誰がゴールドを買っている?

もう買うべき国債が枯渇し、黒田さんがゴールドを買いはじめようものなら話題になるでしょうね。

Copyright ©2009-2019 ZeroHedge.com/ABC Media, LTD

Authored by Kevin Muir via The Macro Tourist blog,

I’ll warn you right off the bat, I have been waiting to write this piece for the past few days. You see, it’s a gold post, and as much as I try to take a bigger picture view, the trader-in-me still hates writing a bullish piece just as the market is about to have a minor correction. So I often get cute and wait for a dip before I publish.

But the gold decline refuses to materialize and I have decided to just post my piece - hoping I am not top-ticking this recent rally, but fearing it’s probably the surest sign we are headed lower over the short run.

私はすぐに警告しよう、私はこの記事を書くのを数日待っていた。ご存知の通りゴールドに関するものだ、私はできるだけ俯瞰図を書くように心がけよう、市場にはまだ小さな調整が待ち構えていそうで、私の中のトレーダーとしての立場としてはまだ強気の記事を書きたくない。というわけで私は記事を書くのに押し目を待っている。しかしゴールド下落は申告になりそうもなく、私はこの記事を書くことにしたーー私は最近のラリーを追いかけているわけではない、むしろ短期的には下落に向かう恐れを持っている。

Yet over the long-run, I contend something has changed in the gold market. Something we should all be paying attention to.

でも、長期的視点では、私はゴールド市場でなにか変化があったと信じている。誰もがこれに注目すべきだ。

Let’s have a look at the trading over the past year. Last November, gold took off and ran from $1,180 to $1,320.

まずはここ数年の値動きを見てみよう。昨年11月に、ゴールドは離陸した、$1180から$1320へとだ。

To some extent the initial move of November and December might be easily explained. Don’t forget that during this period the stock market was selling off hard and there was a fair amount of fear in the market.

11月12月の最初の値動きは簡単に説明できるかもしれない。忘れてはいけないが、この時期には株式市場は激しく下落し市場には恐怖心が蔓延していた。

But why hasn’t gold sold off in the past two months as the fear subsided?

You might argue that gold is simply rallying along with the decline in real yields. Powell’s historic flip-flop has certainly caused real rates to decline and help gold.

しかしこの2か月恐怖心が和らいでもどうしてゴールドは下落しなかったのか?金利が下がってきたために単にゴールドラリーがあったと皆さんは思うかもしれない。Powellの歴史的な転換はたしかに金利を引き下げゴールドの手助けになった。

However, many market participants believe gold’s price movement is best explained by movements in the US dollar.

しかしながら、市場参加者の多くはゴールド価格は米ドルの動きで説明できると信じているかもしれない。

For the first three quarters of 2018 gold was indeed trading almost lockstep inverse to the US dollar. The US dollar was going up while gold was falling tick-for-tick.

2018年の最初の3四半期はたしかにゴールドは米ドルとは逆に歩調を揃えた。米ドルの上昇に伴いゴールドは順次下落した。

Since October this relationship has broken down and now both securities are heading higher.

10月からはこの関連が壊れて今や両者は歩調を合わせて上昇している。

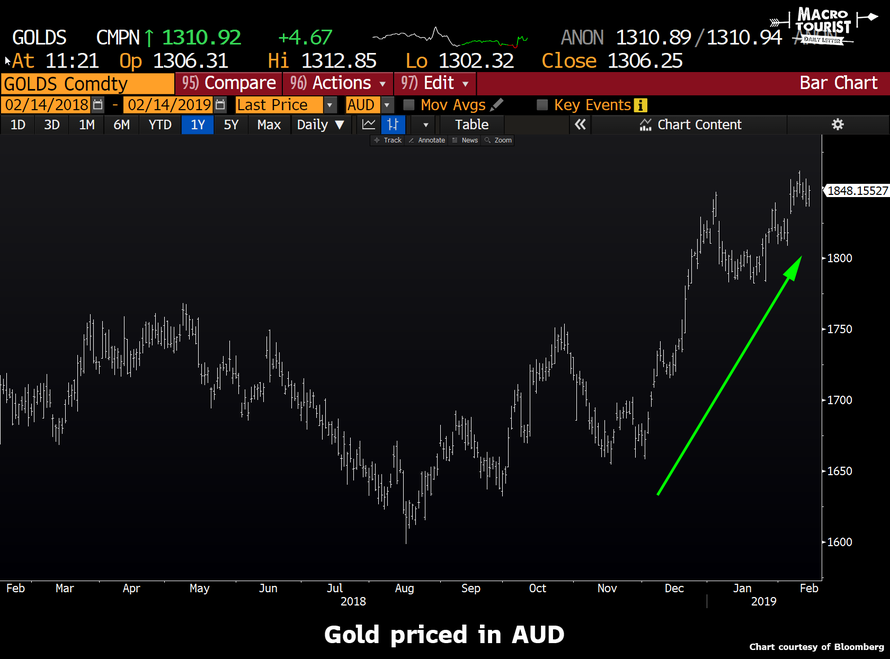

The easiest way to visualize this phenomenon is to show some charts of gold priced in other currencies.

この状況を簡単に図示するのは他国通貨でゴールドチャートを見ることだ。

Whether it’s gold priced in CNY, EUR, JPY or AUD, it’s all the same chart - gold has had a strong rally in every currency.

CNY,EUR,JPYそしてAUDでゴールドの動きを見ると、どの通貨でもゴールドは強いラリーをしている。

Gold is not going up because of US dollar weakness - it’s going up in real terms.

The question is why?

米ドルが弱いからゴールドが上昇しているわけではないーー実際に上昇している。問題はどうしてかということだ

There is little doubt that the dovish tilt by Powell has helped gold, but if you look at when the rally started, it was way before his post-Christmas cave.

ほとんど疑いなくPowellのハト派視線がゴールドを助けた、しかしラリーが始まった時期を見ると、彼が発言したクリスマスイブよりずっと前のことだ。

I don’t have any wonderfully original insights to present to you today. Rather, what little I can offer is to connect some dots and make a guess that the timing is finally lining up for some bigger picture macro trends that have been brewing for some time.

今の所私は皆さんにお伝えできる素晴らしい独自の洞察が在るわけではない。むしろ、その要因を点から紡ぎあげることがほとんどできない、単に推測するだけだが、このタイミングの背景にはなにか大きなマクロトレンドが在るのではないかと想像する、どこかの時期から醸成されたものだ。

I urge you to read the recent report by the World Gold Council titled “Gold Demand Trends Full year and Q4 2018. From the executive summary:

私は最近のWrold Gold Councilの記事を読むことをおすすめする「2018Q4および通年のゴールド需要トレンド」。この要約はこういう具合だ:

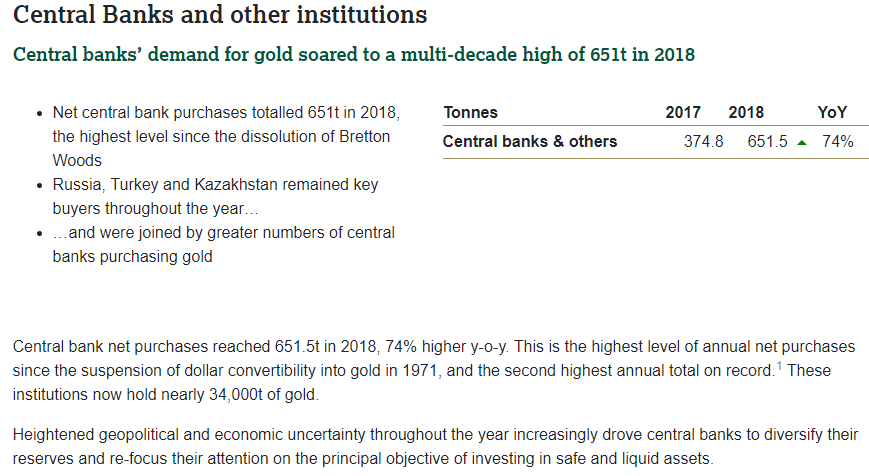

Look at those figures closely. Central Bank buying up 74% year-over-year! Highest annual net purchases since Nixon closed the gold window! These are some astounding figures that few are talking about. Everyone is babbling on about every Trump tweet or focusing on the minute-by-minute progress in the Chinese-American trade negotiations, yet right in front of us has been a dramatic shift in the demand picture of the gold market.

これらの図をよく見てほしい。YoYで中央銀行の買いが74%増えている!ニクソンがゴールド兌換を止めた年以来の買い入れだ!ほとんど誰もこのことを議論していないが、この事実はすごいことだ。だれもがトランプのツイートや米中貿易協議の細かな進展でおしゃべりしている、しかし我々の眼前にあるのはゴールド市場の需要に関する劇的な変化だ。

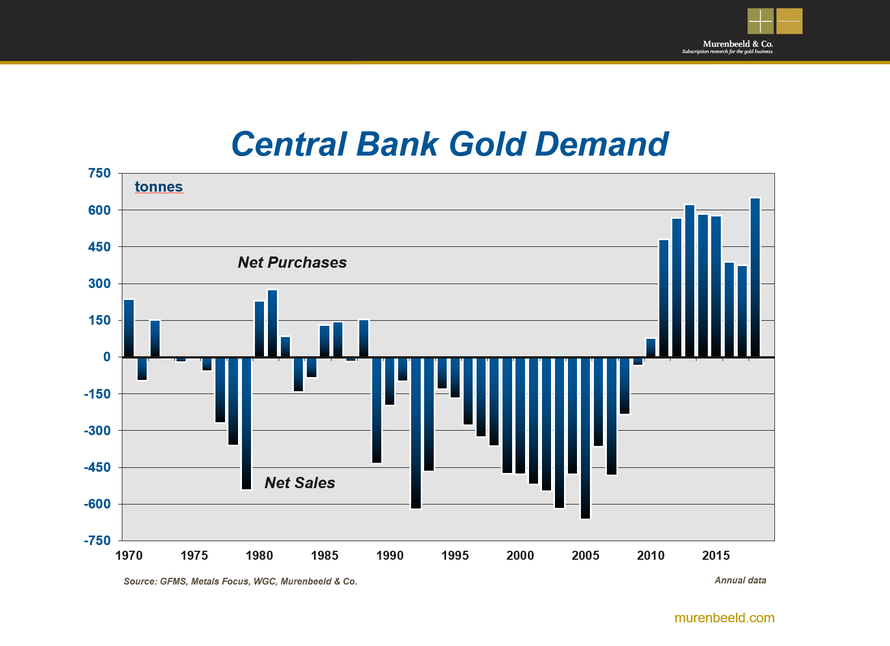

My good friends at Murenbeeld & Co. created this great chart for me that shows the net purchases by the Central Banks over the past few decades to get a sense of the scale of the buying.

Murenbeeld & Co.にいる私の古くからの友人がこの素晴らしいチャートを作ってくれた、ここ何十年かの中央銀行によるネットでの買いを示している、これを見ると買いのスケールが以下ほどのものかを把握できる。

It really drives home the change in trend. We went from sloppy back-and-forth Central Bank action in the 1970s, to just-get-it-off-the-sheets stupid selling in the 1990s and 2000s, to the recent buy-whatever-is-available-without-driving-the-price-too-high action.

このチャートは本当にトレンド変化を示している。1970年代には中央銀行は売ったり買ったりだった、1990年代と2000年代には馬鹿げた売りが続いた、最近では価格をあまり上昇させないように買い進んでいる。

For the past eight years Central Banks have been hovering gold faster than Lindsey Lohan downs greyhounds at her LL vodka launch party.

この8年、中央銀行は女優Lindsey Lohanがカクテルを飲み干すよりももっと早くゴールドを飲み込んでいる。

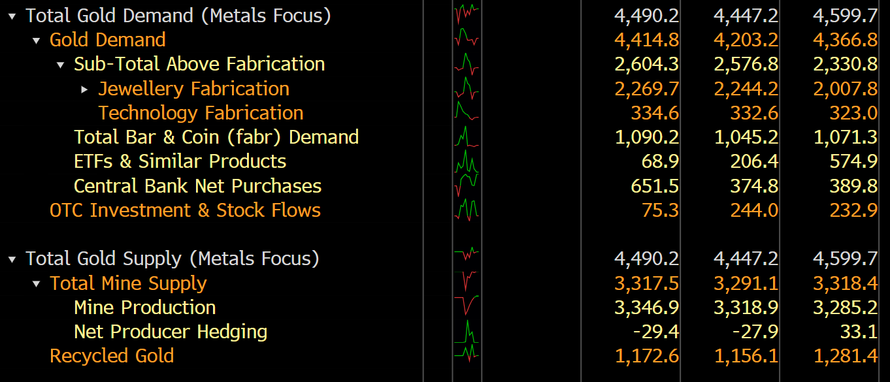

And it’s not like this is a small part of the gold supply-demand picture. There are approximately 3,300 tonnes of gold mined each year.

そしてこの規模は決してゴールドの需給からすると小さくない。毎年のゴールド産出量は3,300トン程度だ。

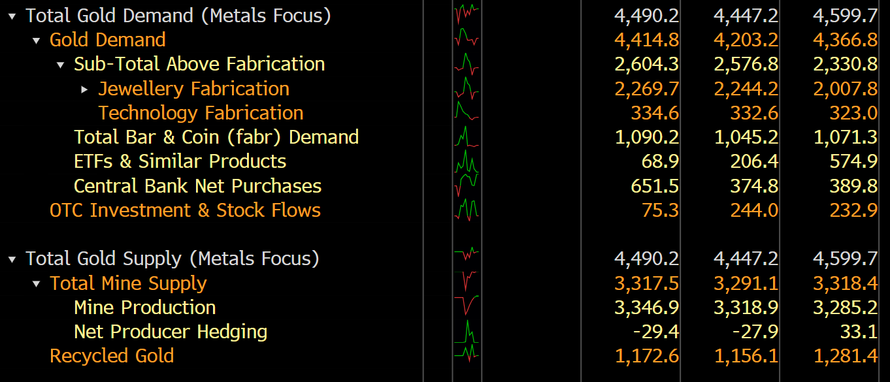

Here is a Bloomberg snapshot of the worldwide demand and supply picture over the past three years:

ここにブルームバーグが示すのは過去3年の世界需給だ:

If we think about the swing from 2005 when Central Banks sold 600 million tonnes of gold to last year when they bought approximately 600 million tonnes, it’s a demand shift of more than 35% of total supply.

2005年に中央銀行が600Mトンゴールドを売っていた時と昨年の600Mの買いとの振れ幅を考えると、この需要シフトは全供給の35%にもなる。

One of the best gold presentations ever created was from Grant Williams. It was titled “Nobody Cares” and I have highlighted it in previous MacroTourist posts.

Grant Williamsがゴールドに対するとても素晴らしい発表をした。そのタイトルは「誰も気にしない」そして私は以前のMacro Tourist記事でその要点を掻い摘んだ。

Although it was given in 2016, I think Grant’s points are all the more applicable today. In the presentation he goes through the numbers and shows how a little change in demand could have an outsized effect on prices. Grant thought this change in demand would come from investors, but what if he got the entity with the blue tickets wrong? What if it’s not investors who will come for the gold but instead the Central Banks?

再びその記事へのリンクを示した、誰もがもう一度この記事を読み直すことだろう。この記事が書かれたのは2016年のことだが、Grantの指摘は今でも通用すると私は思っている。彼が発表で数値を上げて解説したがほんの少し需要が変わるだけで大きく価格が動く。Grantoはこの需要をういだすのは投資家だと思っていた、しかし彼の推測が全く違っていたとしたら?ゴールドを取りに来るのが投資家でなく中央銀行だったとしたらどうだろう?

I have long postulated that someday the PBOC or the BOJ would come for gold in a big way, and that when that happened, gold wouldn’t be moving by $50s or $100s, but instead would explode higher by $500s or $1,000s. I know that seems preposterous, but stop and think about what the Swiss Central Bank, the ECB or the BOJ have done when it comes to monetizing their balance sheet over the past decade. Do you know what that sort of buying would do to the gold market?

For the past six years gold has been boring.

私はずっと想定していたが、いつの日かPBOCとかBOJが大きくゴールドを取りに来るのではないかと、そしてそういう事が起きると、ゴールドの値動きは$50とか$100なんてものではない、$500とか$1,000の規模で爆発的に上昇するだろう。これが馬鹿げた妄想であることは承知の上だ、しかしちょっと立ち止まって考えてみてほしい、スイス中央銀行やECBそしてBoJがこの10年自らのバランスシートを膨らませてきたことを。この手の買いがゴールド市場に向かった時どうなるかわかるだろうか?

これまで6年ほどゴールドは退屈だった。

All the gold bears have been gloating about precious metals’ terrible performance.

ゴールドへのベア派は貴金属のひどいパフォーマンスを嘲笑っていた。

I look at it differently. We have had a rip-roaring bull market in risk assets and gold has treaded water. To me, its performance has been encouraging.

私は見方は違う。我々はリスク資産の騒々しいブル相場を経験してきた、そしてゴールドは踏みにじられた。私にとってはそのパフォーマンスは勇気づけられるものだ。

The real reason I want to end with that long term chart is that it is easy to think that since we have rallied from $1,180 to $1,310 you have missed the move.

The fact that it is rallying when it shouldn’t only makes the recent moves all the more important. Think about how many long-term gold bulls have abandoned gold and are often now advocating waiting for it to decline to $800 or $900 before loading up the boat.

この長期チャートを示す本当の理由は、私どもは$1,180から$1,310までのラリーを見てきたが、皆さんはこのラリーを見逃したろう。本当はこのラリーが大切なのは最近の短期ラリーだけではないということだ。思い起こしてほしい、どれだけ多くの長期投資ゴールドブル派がゴールドを手放したことか、そして今やこの相場に乗り込む前にゴールドが$800とか$800に下落するのをバカのように待っていることか。

Well, I don’t know much, but I know that markets seldom make it so easy. To me the hard trade is to buy gold up here. It seems lofty and prone to a pullback. But the best bull markets get overbought and stay overbought.

そう、私も本当のことはよくわからない、むしろ相場はそう簡単ではないことも私は分かっている。私にとってここから高値でゴールドを買い込むことだ。今はとても高値で引き戻しそうにも見える。しかし、素晴らしいブル相場というものは買われすぎとなりさらに買われすぎとなるものだ。

I think Grant Williams’ theory is finally coming true - he just had the wrong buyer. Just imagine if he ends up being right about the rest of the traditional money management industry chasing gold in a desperate attempt to get even a small allocation to gold. Yeah, yeah, I know. Gold is a barbarous relic that has no economic value. Well, just don’t tell that to the Central Bankers who are loading up their vaults with it…

私自身はGrant Williamsの理論は最終的に正しいと思っているーー彼は買い場を間違った。ちょっと想像してほしい、もし彼が正しく、他の多くのマネーマネージャがたとえほんの少しでもゴールドを追いかけようとしたらどうなるか。そう、まったく、私は分かっている。ゴールドは未開の遺物であり、経済的な価値はない。そう、決してこのことを中央銀行には言わないことだ、彼らは自らの金庫を金塊でいっぱいにしようとしている・・・

I’ll warn you right off the bat, I have been waiting to write this piece for the past few days. You see, it’s a gold post, and as much as I try to take a bigger picture view, the trader-in-me still hates writing a bullish piece just as the market is about to have a minor correction. So I often get cute and wait for a dip before I publish.

But the gold decline refuses to materialize and I have decided to just post my piece - hoping I am not top-ticking this recent rally, but fearing it’s probably the surest sign we are headed lower over the short run.

私はすぐに警告しよう、私はこの記事を書くのを数日待っていた。ご存知の通りゴールドに関するものだ、私はできるだけ俯瞰図を書くように心がけよう、市場にはまだ小さな調整が待ち構えていそうで、私の中のトレーダーとしての立場としてはまだ強気の記事を書きたくない。というわけで私は記事を書くのに押し目を待っている。しかしゴールド下落は申告になりそうもなく、私はこの記事を書くことにしたーー私は最近のラリーを追いかけているわけではない、むしろ短期的には下落に向かう恐れを持っている。

Yet over the long-run, I contend something has changed in the gold market. Something we should all be paying attention to.

でも、長期的視点では、私はゴールド市場でなにか変化があったと信じている。誰もがこれに注目すべきだ。

まずはここ数年の値動きを見てみよう。昨年11月に、ゴールドは離陸した、$1180から$1320へとだ。

To some extent the initial move of November and December might be easily explained. Don’t forget that during this period the stock market was selling off hard and there was a fair amount of fear in the market.

11月12月の最初の値動きは簡単に説明できるかもしれない。忘れてはいけないが、この時期には株式市場は激しく下落し市場には恐怖心が蔓延していた。

But why hasn’t gold sold off in the past two months as the fear subsided?

You might argue that gold is simply rallying along with the decline in real yields. Powell’s historic flip-flop has certainly caused real rates to decline and help gold.

しかしこの2か月恐怖心が和らいでもどうしてゴールドは下落しなかったのか?金利が下がってきたために単にゴールドラリーがあったと皆さんは思うかもしれない。Powellの歴史的な転換はたしかに金利を引き下げゴールドの手助けになった。

However, many market participants believe gold’s price movement is best explained by movements in the US dollar.

しかしながら、市場参加者の多くはゴールド価格は米ドルの動きで説明できると信じているかもしれない。

For the first three quarters of 2018 gold was indeed trading almost lockstep inverse to the US dollar. The US dollar was going up while gold was falling tick-for-tick.

2018年の最初の3四半期はたしかにゴールドは米ドルとは逆に歩調を揃えた。米ドルの上昇に伴いゴールドは順次下落した。

Since October this relationship has broken down and now both securities are heading higher.

10月からはこの関連が壊れて今や両者は歩調を合わせて上昇している。

この状況を簡単に図示するのは他国通貨でゴールドチャートを見ることだ。

Whether it’s gold priced in CNY, EUR, JPY or AUD, it’s all the same chart - gold has had a strong rally in every currency.

CNY,EUR,JPYそしてAUDでゴールドの動きを見ると、どの通貨でもゴールドは強いラリーをしている。

Gold is not going up because of US dollar weakness - it’s going up in real terms.

The question is why?

米ドルが弱いからゴールドが上昇しているわけではないーー実際に上昇している。問題はどうしてかということだ

There is little doubt that the dovish tilt by Powell has helped gold, but if you look at when the rally started, it was way before his post-Christmas cave.

ほとんど疑いなくPowellのハト派視線がゴールドを助けた、しかしラリーが始まった時期を見ると、彼が発言したクリスマスイブよりずっと前のことだ。

I don’t have any wonderfully original insights to present to you today. Rather, what little I can offer is to connect some dots and make a guess that the timing is finally lining up for some bigger picture macro trends that have been brewing for some time.

今の所私は皆さんにお伝えできる素晴らしい独自の洞察が在るわけではない。むしろ、その要因を点から紡ぎあげることがほとんどできない、単に推測するだけだが、このタイミングの背景にはなにか大きなマクロトレンドが在るのではないかと想像する、どこかの時期から醸成されたものだ。

I urge you to read the recent report by the World Gold Council titled “Gold Demand Trends Full year and Q4 2018. From the executive summary:

私は最近のWrold Gold Councilの記事を読むことをおすすめする「2018Q4および通年のゴールド需要トレンド」。この要約はこういう具合だ:

Look at those figures closely. Central Bank buying up 74% year-over-year! Highest annual net purchases since Nixon closed the gold window! These are some astounding figures that few are talking about. Everyone is babbling on about every Trump tweet or focusing on the minute-by-minute progress in the Chinese-American trade negotiations, yet right in front of us has been a dramatic shift in the demand picture of the gold market.

これらの図をよく見てほしい。YoYで中央銀行の買いが74%増えている!ニクソンがゴールド兌換を止めた年以来の買い入れだ!ほとんど誰もこのことを議論していないが、この事実はすごいことだ。だれもがトランプのツイートや米中貿易協議の細かな進展でおしゃべりしている、しかし我々の眼前にあるのはゴールド市場の需要に関する劇的な変化だ。

My good friends at Murenbeeld & Co. created this great chart for me that shows the net purchases by the Central Banks over the past few decades to get a sense of the scale of the buying.

Murenbeeld & Co.にいる私の古くからの友人がこの素晴らしいチャートを作ってくれた、ここ何十年かの中央銀行によるネットでの買いを示している、これを見ると買いのスケールが以下ほどのものかを把握できる。

It really drives home the change in trend. We went from sloppy back-and-forth Central Bank action in the 1970s, to just-get-it-off-the-sheets stupid selling in the 1990s and 2000s, to the recent buy-whatever-is-available-without-driving-the-price-too-high action.

このチャートは本当にトレンド変化を示している。1970年代には中央銀行は売ったり買ったりだった、1990年代と2000年代には馬鹿げた売りが続いた、最近では価格をあまり上昇させないように買い進んでいる。

For the past eight years Central Banks have been hovering gold faster than Lindsey Lohan downs greyhounds at her LL vodka launch party.

この8年、中央銀行は女優Lindsey Lohanがカクテルを飲み干すよりももっと早くゴールドを飲み込んでいる。

And it’s not like this is a small part of the gold supply-demand picture. There are approximately 3,300 tonnes of gold mined each year.

そしてこの規模は決してゴールドの需給からすると小さくない。毎年のゴールド産出量は3,300トン程度だ。

Here is a Bloomberg snapshot of the worldwide demand and supply picture over the past three years:

ここにブルームバーグが示すのは過去3年の世界需給だ:

If we think about the swing from 2005 when Central Banks sold 600 million tonnes of gold to last year when they bought approximately 600 million tonnes, it’s a demand shift of more than 35% of total supply.

2005年に中央銀行が600Mトンゴールドを売っていた時と昨年の600Mの買いとの振れ幅を考えると、この需要シフトは全供給の35%にもなる。

One of the best gold presentations ever created was from Grant Williams. It was titled “Nobody Cares” and I have highlighted it in previous MacroTourist posts.

Grant Williamsがゴールドに対するとても素晴らしい発表をした。そのタイトルは「誰も気にしない」そして私は以前のMacro Tourist記事でその要点を掻い摘んだ。

-

PIMCO, GOLD BULL? - April 22nd, 2016

-

THE REAL MESSAGE FROM THE GDXJ MESS - April 19th, 2017

Although it was given in 2016, I think Grant’s points are all the more applicable today. In the presentation he goes through the numbers and shows how a little change in demand could have an outsized effect on prices. Grant thought this change in demand would come from investors, but what if he got the entity with the blue tickets wrong? What if it’s not investors who will come for the gold but instead the Central Banks?

再びその記事へのリンクを示した、誰もがもう一度この記事を読み直すことだろう。この記事が書かれたのは2016年のことだが、Grantの指摘は今でも通用すると私は思っている。彼が発表で数値を上げて解説したがほんの少し需要が変わるだけで大きく価格が動く。Grantoはこの需要をういだすのは投資家だと思っていた、しかし彼の推測が全く違っていたとしたら?ゴールドを取りに来るのが投資家でなく中央銀行だったとしたらどうだろう?

I have long postulated that someday the PBOC or the BOJ would come for gold in a big way, and that when that happened, gold wouldn’t be moving by $50s or $100s, but instead would explode higher by $500s or $1,000s. I know that seems preposterous, but stop and think about what the Swiss Central Bank, the ECB or the BOJ have done when it comes to monetizing their balance sheet over the past decade. Do you know what that sort of buying would do to the gold market?

For the past six years gold has been boring.

私はずっと想定していたが、いつの日かPBOCとかBOJが大きくゴールドを取りに来るのではないかと、そしてそういう事が起きると、ゴールドの値動きは$50とか$100なんてものではない、$500とか$1,000の規模で爆発的に上昇するだろう。これが馬鹿げた妄想であることは承知の上だ、しかしちょっと立ち止まって考えてみてほしい、スイス中央銀行やECBそしてBoJがこの10年自らのバランスシートを膨らませてきたことを。この手の買いがゴールド市場に向かった時どうなるかわかるだろうか?

これまで6年ほどゴールドは退屈だった。

All the gold bears have been gloating about precious metals’ terrible performance.

ゴールドへのベア派は貴金属のひどいパフォーマンスを嘲笑っていた。

I look at it differently. We have had a rip-roaring bull market in risk assets and gold has treaded water. To me, its performance has been encouraging.

私は見方は違う。我々はリスク資産の騒々しいブル相場を経験してきた、そしてゴールドは踏みにじられた。私にとってはそのパフォーマンスは勇気づけられるものだ。

The real reason I want to end with that long term chart is that it is easy to think that since we have rallied from $1,180 to $1,310 you have missed the move.

The fact that it is rallying when it shouldn’t only makes the recent moves all the more important. Think about how many long-term gold bulls have abandoned gold and are often now advocating waiting for it to decline to $800 or $900 before loading up the boat.

この長期チャートを示す本当の理由は、私どもは$1,180から$1,310までのラリーを見てきたが、皆さんはこのラリーを見逃したろう。本当はこのラリーが大切なのは最近の短期ラリーだけではないということだ。思い起こしてほしい、どれだけ多くの長期投資ゴールドブル派がゴールドを手放したことか、そして今やこの相場に乗り込む前にゴールドが$800とか$800に下落するのをバカのように待っていることか。

Well, I don’t know much, but I know that markets seldom make it so easy. To me the hard trade is to buy gold up here. It seems lofty and prone to a pullback. But the best bull markets get overbought and stay overbought.

そう、私も本当のことはよくわからない、むしろ相場はそう簡単ではないことも私は分かっている。私にとってここから高値でゴールドを買い込むことだ。今はとても高値で引き戻しそうにも見える。しかし、素晴らしいブル相場というものは買われすぎとなりさらに買われすぎとなるものだ。

I think Grant Williams’ theory is finally coming true - he just had the wrong buyer. Just imagine if he ends up being right about the rest of the traditional money management industry chasing gold in a desperate attempt to get even a small allocation to gold. Yeah, yeah, I know. Gold is a barbarous relic that has no economic value. Well, just don’t tell that to the Central Bankers who are loading up their vaults with it…

私自身はGrant Williamsの理論は最終的に正しいと思っているーー彼は買い場を間違った。ちょっと想像してほしい、もし彼が正しく、他の多くのマネーマネージャがたとえほんの少しでもゴールドを追いかけようとしたらどうなるか。そう、まったく、私は分かっている。ゴールドは未開の遺物であり、経済的な価値はない。そう、決してこのことを中央銀行には言わないことだ、彼らは自らの金庫を金塊でいっぱいにしようとしている・・・