Baoshang Bank とBank of Jinzhouに続き今度は3度目となる中国の銀行救済だ。

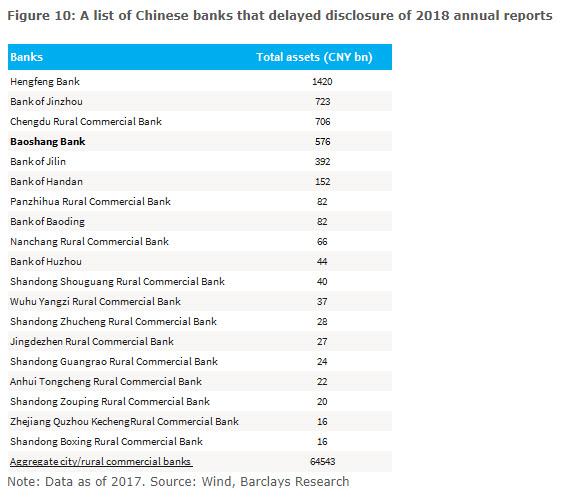

Last month, when reporting on the imminent failure of yet another Chinese bank in

the inglorious aftermath of Baoshang Bank's late May state takeover, we

dusted off a list of deeply troubled Chinese financial institutions

that had delayed their 2018 annual reports...

... and noted that the #2 bank on this list, Bank of Jinzhou recently

met financial institutions in its home Liaoning province to discuss

measures to deal with liquidity problems, and in a parallel bailout to

that of Baoshang, the bank was in talks to "introduce strategic

investors" after a report that China’s financial regulators are seeking

to resolve its liquidity problems sent its dollar-denominated debt

plunging.

・・・そしてこの表の2番めの銀行、Bank of Jinzhouが最近遼寧省の金融機関と流動性問題に関して会合を持った、そしてBaoshangと同様の救済となった、ドル建て債権急落による流動性問題を解決する中国金融監督当局と「戦略的投資家を導入」する議論を行った。

Just a few days later, that's precisely what happened,

when in late July, Industrial and Commercial Bank of China (ICBC), the

country’s largest lender by assets, China Cinda Asset Management and

China Great Wall Asset Management, two of China’s four largest

distressed debt managers, said on Sunday they would take stakes in Bank

of Jinzhou.

その数日後、そのとおりにことは進んだ、7月遅くに、中国工商銀行ICBC、中国最大の貸し手だ、China Cinda Asset ManagementとChina Great Wall Asset Management,この2社は中国4大不良債権処理会社のうちの2つだ、日曜にこれらの会社がBank of Jinzhouを吸収することを開示した。

To be sure, there was some token debate over the semantics: was this bailout a nationalization or a state-bank funded takeover:

“For Baoshang Bank, the government took a state takeover, while for

Bank of Jinzhou, the government introduced some state-owned strategic

investors,” said Dai Zhifeng, analyst with Zhongtai Securities Co; in

reality both were government rescues, only in the latest case Beijing

used state-owned bank intermediaries.

“The latter approach is more market-oriented and showcased the

determination of regulators to resolve problematic banks, while

injecting confidence into the market,” Dai said, although when stripped

of all the pig lipstick, what just happened in China is that another

major bank, one with $100 billion in assets, just collapsed and received

a government-backed rescue.

「Baoshang Bankの場合は政府による接収だった、一方Bank of Jinzhouの場合は、政府が戦略的国有企業投資家を募った、」とDai Zhifengは言う、彼はZhongtai Securities Coのストラテジストだ;現実にはどちらも政府による救済だった、直近ケースに限り、北京政府は国有銀行による仲介を選択した。「後者のほうが市場高感度が高い、そして監督当局が問題銀行救済に関するショーケースとなる、市場の信頼が得やすい、」とDai は言う、しかしながらお化粧を剥がすと、今中国で起きていることは、もう一つの大手銀行、っさんが$100Bを超える大規模銀行、これが倒産し政府の救済を受けた。

The bigger problem, and the reason why Chinese bank stocks have

tumbled ever since the Baoshang Bank bailout, is that investors (and

depositors) were worried that now that Beijing has started down the path

of bank bailouts, it was unclear where it would stop.

より大きな問題、そしてBaoshang Bank 救済以来どうして中国の銀行株が下落しているかというと、投資家(そして預金者)は北京政府が銀行救済から手を引き始めたのではないかと懸念していることだ、どの時点で止めるかは明らかではない。

And so, fast forward to this week when overnight, the SCMP reported that China’s

sovereign wealth fund has taken over Heng Feng Bank - the bank at the

very top of the list shown above, one with roughly $200 billion in

assets - a troubled lender linked to fugitive financier Xiao Jianhua,

in the third case in as many months of the state exerting its grip over

wayward financial institutions. というわけで今週の出来事を巻き戻して見ると、SCMP中国南方新聞がこういう記事を書いた、中国国家資産ファンドがHeng Feng Bankを吸収したーー当行は上に示したリストの最上段にある、資産規模は$200Bにもなるーー逃亡者であるXiao Jianhua関連企業に貸し出しをしていた、予測不能な金融機関を把握しようと何ヶ月も努力してきた結果の3度目の救済だ。

According to the report, Central Huijin Investment, a subsidiary of

the China Investment Corporation that acts as the Chinese government’s

shareholder in the country’s four biggest banks, emerged as a strategic

investor in Heng Feng, according to a brief report overnight by Shanghai

Securities News, published by state news agency Xinhua.

The investment was a breakthrough in Heng Feng’s debt restructuring

led by the Shandong provincial government, the state-owned newspaper

said, without citing a source or providing financial details. Huijin’s

investment would increase Heng Feng’s capital adequacy, improve the

troubled bank’s management and enhance its operational capability, the

paper said.

In short, a 3rd Chinese bank in as many months received an implicit

(or explicit) state bailout, and with the dominoes now falling, it's

just a matter of time before most if not all of the banks shown in the

list above collapse.

Some more details on bailout #3: この3度目の救済の詳細

Heng Feng, based in Yantai city, was founded in 1987. It operated 18

branches and 306 sub-branches across the country. It is among more than a

dozen city-level and rural lenders that had been put on notice by the

authorities for a shake-up, as regulators step up their programme of

cleaning up financial malfeasance and profligate lending.

It’s also the second of several banks in Xiao’s financial empire to

be put under state ward, after the May 24 nationalisation of Baoshang

Bank in Inner Mongolia’s Baotou city. As we reported back in

May, Xiao’s Tomorrow Group, which owned 89% of Baoshang, had

misappropriated large sums from the bank, triggering serious credit

risks that prompted the government to step in, the central bank said.

Xiao himself had not been seen in public since he was persuaded to

return to mainland China from Hong Kong on the eve of the 2017 Lunar New

Year to help with investigations into his financial affairs. Like so

many other former oligarchs, he simply disappeared somewhere deep inside

China's "corrections" apparatus.

As the SCMP notes, at its apex, Tomorrow Group owned stakes via

proxies in hundreds of Chinese listed companies, including at least 10

banks, the China Banking & Insurance Regulatory Commission said on

June 9.

It all ended with a bang, however, with the Baoshang Bank seizure in late May.

Then, as we reported two months later, Baoshan was joined on July 29

by Bank of Jinzhou, which received the backing of three Chinese

financial institutions, including Industrial & Commercial Bank of

China. ICBC put 3 billion yuan (US$436 million) into Bank of Jinzhou,

and assigned at least four senior executives to manage it. Cinda Asset

Management and Great Wall Asset Management would also pour funds into

Bank of Jinzhou.

しかしながら、5月お足のBaoshang Bank差し押さえは大成功で終わった。その後ZeroHedgeは二ヶ月後7月29日にBank of JinzhouがBaoshanの仲間入りしたことを記事にした、この際に中国の3金融機関の保証を受けている、そのうちの一つが中国工商銀行ICBCだ。ICBCはUS$436MをBank of Jinzhouにつぎ込んだ、そして4人の役員も派遣した。Cinda Asset ManagementとGreat Wall Asset ManagementもBank of Jinzhouに資金を注入した。

The change in strategy, where Beijing was now openly seizing or

bailing out insolvent banks - Baoshang was the Chinese government’s

first nationalisation of a private bank since 1998 - led to a collective

collapse in the stock prices of China’s listed banks, driving their

valuations to record lows, amid fears that the shakeout would affect

more lenders, and that the largest and best capitalized institutions

would be called upon to bail them out.

That's precisely what is happening right now, and unfortunately it's

about to get worse for a simple reason that was all the rage back in

2015 - namely the soaring amount of Chinese NPLs, a number which has

been drastically massaged by the banks, regulators and politicians, to

make China's banking system appears safer than it was (see " CLSA Just Stumbled On The Neutron Bomb In China's Banking System"). As the SCMP notes, the level of non-performing loans

among local lenders licensed to operate within city of urban centres

were at 1.9% of their total lending at the end of March, worse than their larger peers, according to CBIRC data. The real number is likely orders of magnitude higher.

これがまさにいま中国で起きていることだ、そして残念なことに状況は悪化している、その理由は単純で2015年の猛威再来ということだーーすなわち中国不良債権洗い出しで、銀行、監督当局、政治屋による厳しい監査で数字が見直され、中国銀行システムは以前よりも安全になった。SCMPによると、5月末時点で地方の認定貸し出し組織の不良債権比率は1.9%だった、この数値は同業大手よりも大きい、とCBIRCデータは示す。実際の数値はたぶんこれよりも一桁大きいと思われる。

These local, city banks were also the least capitalised among all

bank categories, with 12.6% capital adequacy ratio, compared with 18.3%

in foreign banks.

It gets even worse when one looks at China's rural commercial banks,

which are licensed to serve villages and smaller towns, and which had

4.1% of their lending classified as bad loans, CBRC data showed. That

compared with the 1.1 per cent average among larger nationwide

commercial banks, and 0.8 per cent among foreign banks, the data showed.

None of those numbers is remotely close to reality, and with China's

economic growth now sliding, it is just a matter of time before things

get far worse.

Incidentally, just days before the Heng Feng rescue, JPMorgan

correctly downgraded China's banks due to increasing pressure for banks

to support growth agenda as macro risk escalates:

The J.P. Morgan economics team revised down its GDP growth forecast

for 2020 by 0.1ppt due to the recent sharp turn in Sino-U.S. trade

negotiations. But even prior to that, declining PPI and industrial

profits growth, suggesting declining debt-servicing ability and

weakening cash flow for Corporate China, increase the risks that banks will be asked to support macro growth at the potential expense of profitability. Recent official PBOC comments on an accelerating interest rate liberalization process are illustrative of such rising risks.

Additionally, JPM cautioned investors to stay away from Chinese banks

as, "(1) we cut our NIM and earnings estimates to factor in potential

NIM compression due to interest rate liberalization; (2) banks’

re-rating path comes to a halt, at least for now, due to the re-leverage

of Corporate China leading to debt concerns; and (3) rising

concerns of failed small banks contaminating the balance sheets of large

banks may lead to de-rating pressure on large banks."

It now appears that Beijing has indeed picked a model where concern

(3) is especially valid, as large banks will be brought in to bail out

smaller, insolvent ones (think JPMorgan and Bear Stearns), in the

process "contaminating" their balance sheets, as what until now was a

localized financial weakness diffuses across the entire banking sector.

But what may be worst for China, is that it as of this moment its

options to boost the economy are severely limited following the latest

inflation data which was "the worst of both worlds", as PPI prices

posted their first decline in 3 years, while CPI jumped to 16 month

highs as food prices continued to soar.

This, as Bloomberg's Kyoungwha Kim wrote, is "an ominous sign for

equities because it underscores the difficulties the PBOC faces if it

wants to boost policy stimulus", or as we summarized it last night:

The bottom line: Trump now appears to be winning the trade war with

China, whose economic contraction is accelerating and between slowing

trade, sliding corporate profits (PPI), rising inflation (CPI), a

devaluing Yuan, a record debt load, and now a sudden crisis in its

banking sector, Beijing has found itself paralyzed and with zero

credibly options how to kickstart the economy.

The only thing that's left is for China to admit that this is indeed

the case, so sit back, relax and watch as bank after bank on the list

above fails and China's financial cancer spreads across the country with

the $40 trillion in assets (which is certainly not bad news for either

gold or bitcoin).

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...

Amazonで買物をしてContrarianJを応援しよう Albert Edwards: This Was The Final Recessionary Shoe, And It Has Now Fallen by Tyler Durden Thu, 06/27/2019 - 12:45 Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007... ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・ ... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions. ・・・市場は準混乱状態になった、というのも歴史的に見てイールドカーブ反転が過去7回の景気後退の前兆となっているからだ。 However, while the inversion was certainly a memorable event, the question on everyone's lips is how do risk assets perform once the curve flattens and/or inverts. According to backtests from Goldman, since the mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. ...

中国が債務増加していることはたしかです。ただ日本の例を日銀資金循環報告でみると家計、320兆円、民間非金融機関1,785兆円、一般政府 1,284兆円となります。合算すると3,300兆円にもなり、GDPの600%を超えています。 https://www.boj.or.jp/statistics/sj/sjexp.pdf この記事の統計と同じ考え方で数値を採用しているのかどうか気になります。 加えて、この資金循環報告に書かれている海外資産というのが内数なのか外数なのか?私にはよくわかりません。当然海外債務も結構な額になります。一度日銀資金循環 図表1を見てください。詳しい方に教えていただければ。 この中国のたどる道は昔のソ連とかMMTと同様で、自国通貨ならいくら発行しても倒産はしない、というか為政者が痛みに耐えることができず緩和を続けるというものです。でも最終的には限界点に達します。ソ連は建国から崩壊まで70年かかりました。 自由主義経済なら立ち行かなくなった企業は退場してもらうというのが減速なのですが、これがうまくゆかないわけです。 でも日本は中国のはるか先を言っているように見えます。ちょっと検索したのですが、日本の債務に関しては政府債務に言及したものばかりで、この記事のように民間、個人まで総合的に記載しているのは日銀の資金循環統計しか見つけることができませんでした。 China Continues To Pile Debt On Top Of More Debt Written by Jesse Colombo | Feb, 27, 2019 Like many countries, China attempted to rein in its debt growth over the past couple years, but ultimately gave up and is now back to piling on even more debt. Bloomberg reports – 多くの国と同様に、中国もここ2年ほど債務増加を抑えようとしてきた、しかし結局の所諦めてしまい、今や更に債務を積み上げている。ブルームバーグ記事ーー For almost two years,...