For

those who have grown bored with the ongoing US-China trade war whose

escalation was obvious to all but the dumbest BTFD algos, the biggest

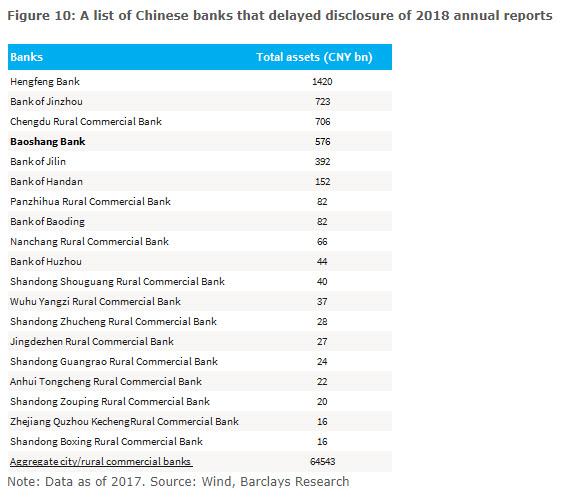

news of the past week was that yet another Chinese bank was bailed out by the Chinese

government - the third in the past three months - and a substantial one

at that: with over 1.4 trillion yuan in assets ($200BN), Hang Feng

Bank's nationalization was certainly large enough to make a dent on the

Chinese financial system and on the Chinese Sovereign Wealth Fund, which

drew the short straw and was told to bailout the troubled Chinese bank (more here).

Hang Feng's bailout followed those of Baoshang and Bank of Jinzhou, which means that 3 of the top 4 most troubled banks have now been either nationalized by an SOE or seized by the government, which is effectively the same thing.

Hang Feng救済はBaoshang とBank of Jinzhouに続くものであり、4大問題銀行の内3行がすでに国有化され、国有企業化政府に吸収された、どれも似たようなものだ。

Of course, to regular readers this development was hardly surprising,

especially after our post in mid-July when we saw the $40 trillion

Chinese banking system approach its closest encounter with the

proverbial "Lehman moment" yet, when inexplicably the four-day repo rate

on China’s government bonds (i.e., the cost for investors to pledge

their Chinese government bond holdings for short-term funding) on the

Shanghai exchange briefly spiked to 1,000% in afternoon trading.

While some attributed the surge to a fat finger, far more ominous

signs were already present, and in the aftermath of the Baoshang

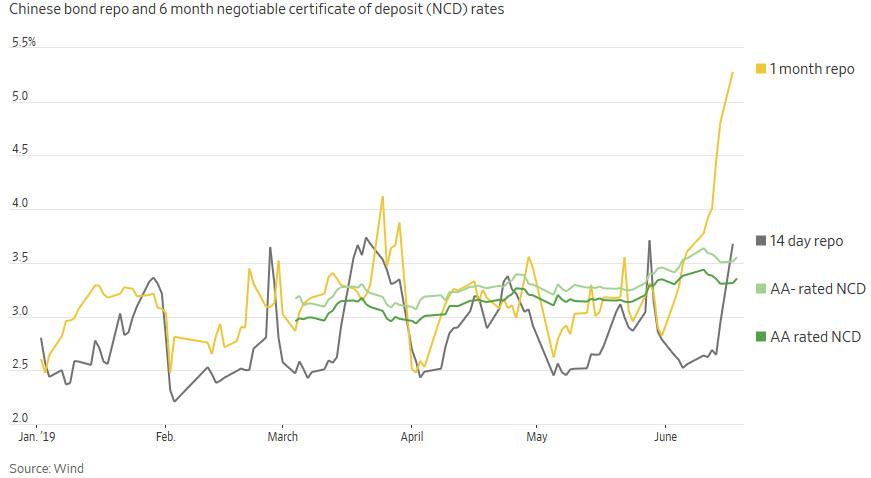

failure, which has sent Chinese banking stocks tumbling, one-day and

seven-day weighted average borrowing rates had remained low thanks to

huge central bank cash injections - such as the 250BN yuan we described back in May - longer tenors such as the 1 month repo have marched sharply higher.

And now, none other than Goldman points out that something is clearly

breaking inside China's banking system as one after another small bank

domino falls, and as following the Baoshang Bank takeover in late May,

interbank lenders have become more cautious towards the credit risk of

smaller and weaker financial institutions.

今や他でも無いゴールドマンがこう指摘する、中国銀行システム内部で明らかに何かが壊れている、小型銀行が次々と倒産するドミノが起きている、5月遅くにBaoshang Bank を接収した後、銀行間貸し手は更に注意深くなり、弱小金融機関の与信リスクを懸念している。

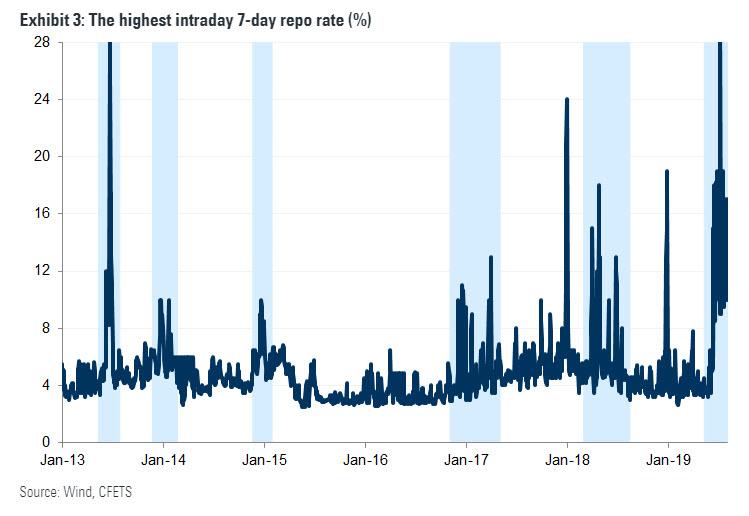

The result: a Chinese banking system in which banks have lost trust

in one another, manifested itself in much tighter liquidity in the

interbank market, with the highest intraday 7-day repo rates

staying above 8% over the past month as questions swirl over the

viability of the underlying collateral. In fact, as shown in

the chart below, the creeping funding freeze among Chinese banks is now

even worse compared to the historic episode in the summer of 2013 when

following an aggressive ramp up in Beijing's deleveraging campaign, repo

rates exploded to the point that banks effectively stopped interacting

with each other.

As Goldman observes, "the sustained spikes in intraday repo rates

suggest that some banks are still under pressure and are having to pay

higher costs to obtain funding in the interbank market. A number of

action has been taken to ease concerns regarding credit risk at smaller

banks, including the recent equity injection into Bank of Jinzhou by

ICBC Financial Asset Investment Company and China Cinda Asset

Management."

ゴールドマンの見立てでは、「日中のレポレートスパイクが常態化し、これはいくつかの銀行がまだ圧力下にあり、高い金利を負担してもインターバンク市場で資金調達せざるを得ない状況にあることを示している。小型銀行の与信リスク懸念を緩和するいくつかの措置が取られている、たとえば最近のICBC Financial Asset InvestmentCompanyとChina Cinda Asset ManagementからBank of Jinzhouへの資本注入だ。」

Nonetheless, as the bank concludes, "it will take more time before

market conditions will normalize." Meanwhile, if more banks from the

list above, or worse, larger banks, end up failing - and so far there is

every indication that the process is only getting worse - the Chinese

funding freeze could get so large that the most dreaded event finally

take place: a bank run among one of China's largest, state-owned banks,

which as a reminder, are also the largest in the world.

One final, if key, point: it's not just Chinese banks that are in

funding peril, Chinese corporations are are on the firing line, and as

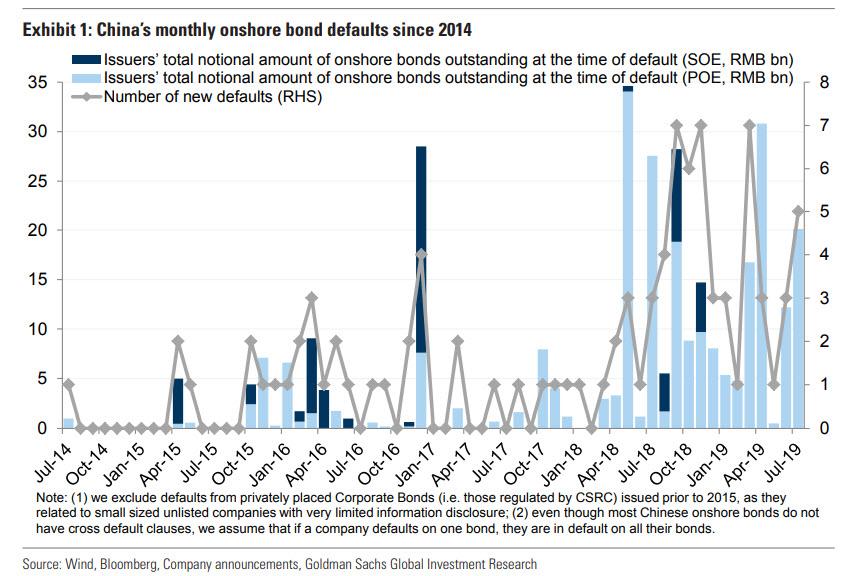

Goldman points out in the same report, the pace of China onshore bond

defaults is showing no signs of slowing down. According to the bank's

estimates there were five new defaults in July, bringing the total

number of new defaults this year to 23 (Exhibit 1), compared with 38 new

defaults that occurred in 2018. These 23 issuers had RMB 90.5bn of

onshore bonds outstanding at the time of default, equating to 0.5% of all onshore corporate bonds outstanding at the start of 2019. However,

all the defaults so far this year are from privately owned enterprises

(POEs), and the RMB 90.5bn of onshore bonds outstanding at the time of

default equates to 3.5% of all POE bonds outstanding at the start of

this year. To us, the elevated level of defaults continue to impact

weaker credit, as the net issuance of bonds rated AA or lower turned

negative in July.

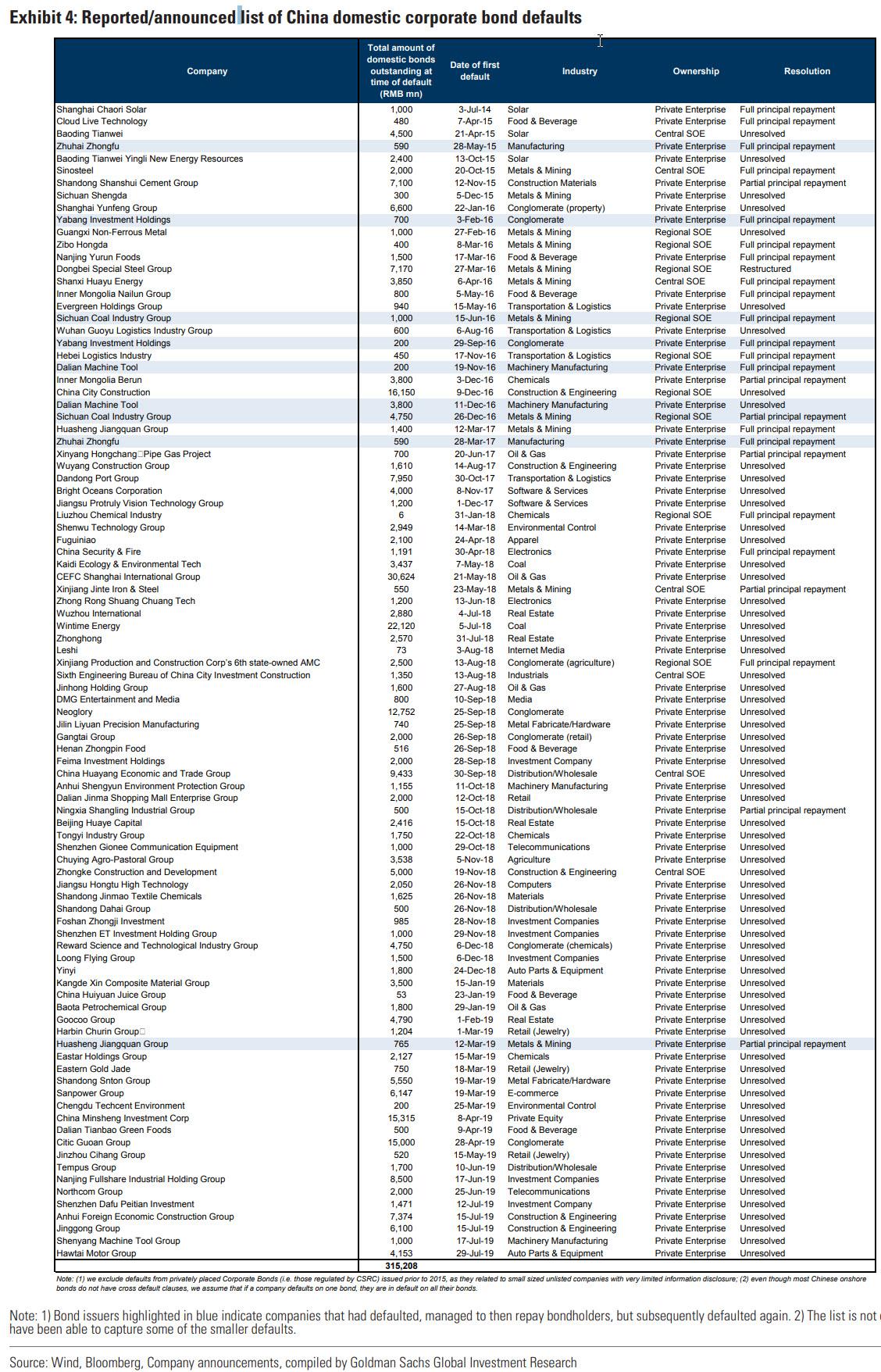

For those curious, below is a comprehensive, if not complete, list of

Chinese corporations that have defaulted since 2014, when China first

started permitting corporations to fail (smaller companies have been

omitted).

Class 8 Heavy Truck Orders Crash 68% in January by Tyler Durden Wed, 02/06/2019 - 17:25 Among the latest dismal news about the strength of the US economy, on Tuesday ACT Research released preliminary truck orders for January 2019 which showed that Class 8 truck orders collapsed an astounding 68% for January. The decline is being attributed to a 300,000+ vehicle backlog potentially prompting fleets to halt purchases in the near term. 米国経済に関し最近憂鬱なニュースが多い中で、火曜にACT researchが2019年1月のトラック発注を開示した、1月にClass 8のトラック発注がなんと68%も急落した。この発注減は短期的に300,000台超の潜在在庫を生み出す。 Specifically, in January Class 8 net orders were 15,800 units (14,700 SA; 176,400 SAAR), down 68% YoY and down 26% MoM. Class 5- 7 January net orders were 23,400...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...

中国が債務増加していることはたしかです。ただ日本の例を日銀資金循環報告でみると家計、320兆円、民間非金融機関1,785兆円、一般政府 1,284兆円となります。合算すると3,300兆円にもなり、GDPの600%を超えています。 https://www.boj.or.jp/statistics/sj/sjexp.pdf この記事の統計と同じ考え方で数値を採用しているのかどうか気になります。 加えて、この資金循環報告に書かれている海外資産というのが内数なのか外数なのか?私にはよくわかりません。当然海外債務も結構な額になります。一度日銀資金循環 図表1を見てください。詳しい方に教えていただければ。 この中国のたどる道は昔のソ連とかMMTと同様で、自国通貨ならいくら発行しても倒産はしない、というか為政者が痛みに耐えることができず緩和を続けるというものです。でも最終的には限界点に達します。ソ連は建国から崩壊まで70年かかりました。 自由主義経済なら立ち行かなくなった企業は退場してもらうというのが減速なのですが、これがうまくゆかないわけです。 でも日本は中国のはるか先を言っているように見えます。ちょっと検索したのですが、日本の債務に関しては政府債務に言及したものばかりで、この記事のように民間、個人まで総合的に記載しているのは日銀の資金循環統計しか見つけることができませんでした。 China Continues To Pile Debt On Top Of More Debt Written by Jesse Colombo | Feb, 27, 2019 Like many countries, China attempted to rein in its debt growth over the past couple years, but ultimately gave up and is now back to piling on even more debt. Bloomberg reports – 多くの国と同様に、中国もここ2年ほど債務増加を抑えようとしてきた、しかし結局の所諦めてしまい、今や更に債務を積み上げている。ブルームバーグ記事ーー For almost two years,...

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...