by Mario Draghi have been permanently crushed, and like in the US, the only question now is when will QE return.

更に悪いことに、欧州は最悪のときに収斂を迎えている:ECBがQEを終了した、Mario Draghiが金利引き上げなどしようものなら急落だ、そして米国と同様に問題はいつQEを再開するかだ。

As a result, the Bloomberg euro index is near its lowest since mid-2017 and European stocks have never been cheaper relative to bonds in terms of yield gap. And investors are not happy.

結果として、ブルームバーグのユーロ指数は2017年半ば以来で最低だ、そして欧州株価はイールドギャップを考えると債権より割安では決して無い。そして投資家はハッピーではない。

「私が今懸念しているのは欧州だ」とSalman Ahmedは言う、彼はLombard Odierの主任投資ストラテジストだ。「中国が減速しているのは明らかだ、しかし強い刺激作が順次実行されている。しかしながら、欧州では状況が急速に悪化している。」

While Europe is no stranger to sluggish growth, the extent and suddenness of the latest bout of weakness is different, as unlike previous episodes, it "reflects that the slowdown is hitting the core of the region."

欧州では成長鈍化でも驚かないが、最近の弱さへの急変はちょっとこれまでのものとは異なる、「景気減速がこの地域の中核を襲っている」。

As Bloomberg notes, while the likes of Greece were at the root of past sluggishness, this time Germany’s prospects are crumbling after a protracted slump in manufacturing. Household spending has also ground to a halt in France, which is beset by the Yellow Vest protests.

ブルームバーグによると、前回はギリシャが震源だったが、今回はドイツの製造業で後退が続いている。フランスでは家計支出が低迷し、これがイエローベストの抗議を引き起こした。

"Together those two countries account for about half the euro-area economy", and any coordinated contraction in the two assures a Eurozone recession, best summarized by the following quote from Ludovic Subran, deputy chief economist at Allianz.: "If France stops consuming and Germany stops producing you have a major problem in the euro zone."

「この2国を合わせると欧州経済の半分になる」、そして2国同時に収斂すると欧州景気後退は確実だ、Ludovic Subranがこの状況をうまくまとめている、彼はAllianzの主任代理エコノミストだ:「もしフランスが消費を止めドイツが生産を止めるなら、欧州の大問題となる。」

問題は経済だけではない、以前とよく似た欧州の悪魔が潜んでいる、これがまた出現し始めた:イタリアの債権利率だ、ここ数ヶ月は積極的に買われていたが、財政懸念、銀行の健全性懸念、Brexitが解決されない懸念で金利があがりはじめた。昨日にはSantander銀行がココ債のコールを実行しなかったばかりか欧州銀行の苦悩が続く。さらにもう一つ:ドイツ銀行だ。

And speaking of the devil, Deutsche Bank's chief economist David Folkerts-Landau said this month that “downside risks have risen sharply in Europe” (he did not discuss his employer's key role therein).

そして悪魔といえば、ドイツ銀行のチーフエコノミストDavid Folkerts-Laundauがこういった、「欧州では下落リスクが急増している」(彼は自らの勤め先については議論しなかった)。

As for the reasons behind Europe's collapsing economy, they have been widely discussed previously, and revolve mostly around China's economic slowdown, with automakers such as Fiat citing weaker demand in the world’s second-largest economy. That’s filtering through to other companies, "with Brussels-based Umicore saying last week that profit will be held back by the global automotive slowdown."

欧州経済急落の背景にあるのは、これまで広く議論されてきたが、中国経済減速の議論もあり、Fiatのような自動車メーカも需要が弱い。これが他の企業にも影響し、「ブリュッセルを拠点とするUmicoreの先週の話では、世界的自動車産業の減速で利益が減ると見られている。」

Even companies reporting resilience in China are wary. L’Oreal chief Jean-Paul Agon said this month the economic backdrop will remain “volatile and unpredictable,” though the French cosmetics giant also posted forecast-beating sales helped by the “dynamism of Chinese consumers.”中国で実績のある企業も心配している。L'Oreal社の主任Jean-Paul Agonが今月言うことには、景気環境は「変動が大きく予想できない」、ただしフランスの化粧品大手は「中国消費者の 変化」で予想を上回る売上だという。

All of this is known; what is not known is what Europe can or will do if its slowdown fails to reverse: "If it does get worse, there’s a question over how authorities could respond, and the European Central Bank has little left in the tank."

これらはすでに知られたことだ、わからないことは低迷が反転に失敗するなら欧州はどうなるかだ:「更に悪くなるなら、当局がどう対処するかが疑問だ、そしてECBにはもう弾があまり残っていない。」

Yet another unprecedented central bank intervention may still be needed. According to Bloomberg, Germany’s downside may be limited by "record-low unemployment along with modest fiscal stimulus. And Bloomberg Economics research suggests that spillovers from Germany to other euro nations is usually containable. That’s partly because it has a different structure and its shocks are country-specific."

さらなる前代未聞の中央銀行介入が必要かもしれない。ブルームバーグによると、ドイツの下落に関しては記録的な低失業率もあり、穏やかな財政刺激で対処できるかもしれない。ブルームバーグエコノミストの調査では、ドイツから他のユーロ諸国への影響は限られるかもしれないと示唆する。国により構造が異なりショックはそれぞれの国特有だからだ。

Unless, of course, this time is different, with it is because even with a slumping Euro, Germany's export powerhouse is unable to capitalize on this export subsidy.

Meanwhile, like Deutsche Bank, Goldman recently downgraded its near-term euro-area expectations, although it remains optimistic on the longer-term outlook, and sees an improvement later this year, thanks to a boost from lower oil prices and fiscal policy. ABN Amro economist Aline Schuling shares the view: "The domestic economy is quite resilient. You could very well have a negative first quarter and a weakish second, but after that it should pick up again. I don’t expect a deep or prolonged recession."

今回が例外でない限り、欧州景気後退となれば、ドイツの輸出は芳しくない。同時に、ドイツ銀行と同様に、ゴールドマン・サックスは最近欧州の短期予想を格下げした、ただし長期的には楽観している、そして今年遅くには回復すると見ている、原油価格低下と財政政策の後押しでだ。ABN AmroのエコノミストAline Schulingはこう見ている:「国内経済は弾力がある。Q1はマイナスQ2は弱いかもしれない、しかしその後持ち直すはずだ。私は深く長い景気後退になるとは予想していない。」

Which is bad news for traders, now that the world is back in a global race to the rates bottom, because the deeper and more prolonged the recession, the more assured yet another major intervention by the ECB.

これはトレーダーに取っては悪い話だ、今の所世界中で金利は底値になっている、景気後退が長引きもっと深刻になると、さらなるECBの介入となろう。