FEDは株式市場を目標にしていないって?

日本のバブル以降の状況を見た識者には、中国や米国は同じ轍を踏まないだろう、といっている人もいました。でも皆結局同じなんですね、結局金融政策は政治家から離れることができないし、たとえ選挙のない国でも政治家は国民の人気を失うことはできないというわけです。今や日本がMMT先進国であり、30年つづけてもまだいまのところ特異点には達していません。永遠に持続可能でないことはわかりますが、いつ特異点に達するか?それはわかりません。

日本ではGDPが500兆円程度なので2%の成長なら、GDPが10兆円増加する。ただし

GDP=財政支出+消費+投資+経常収支 なので、毎年財政出が30兆円赤字水増しで未来を先取りしているなら、他の要因がマイナスになっているはず。史上最長の景気拡大を多くの人が実感できないのももっとも。

The Fed Doesn’t Target The Market?

Written by Lance Roberts | Mar, 4, 2019

Earlier this month, I penned an article asking if we “really shouldn’t worry about the Fed’s balance sheet?” The question arose from a specific statement made by previous New York Federal Reserve President Bill Dudley:

今月始めに、私はこういう疑問を投げかけた「FEDバランスシートは本当に問題ないのだろうか?」。この疑念が湧いたのはNew York FED前議長のBill Dudleyのある発言からだ:

私はこの状況に驚き戸惑っている。本来の機能以上に注目を浴びている。」

As I noted, there is a specific reason why “financial types” have a preoccupation with the balance sheet.

私が示したように、「金融姿勢」に関して特にバランシートが注目されているのは特別な理由がある。

The preoccupation came to light in 2010 when Ben Bernanke added the “third mandate” to the Fed – the creation of the “wealth effect.”

皆が注目するようになったのは2010年のことだ、このときBen BernankeがFEDの「第三の任務」を付け加えたーー「資産効果」の生成だ。

「これまでの金融緩和手法がまたもや有効に見える。投資家がこの追加任務を懸念し、株価が上がり長期金利は下がった。金融環境緩和は経済成長を引き起こすだろう。たとえば、住宅ローン金利が下がると住宅が買われやすくなり、すでに住宅を持っている人はローン借り換えで現金を手にする。企業債権金利が下がると投資がしやすくなるだろう。そして株価上昇で消費者の資産が増え信頼感を増す、これが消費を促進する。消費が増えると収入が増え企業収益が増える、これが正帰還をおこし、さらなる経済拡大を推進する。」

ーーBen Bernanke , Washington Post Op-Ed, November, 2010。

As he noted, the Fed specifically targeted asset prices to boost consumer confidence. Given that consumption makes up roughly 70% of economic growth in the U.S., it makes sense. So, not surprisingly, when the economy begins to show signs of deterioration, the Fed acts to offset that weakness.

彼が書いたとおり、FEDは消費者信頼を増すために株価を特に目標とした。米国では個人消費が経済成長の70%をしめるわけで、意味のあることだ。そのため、驚くことではないが、経済が悪化の兆候を示すと、FEDはこの弱さを相殺する行動を取る。

This is why the slowdown in global growth became an important factor behind the central bank’s decision to put plans for interest rate increases on hold. That comment was made by Federal Reserve Vice Chairman Richard Clarida during a question-and-answer session last week.

だからこそ、世界の中央銀行が金利上昇の決断をすると、世界経済成長減速の深刻な要因となる。このコメントがFED副議長Richard Claridaから発せられた、先週のQ&Aでのことだ。

「実際、世界経済は減速している。すでにイタリアではマイナス成長だ、ドイツの成長率はわずか1%、そして中国も減速している。これら全てを政策に織り込まねばならない。世界経済成長原則は米国輸出に悪影響を及ぼすだろう、そしてそれが金融株式市場にマイナス効果を引き起こすだろう、金融政策としてはまず考慮せねばならない。」

As we noted previously in “Data or Markets,” the Fed is not truly just “data dependent.” They are, in many ways, co-dependent on each other. A strongly rising market allows the Fed to raise rates and reduce accommodative as higher asset prices support confidence. However, that “leeway” is quickly reduced when asset prices reverse. This has been the Fed cycle for the last 40-years.

The problem for the Fed is they have now become “liquidity trapped.”

What is that? Here is the definition:

私どもは以前の「Data or Markets」という記事の中でこう書いた、本当はFEDは「データ依存」ではない。それらは複雑に相互依存している。市場が力強く上昇しているときにはFEDは金利を引き上げ、株価推進政策を弱めることができる。しかしながら、株価が反落するとその「裁量範囲」も急速に縮まる。こうして過去40年FEDがサイクルを生み出してきた。FEDが直面する問題は、今や「流動性のわな」にとらわれているということだ。

いったい「流動性のわな」とはどういうことだ?その定義はこういうものだ:

「流動性のわなとはケインズ経済学で説明される状況であり、中央銀行が市中銀行にマネーを注入しても金利を下げることができずかつ経済成長促進をできない状況だ。流動性の罠が起きるのは人々が現金を貯め込むことにより引き起こされる、というのも彼らがデフレや不十分な需要もしくは戦争のようなことを予感するためだ。流動性のわなの特徴とは短期金利がゼロ近くになり、マネタリーベースを変えても一般物価レベルに反映されなくなる。」

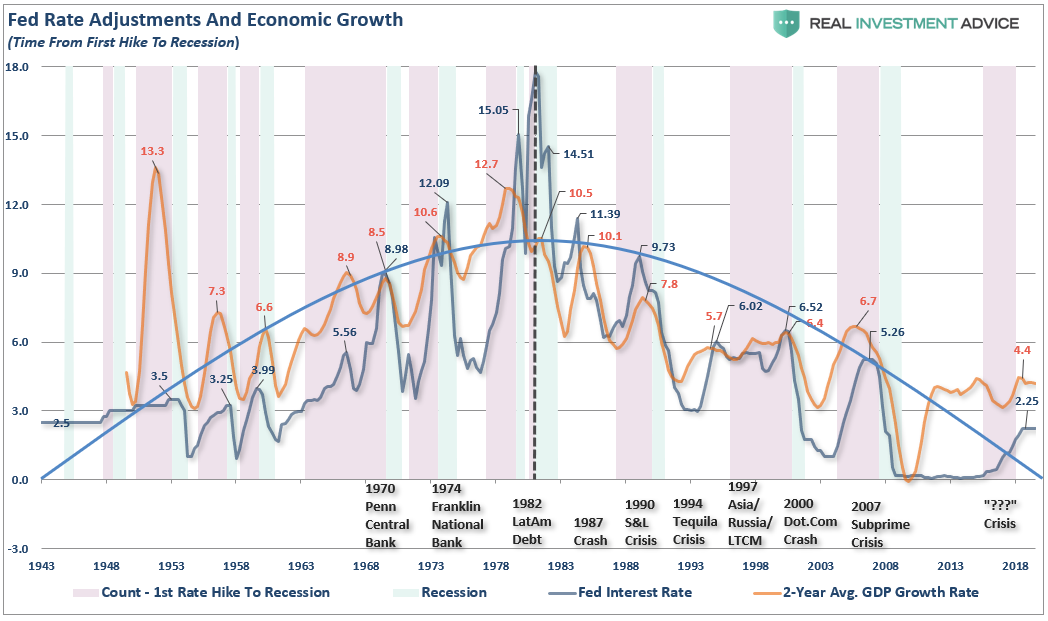

The chart below shows the correlation between the decline of GDP and the Fed Funds rate.

下のチャートが示すのはGDP成長率の低下とFFRの相関を示している。

There are two important things to notice from the chart above. The first is that prior to 1980, the trend of both economic growth and the Fed Funds rate were rising. Then, post-1980, as then Fed Chairman Paul Volker and President Ronald Reagan set out to break the back of inflation, each successive cycle of rate increases were started from a level lower than the previous cycle.

このチャートで大切なことが2つある。まず第一に1980年以前の出来事だ、経済成長率とFFRはともに上昇していた。その後1980以降になると、FED議長 Paul Volkerとレーガン大統領が経済基盤を壊してしまうインフレ政策を取った、その後の金利引き上げサイクルはその開始時の金利が以前のものを下回った。

The difference between the two periods was the amount of debt in the system and the shift from an expansive production and manufacturing based economy to one driven primarily by services which have a substantially lower multiplier effect. Since 1980, it has required increasing levels of debt to manufacture $1 of GDP growth.

この1980年前後の違いは金融システム全体の債務量であることと、もう一つは製造業拡大からサービス業主体の経済にシフトしたことだ、サービス業は基本的に乗数効果が低い。1980年以来、GDPを$1増やすのに必要な債務が増え続けている。

In every case, the rate cycle increase ALWAYS led to either a recession, bear market, crisis, or all three. Importantly, those events occurred not when the Fed STARTED hiking rates, but when they recognized that their tightening process was confronted by weakening economic growth.

どの場合も、金利を引き上げると必ず景気後退、ベア相場、経済危機、のどれかを引き起こすものだ、3つ同時ということもある。大切なことは、これらの出来事が起きるのはFEDが金利引き上げを開始したときではない、そうではなく彼らが引き締め政策が経済成長鈍化に直面したときだ。

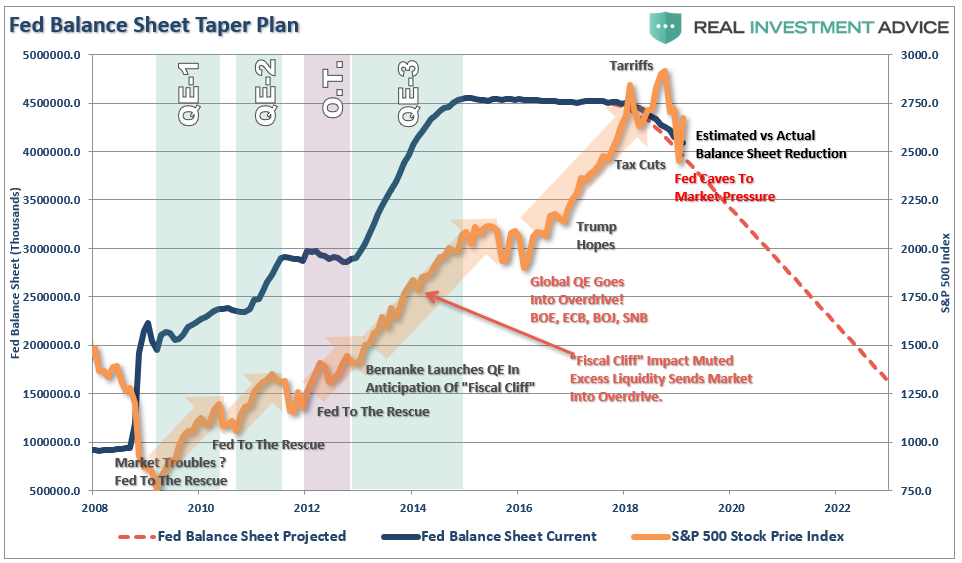

As Richard Clarida noted in his speech, one of the potential risks to Central Banks globally is the lack of monetary policy firepower available. We previously pointed out that in 2009, the Fed went to work to rescue the economy with a $915 billion balance sheet and Fed Funds at 4.2%. Today, that balance sheet remains above $4 trillion and rates are at 2.5%.

FEDのか帰る問題とはこういうことだ、低金利が短期的には経済成長を促進するが、その成長は積み上げられた債務レベル増加によるものだということだ。しかるに、経済は金利政策変更に耐えることができない。上のチャートを見ても解ることだが、一連の金利引き上げは決して前回のピークに達していない。たとえば、2007年には、FFRは5%程度あった、このときFEDは金利を引き下げ始めて金融危機に対処した。現在では、経済の弱さに対処しようとFEDが金利引き下げを始めても、前回の半分の金利からの引き下げとなる。Richard Claridaが彼のスピーチで述べたことだが、世界の中央銀行が抱えるリスクはどこも金融政策の弾が欠けているということだ。私どもが2009年に指摘したことだが、FEDが経済救済を開始したとき、バランスシートは$915Bで金利は4.2%だった。現在、このバランスシートは$4Tを超えており、金利は2.5%に過ぎない。

It isn’t lost on the Fed that if a recession were to occur, their main lever for stimulating economic activity, interest rate reductions, will have little value. Given the amount of debt outstanding and the onerous burden of servicing it, the marginal benefit of lower rates will likely not be enough to lift the country out of a recession. In such a tough situation the next lever at their disposal is increasing their balance sheet and flooding the markets with liquidity via QE.

もし景気後退が起こったとしても、FEDは負けてしまったわけではないが、主要政策である金利引き下げの余地はほとんど効果が無いだろう。すでに多額の債務が積み上がりその債務負荷があるなかで、多少の金利引き下げは経済を景気後退から救済するには不十分だろう。このような困難な状況で次の政策としてはバランスシートを増やし市場にQEで流動性を洪水のように注入することだ。

However, even that may not be enough as both Ben Bernanke and Janet Yellen have acknowledged that they were aware that each successive round of QE was somewhat less effective than the last. That certainly must be a concern for Powell if he is called upon to re-engage QE in a recession or another economic crisis.

しかしながらこういうことをしても充分でないことをBen BernankeとJanet Yellenが言っている、彼らも気づいているが一連のQEを見ても繰り返すほどに効果は薄くなっている。Powellにとっても懸念されることに違いない、次の景気後退や経済危機に直面して再びQEを実行するにしてもだ。

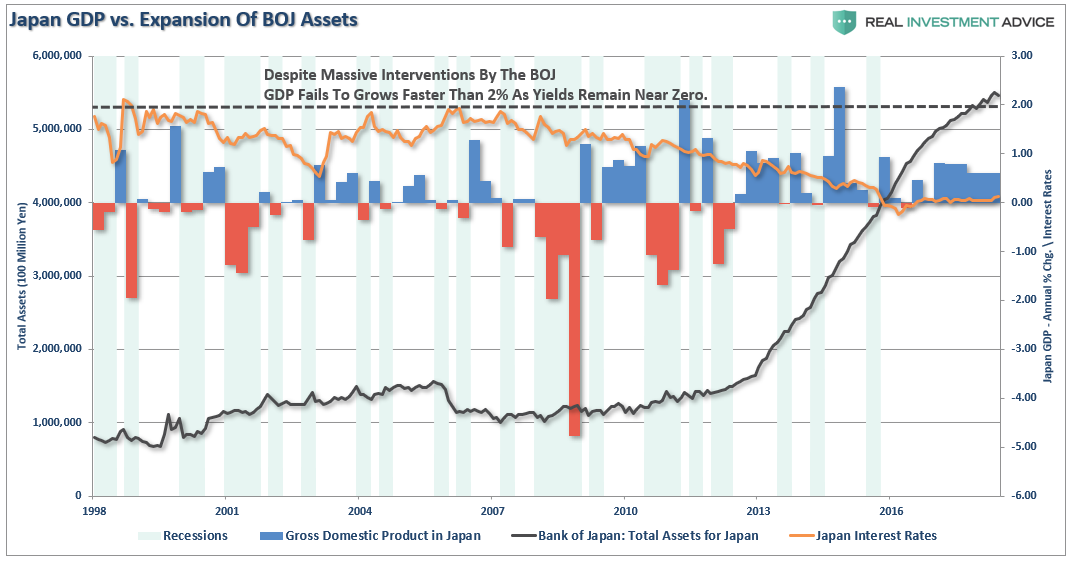

For the Federal Reserve, they are now caught in the same “liquidity trap” that has been the history of Japan for the last three decades. One only needs to look at Japan for an understanding that QE, low-interest rate policies, and expansion of debt have done little economically. Take a look at the chart below which shows the expansion of the BOJ assets versus the growth of GDP and levels of interest rates.

FEDにとって、彼らは今や同じ「流動性のわな」に捕まっている、それは日本が過去30年経験したことだ。誰もが振り返る必要があるのは日本だ、QE,低金利政策、そして債務拡大をしても経済にはほとんど効果がなかった、この国の実例を見るだけで十分だ。下のチャートを見てほしい、ここには日銀資産とGDP成長率そして金利を示している。

Notice that since 1998, Japan has not achieved a 2% rate of economic growth. Even with interest rates still near zero, economic growth remains mired below one-percent, providing little evidence to support the idea that inflating asset prices by buying assets leads to stronger economic outcomes.

注目すべきは、1998年以来日本は経済成長が2%を超えたことがない。金利がほとんどゼロにもかかわらず、経済成長は1%以下を漂っている、これを見れば資産買取により資産価格を膨らまえせても強い経済を生み出さないということを証明している。

But yet, the current Administration believes our outcome will be different.

しかしながら、現在の連邦政府はその結果が違うと信じている。

With the current economic recovery already pushing the long end of the economic cycle, the risk is rising that the next economic downturn is closer than not. The danger is that the Federal Reserve is now potentially trapped with an inability to use monetary policy tools to offset the next economic decline when it occurs.

現在の景気回復期間は十分に長く、次の景気後退が来る可能性が増している。危険なことに、次の景気後退が来てもFEDはそれに対処する弾を殆ど持っていない。

This is the same problem that Japan has wrestled with for the last 30-years. While Japan has entered into an unprecedented stimulus program (on a relative basis twice as large as the U.S. on an economy 1/3 the size) there is no guarantee that such a program will result in the desired effect of pulling the Japanese economy out of its 30-year deflationary cycle. The problems that face Japan are similar to what we are currently witnessing in the U.S.:

この状況は日本がこの30年格闘してきた状況とそっくりだ。日本は巨額の前代未聞の刺激策を取ってきた(経済規模が1/3ということを考えると相対的に米国の倍の規模の刺激を行った)しかしながら、この30年日本経済を見ての通り、そのような政策は期待した効果を引き起こさないだろう。日本が直面する問題は現在米国で見られるものとよく似ている:

投資家、個人にとっての本当の懸念は実経済だ。我々はいま「踊り場」にいるに過ぎない、一方で主要メディアは囃し立てるのとは異なる。経済的風景を見ると明らかになにか欠陥がある、そして現在の長期的なインフレ圧力低下がそれを教えてくれる。FEDにとっての大きな問題は如何にして「流動性のわな」から抜け出すかということだ、経済や金融市場に凹みを生じずに抜け出すかということだ。

しかしながら、一つの主張がある、投資家にとって最も大切なことだ、バランスシート規模と次の景気後退時にそれを使うことに関して Bill Ducleyがこう述べた。

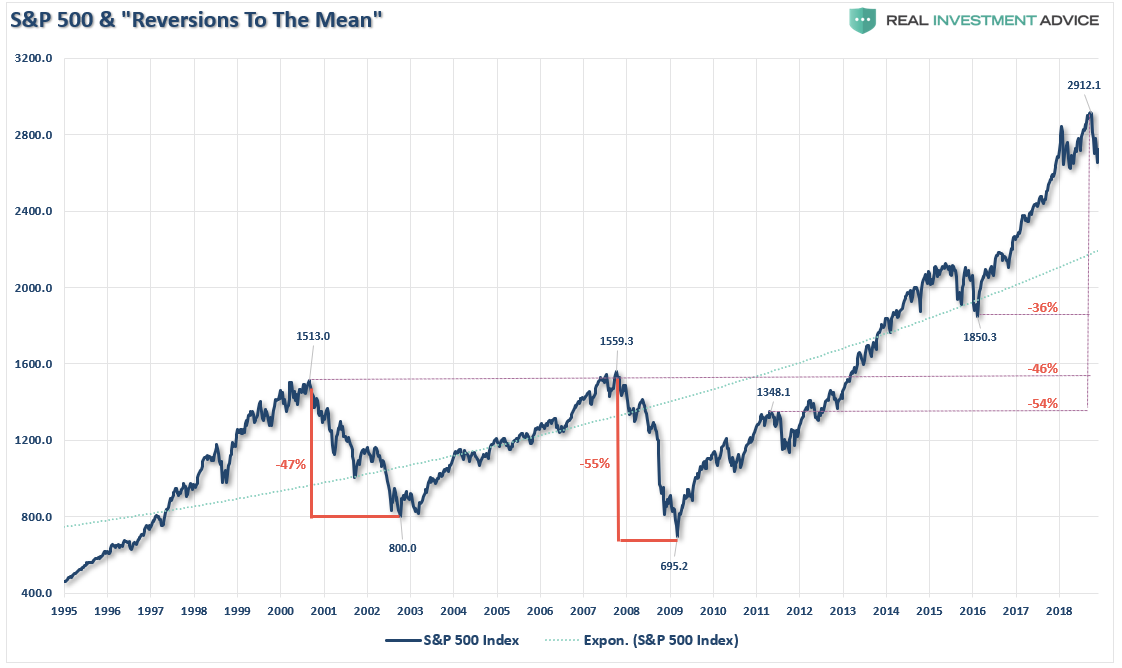

In other words, it will likely require a substantially larger correction than what we have just seen to bring “QE” back into the game. Unfortunately, as I laid out in “Why Another 50% Correction Is Possible,” the ingredients for a “mean-reverting” event are all in place.

言い換えるならば、我々が今目の当たりにしているよりももっと大きな調整があっと時のみに「QE」を復活するだろう。残念なことに、私はこういう記事を書いた「どうして今のレベルから50%の調整が起こりうるか」、「平均回帰」がその背景にある。

今の所投資家にとっての最大のリスクは次の後退の規模だ。下のチャートに示すが潜在的な反落範囲は36%から54%を超える。」

もっと大切なことは、中央銀行が短期で止めた2015−2016の調整を含む過去三度の調整においては、長期的な上昇トレンドから大きく乖離した状態から始まった。長期トレンドからの現在の乖離は史上最大のものであり、平均回帰はそれに比例して大きいだろう。

While Bill makes the point that “QE” is available as a tool,

it won’t likely be used until AFTER the Fed lowers interest rates back

to the zero-bound. Which means that by the time “QE” comes to the fore, the damage to investors will likely be much more severe than currently contemplated.

Billは「QE」をツールとして利用できると言うが、FEDが金利をゼロにしてからでないと使われないだろう。ということは「QE」が全面に出てくるときには、投資家のだめっじは現在想定されるものよりももっと大きいだろう。

Yes, the Fed absolutely targets the financial markets with their policies. The only question will be what “rabbit” they pull out of their hat if it doesn’t work next time?

そう、FEDは絶対に金融市場を目標に政策を決めている。唯一の問題は、それが有効でないときに、彼らは手品の帽子のなかからどんな「うさぎ」を取り出すのだろう?

I am not sure even they know.

彼らは知っているかもしれないが、私にはわからない。

今月始めに、私はこういう疑問を投げかけた「FEDバランスシートは本当に問題ないのだろうか?」。この疑念が湧いたのはNew York FED前議長のBill Dudleyのある発言からだ:

“Financial types have long had a preoccupation: What will the Federal Reserve do with all the fixed income securities it purchased to help the U.S. economy recover from the last recession? The Fed’s efforts to shrink its holdings have been blamed for various ills, including December’s stock-market swoon. And any new nuance of policy — such as last week’s statement on “balance sheet normalization” — is seen as a really big deal.「金融姿勢が長らく注目されてきた:前回の景気後退以来の米国景気回復を手助けするためにFEDは債権買取をしていたがFEDはこれからどうするのだろう?FEDはバランスシート縮小をしてきたがこれが各方面から責められてきた、12月の株式急落もその一つだ。そして今後どういう政策をとるにしろーー例えば先週は「バランスシート正常化」に関しての言及があったがーーこれが本当に大きな影響を果たすと見られている。

I’m amazed and baffled by this. It gets much more attention than it deserves.”

私はこの状況に驚き戸惑っている。本来の機能以上に注目を浴びている。」

As I noted, there is a specific reason why “financial types” have a preoccupation with the balance sheet.

私が示したように、「金融姿勢」に関して特にバランシートが注目されているのは特別な理由がある。

The preoccupation came to light in 2010 when Ben Bernanke added the “third mandate” to the Fed – the creation of the “wealth effect.”

皆が注目するようになったのは2010年のことだ、このときBen BernankeがFEDの「第三の任務」を付け加えたーー「資産効果」の生成だ。

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate this additional action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”

– Ben Bernanke, Washington Post Op-Ed, November, 2010.

「これまでの金融緩和手法がまたもや有効に見える。投資家がこの追加任務を懸念し、株価が上がり長期金利は下がった。金融環境緩和は経済成長を引き起こすだろう。たとえば、住宅ローン金利が下がると住宅が買われやすくなり、すでに住宅を持っている人はローン借り換えで現金を手にする。企業債権金利が下がると投資がしやすくなるだろう。そして株価上昇で消費者の資産が増え信頼感を増す、これが消費を促進する。消費が増えると収入が増え企業収益が増える、これが正帰還をおこし、さらなる経済拡大を推進する。」

ーーBen Bernanke , Washington Post Op-Ed, November, 2010。

As he noted, the Fed specifically targeted asset prices to boost consumer confidence. Given that consumption makes up roughly 70% of economic growth in the U.S., it makes sense. So, not surprisingly, when the economy begins to show signs of deterioration, the Fed acts to offset that weakness.

彼が書いたとおり、FEDは消費者信頼を増すために株価を特に目標とした。米国では個人消費が経済成長の70%をしめるわけで、意味のあることだ。そのため、驚くことではないが、経済が悪化の兆候を示すと、FEDはこの弱さを相殺する行動を取る。

This is why the slowdown in global growth became an important factor behind the central bank’s decision to put plans for interest rate increases on hold. That comment was made by Federal Reserve Vice Chairman Richard Clarida during a question-and-answer session last week.

だからこそ、世界の中央銀行が金利上昇の決断をすると、世界経済成長減速の深刻な要因となる。このコメントがFED副議長Richard Claridaから発せられた、先週のQ&Aでのことだ。

“The reality is that the global economy is slowing. You’ve got negative growth in Italy, Germany may just grow…1% this year, [and] a slowdown in China. These are all things that we need to factor in.

Slower global growth would crimp U.S. exports and could also negatively influence financial and asset markets, a primary transmission mechanism for monetary policy.”

「実際、世界経済は減速している。すでにイタリアではマイナス成長だ、ドイツの成長率はわずか1%、そして中国も減速している。これら全てを政策に織り込まねばならない。世界経済成長原則は米国輸出に悪影響を及ぼすだろう、そしてそれが金融株式市場にマイナス効果を引き起こすだろう、金融政策としてはまず考慮せねばならない。」

As we noted previously in “Data or Markets,” the Fed is not truly just “data dependent.” They are, in many ways, co-dependent on each other. A strongly rising market allows the Fed to raise rates and reduce accommodative as higher asset prices support confidence. However, that “leeway” is quickly reduced when asset prices reverse. This has been the Fed cycle for the last 40-years.

What is that? Here is the definition:

私どもは以前の「Data or Markets」という記事の中でこう書いた、本当はFEDは「データ依存」ではない。それらは複雑に相互依存している。市場が力強く上昇しているときにはFEDは金利を引き上げ、株価推進政策を弱めることができる。しかしながら、株価が反落するとその「裁量範囲」も急速に縮まる。こうして過去40年FEDがサイクルを生み出してきた。FEDが直面する問題は、今や「流動性のわな」にとらわれているということだ。

いったい「流動性のわな」とはどういうことだ?その定義はこういうものだ:

“A liquidity trap is a situation described in Keynesian economics in which injections of cash into the private banking system by a central bank fail to lower interest rates and hence fail to stimulate economic growth. A liquidity trap is caused when people hoard cash because they expect an adverse event such as deflation, insufficient aggregate demand, or war. Signature characteristics of a liquidity trap are short-term interest rates that are near zero and fluctuations in the monetary base that fail to translate into fluctuations in general price levels.”

「流動性のわなとはケインズ経済学で説明される状況であり、中央銀行が市中銀行にマネーを注入しても金利を下げることができずかつ経済成長促進をできない状況だ。流動性の罠が起きるのは人々が現金を貯め込むことにより引き起こされる、というのも彼らがデフレや不十分な需要もしくは戦争のようなことを予感するためだ。流動性のわなの特徴とは短期金利がゼロ近くになり、マネタリーベースを変えても一般物価レベルに反映されなくなる。」

The chart below shows the correlation between the decline of GDP and the Fed Funds rate.

下のチャートが示すのはGDP成長率の低下とFFRの相関を示している。

There are two important things to notice from the chart above. The first is that prior to 1980, the trend of both economic growth and the Fed Funds rate were rising. Then, post-1980, as then Fed Chairman Paul Volker and President Ronald Reagan set out to break the back of inflation, each successive cycle of rate increases were started from a level lower than the previous cycle.

このチャートで大切なことが2つある。まず第一に1980年以前の出来事だ、経済成長率とFFRはともに上昇していた。その後1980以降になると、FED議長 Paul Volkerとレーガン大統領が経済基盤を壊してしまうインフレ政策を取った、その後の金利引き上げサイクルはその開始時の金利が以前のものを下回った。

The difference between the two periods was the amount of debt in the system and the shift from an expansive production and manufacturing based economy to one driven primarily by services which have a substantially lower multiplier effect. Since 1980, it has required increasing levels of debt to manufacture $1 of GDP growth.

この1980年前後の違いは金融システム全体の債務量であることと、もう一つは製造業拡大からサービス業主体の経済にシフトしたことだ、サービス業は基本的に乗数効果が低い。1980年以来、GDPを$1増やすのに必要な債務が増え続けている。

In every case, the rate cycle increase ALWAYS led to either a recession, bear market, crisis, or all three. Importantly, those events occurred not when the Fed STARTED hiking rates, but when they recognized that their tightening process was confronted by weakening economic growth.

どの場合も、金利を引き上げると必ず景気後退、ベア相場、経済危機、のどれかを引き起こすものだ、3つ同時ということもある。大切なことは、これらの出来事が起きるのはFEDが金利引き上げを開始したときではない、そうではなく彼らが引き締め政策が経済成長鈍化に直面したときだ。

The Trap 罠

The problem for the Fed is that while lower interest rates may help spur economic growth in the short-term, the growth has come from an increasing level of debt accumulation. Therefore, the economy cannot withstand a reversal of those rates. As shown above, each successive round of rate increases was never able to achieve a rate higher than the previous peak. For example, in 2007, the Fed Funds rate was roughly 5% when the Fed started lowering rates to combat the financial crisis. Today, if the Fed started lowering rates to combat economic weakness, they would do so from less than half that previous rate.As Richard Clarida noted in his speech, one of the potential risks to Central Banks globally is the lack of monetary policy firepower available. We previously pointed out that in 2009, the Fed went to work to rescue the economy with a $915 billion balance sheet and Fed Funds at 4.2%. Today, that balance sheet remains above $4 trillion and rates are at 2.5%.

FEDのか帰る問題とはこういうことだ、低金利が短期的には経済成長を促進するが、その成長は積み上げられた債務レベル増加によるものだということだ。しかるに、経済は金利政策変更に耐えることができない。上のチャートを見ても解ることだが、一連の金利引き上げは決して前回のピークに達していない。たとえば、2007年には、FFRは5%程度あった、このときFEDは金利を引き下げ始めて金融危機に対処した。現在では、経済の弱さに対処しようとFEDが金利引き下げを始めても、前回の半分の金利からの引き下げとなる。Richard Claridaが彼のスピーチで述べたことだが、世界の中央銀行が抱えるリスクはどこも金融政策の弾が欠けているということだ。私どもが2009年に指摘したことだが、FEDが経済救済を開始したとき、バランスシートは$915Bで金利は4.2%だった。現在、このバランスシートは$4Tを超えており、金利は2.5%に過ぎない。

It isn’t lost on the Fed that if a recession were to occur, their main lever for stimulating economic activity, interest rate reductions, will have little value. Given the amount of debt outstanding and the onerous burden of servicing it, the marginal benefit of lower rates will likely not be enough to lift the country out of a recession. In such a tough situation the next lever at their disposal is increasing their balance sheet and flooding the markets with liquidity via QE.

もし景気後退が起こったとしても、FEDは負けてしまったわけではないが、主要政策である金利引き下げの余地はほとんど効果が無いだろう。すでに多額の債務が積み上がりその債務負荷があるなかで、多少の金利引き下げは経済を景気後退から救済するには不十分だろう。このような困難な状況で次の政策としてはバランスシートを増やし市場にQEで流動性を洪水のように注入することだ。

However, even that may not be enough as both Ben Bernanke and Janet Yellen have acknowledged that they were aware that each successive round of QE was somewhat less effective than the last. That certainly must be a concern for Powell if he is called upon to re-engage QE in a recession or another economic crisis.

しかしながらこういうことをしても充分でないことをBen BernankeとJanet Yellenが言っている、彼らも気づいているが一連のQEを見ても繰り返すほどに効果は薄くなっている。Powellにとっても懸念されることに違いない、次の景気後退や経済危機に直面して再びQEを実行するにしてもだ。

For the Federal Reserve, they are now caught in the same “liquidity trap” that has been the history of Japan for the last three decades. One only needs to look at Japan for an understanding that QE, low-interest rate policies, and expansion of debt have done little economically. Take a look at the chart below which shows the expansion of the BOJ assets versus the growth of GDP and levels of interest rates.

FEDにとって、彼らは今や同じ「流動性のわな」に捕まっている、それは日本が過去30年経験したことだ。誰もが振り返る必要があるのは日本だ、QE,低金利政策、そして債務拡大をしても経済にはほとんど効果がなかった、この国の実例を見るだけで十分だ。下のチャートを見てほしい、ここには日銀資産とGDP成長率そして金利を示している。

Notice that since 1998, Japan has not achieved a 2% rate of economic growth. Even with interest rates still near zero, economic growth remains mired below one-percent, providing little evidence to support the idea that inflating asset prices by buying assets leads to stronger economic outcomes.

注目すべきは、1998年以来日本は経済成長が2%を超えたことがない。金利がほとんどゼロにもかかわらず、経済成長は1%以下を漂っている、これを見れば資産買取により資産価格を膨らまえせても強い経済を生み出さないということを証明している。

But yet, the current Administration believes our outcome will be different.

しかしながら、現在の連邦政府はその結果が違うと信じている。

With the current economic recovery already pushing the long end of the economic cycle, the risk is rising that the next economic downturn is closer than not. The danger is that the Federal Reserve is now potentially trapped with an inability to use monetary policy tools to offset the next economic decline when it occurs.

現在の景気回復期間は十分に長く、次の景気後退が来る可能性が増している。危険なことに、次の景気後退が来てもFEDはそれに対処する弾を殆ど持っていない。

This is the same problem that Japan has wrestled with for the last 30-years. While Japan has entered into an unprecedented stimulus program (on a relative basis twice as large as the U.S. on an economy 1/3 the size) there is no guarantee that such a program will result in the desired effect of pulling the Japanese economy out of its 30-year deflationary cycle. The problems that face Japan are similar to what we are currently witnessing in the U.S.:

この状況は日本がこの30年格闘してきた状況とそっくりだ。日本は巨額の前代未聞の刺激策を取ってきた(経済規模が1/3ということを考えると相対的に米国の倍の規模の刺激を行った)しかしながら、この30年日本経済を見ての通り、そのような政策は期待した効果を引き起こさないだろう。日本が直面する問題は現在米国で見られるものとよく似ている:

- A decline in savings rates to extremely low levels which depletes productive investments

貯蓄率が極端に低下し、生産的な投資が減る - An aging demographic that is top heavy and drawing on social benefits at an advancing rate.

人口動態の高齢化、これが社会保障費をさらに増やす - A heavily indebted economy with debt/GDP ratios above 100%.

大きく債務に依存した経済、債務/GDP比率が100%を超える - A decline in exports due to a weak global economic environment.

世界経済低調で輸出に陰りが見える - Slowing domestic economic growth rates.

国内経済成長率の鈍化 - An underemployed younger demographic.

若年層の失業 - An inelastic supply-demand curve

受給曲線の硬直化 - Weak industrial production

弱い工業生産 - Dependence on productivity increases to offset reduced employment

生産性改善で雇用が減る

投資家、個人にとっての本当の懸念は実経済だ。我々はいま「踊り場」にいるに過ぎない、一方で主要メディアは囃し立てるのとは異なる。経済的風景を見ると明らかになにか欠陥がある、そして現在の長期的なインフレ圧力低下がそれを教えてくれる。FEDにとっての大きな問題は如何にして「流動性のわな」から抜け出すかということだ、経済や金融市場に凹みを生じずに抜け出すかということだ。

The One Thing 一つ大切なこと

However, the one statement, which is arguably the most important for investors, is what Bill Dudley stated relative to the size of the balance sheet and it’s use a tool to stem the next decline.しかしながら、一つの主張がある、投資家にとって最も大切なことだ、バランスシート規模と次の景気後退時にそれを使うことに関して Bill Ducleyがこう述べた。

“The balance sheet tool becomes relevant only if the economy falters badly and the Fed needs more ammunition.”「景気が低迷しFEDがさらなる政策の弾を必要としたとき、そのときに限りバランスシート変更を政策手法とすべきだ。」

In other words, it will likely require a substantially larger correction than what we have just seen to bring “QE” back into the game. Unfortunately, as I laid out in “Why Another 50% Correction Is Possible,” the ingredients for a “mean-reverting” event are all in place.

言い換えるならば、我々が今目の当たりにしているよりももっと大きな調整があっと時のみに「QE」を復活するだろう。残念なことに、私はこういう記事を書いた「どうして今のレベルから50%の調整が起こりうるか」、「平均回帰」がその背景にある。

“What causes the next correction is always unknown until after the fact. However, there are ample warnings that suggest the current cycle may be closer to its inevitable conclusion than many currently believe. There are many factors that can, and will, contribute to the eventual correction which will ‘feed’ on the unwinding of excessive exuberance, valuations, leverage, and deviations from long-term averages.「次の調整のキッカケというのは実際に起こるまでわからないものだ。しかしながらすでに多くの警告が発せられている、現在のサイクルはすでにその週末に近く、それは多くの人が信じているよりも近いものだ。やがてくる調整を引き起こすキッカケはたくさんある、過剰な熱狂、バリュエーション、レバレッジ、そして長期平均からの乖離、これらの巻き戻しがきっかけになるだろう。

The biggest risk to investors currently is the magnitude of the next retracement. As shown below the range of potential reversions runs from 36% to more than 54%.”

今の所投資家にとっての最大のリスクは次の後退の規模だ。下のチャートに示すが潜在的な反落範囲は36%から54%を超える。」

“It’s happened twice before in the last 20 years and with less debt, less leverage, and better-funded pension plans.「過去20年で同様のことが二度起きている、しかも債務量はすくなく、年金基金から多くの資金が提供されていた。

More importantly, notice all three previous corrections, including the 2015-2016 correction which was stopped short by Central Banks, all started from deviations above the long-term exponential trend line. The current deviation above that long-term trend is the largest in history which suggests that a mean reversion will be large as well.

もっと大切なことは、中央銀行が短期で止めた2015−2016の調整を含む過去三度の調整においては、長期的な上昇トレンドから大きく乖離した状態から始まった。長期トレンドからの現在の乖離は史上最大のものであり、平均回帰はそれに比例して大きいだろう。

It is unlikely that a 50-61.8% correction would happen outside of the onset of a recession. But considering we are already pushing the longest economic growth cycle in modern American history, such a risk which should not be ignored.”景気後退以外で50−61.8%の調整が起きそうにはない。しかし我々は現在近代米国史最長の景気回復を推し進めており、そのリスクを無視すべきではない。」

Billは「QE」をツールとして利用できると言うが、FEDが金利をゼロにしてからでないと使われないだろう。ということは「QE」が全面に出てくるときには、投資家のだめっじは現在想定されるものよりももっと大きいだろう。

Yes, the Fed absolutely targets the financial markets with their policies. The only question will be what “rabbit” they pull out of their hat if it doesn’t work next time?

そう、FEDは絶対に金融市場を目標に政策を決めている。唯一の問題は、それが有効でないときに、彼らは手品の帽子のなかからどんな「うさぎ」を取り出すのだろう?

I am not sure even they know.

彼らは知っているかもしれないが、私にはわからない。