What a difference a few years makes. Back in the summer of 2015, a WSJ op-ed writer, who somehow was unaware of the past 6,000 years of human history, infamously and embarrassingly said "Let’s Be Honest About Gold: It’s a Pet Rock."

Fast forward to today, when with every central bank once again rushing

to debase its currency in what increasingly appears to be the final race

to the debasement bottom, when even BOE head Mark Carney recommends

that it is time to retire the dollar as the world's reserve currency, pet rock gold has emerged as the second best performing asset of the year... and at the rate it is going -4th in 2017, 3rd in 2018, 2nd in 2019 - gold will be the standout asset class of 2020.

Which naturally has sparked comparisons for gold's performance in

2019 with 2008+, when gold exploded higher as the financial system

nearly collapsed and central banks started injecting trillions in

liquidity into the system to keep it afloat.

Are such comparisons appropriate?

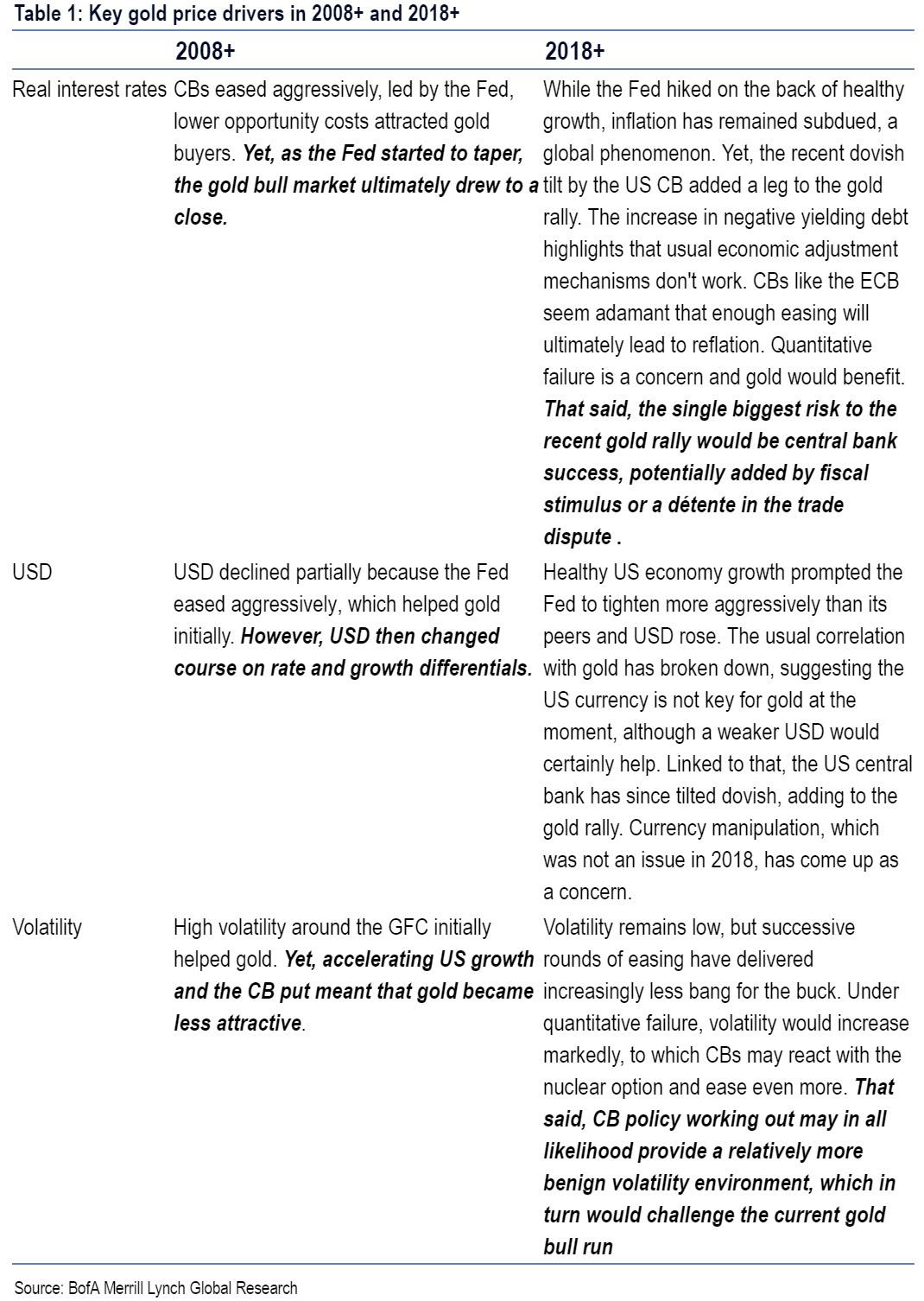

As Bank of America writes in "anatomy of two gold bull markets", in comparing the gold bull markets in 2008 and 2018, real rates remain key price drivers,

while a critical difference in market dynamics - this time around - is

that central banks have been unable to reflate global economies and

even as metrics like the value and proportion of negative yielding

assets has been increasing, further easing is on the cards. Linked to

that, Bank of America makes a stunning admissions: "the risk of quantitative failure, which was not a concern in 2008, makes gold an attractive asset."

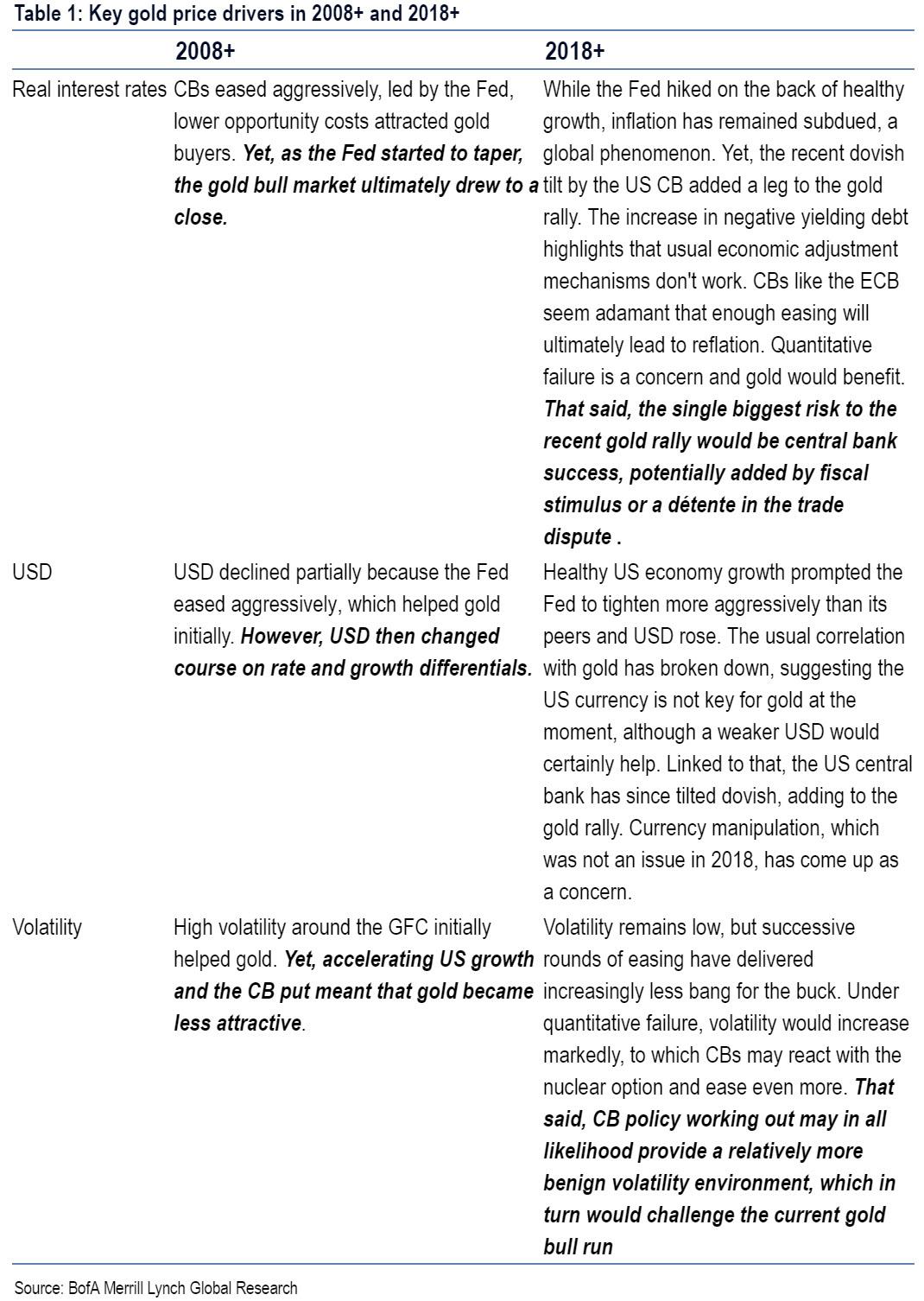

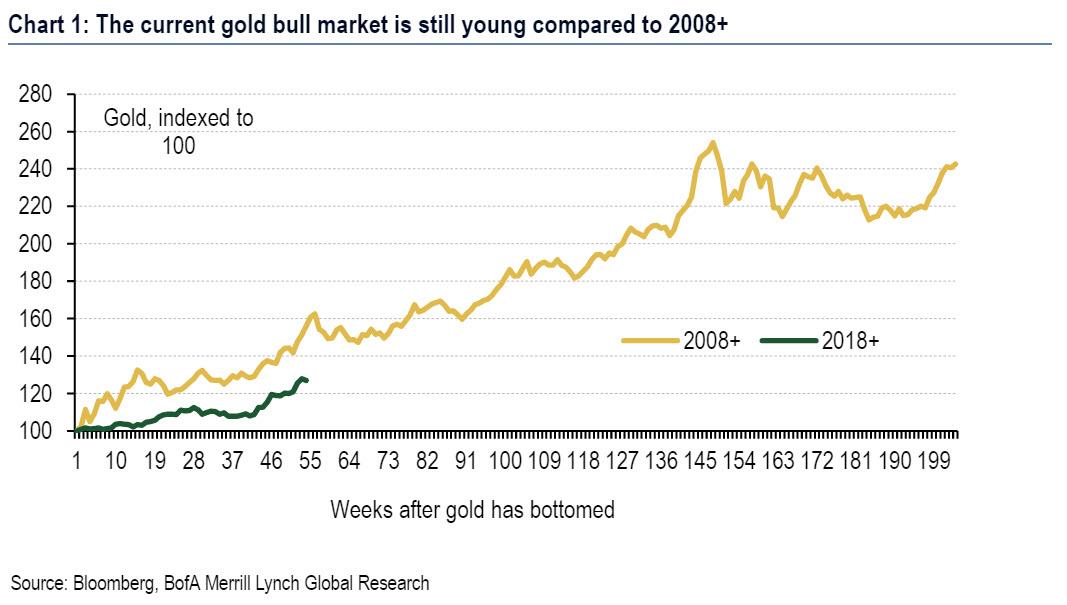

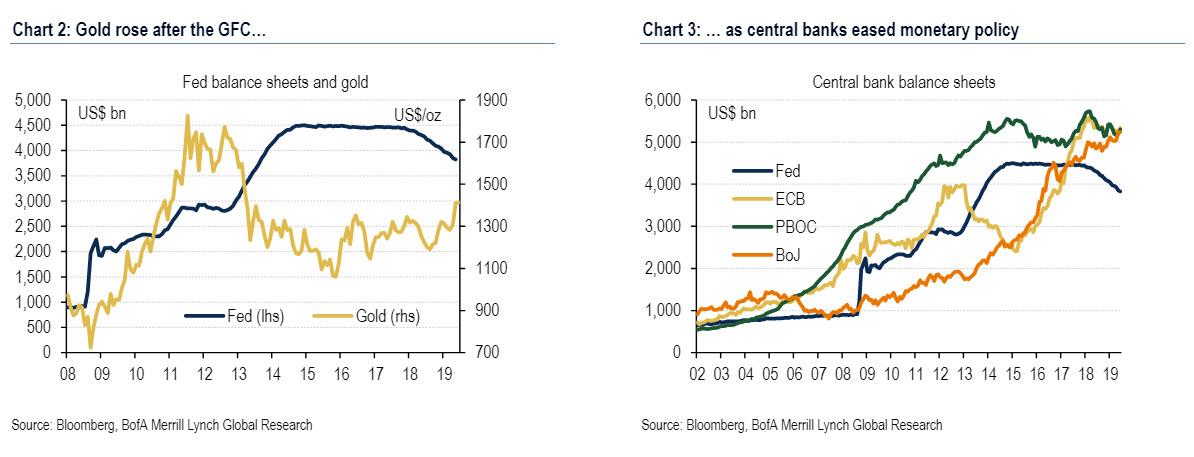

Taking a step back, for those who have not been following the

performance of gold in the past year, the yellow metal has been one of

the best performing commodities over the past year, rallying by 31%

since bottoming in August 2018, as whon in the first chart which

highlights that recent price dynamics have to some extent mirrored those

seen in 2008+; the data also shows that the current bull market is

still young. Partially because of that, Bank of America notes that it

has been frequently been asked how the current macro backdrop compares

to dynamics 10 years ago.

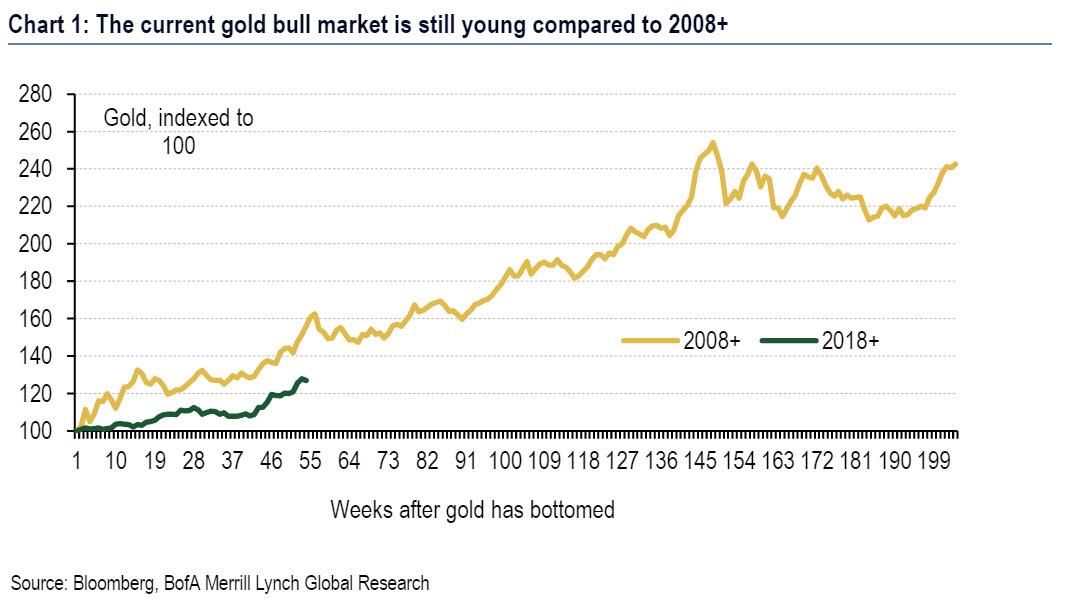

So what sparked the tremendous 2008 rally which lasted for the next three years?

では2008年の素晴らしいラリーは何が原因だったのだろう、しかもその後三年も続いた。

Looking back at the Great Financial Crisis, central banks reacted to

the turmoil on financial markets by easing monetary policy through both

traditional, but increasingly also non-traditional policy tools

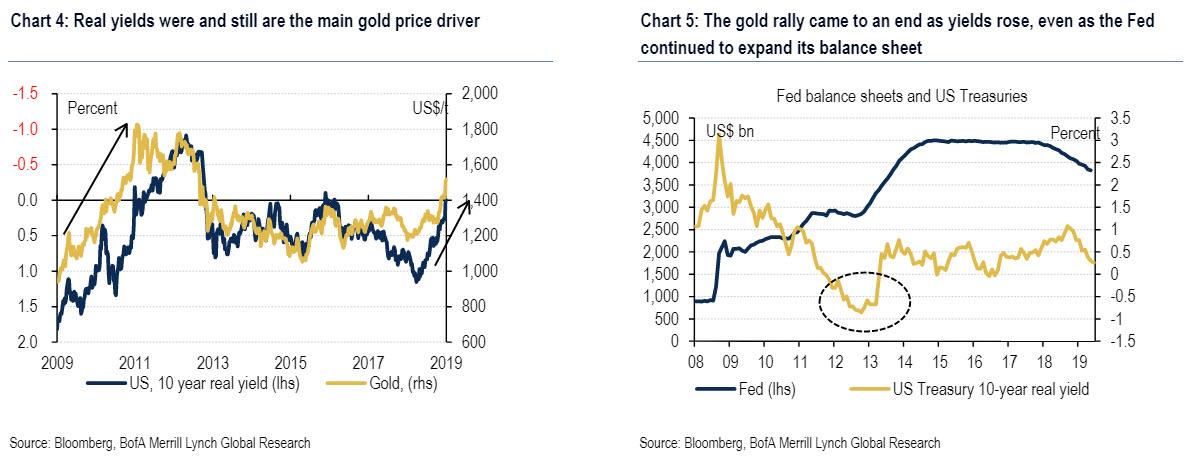

Since gold is a non-yielding asset, the reduction in opportunity

costs and uncertainty over where the global economy and markets were

headed made the commodity an interesting investment.

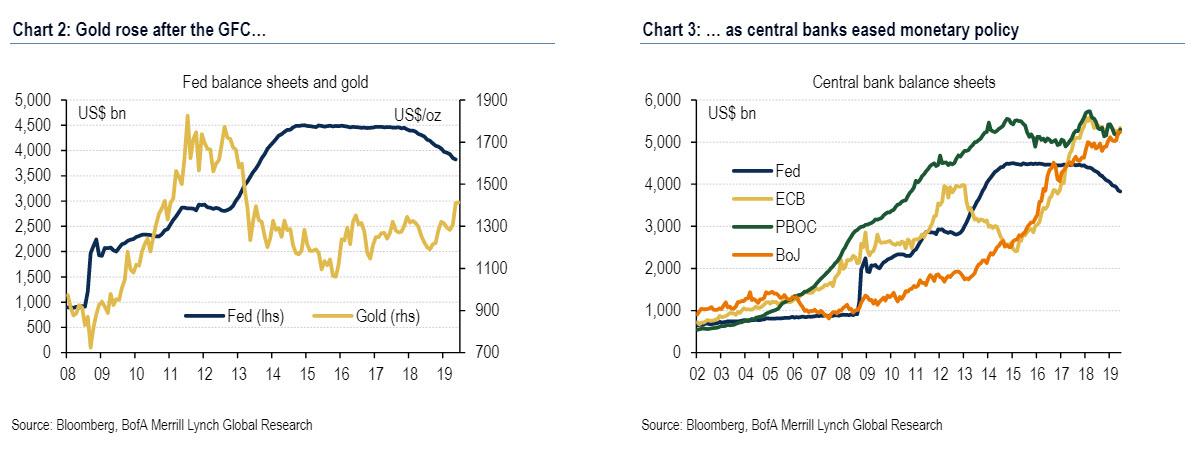

This is shown in Chart 4, which suggests that sharp declines in US real rates post GFC were accompanied by steady increases in gold quotations. Yet,

US rates then started to change direction in 2013, the year Fed

chairman Ben Bernanke caused the taper tantrum announcing that the Fed

would gradually reduce its bond purchases (Chart 5). This effectively

put an end to gold increases.

この状況はChart 4に示される、GFC後の米国実質金利が急落しそれにともな013いゴールド相場が安定して上昇している。しかし2013年に米国金利がその動きを変えた、この年FED議長 Ben Bernankeがtaper tantrumを引き起こしたのだ、FEDが徐々に債権買取を減らすと宣言した(Chart 5).これが実質的にゴールド上昇に終わりを告げた。

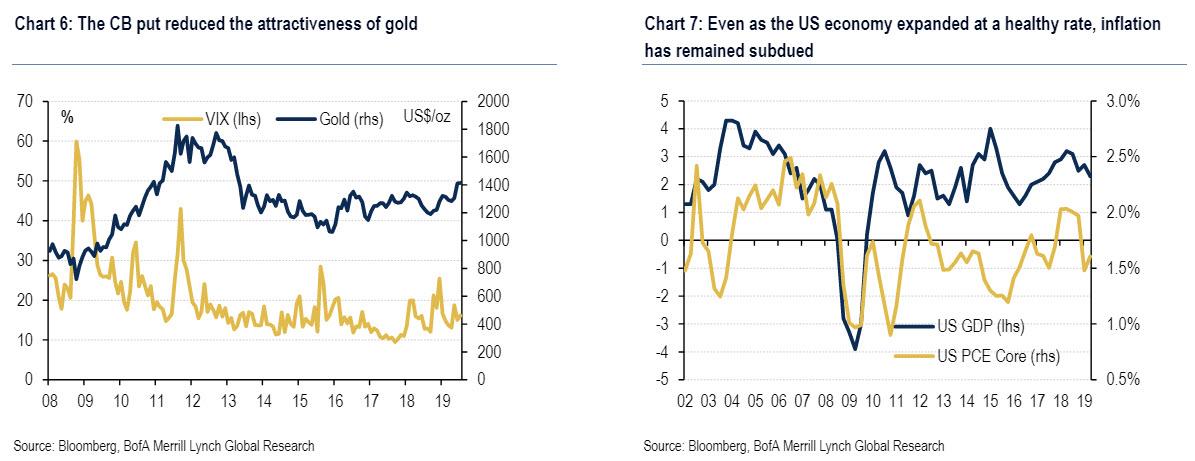

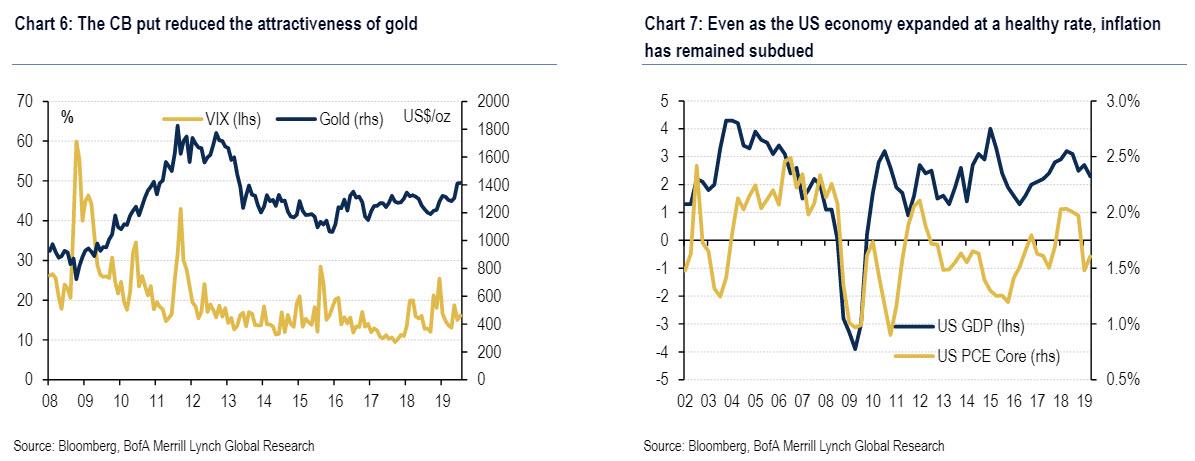

After the gold price rally ended, and fell sharply in the wake of the

taper tantrum, gold prices then remained subdued also because ongoing

monetary policy support kept markets buoyant. This is shown in chart 6, which highlights that falling volatility was ultimately accompanied by lower gold quotations.

Of course, this was also influenced by an acceleration of the US

economy, which picked up post GFC and in 2015 printed some of the

highest growth rates in a decade

Unfortunately, the central banks' fairy tale did not last, and the

"strong economic growth" came with a significant wrinkle: inflation

remained well below the 2% target. The chart shows data for the US, but

the lack of upward pressure on general price levels has been equally

pronounced in other countries/ regions including Japan/ Europe.

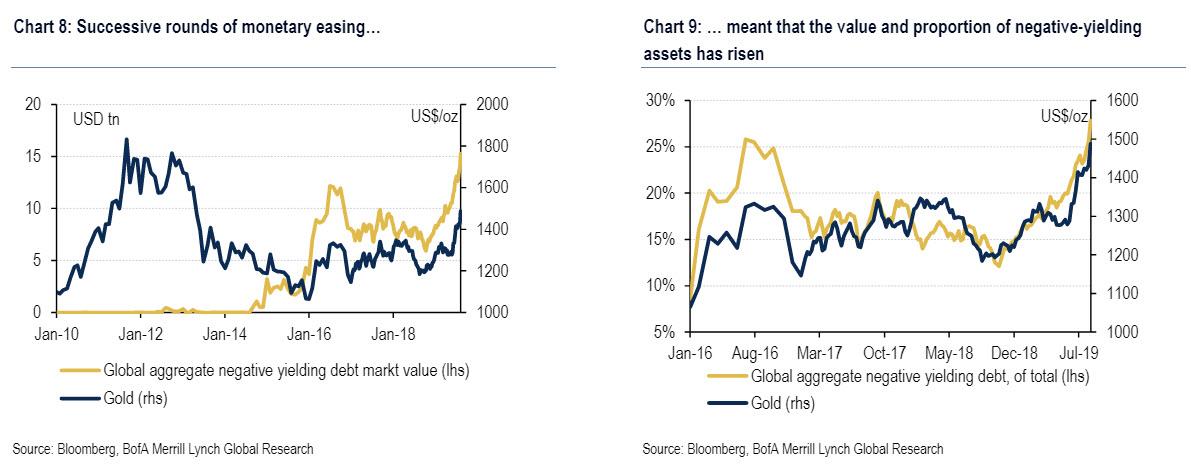

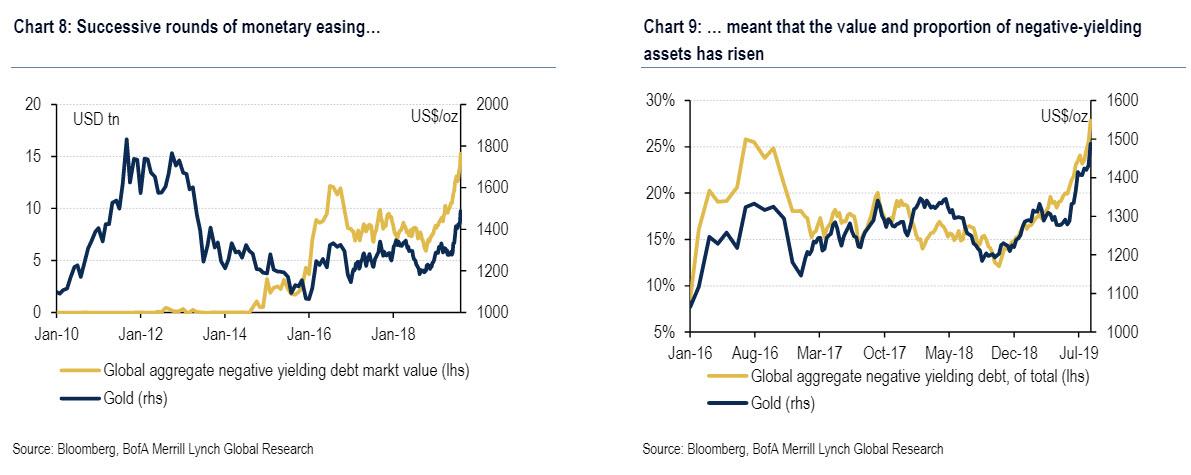

Yet notwithstanding the ongoing lack of reflation, central banks

around the world seem adamant that monetary easing will ultimately do

the job - as in it didn't work last time, but it will work this time, we

promise - and hence expectations are for more stimulus. The

side-effects of that are mirrored by Chart 8 and Chart 9: value

and proportion of debt with negative yields has risen almost

exponentially of late and this has been a powerful driver of the gold.

This, according to BofA commodity strategists, has various

implications. Most notably, "ultra-easy monetary policies have led to

distortions across various asset classes"; worse - and these are not our

words, but of Bank of America - "it also stopped normal economic

adjustment/ renewal mechanisms by for instance sustaining economic

participants that would normally have gone out of business", i.e. a

record number of zombie corporations.

In addition, as everyone knows, debt levels have continued to

increase, making it more difficult for central banks to normalize

monetary policy as 2018 showed so vividly (and for Powell, painfully).

Which brings us to BofA's conclusion: "We fear that this

dynamic could ultimately lead to "quantitative failure", under which

markets refocus on those elevated liabilities and the lack of global

growth, which would in all likelihood lead to a material increase in

volatility." こういう状況でBoAはこう結論づける:「この力学が「量的失策」となることを恐れている、市場は再度債務増加と世界的成長欠如に注目している、これはボラティリティを大きく増やすことだろう。」

How does gold fall into this: "At the same time, and perhaps

perversely, such a sell-off may prompt central banks to ease more

aggressively, making gold an even more attractive asset to hold." この状況でゴールドはどうなるだろう:「それと同時に、たぶん株式下落を見て中央銀行にさらなる緩和を督促するかもしれない、こうなるとゴールドは更に魅力をますことになる。」

In other words, as the world approaches the financial endgame and

central banks are out of ammo beside just doing more of the same - that

led the world to the current catastrophic state - gold will be the

biggest beneficiary of the upcoming financial cataclysm. And, no, this

is not some fringe blog predicting the apocalypse, this is the

prediction of one the 4 largest US banks.

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...

Amazonで買物をしてContrarianJを応援しよう Albert Edwards: This Was The Final Recessionary Shoe, And It Has Now Fallen by Tyler Durden Thu, 06/27/2019 - 12:45 Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007... ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・ ... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions. ・・・市場は準混乱状態になった、というのも歴史的に見てイールドカーブ反転が過去7回の景気後退の前兆となっているからだ。 However, while the inversion was certainly a memorable event, the question on everyone's lips is how do risk assets perform once the curve flattens and/or inverts. According to backtests from Goldman, since the mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. ...

中国が債務増加していることはたしかです。ただ日本の例を日銀資金循環報告でみると家計、320兆円、民間非金融機関1,785兆円、一般政府 1,284兆円となります。合算すると3,300兆円にもなり、GDPの600%を超えています。 https://www.boj.or.jp/statistics/sj/sjexp.pdf この記事の統計と同じ考え方で数値を採用しているのかどうか気になります。 加えて、この資金循環報告に書かれている海外資産というのが内数なのか外数なのか?私にはよくわかりません。当然海外債務も結構な額になります。一度日銀資金循環 図表1を見てください。詳しい方に教えていただければ。 この中国のたどる道は昔のソ連とかMMTと同様で、自国通貨ならいくら発行しても倒産はしない、というか為政者が痛みに耐えることができず緩和を続けるというものです。でも最終的には限界点に達します。ソ連は建国から崩壊まで70年かかりました。 自由主義経済なら立ち行かなくなった企業は退場してもらうというのが減速なのですが、これがうまくゆかないわけです。 でも日本は中国のはるか先を言っているように見えます。ちょっと検索したのですが、日本の債務に関しては政府債務に言及したものばかりで、この記事のように民間、個人まで総合的に記載しているのは日銀の資金循環統計しか見つけることができませんでした。 China Continues To Pile Debt On Top Of More Debt Written by Jesse Colombo | Feb, 27, 2019 Like many countries, China attempted to rein in its debt growth over the past couple years, but ultimately gave up and is now back to piling on even more debt. Bloomberg reports – 多くの国と同様に、中国もここ2年ほど債務増加を抑えようとしてきた、しかし結局の所諦めてしまい、今や更に債務を積み上げている。ブルームバーグ記事ーー For almost two years,...