Powellは債権ブルを維持

Powell Keeps The Bond Bull Kicking

Written by Lance Roberts | Mar, 21, 2019

In

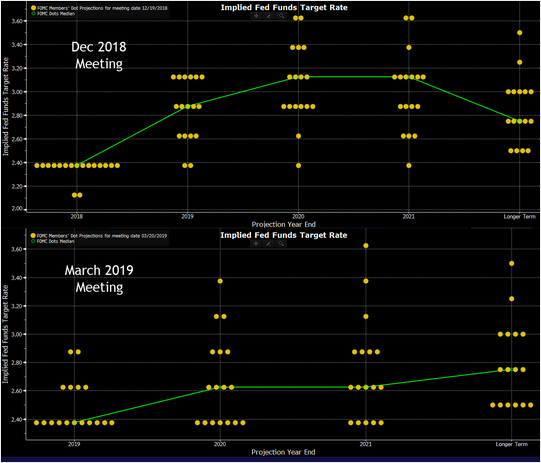

a widely expected outcome, the Federal Reserve announced no change to

the Fed funds rate but did leave open the possibility of a rate hike

next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September.

多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。

The key language from yesterday’s announcement was:

昨日の発表の重要な部分はこういう具合だ:

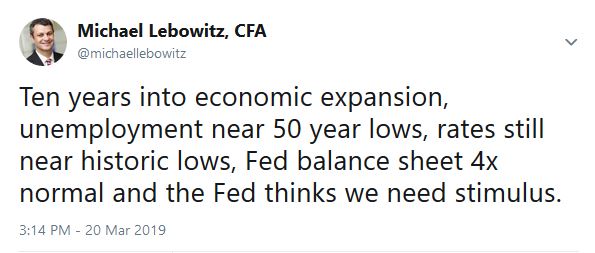

What is interesting is that despite the language that “all is okay with the economy,” the Fed has completely reversed course on monetary tightening by reducing the rate of balance sheet reductions in coming months and ending them entirely by September. At the same time, all but one future rate hike has disappeared, and the Fed discussed the economy might need easing in the near future. To wit, my colleague Michael Lebowitz posted the following Tweet after the Fed meeting:

興味深いことは、言葉では「経済はすべて順調」といいながら、FEDは金融政策では全く引き締めとは逆のことをしている、バランスシート削減を弱め9月には停止するという。同時に将来の金利引き上げもほとんど消え失せた、そしてFEDは近い将来に緩和が必要かもしれないと議論した。FOMC後に私の同僚のMichael LebowitsはこういうTweetを投稿した:

10年も景気拡大が続き、失業率は50年ぶりの低位だ、金利は歴史的な低位にある、またFEDバラランスシートは正常の4xでFEDはさらなる刺激が必要だと考えている。

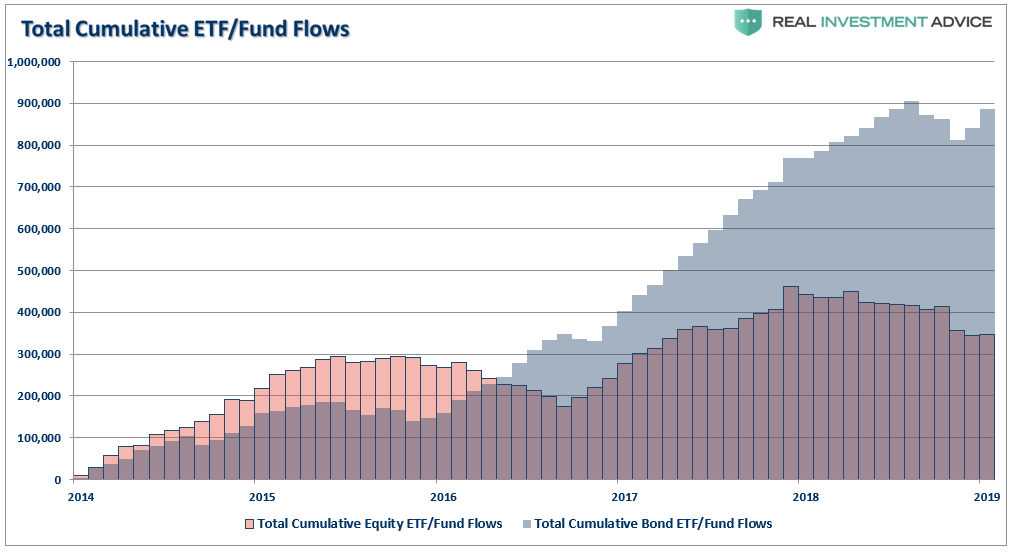

This assessment of a weak economy is not good for corporate profitability or the stock market. However, it seems as if investors have already gotten the “message” despite consistent headline droning about the benefits of chasing equities. Over the last several years investors have continued to chase “safety” and “yield.” The chart below shows the cumulative flows of both ETF’s and Mutual Funds in equities and fixed income.

この弱い経済分析は企業収益や株価を見ているわけではない。そうではなく、株で利益を得ることに喧しい投資家がまるですでに「メッセージ」を受け取ったかのようだ。ここ数年、投資kは「安全」と「金利」を共に追い求めてきた。下のチャートに示すのは株式と金利商品に対するETFや信託商品の累積資金流入を示す。

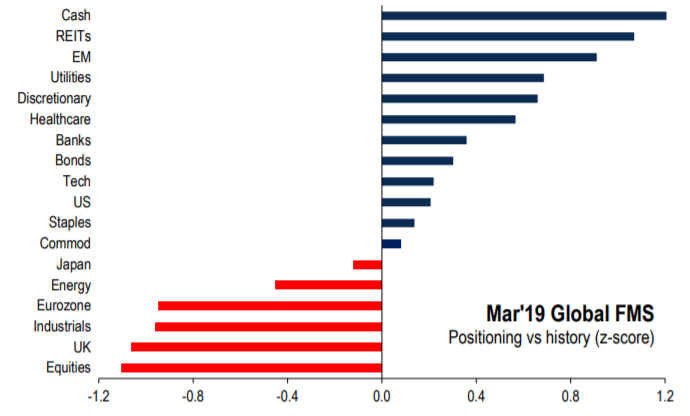

This chase for “yield” over “return” is also seen in the global investor positing report for March.

この「リターン」に対する「金利」追従は世界的な投資家の3月のポジションを見てもわかることだ。

Clearly, investors have continued to pile into fixed income and safer equity income assets over the last few years despite the sharp ramp up in asset prices. This demand for “yield” and “safety” has been one of the reasons we have remained staunchly bullish on bonds in recent years despite continued calls for the “Death of the Bond Bull Market.”

明らかに、投資家は金利商品やより安全な株式に資金を積み上げている、株価急上昇にもかかわらずこの数年の動きはこういうものだ。この「金利」と「安全」に対する需要を見ると、ここ数年我々は断固として債権に強気ということだ、「債権ブル相場の終わり」ということがずっと言われるにもかかわらずにだ。

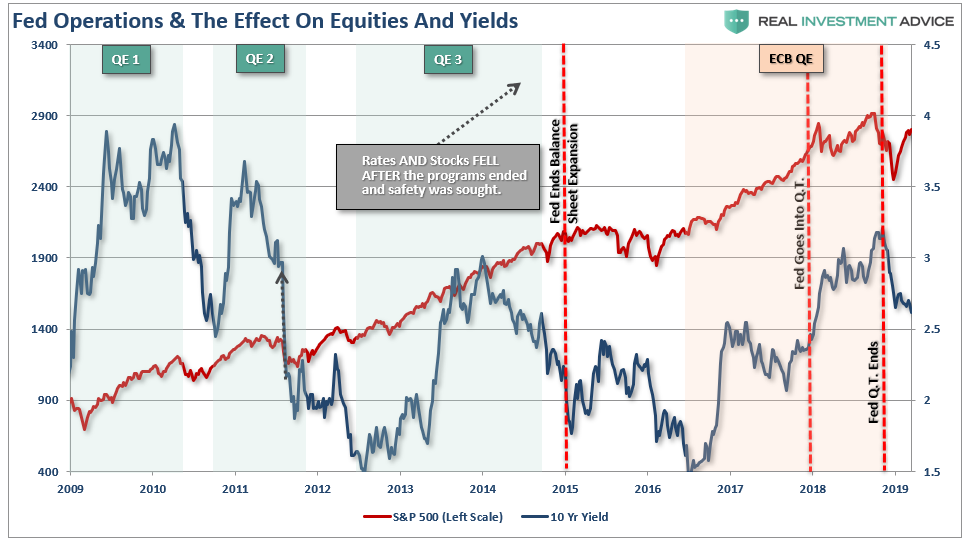

Importantly, one of the key reasons we have remained bullish on bonds is that, as shown below, it is when the Fed is out of the “Q.E” game that rates fall. This, of course, was the complete opposite effect of what was supposed to happen.

大切なことは、我々が債権に強気な理由の一つが、下のチャートに示すとおり、FEDが「QE」をやめると金利が下落する。当然のことながら、このことは本来起こりそうなこととは全く逆だった。

Of course, the reasoning is simple enough and should be concerning to investors longer-term. Without “Q.E” support, economic growth stumbles which negatively impacts asset prices pushing investors into the “safety” of bonds.

当然のことながらその理由はシンプルなもので、投資家の長期的な懸念によるものだ。「QE」の援助がないと経済成長が鈍化し株価にマイナスインパクトを与える、こうなると投資家は債権の「安全」をもとめる。

(訳注:図中の右端のFed QT endsはタイプミスでしょう)

As the Fed now readily admits, their pivot to a more “dovish” stance is due to the global downturn in economic growth, and the bond market has been screaming that message in recent months. As Doug Kass noted on Tuesday:

いまやFEDが認めるように、世界経済成長鈍化により彼らはさらなる「ハト派」スタンスに転換した、そしてここ数ヶ月債券市場はこれに反応している。Doug Kassが火曜にこういうことを書き記した:

米国債10年ものの金利は今朝2.60%を下回った(私は2019年には2.25%まで下落すると見ている)

He is correct, yields continue to tell us an important story.

彼の主張は正しい、金利は常に重要なことを教えてくれる。

First, three important facts are affecting yields now and in the foreseeable future:

まず最初に、現在と近い将来の金利に関して銃用なことが3件ある:

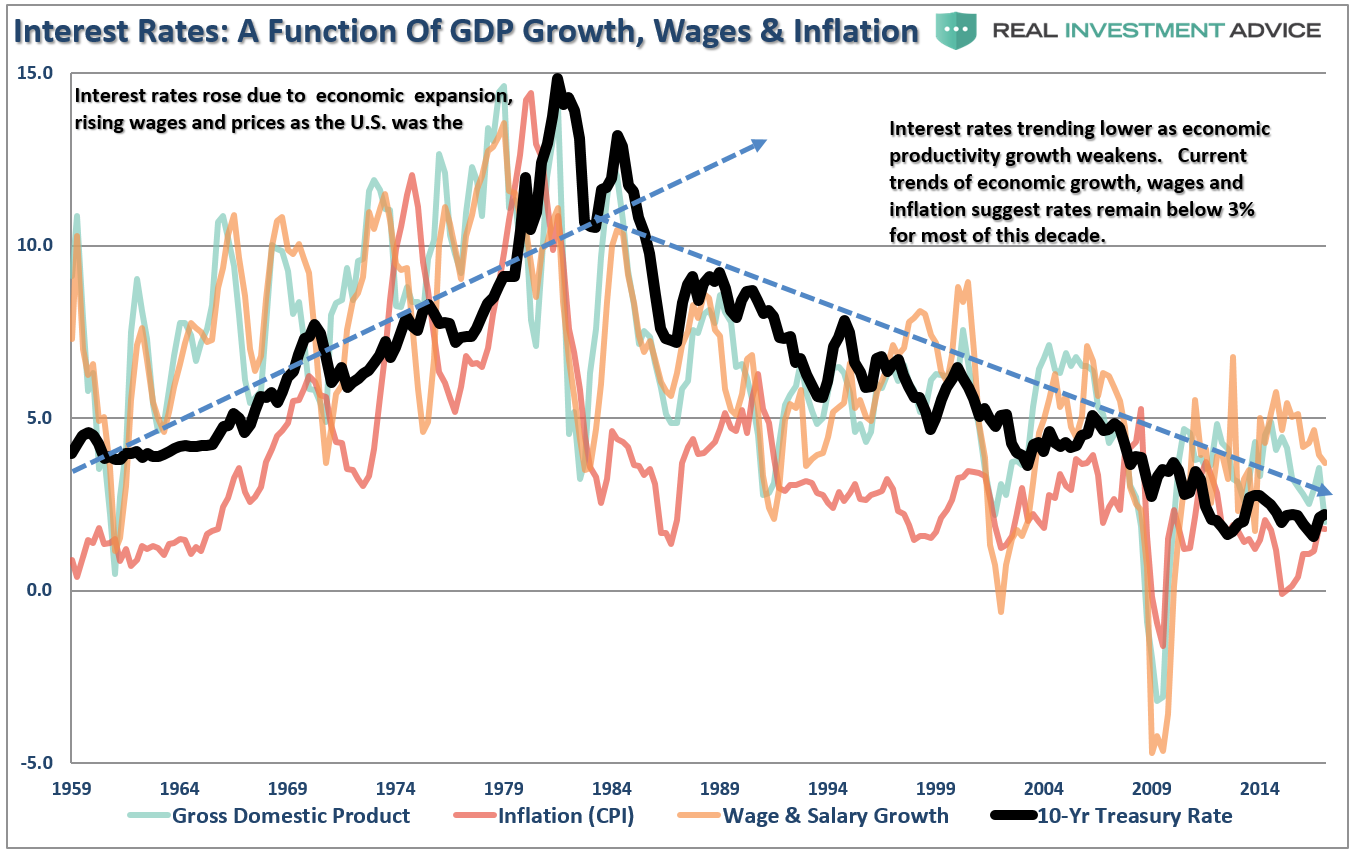

私はこれまで何度も議論してきたが、金利というのは3要因の関数である:経済成長、給与増加、そしてインフレーション。この関係は下のチャートで読み取れる。

Okay…maybe not so clearly.

わかった・・・・それほど明確ではないかもしれない。

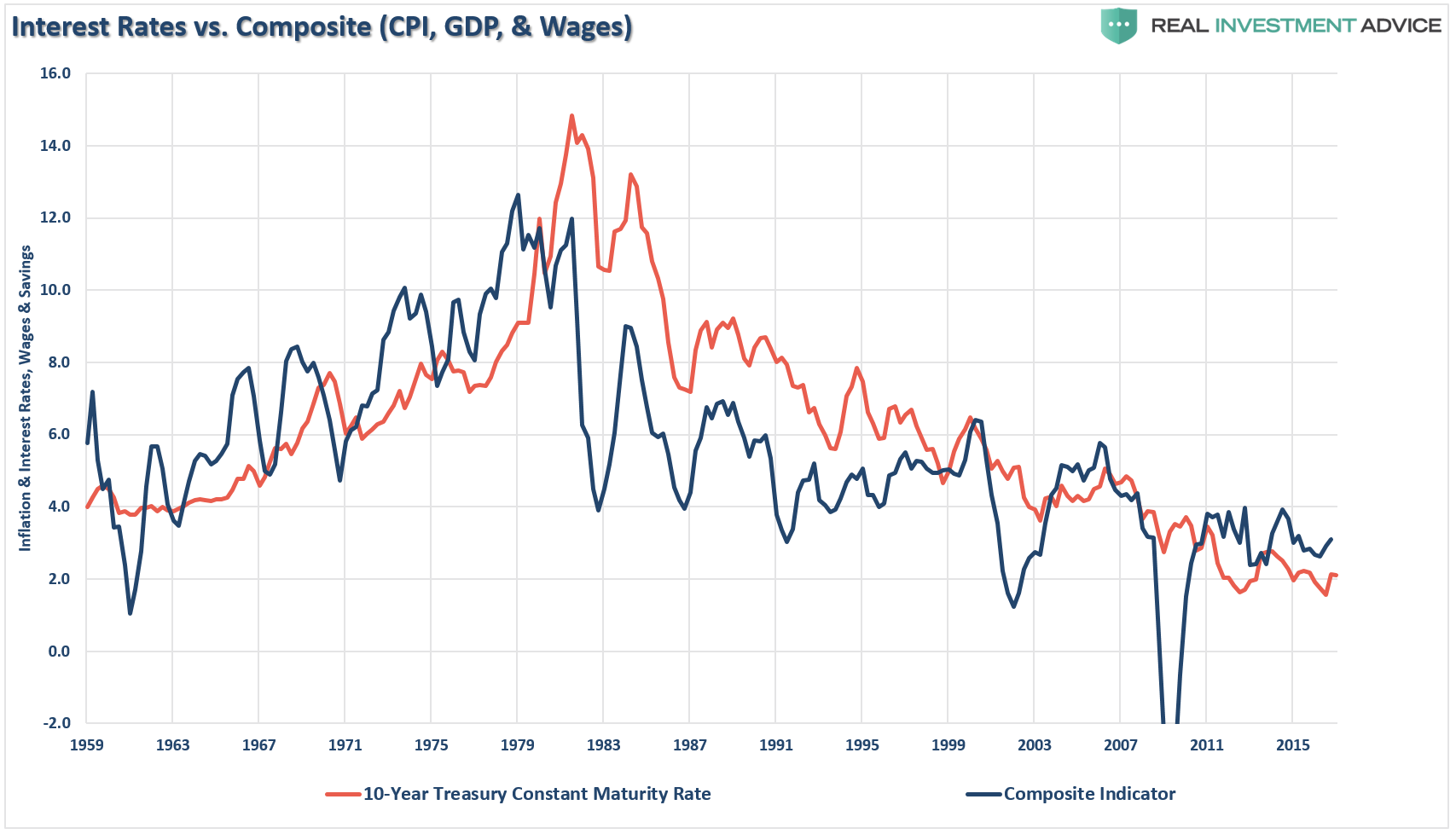

Let me clean this up by combining inflation, wages, and economic growth into a single composite for comparison purposes to the level of the 10-year Treasury rate.

この関係をもっとわかりやすくするために、インフレ、給与、経済成長を一つの複合指数とし米国債10年もの金利と比較しよう。

As you can see, the level of interest rates is directly tied to the strength of economic growth, wages and inflation. This should not be surprising given that consumption is roughly 70% of economic growth.

見ての通り、金利レベルは経済成長、給与、インフレと強い相関関係にある。これは驚くべきことではない、というのも消費は経済成長の70%を占めるからだ。

As Doug notes, the credit markets have been right all along the way. At important points in time, when the Fed signaled policy changes, credit markets have correctly interpreted how likely those changes were going to be. A perfect example is the initial rate hike path set out in December 2015 by then Fed Chairman Janet Yellen. This was completely wrong at the time and the credit markets told us so from the beginning.

Dougが主張するように、債券市場はこれに従ってきた。今まさに大切なことは、FEDが政策変更を発したとき、債券市場はこの変化がどちらに向かうかを解釈するものだ。その良い例が2015年12月の最初の金利引き上げだ、当時FED議長はJanet Yellenだった。彼女の判断はまったく間違っていたわけで、債券市場はそのことを最初から教えてくれた。

The credit markets have kept us on the right side of the interest rate argument in repeated posts since 2013. Why, because the credit market continues to tell us an important story if you are only willing to listen.

2013年以来度々記事にしているが、債券市場は金利動向に対する見通しを教えてくれる。というのも、聞く耳を持つ人には債券市場は重要な知見を与えてくれる。

Since 2009, asset prices have been lofted higher by artificially suppressed interest rates, ongoing liquidity injections, wage and employment suppression, productivity-enhanced operating margins, and continued share buybacks have expanded operating earnings well beyond revenue growth.

2009年以来、人工的に抑圧された金利で株価はそびえ立つほど高くなった、さらに流動性注入がつづき、給与と雇用は抑制された、生産性向上で営業利益は高まった、そして継続する自社株買いで売上成長以上に収益増加が拡大した。

As I wrote in mid-2017:

私は2017年半ばにこう書いた:

「FEDは自らが人工的に作り出した状況を愚かにも信じてしまい、経済の先行きは本当に明るいと信じた。残念なことに、FEDとWall Streetは現在生じている流動性の罠を認識していない、短期金利をゼロにしたためにマネタリーベース変化が高インフレを引き起こさないのだ。

It didn’t take long for that prediction to come to fruition and change the Fed’s thinking.

この予想が現実のものとなるまでにそう時間はかからないだろう、そうなるとFEDも考え方を改めるだろう。

On December 24th, 2018, while the S&P 500 was plumbing it’s depths of the 2018 correction, I penned “Why Gundlach Is Still Wrong About Higher Rates:”

2018年12月24日にS&P500はこの年の大きな調整を迎えた、このとき私はこういう記事を書いた「金利引き上げに関してどうしてGundlachの見立ては間違っているか:」

「どこかの時点でFEDは政策転換して「QE」を始めるだろう、さらにFFRをゼロに逆戻りさせる。

What I didn’t know then was that literally the next day the Fed would reverse course.

この記事を書いたときには私は知らなかったが、文字通りその翌日にFEDは方針を逆転させた。

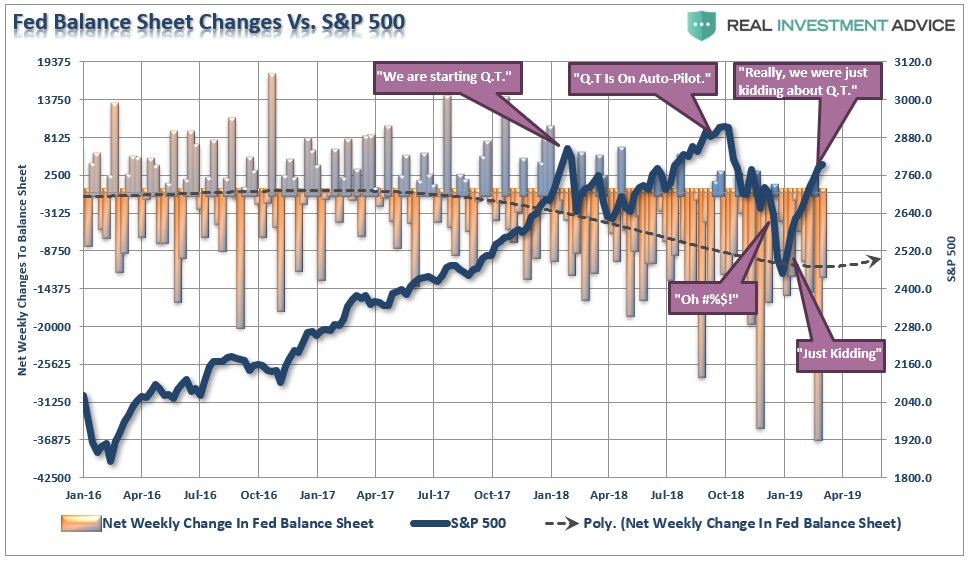

The chart below shows the rolling 4-week change in the Fed’s balance sheet versus the S&P 500.

下のチャートはFEDバランスシート変化の4週移動平均とS&P500を示す。

The issue for the Fed is that they have become “market dependent” by allowing asset prices to dictate policy. What they are missing is that if share prices actually did indicate higher rates of economic growth, not just higher profits due to stock buybacks and accounting gimmickry, then US government bond yields would be rising due to future rate hike expectations as nominal GDP would be boosted by full employment and increased inflation. But that’s not what’s happening at all.

FEDが言うには株価を政策で維持するために「market dependent」としている。彼らが誤解しているのは株価上昇が高い経済成長を示しているということだ、しかし実際には高い利益というのは自社株買いと会計マジックで得たものだ、さらには将来の金利引き上げ期待で米国債金利が上昇し、完全京都インフレ増加で名目GDPも増えるだろうと勘違いした。しかしこういう事は全く起きなかった。

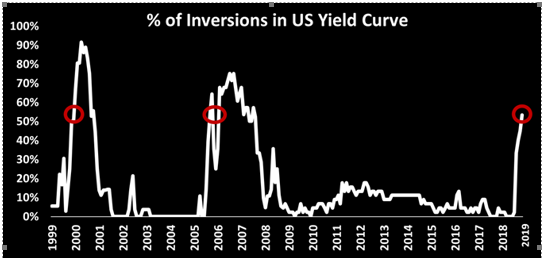

Instead, the US 10-year bond is pretty close to 2.5% and the yield curve is heading into inversion.

むしろ、米国10年債の金利は2.5%に近づき、イールドカーブは反転域に向かっている。

Since inversions are symptomatic of weaker economic growth, such would predict future rate hikes by the Fed will be limited. Not surprisingly, that is exactly what is happening now as shown by yesterday’s rapid decline in the Fed’s outlook.

イールドカーブ反転は弱い経済成長の症例であり、こうなると今後のFED金利引き上げは限られてくることが予想される。驚くことではないが、これはまさに今起きていることで、昨日のFEDの見通しが急落したことで明らかだ。

Why?

どうしてかって?

Let’s go back to that 2017 article:

2017年の記事を振り返ろう:

「しかしながら、資金調達コスト上昇は金融システム全体をウイルスのように蝕む。株式の上昇下落は平均的米国人や国内経済にそれほど影響を与えない。しかし金利はこれとは全く異なる。

All it took was for interest rates to crest 3% and home, auto, and retail sales all hit the skids. Given the current demographic, debt, pension, and valuation headwinds, the future rates of growth are going to be low over the next couple of decades – approaching ZERO.

金利が3%にでもなろうものなら、住宅、自動車、小売売上どれもが滑ってしまう。現在の人口動態、債務、年金、そして株価バリュエーション、どれもが向かい風で、今後何十年も将来の金利増加は低いものでーーゼロに近づく。

While there is little left for interest rates to fall in the current environment, there is also not a tremendous amount of room for increases. Therefore, bond investors are going to have to adopt a “trading” strategy in portfolios as rates start to go flat-line over the next decade.

現在の環境では金利下落余地はほとんど無く、また大きく増加する余地もない。しからうに国債投資家は今後10年は金利にほとんど変化がないということを前提にポートフォリオの「売買戦略」を立てねばならない。

Whether, or not, you agree there is a high degree of complacency in the financial markets is largely irrelevant. The realization of “risk,” when it occurs, will lead to a rapid unwinding of the markets pushing volatility higher and bond yields lower. This is why I continue to acquire bonds on rallies in the markets, which suppresses bond prices, to increase portfolio income and hedge against a future market dislocation.

みなさんがどう思おうが、金融市場にはとても高い安心感があり、これはとても見当違いなものだ。「リスク」が現実のものとなったとき、市場は急速に巻き戻されボラティリティは大きくなり国債金利は低下するだろう。だからこそ私は株式市場でラリーが起きたときに国債を買い続けているわけで、そういうときには国債価格が低下する、将来の株式市場転移時のヘッジとポートフォリオからの収入増のためだ。

In other words, I get paid to hedge risk, lower portfolio volatility and protect capital.

言い換えると、私はヘッジリスクを支払っているわけで、ポートフォリオの変動を低下させ資金保全をしているのだ。

Bonds aren’t dead, in fact, they are likely going to be your best investment in the not too distant future.

国債はa死んだわけではない、実際、そう遠くない将来を見通すなら最良の投資対象となりつつある。

「私は世界の7不思議が何かはしらない、しかし8番目の不思議は複利だ。」ーーBaron Rothschild

多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。

The key language from yesterday’s announcement was:

昨日の発表の重要な部分はこういう具合だ:

“Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter. Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low.「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。

Recent indicators point to slower growth of household spending and business fixed investment in the first quarter. On a 12-month basis, overall inflation has declined, largely as a result of lower energy prices; inflation for items other than food and energy remains near 2 percent. On balance, market-based measures of inflation compensation have remained low in recent months, and survey-based measures of longer-term inflation expectations are little changed.”最近のQ1動向を見ると家計消費増や企業投資は鈍化している。12か月でみると、全体的なインフレは後退している、その主要因はエネルギー価格低下だ;食料とエネルギーを除くインフレ率は2%近くだ。全てを勘案すると、ここ数ヶ月市場が評価するインフレは低いままだ、そして長期インフレ期待にほとんど変化がない。」

What is interesting is that despite the language that “all is okay with the economy,” the Fed has completely reversed course on monetary tightening by reducing the rate of balance sheet reductions in coming months and ending them entirely by September. At the same time, all but one future rate hike has disappeared, and the Fed discussed the economy might need easing in the near future. To wit, my colleague Michael Lebowitz posted the following Tweet after the Fed meeting:

興味深いことは、言葉では「経済はすべて順調」といいながら、FEDは金融政策では全く引き締めとは逆のことをしている、バランスシート削減を弱め9月には停止するという。同時に将来の金利引き上げもほとんど消え失せた、そしてFEDは近い将来に緩和が必要かもしれないと議論した。FOMC後に私の同僚のMichael LebowitsはこういうTweetを投稿した:

10年も景気拡大が続き、失業率は50年ぶりの低位だ、金利は歴史的な低位にある、またFEDバラランスシートは正常の4xでFEDはさらなる刺激が必要だと考えている。

This assessment of a weak economy is not good for corporate profitability or the stock market. However, it seems as if investors have already gotten the “message” despite consistent headline droning about the benefits of chasing equities. Over the last several years investors have continued to chase “safety” and “yield.” The chart below shows the cumulative flows of both ETF’s and Mutual Funds in equities and fixed income.

この弱い経済分析は企業収益や株価を見ているわけではない。そうではなく、株で利益を得ることに喧しい投資家がまるですでに「メッセージ」を受け取ったかのようだ。ここ数年、投資kは「安全」と「金利」を共に追い求めてきた。下のチャートに示すのは株式と金利商品に対するETFや信託商品の累積資金流入を示す。

This chase for “yield” over “return” is also seen in the global investor positing report for March.

この「リターン」に対する「金利」追従は世界的な投資家の3月のポジションを見てもわかることだ。

Clearly, investors have continued to pile into fixed income and safer equity income assets over the last few years despite the sharp ramp up in asset prices. This demand for “yield” and “safety” has been one of the reasons we have remained staunchly bullish on bonds in recent years despite continued calls for the “Death of the Bond Bull Market.”

明らかに、投資家は金利商品やより安全な株式に資金を積み上げている、株価急上昇にもかかわらずこの数年の動きはこういうものだ。この「金利」と「安全」に対する需要を見ると、ここ数年我々は断固として債権に強気ということだ、「債権ブル相場の終わり」ということがずっと言われるにもかかわらずにだ。

The Reason The Bond Bull Lives

債権ブル派が生き続ける理由

大切なことは、我々が債権に強気な理由の一つが、下のチャートに示すとおり、FEDが「QE」をやめると金利が下落する。当然のことながら、このことは本来起こりそうなこととは全く逆だった。

Of course, the reasoning is simple enough and should be concerning to investors longer-term. Without “Q.E” support, economic growth stumbles which negatively impacts asset prices pushing investors into the “safety” of bonds.

当然のことながらその理由はシンプルなもので、投資家の長期的な懸念によるものだ。「QE」の援助がないと経済成長が鈍化し株価にマイナスインパクトを与える、こうなると投資家は債権の「安全」をもとめる。

(訳注:図中の右端のFed QT endsはタイプミスでしょう)

As the Fed now readily admits, their pivot to a more “dovish” stance is due to the global downturn in economic growth, and the bond market has been screaming that message in recent months. As Doug Kass noted on Tuesday:

いまやFEDが認めるように、世界経済成長鈍化により彼らはさらなる「ハト派」スタンスに転換した、そしてここ数ヶ月債券市場はこれに反応している。Doug Kassが火曜にこういうことを書き記した:

“Which brings me to today’s fundamental message of the fixed income markets – which are likely being ignored and could be presaging weakening economic and profit growth relative to consensus expectations and, even (now here is a novel notion) that could lead to lower stock prices. That message is undeniable – economic and profit growth is slowing relative to expectations as financial asset prices move uninterruptedly higher.「現在の金利商品のファンダメンタルズを私はこう見ているーー この状況は無視される傾向にあるが市場コンセンサスに比べ弱い経済と弱い利益成長を予兆させるものだ、更には株価下落を引き起こすかもしれない。この主張を否定することはできないーー株価が上昇し続ける中で、経済や利益成長は鈍化している。

- The yield on the 10 year U.S. note has dropped below 2.60% this morning. (I have long had a low 2.25% forecast for 2019)

米国債10年ものの金利は今朝2.60%を下回った(私は2019年には2.25%まで下落すると見ている)

2s-10s イールドカーブスプレッドは14BPにまで縮まった。

- The (yield curve and) difference between 2s and 10s is down to only 14 basis points.

経済統計速報(たとえば Cass Freight Index)は引き続き国内経済成長鈍化を示している。

- High-frequency economic statistics (e.g. Cass Freight Index) continue to point to slowing domestic growth.

米国自動車販売は明らかに転落している。

- Auto sales and U.S. residential activity are clearly rolling over.

PMIや他のデータは失望するものだ。

- PMIs and other data are disappointing.

設備投資は弱まっている。

- Fixed business investment is weakening.

どの国も世界経済から分離してはいないーーそれはたとえ米国であっても同様

- No country is an economic island – not even the U.S.

欧州は景気後退に近づいている、そして中国は過大表現している(巨額の流動性注入にもかかわらずだ)。」

- Europe is approaching recession and China is overstating its economic activity (despite an injection of massive amounts of liquidity).”

He is correct, yields continue to tell us an important story.

彼の主張は正しい、金利は常に重要なことを教えてくれる。

First, three important facts are affecting yields now and in the foreseeable future:

まず最初に、現在と近い将来の金利に関して銃用なことが3件ある:

- All interest rates are relative. With more than

$10-Trillion in debt globally sporting negative interest rates, the

assumption that rates in the U.S. are about to spike higher is likely

wrong. Higher yields in U.S. debt attracts flows of capital from

countries with negative yields which push rates lower in the U.S. Given

the current push by Central Banks globally to suppress interest rates to

keep nascent economic growth going, an eventual zero-yield on U.S. debt

is not unrealistic.

金利というのはいつも相対的なものだ。世界中を見渡すと$10T以上の債務がマイナス金利であり、米国金利だけが急上昇しようとしているという見方は間違っている。米国債務の金利が高まるとマイナス金利の国から資金が流入し、これが米国金利を押し下げる。経済成長を促進しようと世界中の中央銀行は金利を抑圧しており、米国でもやがてゼロ金利になるのも非現実的ではない。 - The coming budget deficit balloon. Given the

lack of fiscal policy controls in Washington, and promises of continued

largess in the future, the budget deficit will eclipse $1 Trillion or

more in the coming years. This will require more government bond

issuance to fund future expenditures which will be magnified during the

next recessionary spat as tax revenue falls.

今後財政赤字が膨れ上がる。ワシントン政府の財政規律が緩んでおり、今後も気前よい財政政策が予想される、今後数年は財政赤字は$1T以上になるだろう。こうなるとさらなる国債発行が求められ、次の景気後退では税収が弱まり状況をさらに悪化するだろう。 - Central Banks will continue to be a buyer of bonds

to maintain the current status quo. As such they will have to be even

more aggressive buyers during the next recession. The next QE program by

the Fed to offset the next economic recession will likely be $2-4

Trillion and might push the 10-year yield towards zero.

現状維持のためには世界の中央銀行は引き続き国債を買い続けるだろう。次の景気後退では彼らはさらに積極的に買い増さねばならないだろう。次の景気後退対策でのFEDのQE規模は$2−4Tとなりそうだ、さらに米国債10年もの金利もゼロに近づくかもしれない。

私はこれまで何度も議論してきたが、金利というのは3要因の関数である:経済成長、給与増加、そしてインフレーション。この関係は下のチャートで読み取れる。

Okay…maybe not so clearly.

わかった・・・・それほど明確ではないかもしれない。

Let me clean this up by combining inflation, wages, and economic growth into a single composite for comparison purposes to the level of the 10-year Treasury rate.

この関係をもっとわかりやすくするために、インフレ、給与、経済成長を一つの複合指数とし米国債10年もの金利と比較しよう。

As you can see, the level of interest rates is directly tied to the strength of economic growth, wages and inflation. This should not be surprising given that consumption is roughly 70% of economic growth.

見ての通り、金利レベルは経済成長、給与、インフレと強い相関関係にある。これは驚くべきことではない、というのも消費は経済成長の70%を占めるからだ。

As Doug notes, the credit markets have been right all along the way. At important points in time, when the Fed signaled policy changes, credit markets have correctly interpreted how likely those changes were going to be. A perfect example is the initial rate hike path set out in December 2015 by then Fed Chairman Janet Yellen. This was completely wrong at the time and the credit markets told us so from the beginning.

Dougが主張するように、債券市場はこれに従ってきた。今まさに大切なことは、FEDが政策変更を発したとき、債券市場はこの変化がどちらに向かうかを解釈するものだ。その良い例が2015年12月の最初の金利引き上げだ、当時FED議長はJanet Yellenだった。彼女の判断はまったく間違っていたわけで、債券市場はそのことを最初から教えてくれた。

The credit markets have kept us on the right side of the interest rate argument in repeated posts since 2013. Why, because the credit market continues to tell us an important story if you are only willing to listen.

2013年以来度々記事にしているが、債券市場は金利動向に対する見通しを教えてくれる。というのも、聞く耳を持つ人には債券市場は重要な知見を与えてくれる。

The bond market is screaming “secular stagnation.”国債市場は「長期停滞」を伝える。

Since 2009, asset prices have been lofted higher by artificially suppressed interest rates, ongoing liquidity injections, wage and employment suppression, productivity-enhanced operating margins, and continued share buybacks have expanded operating earnings well beyond revenue growth.

2009年以来、人工的に抑圧された金利で株価はそびえ立つほど高くなった、さらに流動性注入がつづき、給与と雇用は抑制された、生産性向上で営業利益は高まった、そして継続する自社株買いで売上成長以上に収益増加が拡大した。

As I wrote in mid-2017:

私は2017年半ばにこう書いた:

“The Fed has mistakenly believed the artificially supported backdrop they created was actually the reality of a bright economic future. Unfortunately, the Fed and Wall Street still have not recognized the symptoms of the current liquidity trap where short-term interest rates remain near zero and fluctuations in the monetary base fail to translate into higher inflation.

「FEDは自らが人工的に作り出した状況を愚かにも信じてしまい、経済の先行きは本当に明るいと信じた。残念なことに、FEDとWall Streetは現在生じている流動性の罠を認識していない、短期金利をゼロにしたためにマネタリーベース変化が高インフレを引き起こさないのだ。

Combine that with an aging demographic, which will further strain the financial system, increasing levels of indebtedness, and lack of fiscal policy, it is unlikely the Fed will be successful in sparking economic growth in excess of 2%. However, by mistakenly hiking interest rates and tightening monetary policy at a very late stage of the current economic cycle, they will likely be successful at creating the next bust in financial assets.”人口動態の高齢化と相まり、金融システムにはさらなる歪が起きるだろう、債務依存が高まり、財政規律が保たれなくなる、FEDが2%以上の経済成長を引き起こすのは望み薄だ。しかしながら、景気サイクルの最終局面で金利引き上げと引き締め政策を間違って実施することで、彼らは次の金融資産破裂を引き起こすだろう。」

It didn’t take long for that prediction to come to fruition and change the Fed’s thinking.

この予想が現実のものとなるまでにそう時間はかからないだろう、そうなるとFEDも考え方を改めるだろう。

On December 24th, 2018, while the S&P 500 was plumbing it’s depths of the 2018 correction, I penned “Why Gundlach Is Still Wrong About Higher Rates:”

2018年12月24日にS&P500はこの年の大きな調整を迎えた、このとき私はこういう記事を書いた「金利引き上げに関してどうしてGundlachの見立ては間違っているか:」

“At some point, the Federal Reserve is going to step back in and reverse their policy back to “Quantitative Easing” and lowering Fed Funds back to the zero bound.

「どこかの時点でFEDは政策転換して「QE」を始めるだろう、さらにFFRをゼロに逆戻りさせる。

When that occurs, rates will not only go to 1.5%, but closer to Zero, and maybe even negative.”これが起きたときには、金利は1.5%程度になるだけでなく、ゼロに近づくだろう、もしかするとマイナス金利となるかもしれない。」

What I didn’t know then was that literally the next day the Fed would reverse course.

この記事を書いたときには私は知らなかったが、文字通りその翌日にFEDは方針を逆転させた。

The chart below shows the rolling 4-week change in the Fed’s balance sheet versus the S&P 500.

下のチャートはFEDバランスシート変化の4週移動平均とS&P500を示す。

The issue for the Fed is that they have become “market dependent” by allowing asset prices to dictate policy. What they are missing is that if share prices actually did indicate higher rates of economic growth, not just higher profits due to stock buybacks and accounting gimmickry, then US government bond yields would be rising due to future rate hike expectations as nominal GDP would be boosted by full employment and increased inflation. But that’s not what’s happening at all.

FEDが言うには株価を政策で維持するために「market dependent」としている。彼らが誤解しているのは株価上昇が高い経済成長を示しているということだ、しかし実際には高い利益というのは自社株買いと会計マジックで得たものだ、さらには将来の金利引き上げ期待で米国債金利が上昇し、完全京都インフレ増加で名目GDPも増えるだろうと勘違いした。しかしこういう事は全く起きなかった。

Instead, the US 10-year bond is pretty close to 2.5% and the yield curve is heading into inversion.

むしろ、米国10年債の金利は2.5%に近づき、イールドカーブは反転域に向かっている。

Since inversions are symptomatic of weaker economic growth, such would predict future rate hikes by the Fed will be limited. Not surprisingly, that is exactly what is happening now as shown by yesterday’s rapid decline in the Fed’s outlook.

イールドカーブ反転は弱い経済成長の症例であり、こうなると今後のFED金利引き上げは限られてくることが予想される。驚くことではないが、これはまさに今起きていることで、昨日のFEDの見通しが急落したことで明らかだ。

Why?

どうしてかって?

Let’s go back to that 2017 article:

2017年の記事を振り返ろう:

“However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy. Interest rates are an entirely different matter.

「しかしながら、資金調達コスト上昇は金融システム全体をウイルスのように蝕む。株式の上昇下落は平均的米国人や国内経済にそれほど影響を与えない。しかし金利はこれとは全く異なる。

Since interest rates affect ‘payments,’ increases in rates quickly have negative impacts on consumption, housing, and investment which ultimately deters economic growth.”金利は「支払い」に影響するため、金利上昇は直ちに消費、住宅、投資にマイナスインパクトを与える、これが圧倒的に経済成長を悪化させる。」

All it took was for interest rates to crest 3% and home, auto, and retail sales all hit the skids. Given the current demographic, debt, pension, and valuation headwinds, the future rates of growth are going to be low over the next couple of decades – approaching ZERO.

金利が3%にでもなろうものなら、住宅、自動車、小売売上どれもが滑ってしまう。現在の人口動態、債務、年金、そして株価バリュエーション、どれもが向かい風で、今後何十年も将来の金利増加は低いものでーーゼロに近づく。

While there is little left for interest rates to fall in the current environment, there is also not a tremendous amount of room for increases. Therefore, bond investors are going to have to adopt a “trading” strategy in portfolios as rates start to go flat-line over the next decade.

現在の環境では金利下落余地はほとんど無く、また大きく増加する余地もない。しからうに国債投資家は今後10年は金利にほとんど変化がないということを前提にポートフォリオの「売買戦略」を立てねばならない。

Whether, or not, you agree there is a high degree of complacency in the financial markets is largely irrelevant. The realization of “risk,” when it occurs, will lead to a rapid unwinding of the markets pushing volatility higher and bond yields lower. This is why I continue to acquire bonds on rallies in the markets, which suppresses bond prices, to increase portfolio income and hedge against a future market dislocation.

みなさんがどう思おうが、金融市場にはとても高い安心感があり、これはとても見当違いなものだ。「リスク」が現実のものとなったとき、市場は急速に巻き戻されボラティリティは大きくなり国債金利は低下するだろう。だからこそ私は株式市場でラリーが起きたときに国債を買い続けているわけで、そういうときには国債価格が低下する、将来の株式市場転移時のヘッジとポートフォリオからの収入増のためだ。

In other words, I get paid to hedge risk, lower portfolio volatility and protect capital.

言い換えると、私はヘッジリスクを支払っているわけで、ポートフォリオの変動を低下させ資金保全をしているのだ。

Bonds aren’t dead, in fact, they are likely going to be your best investment in the not too distant future.

国債はa死んだわけではない、実際、そう遠くない将来を見通すなら最良の投資対象となりつつある。

“I don’t know what the seven wonders of the world are, but the eighth is compound interest.” – Baron Rothschild

「私は世界の7不思議が何かはしらない、しかし8番目の不思議は複利だ。」ーーBaron Rothschild

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

2019/03/21