ただし債務先進国の日本では、家計300兆円、非金融法人400兆円、政府1300兆円とGDPの400%程度の債務を積み上げてもまだ問題が顕在化しません。今も毎年政府債務は30兆円増え続けており、一方GDPはほとんど増えていません。多分海外の政策立案者はこれを先例 or 目安として見ているような気がします。

When

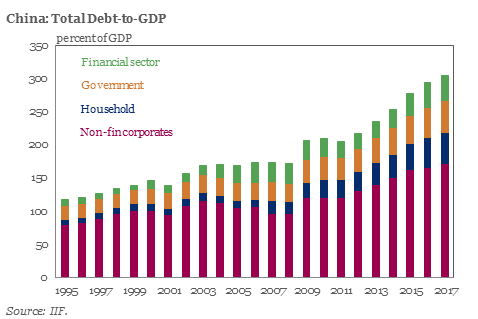

it comes to estimating China's total outstanding debt, there has long

been confusion about the real number with most putting the debt/GDP at

around 250%, while the IIF in 2017 calculated China's debt load as high

as 300% of GDP (which means that by now it is substantially higher).

Then, last year, China watchers added another 40% of debt/GDP to the total when, as S&P calculated,

China’s local governments had accumulated 40 trillion yuan ($6

trillion) - or even more - in off-balance sheet, or Local government

financing vehicles (LGFV) debt, an amount Bloomberg has dubbed China's "hidden debt bomb", suggesting the already record surge in defaults in 2018 is set to accelerate further.

昨年になり、中国ウオッチャーはさらに政務/GDPを40%追加した、S&Pの試算では、中国の地方政府は40T人民元($6T)以上の簿外債務があるとみている、Local government financing vehicles LGFV の形を取ることもある、この債務をブルームバーグは「中国の隠れ債務爆弾」と揶揄する、すでに2018年の倒産は急増しているが、これがさらに加速することを示唆している。

"The potential amount of debt is an iceberg with titanic credit risks," S&P credit analysts wrote in October 2018,

with much of the build-up related to local government financing

vehicles, which don’t necessarily have the full financial backing of

local governments themselves.

Local government debt has quickly emerged, together with "shadow

banking" debt, as one of the main risks for China's economy, because

with the national economy slowing, and as a result of a crackdown on

shadow lending and a Beijing quota for issuance of local-government

bonds not enough to fund infrastructure projects to support regional

growth, authorities across the country have resorted to LGFVs to raise

financing, according to S&P. That’s left LGFVs “walking a tightrope”

between deleveraging and transforming their businesses into more

typical state-owned enterprises, S&P warned.

So fast forward 6 months, when in China's ongoing attempt to contain

the soaring financial risks from its debt bubble, Beijing - seemingly

content with the progress it has made on containing shadow debt - is

re-focusing on the "hidden debt" owed by local governments, as officials

seek to reduce repayment pressures amid falling tax revenues.

And with Beijing adding pressure on local authorities to become more transparent with their liabilities, Bloomberg reports that provinces

and cities from Jiangsu in the east to Qinghai in the west are looking

for means to pay-off or restructure their implicit borrowings, which

include trillions in "off the books" funding via financing vehicles.

Some authorities are seeking cheap refinancing from the nation’s largest

policy lender, the China Development Bank, and others are selling off

state-owned assets such as office buildings and housing.

Efforts to deleverage the "hidden time bomb" of 40 trillion in local

government debt have gained urgency after the government recently

pledged to cut taxes by two trillion yuan ($300 billion), further

draining local coffers and adding to the possibility of missed

repayments. Meanwhile, the lack of official estimates of the total local

government debt load - S&P's CNY40 trillion estimate is just that -

which usually carries higher rates than on-book ones, makes the issue

even trickier.

There is a more pressing reason behind the rush to deleverage: as

Nomura's China economist Lu Ting said, the motive is “just that the

problem can’t be delayed anymore,” as in many places fiscal revenues and gross domestic product aren’t enough to cover the interest and principals.

In other words, China may be just months ahead of its own Minsky Moment.

言い換えると、中国はあと数ヶ月で自らのミンスキーモーメントに達するかもしれない。

With official probes now taking place to quantify the local debt, so

far they’ve shown that hidden debt in some places exceeds the on-book

borrowing, a lawmaker of the National People’s Congress Zhu Mingchun

said over the weekend, according to Bloomberg.

Meanwhile, payments due for local-government financing vehicle debt are soaring and could reach 2.3 trillion yuan this year,

according to estimates by Industrial Securities Co, which notes that

local authorities will have to carry that burden at a time of slowing

revenue growth due to tax cuts and shrinking receipts from land sales.

One possible solution is massive restructuring of the debt: in one

case in December, the CDB led a group of commercial lenders in a swap of

260.7 billion yuan of implicit debt borrowed by Shanxi province to

build highways. The debt was restructured with a tenor of up to 25

years, allowing the local authorities to save 3 billion yuan in interest

payments every year, according to Shanxi Transportation Holdings Group.

As Bloomberg notes, asset sales are also being used. For example, a

district in the northeastern city of Shenyang is planning to sell more

than 38,000 square meters of offices and government-built housing to

repay maturing debt.

Of course, since in China everything is in

some state of being a bubble, officials are simply using “the healthier

part of the balance sheet of the public sector to address some of the

hidden issues,” but they have to make sure the risky loans won’t get out

of control again in the future, because by that time the balance sheet

would be less capable of absorbing them, according to Grace Ng, a China

JPMorgan economist.

China is also taking advantage of the current euphoria involving

local capital markets: a financing platform in the eastern province of

Jiangsu, where the CDB is involved in some cases of debt restructuring,

sold a 270-day bond last week with a coupon of 4.8 percent, 150 basis points lower than a similar note the company issued in January. On

Monday, a financing and investment company owned by a city in Shanxi

province was upgraded to AA+ from AA by China Chengxin International

Credit Rating Co., which cited the better outlook for capital quality.

地方金融市場の現在のeuphoria を中国政府は有利に利用している:江蘇省西部地域での金融機関、当地ではCDBが債務再編を行っている、ここで先週270日債権を4.8パーセントクーポンで売却した、1月に発行された同様の債権よりも150BPも低い。山西省のある市が持つ金融投資会社は月曜にAAからAA+に格上げとなった、China Chengxin International Credit Rationg Coによるものだ、今後の見立ても良好と格付けしている。

"The bigger worry is the moral hazard issue,” said Zhu Ning, a

professor of finance at Tsinghua University and the author of “China’s

Guaranteed Bubble.” “Implicit government guarantees still lie at the

core of so many problems."

And nowhere is the problem of moral hazard greater than in China,

whose financial sector is approaching double the size of its US peer

even as China's GDP is years behind catching up with America's. Which

makes Beijing's choice relatively easy: keep kicking the can, or watch

as the long-overdue Minsky Moment finally arrives and topples the

biggest house of financial cards ever constructed.

Amazonで買物をしてContrarianJを応援しよう Silver Outperforming Gold 2 Adam Hamilton July 26, 2019 3232 Words Silver has blasted higher in the last couple weeks, far outperforming gold. This is certainly noteworthy, as silver has stunk up the precious-metals joint for years. This deeply-out-of-favor metal may be embarking on a sea-change sentiment shift, finally returning to amplifying gold’s upside. Silver is not only radically undervalued relative to gold, but investors are aggressively buying. Silver’s upside potential is massive. ここ2週シルバーは急騰した、ゴールドを遥かに凌ぐものだ。これは注目すべきことだ、もう何年もシルバーはひどいものだった。この極端に嫌われた金属が大きく心理を買えている、とうとうゴールド上昇を増幅するに至った。シルバーは対ゴールドで極端に過小評価されているだけでなく、投資家は積極的に買い進んでいる。シルバーの潜在上昇力は巨大なものだ。 Silver’s performance in recent years has been brutally bad, repelling all but the most fanatical contrarians. Historically silver prices have been mostly ...

結局、中国は隣国日本で20年前に起きたことを学んでいなかったということでしょう、というかどの国もどの政府も十分成熟するまでは「わかっちゃいるけどやめられない」ということでしょうね、きっと。 Spooked By Apple? Wait ‘Til China’s Bubble Bursts Written by Jesse Colombo | Jan, 3, 2019 Apple stock plunged nearly 10% on Thursday after the company cut its revenue forecast due to slowing iPhone sales in China. Apple’s woes dragged U.S. stock indices lower by more than 2% as fears of a more extensive China-driven slowdown spread. アップルの株価は火曜に約10%下落した、同社が中国でのiPhone売上原則を予想したためだ。アップルの弱さが米国株式指数を2%以上押し下げた、中国主導でさらなる原則が広がるのではという懸念からだ。 From the New York Times : ニューヨークタイムスによると: For years, no matter what was happening elsewhere, global companies bet billions upon billions of dollars that China’s consumers would keep spending money. 長年、他国で何が起きようとも多国籍企業は中国消費は巨額を維持することに賭けてきた。 Now, just when the world economy could use their financial firepower, they are no longer so quick to open their wallets. 今や、世界経済が金融弾薬を用いてももはや彼らの財布を緩めることはできない。 The latest sign of a slowdown in...

多量のオピオイドを米国に送り込み、米国で深刻な麻薬中毒問題を引き起こしています。現代版「阿片戦争」です。あのトヨタ初の女性取締役もオピオイド中毒で逮捕解任されましたよね。 US Is Dependent On China For Almost 80% Of Its Medicine by Tyler Durden Fri, 05/31/2019 - 12:55 Experts are warning that the U.S. has become way too reliant on China for all our medicine , our pain killers, antibiotics, vitamins, aspirin and many cancer treatment medicine. 専門家はこう警告する、米国はすべての医薬品、痛み止め、抗生物質、ビタミン、アスピリン、各種抗がん剤で、中国依存度が高すぎる。 Fox Business reports that according to FDA estimates at least 80 percent of active ingredients found in all of America’s medicine come from abroad, primarily from China . And it’s not just the ingredients, China wants to become the world’s dominant generic drug maker. So far Chinese companies are making generic for everything from high blood pressure to chemotherapy drugs. 90 percent of America’s prescriptions a...

Barrick’s average quarterly production since Q4’16 plunged an astounding 8.6% YoY. The reason Barrick’s management blew $6.5b in stock buying Randgold is they desperately needed more production to mask the precipitous drop in their own. Barrick’s total 2018 production of 4525k ounces was 18.0% below the 5516k it mined only a couple years earlier in 2016. At best adding Randgold just regains those losses. Barrickの平均四半期生産は2016Q4以来なんとYoYで8.6%下落している。Barrickの取締役が$6.5Bも投じてRandgoldの株式を購入した理由は、彼らはなんとしても急落する自らの生産量を隠すために生産量増加としたかったからだ。Barrickの2018全生産量は4525Kオンスで、わずか2年前の5516kオンスから18.0%も少ない。Randgoldを買収したところでこの下落を補うに過ぎない。 And GOLD has been suffering the same production struggles as ABX. Over its past 4 reported quarters, Randgold’s gold mined has fallen an average of 7.4% YoY. Can bringing two rapidly-depleting major gold miners together magically make a stronger one? I doubt it. Barrick’s reported production will enjoy a big temporary boost...

S&P Surges To Key Technical Level - Now What? by Tyler Durden Tue, 02/12/2019 - 12:03 Having failed twice last week, the S&P 500 is once again testing its 200DMA as hopes of a border/shutdown deal, a lack of collusion, China trade dreams, and an easy Fed are prompting stocks to new post-Xmas dip highs... 先週二回失敗し、S&P500がまたもや200日移動平均に挑戦している、国境の壁/政府閉鎖問題解決、ロシア疑惑解消、中国貿易改善そしてFEDのハト派姿勢、これらがクリスマス下落後の高値を推進している・・・ The S&P 500 is at its highest since Dec 4th... S&P500は12月4日以来の高値だ・・・ What happens next? では次はどうなる? Earnings recession? Meh, don't worry about it... 収益による景気後退? 別に心配することではない・・・・ Oh and don't worry - Fed Chair Powell just told everyone that he "doe...