Bear markets often overlap with recessions (and typically lead them), but not always.

ベア相場は景気後退と重なることが多い(典型的には先行する)、しかし必ずそうというわけでもない。

It’s important to distinguish between leading and lagging economic indicators and to focus at least as much on trend as level.

大切なことは先行指標と遅行指標を見極めること、そしてすくなくともそのトレンドに注意せよ。

Recession

chatter is abundant lately. It’s increasingly the focus of Q&A

sessions at investor events at which I’ve been speaking. I also received

a series of questions last week about recessions from a Schwab

colleague who has many younger Schwabbies on his team, most of whom have

not lived as working adults through a recession. In putting together

answers to his questions in one of our internal sites, I decided it was a

topic to which I should devote these pages.

Perhaps heightened recession concerns are to be expected given the

duration of the current cycle—which will become the longest post-WWII

expansion if a recession doesn’t begin by July of this year. Or perhaps

it’s because of the recent deterioration in economic data across a

fairly wide spectrum of indicators. I’ve been touching on the topic

quite a bit in my writings as well as on Twitter, but it’s time for a

more evergreen look at recessions.

The bottom line is the U.S. economy will move into a recession at

some point. It’s inevitable. They always occur at the end of a cycle and

set the stage for the subsequent cycle. Recessions haven’t been

outlawed, nor can (or should) they be prevented at all costs by the

Federal Reserve or other policy-makers. What we don’t know is the length

of runway between now and the next recession. I’ve been positing that

at this stage, an earnings recession seems more likely in the near-term

(i.e., starting sometime in this year’s first half) than an economic

recession. But it’s never too early to refresh our memories as to what

to look for to gauge the risk and timing of recessions.

First, let’s get the definition straight. I’m always surprised when I

hear or read the perceived definition of a recession being two

consecutive quarters of negative gross domestic product (GDP). That is not,

nor has ever been, the definition of a recession. The official arbiter

of recessions is the National Bureau of Economic Research (NBER) and

they define a recession as “a significant decline in economic activity

spread across the economy, lasting more than a few months, normally

visible in real GDP, real income, employment, industrial production, and

wholesale-retail sales.” Not coincidentally (pun intended), those

latter four economic readings make up The Conference Board’s Index of

Coincident Indicators, which get released monthly alongside the Leading

Economic Index (LEI), which I’ll get to later in this report.

まずはその定義から始めよう。私はいつも驚くのだが、2四半期連続でGDP成長がマイナスのことだと定義する人がいる。これは決して景気後退の定義ではない。公式に景気後退を判定するのはNBERであり、彼らはこう定義している「経済活動全般に深刻な後退が見られ、これが数ヶ月続くこと、通常はGDP、収入、雇用、工業生産、そして卸売り小売に現れる」。必ずしも同時でなくてよいが、これら4経済指標は The Conference Board's Index of Coincident Indicators と呼ばれる、この値は毎月 Leading Economic Index(LEI)として開示される、この記事の後半でこの議論をしよう。

For “proof” of the difference between the perceived definition and the actual definition, note the following:

世間で言われる定義と実際の定義の違いの「実例」はこういう具合だ:

The 2001 recession did not have back-to-back negative GDP quarters.

2001年の景気後退では連続四半期でのマイナスGDP成長はなかった。

The 1960-1961 recession did not have back-to-back negative GDP quarters.

1960−1961景気後退でも連続四半期でのマイナスGDP成長はなかった。

There were back-to-back negative GDP quarters in 1947, yet there was no recession.

1947年には連続してGDPがマイナス成長だった、しかし景気後退ではなかった。

Below is the full post-Great Depression roster of official recessions.

下に示すのは大恐慌以来のすべての公式景気後退だ。

Source: Charles Schwab, National Bureau of Economic Research (NBER). *Back-to-back “double dip” recessions.

As you can see, the average span of recessions during this time

period was 10.8 months, with a range from six months to 18 months. Keep

in mind, that the NBER is generally late in declaring the start and end

dates of recessions—they do not do any recession forecasting, but

instead wait until the trends are clear with regard to the parameters

they use for declaration and dating purposes.

What should we expect from the stock market during a recession?

Should we assume 20% or more market losses given the tendency for stocks

to enter into a bear market in anticipation of recessions?

The table below shows every S&P 500 bear market (using the

traditional -20% definition) in the post-Great Depression era, but also

what I’ll call “near bear markets” (down at least 19% but less than

20%).

As you can see in the table below, there is typically an overlap

between the two, with bear markets generally starting in advance of

recessions (red entries are bear/near bear markets which overlapped with

recessions). That said, there are bear/near bear markets that have not

accompanied recessions (like 1987); and there are recessions that have

only had near bear markets (like 1991). There are a surprisingly large

number of near bear markets.

Source: Charles Schwab,

Bloomberg, National Bureau of Economic Research.

Bear market defined as

20% or greater drop in S&P 500. Near bear market defined declines

of more than 19% but less than 20%. *3/24/2000–10/9/2002 is generally

considered one long bear market (-49.1%), but there were two 20% rallies

within that span. **10/9/2007 – 3/9/2009 is generally considered one

long bear market (-56.8%), but there was one 20% rally within that span.

Bear markets that overlapped with recessions were generally more

severe than those occurring outside recessions. The average bear/near

bear market without a recession was -24.6%, while the average bear/near

bear market with a recession was -32.2%.

This next section will highlight several popular economic

indicators—and the importance of understanding the difference between

lagging and leading economic indicators. It will also help to illustrate

my well-worn, and oft-cited adage that “when it comes to the

relationship between economic data and the stock market, better or worse

tends to matter more than good or bad.” In other words, we often think

of what’s happening in the economy in “good or bad” or “strong or weak”

terms; when we should be thinking in “better or worse” terms.

Unemployment rate “too low” to suggest increasing recession risk?

失業率が「とても低い」というのは景気後退リスクを示唆しているだろうか?

When discussing recessions with investors, and listening to many

pundits in the media, I often hear today’s low unemployment rate (UR)

cited as a reason not to fret a recession any time in the near future.

But here’s the rub—the unemployment rate is one of the most lagging of

all economic indicators. In fact, as you will see in the chart below,

the unemployment rate has always been low at the outset of recessions.

It’s most significant period of deterioration has historically been

during recessions; not in the lead-up to recessions. Put another way, a

rising unemployment rate doesn’t cause recessions; recessions cause the

unemployment rate to rise.

Source: Charles Schwab,

Department of Labor, FactSet, Ned Davis Research, Inc. (Further

distribution prohibited without prior permission. Copyright 2019(c) Ned

Davis Research, Inc. All rights reserved.), as of January 31, 2019.

In the post-WWII era, the average uptick in the UR from its trough to

the month the recession began has been 0.4%, with a range of 0.0% to

0.7%. In other words, there were times when the UR hadn’t moved up at

all, yet a recession was ultimately declared as having started.

It’s also instructive to see the data in the table above, which

highlights what happens when you compare a highly lagging indicator (the

UR) to a highly leading indicator (the stock market). The worst returns

for the stock market historically came when the UR was in its lowest

zone (think last year); while the best returns have come when the UR was

in its highest zone (think the start of the bull market in March 2009).

This is because the stock market generally anticipates the coming increase in the UR once it’s sniffed out a recession; and also anticipates the coming decrease in the UR once it’s sniffed out a recovery.

Although less “popular” as an indicator, the most leading of the

various employment indicators is initial unemployment claims. In fact,

they’re one of the 10 subcomponents of the LEI, which I’ll get to

shortly. The fact that claims recently broke out to the upside suggests

we need to be on guard for the signal they’re giving about the length of

time between now and the next recession. If they continue to tick

higher, the risk of a recession starting sooner rather than later will

move up.

Unemployment Claims Around Recessions 景気後退前後の失業保険新規受給申請件数

Source: Charles Schwab, Department of Labor, FactSet, as of February 15, 2019.

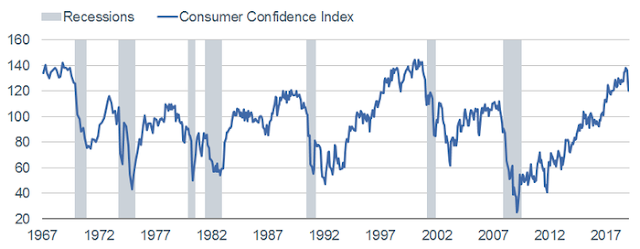

Consumer confidence peaks lead recessions

消費者信頼指数ピークは景気後退につながる

In addition to hearing the unemployment rate cited as a reason not to

fret a recession, I often hear the same about consumer confidence. As

you can see in the chart below of The Conference Board’s measure of

consumer confidence, it remains high in level terms, but is clearly off

the peak. Consumer confidence, as a leading indicator, has typically

peaked out not too far in advance of recessions’ starts.

Consumer Confidence Around Recessions 景気後退前後の消費者信頼指数

Source: Charles Schwab, FactSet, The Conference Board, as of January 31, 2019.

Another consumer confidence-related indicator for recession risk is

the spread between the “present situation” component of the consumer

confidence survey and the “future expectations” component. As you can

see in the chart below, extreme troughs in this spread have been

consistent indicators of coming recessions. (Of course, we don’t yet

know whether we’re at or near the trough for this cycle, but the

currently-extreme spread bears watching.)

Consumer Confidence Spread Around Recessions 景気後退前後の消費者信頼指数スプレッド

Source: Charles Schwab, FactSet, The Conference Board, as of January 31, 2019.

LEI peak? LEIはピーク?

I’ve touched on a couple of the more leading indicators, but let’s

look more broadly at the full set. I focus on the Leading Economic Index

(LEI), put out by The Conference Board. As you can see in the

full-history chart below—in their presently-constituted form (they’ve

been “back-fitted” to account for changes to the indicators that are

most highly-correlated to the business cycle)—the span between LEI peaks

and recession starts has been 13 months, with a range of eight to 21

months. For what it’s worth, the span between LEI troughs and recession

ends has been only two months, with a range of zero-to-five months; so

there is generally more signal lead time heading into recessions than

heading out of them.

Leading Indicators Around Recessions 景気後退前後の Leading Indicators

Source: Charles Schwab, FactSet, The Conference Board, as of January 31, 2019.

In its presently-constituted form, the LEI never failed to give a

heads up that a recession was coming. For what it’s worth, the LEI

peaked last September and declined in two of the subsequent four months.

It’s perhaps too soon to judge whether last September’s peak was the peak for the cycle, especially given the temporary effects of the government shutdown, but we’ll see.

Looking under the LEI’s hood, you can also see where the

deterioration has been concentrated. I also included a Coincident

Economic Index (CEI) section given the aforementioned connection between

those indicators and the NBER definition of recessions. It’s true that

there is not yet any “red” flashing for these indicators in level terms; but there certainly is some flashing occurring if you look at the indicators’ trends.

Source: Charles Schwab, FactSet, The Conference Board, as of January 31, 2019.

Election year 選挙年

One of the aforementioned questions I received from my colleague was

about whether a recession is possible during an election year (yes, I

know the election isn’t until next year). Historically, recessions have

sometimes occurred during election years:

In 1932, we were in the midst of the Great Depression (1929-1933).

In 1948, a recession began in the same exact month as that year’s election.

In 1960, a recession began early that year.

In 1980, we were already in the “double-dip” recession(s) ending in 1982.

In 2008, we were already in the midst of the worst recession since the Great Depression.

Fed models say what?

FEDの景気モデルではどうなっているだろう?

The Federal Reserve has not distinguished itself historically with

forecasting recessions. But that doesn’t mean they haven’t created

forecasting models for both recessions and GDP growth. Among myriad

recession probability models out there, the one from the Federal Reserve

Bank of New York is fairly popular. As you can see in the chart below,

it’s showing a 24% chance of a recession, which doesn’t sound high. But

as shown, with the exception of the late-1960s and mid-1990s, once the

model reached that level it continued to rise and recessions were soon

on the way.

Source: Charles Schwab, Federal

Reserve Bank of New York, as of January 31, 2019. Model uses difference

between 10-year and 3-month Treasury rates to calculate probability of a

recession 12 months ahead.

Both the Atlanta and New York Federal Reserve Banks also publish GDP

forecasting models, which you can see below. Atlanta’s model, called GDPNow,

doesn’t yet have a new forecast for this year’s first quarter, but

their forecast for 2018’s fourth quarter dropped precipitously from 3%

late-last year, but recently rebounding to 1.9% today. The NY Fed’s

model, called Nowcast, does have a forecast for this year’s

first quarter and it’s dropped from 2.6% late-last year to only 1.2%

today (although their fourth quarter 2018 forecast is 2.3%, so higher

than GDPNow’s).

Atlanta FEDとNewYork FEDがともにGDP予想モデルを開示している、下に示すとおりだ。AtlantaモデルはGDPNowと呼ばれる、まだ今年Q1の新規予想を開示していない、しかし彼らの2019Q4予想は昨年遅くの予想3%から急落し、その後持ち直して今日の時点で1.9%だ。NY FedモデルはNowcastと呼ばれ、今年Q1の予想が昨年遅くの2.6%から急落して今や1.2%しかない(ただし2018Q4予想は2.3%でGDPNow

より大きい)。

GDPNow for 4Q2018

Nowcast for 1Q2019

Source: Charles Schwab, Bloomberg, Federal Reserve Bank of New York, as of February 22, 2019.

The mother of all recession indicators

全ての景気後退指標の根拠

We saved the best for last and will conclude with a look at what has

arguably been the best recession forecasting indicator historically—the

yield spread. There are myriad spreads across the Treasury duration

spectrum, but the one historically most useful for forecasting

recessions is the spread between the 10-year and three-month Treasury

yields. As you can see in the chart below, inverted yield curves (when

long-term rates fall below short-term rates) has generally been followed

shortly thereafter by recessions.

Source: Charles Schwab, FactSet, as of February 22, 2019.

More recently, in FEDS Working Paper No. 2018-055, Fed Governor Eric

Engstrom and Fed Research & Statistics Economist Steven A. Sharpe

argued that the spread of short-term Treasury rates—the difference

between the six-quarters-ahead forward rate and the three-month

yield—might be preferable as a predictor because it focuses on

expectations of the near-term path of monetary policy. For what it’s

worth, that spread did invert briefly at the beginning of January this

year.

つい最近、FED論文 No2018-055で、FED総裁 Eric EngstromとFEDエコノミスト Steven A.Sharpeがこう主張した、短期国債金利スプレッドーー6四半期forward rate と3か月もの国債金利差ーーこれが景気後退予想に有用だと、というのもこれらを見ることで短期的な金融政策動向を推測できると。実際これがどれほど有用かと言うと、今年1月初めに短期的にこのスプレッドが反転した。

Concluding with hope 希望を込めた結末

Having little interest in being a Debbie Downer, I’ll conclude with

the reasons why the length of runway between now and the next recession

could remain fairly long. Both household and business balance sheets

remain relatively healthy. The Fed has taken a dovish turn. Some version

of a trade deal may be in the works. And although still up from last

year’s low, unemployment claims have recently ticked lower again. But

it’s never too early to spend time assessing the risks associated with

recessions. Perhaps last year’s near bear market was an indication of a

recession starting as soon as this year, or perhaps it was a head fake. I

believe an earnings recession is a possibility this year, even if we

can avoid an economic recession starting this year. But given myriad

late-cycle conditions, we continue to urge investors to be prepared for

the end of this cycle.

中国が債務増加していることはたしかです。ただ日本の例を日銀資金循環報告でみると家計、320兆円、民間非金融機関1,785兆円、一般政府 1,284兆円となります。合算すると3,300兆円にもなり、GDPの600%を超えています。 https://www.boj.or.jp/statistics/sj/sjexp.pdf この記事の統計と同じ考え方で数値を採用しているのかどうか気になります。 加えて、この資金循環報告に書かれている海外資産というのが内数なのか外数なのか?私にはよくわかりません。当然海外債務も結構な額になります。一度日銀資金循環 図表1を見てください。詳しい方に教えていただければ。 この中国のたどる道は昔のソ連とかMMTと同様で、自国通貨ならいくら発行しても倒産はしない、というか為政者が痛みに耐えることができず緩和を続けるというものです。でも最終的には限界点に達します。ソ連は建国から崩壊まで70年かかりました。 自由主義経済なら立ち行かなくなった企業は退場してもらうというのが減速なのですが、これがうまくゆかないわけです。 でも日本は中国のはるか先を言っているように見えます。ちょっと検索したのですが、日本の債務に関しては政府債務に言及したものばかりで、この記事のように民間、個人まで総合的に記載しているのは日銀の資金循環統計しか見つけることができませんでした。 China Continues To Pile Debt On Top Of More Debt Written by Jesse Colombo | Feb, 27, 2019 Like many countries, China attempted to rein in its debt growth over the past couple years, but ultimately gave up and is now back to piling on even more debt. Bloomberg reports – 多くの国と同様に、中国もここ2年ほど債務増加を抑えようとしてきた、しかし結局の所諦めてしまい、今や更に債務を積み上げている。ブルームバーグ記事ーー For almost two years,...

Class 8 Heavy Truck Orders Crash 68% in January by Tyler Durden Wed, 02/06/2019 - 17:25 Among the latest dismal news about the strength of the US economy, on Tuesday ACT Research released preliminary truck orders for January 2019 which showed that Class 8 truck orders collapsed an astounding 68% for January. The decline is being attributed to a 300,000+ vehicle backlog potentially prompting fleets to halt purchases in the near term. 米国経済に関し最近憂鬱なニュースが多い中で、火曜にACT researchが2019年1月のトラック発注を開示した、1月にClass 8のトラック発注がなんと68%も急落した。この発注減は短期的に300,000台超の潜在在庫を生み出す。 Specifically, in January Class 8 net orders were 15,800 units (14,700 SA; 176,400 SAAR), down 68% YoY and down 26% MoM. Class 5- 7 January net orders were 23,400...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...