Last

Friday afternoon, when what few traders were not on vacation were

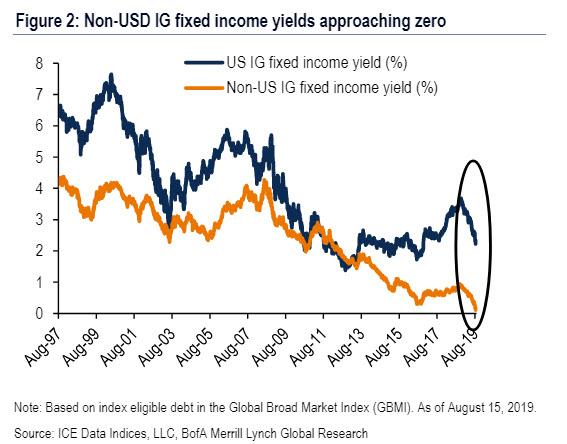

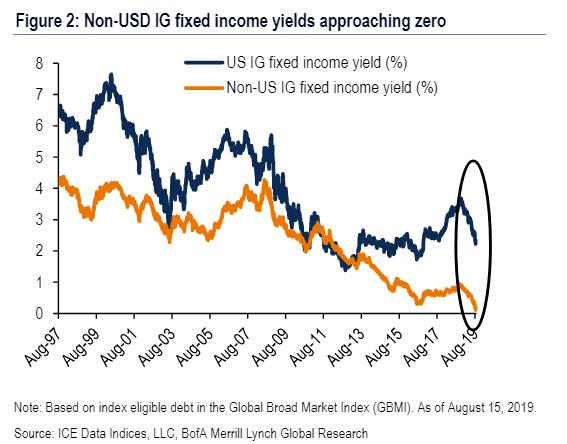

planning the venue of their evening alcohol consumption, we showed a remarkable analysis by Bank of America, which found that yields on the $27.8 trillion non-USD global

investment grade bond market had declined to just 16bps and that the US

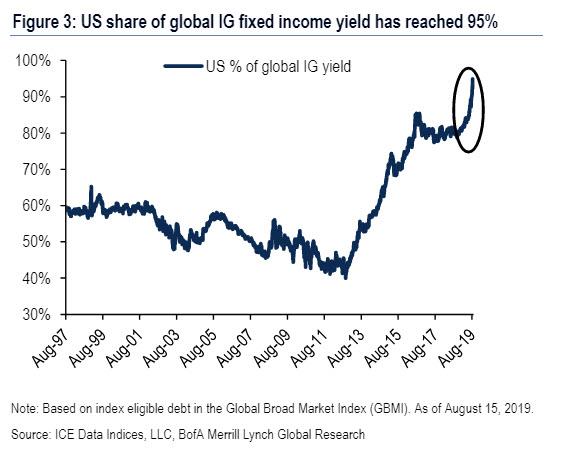

share of global investment grade yields has climbed to 94%. But the

punchline is that, as we said, "non-USD sovereign yields had

dropped to just 2bps, meaning that any day now foreign sovereign debt

may have no yield at all on average."

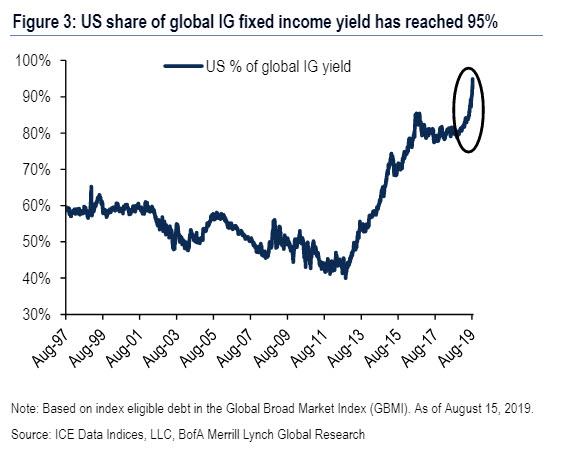

Fast forward to Monday, when following another surge in global bond

prices, Bank of America refreshed its analysis, and foudn that the

striking trends noted last week had become even more fascinating, to wit

yields on the $27.8tn non-USD global IG fixed income market had

declined to just 11bps (down from 16bps just one day earlier)...

... and the US share of global IG yields climbed to 95%...

... meaning that any foreign investor who is desperate for even the

smallest trace of positive yield has no choice but to come to the US,

something Kyle Bass echoed earlier on CNBC: "US rates are going to zero

because they are the only DM yields with an integer in front of them."

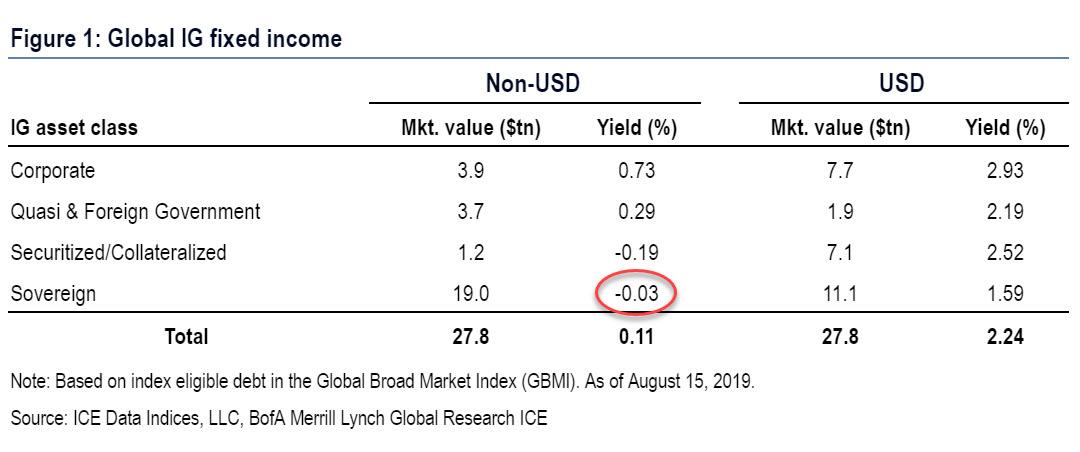

But the biggest shock is that for Albert Edwards, vindication is here

if only outside the US for now: as per the BofA update, non-USD

sovereign yields on $19 trillion in global debt - which was a paltry but

positive +0.02% on Friday - have now turned negative on average for the

first time ever at -3bps.

The silver lining: for now the average US sovereign yield is like a

beacon for foreign investors, offering a "juicy" 1.59% but we fully

expect this number to keep dropping as offshore pension funds rush to

lock in positive yields while they can; naturally any further Fed rate

cuts or "some QE" will only bring the US D-Day that much closer.

It's not just us: commenting on the Japanification of the world, Bank

of America's Hans Mikkelsen wrote that "we continue to think there is a

wall of new money being forced into the global corporate bond market"

and adds that "the trigger is lower interest rate volatility or simply

the passage of time, as a lot of foreign investors are being charged

(negative yields) for being underinvested."

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....