With

the world's central banks aggressively easing monetary policy overnight

as analysts watch in stunned amazement as the world's interest rate

careens ever faster toward zero, Trump is angrily watching the dollar as

it keeps rising day after day, bringing us ever closer to the moment

the US president declares on twitter a "national emergency" over the dollar and unleashes a major dollar devaluation.

Which is why it is not at all surprising that today Bank of America

has published a report warning that FX intervention risks are rising, in

which the bank notes that it is inclined to think the first stage of any

policy shift from the Administration will be to discard the strong USD

policy and hope/persuade the Fed to ease rates further. It is

also not surprising that BofA's FX strategist Kamal Sherma believes the

odds of intervention to weaken USD have risen in light of this week's

developments, but the success of any such actions would depend on a

number of factors including the parameters around which intervention

would occur.

Here Sharma reminds us of the textbook example of successful FX

intervention, namely the Plaza Accord of 1985 when the G-5 nations

coordinated to weaken USD.

So is another Plaza Accord imminent? As the FX strategist explains

below, there are similarities between events then and now, but also

crucial differences that lead him to conclude the US Administration will

not be able to rely on its major trading partners to help weaken the

USD.

The Plaza Accord revisited プラザ合意 再検討

As Bank of America writes, September 22 marks 34 years since the G5

leaders signed a collective agreement to weaken the USD against the

backdrop of growing internal and external US imbalances (the dual

deficit). The Plaza Accord is widely held as the most successful

episode of coordinated FX intervention and in the following two years,

the USD TWI fell nearly 50%. But, while the Plaza Accord is

often viewed through the prism of coordinated FX intervention to weaken

USD, the basis of the Accord was built on specific economic pledges:

Coordinated FX intervention was therefore part of an overall

strategy to address the internal/external imbalances that drove USD

appreciation. Though the Accord was ostensibly designed to help

alleviate US imbalances versus other G-5 nations, Plaza is seen by

economists as a direct response from the US of threat from Japan's

growing status as an economic superpower. It is consequently seen as the catalyst for Japan's lost decade of growth through the 1990s. 協調為替介入は米ドル評価適正化のために内外不均衡を全体的に調整するというものだった。この合意は表向きはG5諸国に対する米国の不均衡の痛みを緩和するものだったが、エコノミストからは日本の成長が経済的スーパーパワーとなり米国の脅威となることに対する直接対処だった。その結果としてこれをきっかけとして日本は1990年代までの失われた10年を迎えることになる。 Some history 関連する歴史事項

In the run up to the 1985 Accord, the USD TWI appreciated 55% making

it the largest percentage rally in the USD in the past 50 years taking

place against the backdrop of tight monetary policy (under Fed Chair

Volcker) and expansionary fiscal policy (Reaganomics). Martin Feldstein

(former Chair of Council of Economic Advisors) has argued that USD

strength was not the problem; it was symptomatic of the US policy mix. US financial conditions (according to the Chicago Fed, Chart 2) are comparable to current levels. To

date, USD has appreciated by nearly 40% since its 2011 lows, and while

there are similarities between the narrative in 1985 and now (increasing

protectionist policies from the US Administration, concern over

Japanese economic dominance), there are also differences between 1985

and the present period. In 1985, USD strength prompted extensive

lobbying by US industry to weaken the greenback. While recent US

earnings statements make it clear that there are rising FX headwinds to

profits, systematic calls from US industry to weaken the USD have been

largely contained (perhaps thanks to the offsetting benefit of record

stock buybacks). In addition, while the driver of USD strength through

the early 1980s was largely a function of the US domestic policy mix, the

US Administration currently views dollar strength as a function of

global central banks deliberately keeping policy loose in an effort to

prevent respective currency appreciation. 1985年の合意までに、貿易平均USDは55%も上昇していた、過去50年でもっとも大きなラリーだった、その原因はボルカーFED議長の引き締め政策とレーガン大統領による財政拡大にあった。元財政諮問委員会議長のMartin Feldstein は強いドルは問題ではないと主張した;問題は米国のポリシーミックスだと言った。米国の財政状況(シカゴFED、チャート2)は現在とよく似ている。現在までに、USDは2011年の安値から40%も上昇した、そして1985年当時と現在は似通ったところがある(米国政府からの保護主義が台頭し、日本の経済的覇権が懸念された)、たしかに1985年当時と現在に異なる点もある。1985年当時、強いUSDのために産業界からドルを弱めるように強い要望があった。最近の米国企業の決算収益をみると為替が向かい風なのは明らかだが、しかしながら産業界から米ドルを弱めるようにという主張は抑えられている(多分記録的な自社株買いの効果で相殺されているためだ)。更に加えると、1980年代前半の強いドルを支えていたのはおもに米国国内のポリシーミックスによるものだったが、しかしながら、現在米国政府はドルの強さを世界の中央銀行の意図的な緩和策のためと見ている、自国通貨が好まれないように金利を下げている結果だと。

Meanwhile, as Sharma notes, inflation targeting is increasingly

becoming an ineffective tool and as central bank policy rates once again

synchronize the result has been a policy of benign neglect toward FX.

As the BofA strategist puts it, a weak currency suits the needs of many policy officials outside of the US and

the recent downgrade by the ECB to its inflation projections suggests

little motivation to challenge current exchange arrangements agreed in

G7 communiqués. This is important because many countries (particularly

France and Germany) were concerned about a weakening of their respective

currencies versus USD in 1985. G5 countries were therefore a willing

partner in efforts to weaken the USD. Now, FX is an essential part of

the policy armory. Europe and Japan are now more accepting of FX weakness than FX strength. それと同時に、Sharmaはこう書く、インフレ目標がどんどん無効なツールとなり、多くの中央銀行の金利政策が同期してゆるやかに為替を下げている。このBoAストラテジストはこの状況をみて、米国外の多くの政策立案者は弱い自国通貨を求め、そして最近ECBはインフレ目標も下げたわけで、為替に関するG7合意声明を守ろうという意思は殆ど見えない。この点がとても重要で、多くの国、特にドイツとフランスは1985年当時自国通貨が対ドルで弱くなることを懸念していた。G5各国はUSDを安くすることを望んでいた。しかし今や、為替は基本的な政策兵器庫である。欧州も日本もいまは弱い自国通貨を望んでいる。

According to some estimates, the combined interventions by G5 totaled

$10bn. According to the BIS Triennial Survey, average daily FX turnover

in 1989 was $655bn. Assuming a turnover figure of $500bn for 1985,

total Plaza Accord intervention, accounted for around 2% of daily market

turnover. With current daily turnover at $5.5tn, an equivalent amount of intervention would imply over $100bn in FX. According

to BofA calculations, the US could muster reserves in excess of these

levels (~$140bn), although it is clear that the amounts of intervention

would have to be substantial and sustained for it to be credible.

Meanwhile, in subsequent years, the Bank of Japan intervened on 126 days

between January 2003 and March 2004, purchasing over $315bn to weaken JPY. This

was a sustained period of intervention, but question marks remain over

its long-term efficacy (note: such interventions were disastrous and

only the current period of QQE helped stabilize the yen decidedly below

100 vs the USD).

The effectiveness of interventions has more broadly

involved the element of surprise and positioning: of note, BofA's own

proprietary indicators do not suggest investors are holding sizeable USD longs positions to make USD selling intervention have sustained impact.

在る見積もりによると、G5協調介入総額は$10Bだった。BISの3年ごとの調査によると、1989年当時毎日の平均為替取引は$655Bだった。1985年当時の為替取引を$500Bと仮定すると、プラザ合意の全介入費用は毎日の取引の2%ということになる。現在では毎日の為替取引は$5.5Tにもなり、同様の介入を行うなら$100B以上の費用を要する。BoAの試算では、米国はこのレベルの資金(約$140B)ならかき集めることができる、しかしながら、明らかにこのレベルの介入が有効なのも信頼関係があってのことだ。やがてその数年後に、日銀が2003年1月から2004年3月まで126日間介入を行った、JPYを弱めるために$315B以上の買取を行ったのだ。この期間というのは介入を行った期間だ、しかし長期的な有効性には疑念が残る(メモ:この介入は悲惨なものだった、そして現在のQQEでJPYは対ドルで確実に100より安くなっている)。介入の有効性は意外性とその規模によるものだ、BoAの見立てでは、USD売り介入が持続的な影響を持つほどには投資家は大きなUSDロングポジションを持っていない。 How to measure success 介入成功をどう判定するか

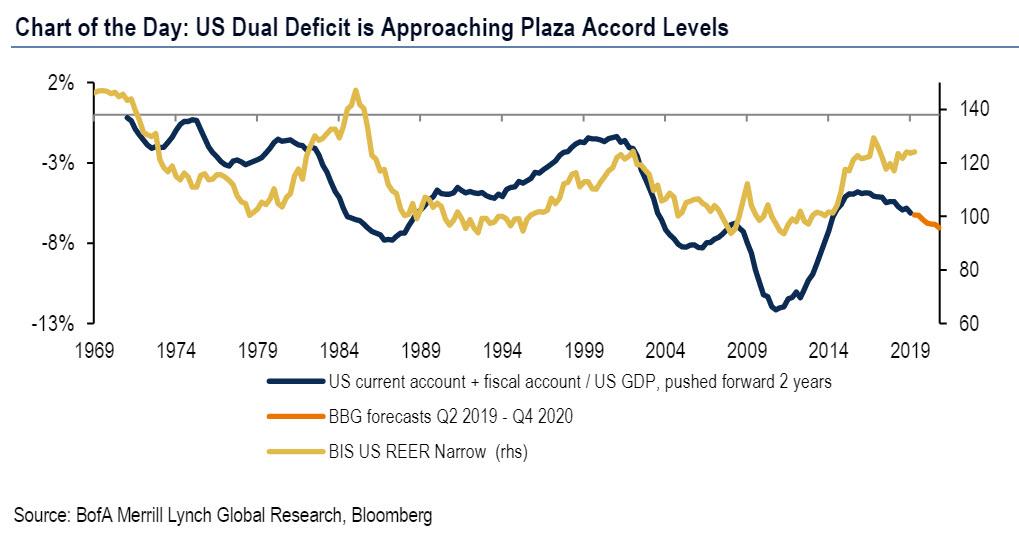

As shown below in the bank's Chart of the Day: "US Dual Deficit is

Approaching Plaza Accord Levels", the rapid depreciation of the USD

following Plaza eventually led to a steady improvement in the dual

deficit. However, the issue for the Trump Administration is

whether that improvement can come ahead of the 2020 Presidential

election for him to claim that his interventionist policy has been a

success. His 2016 campaign pledge to narrow the US trade

deficit (particularly with China) is currently at odds with the dynamics

of external US trade data, which show the merchandise deficit with

China hitting a five-year high in June.

下のチャートはBoAによるChart of the Day だ:「米国の双子の赤字はプラザ合意レベルに近づいている」、プラザ合意後のUSD下落はやがて双子の赤字を安定的に解消した。しかしながら、トランプ政権に取っての問題は、この改善が2020年の大統領選挙の前に実現するかどうかだ、彼は選挙で介入政策の政策を主張したい。彼の2016年選挙公約は貿易赤字の削減(特に対中国)だったが、6月には対中国貿易は5年ぶりの大幅赤字になっている。

Indeed, as noted above, the complicating factor for the US Administration is whether any depreciation of USD will lead to a material improvement in the trade deficit in time for the 2020 election. The

J-curve theory suggests a country's trade deficit will initially

deteriorate following currency devaluation.

Certainly the evidence from

UK and Canadian trade data suggests both deficits have not materially

improved since the financial crisis despite the 20% and 30%

depreciations of CAD and GBP TWI respectively. What is clear is that

with 15 months left until the 2020 Presidential election, any

depreciation in USD is unlikely to have a material impact on the US

trade balance. The US current account deficit continued to deteriorate

until 1987, two years after the Plaza Accord.

What to expect in the coming months? 今後数ヶ月はどうなる?

Ironically, the Osaka G20 Summit held earlier this year reiterated

its commitments from March 2018 to refrain from FX intervention:

"Flexible exchange rates, where feasible, can serve as a shock

absorber. We recognize that excessive volatility or disorderly movements

in exchange rates can have adverse implications for economic and

financial stability. We will refrain from competitive devaluations, and

will not target our exchange rates for competitive purposes".

We say ironically, because the latest G20 Communiqué is

effectively the antithesis of the 1985 Plaza Accord and along the with

the US Administration's strong USD policy are two initial challenges

that it faces were it to intervene. Here, BofA would focus

strongly on the Administrations' commentary around both areas as signs

that it is moving toward a more interventionist approach.

One way that this could be formalized is firming up the commitments

around the US Treasury FX Manipulation Report, which is due for release

in October, even though we already know that China will be declared a

manipulator. At present, BofA sees bilateral negotiation as the only

recourse the US has if it labels a country as a currency manipulator.

There is one other possibility: the US could revise the framework around

the FX Manipulation Report so it includes a new metric that

takes into account the relative monetary policy stance of foreign

central banks as a de facto signal that they have a policy of benign

neglect toward their currency. Either the country in question

reverses course on its monetary policy, or the US Authorities reserve

the right to intervene to weaken the USD to create a "level playing

field".

And since not a single foreign central bank will concede to such a

requirement in a time when the global race to the bottom, as the name

suggest is "global", the US will have free reign to finally unleash hell

on the dollar.

Finally, we remind readers of an unorthodox - if highly efficient -

method to devalue the dollar that was proposed by bond trading legend,

and MOVE index creator, Harley Bassman back in 2016 when he worked for

PIMCO - the Fed buying gold.

Before all is said and done and the central banks' reign of terror is

finally over, we are certain that this dramatic step will also be

attempted.

中国が債務増加していることはたしかです。ただ日本の例を日銀資金循環報告でみると家計、320兆円、民間非金融機関1,785兆円、一般政府 1,284兆円となります。合算すると3,300兆円にもなり、GDPの600%を超えています。 https://www.boj.or.jp/statistics/sj/sjexp.pdf この記事の統計と同じ考え方で数値を採用しているのかどうか気になります。 加えて、この資金循環報告に書かれている海外資産というのが内数なのか外数なのか?私にはよくわかりません。当然海外債務も結構な額になります。一度日銀資金循環 図表1を見てください。詳しい方に教えていただければ。 この中国のたどる道は昔のソ連とかMMTと同様で、自国通貨ならいくら発行しても倒産はしない、というか為政者が痛みに耐えることができず緩和を続けるというものです。でも最終的には限界点に達します。ソ連は建国から崩壊まで70年かかりました。 自由主義経済なら立ち行かなくなった企業は退場してもらうというのが減速なのですが、これがうまくゆかないわけです。 でも日本は中国のはるか先を言っているように見えます。ちょっと検索したのですが、日本の債務に関しては政府債務に言及したものばかりで、この記事のように民間、個人まで総合的に記載しているのは日銀の資金循環統計しか見つけることができませんでした。 China Continues To Pile Debt On Top Of More Debt Written by Jesse Colombo | Feb, 27, 2019 Like many countries, China attempted to rein in its debt growth over the past couple years, but ultimately gave up and is now back to piling on even more debt. Bloomberg reports – 多くの国と同様に、中国もここ2年ほど債務増加を抑えようとしてきた、しかし結局の所諦めてしまい、今や更に債務を積み上げている。ブルームバーグ記事ーー For almost two years,...

Class 8 Heavy Truck Orders Crash 68% in January by Tyler Durden Wed, 02/06/2019 - 17:25 Among the latest dismal news about the strength of the US economy, on Tuesday ACT Research released preliminary truck orders for January 2019 which showed that Class 8 truck orders collapsed an astounding 68% for January. The decline is being attributed to a 300,000+ vehicle backlog potentially prompting fleets to halt purchases in the near term. 米国経済に関し最近憂鬱なニュースが多い中で、火曜にACT researchが2019年1月のトラック発注を開示した、1月にClass 8のトラック発注がなんと68%も急落した。この発注減は短期的に300,000台超の潜在在庫を生み出す。 Specifically, in January Class 8 net orders were 15,800 units (14,700 SA; 176,400 SAAR), down 68% YoY and down 26% MoM. Class 5- 7 January net orders were 23,400...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...