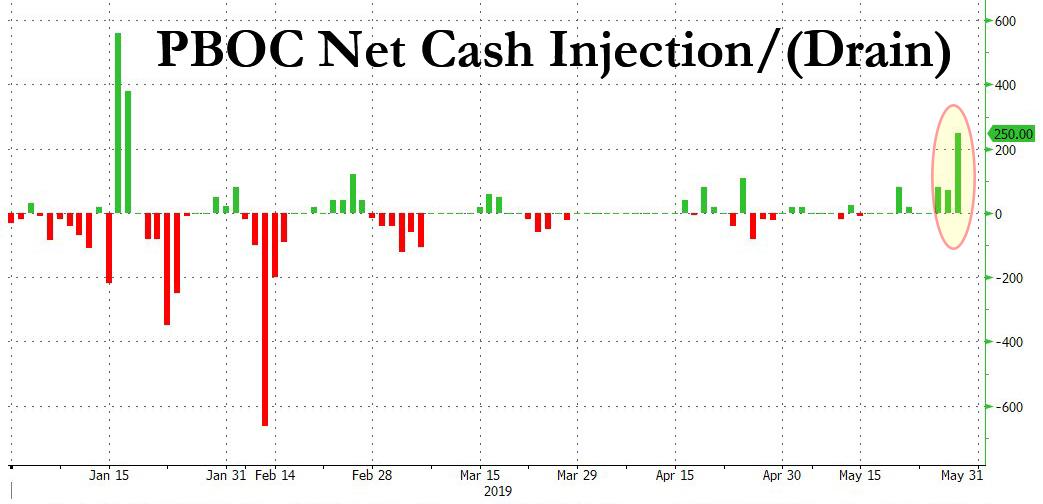

Yesterday we reported that

in the aftermath of the failure of China's Baoshang Bank (BSB), and its

subsequent seizure by the government - the first takeover of a

commercial bank since the Hainan Development Bank 20 years ago - the

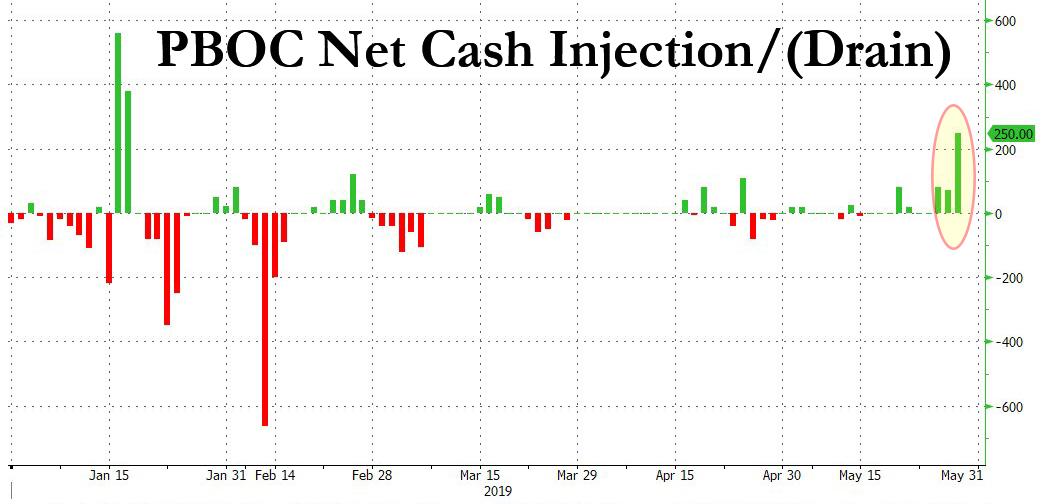

PBOC appeared to panic and injected a whopping 250 billion yuan via an

open-market operation, the largest since January.

昨日ZeroHedgeが記事を書いた、中国のBaoshang Bank(BSB)倒産と国有化の後遺症ーー20年前のHainan Development Bank 海南開発銀行 倒産以来の国有化ーーこれでPBOCはパニック状態になりなんと250B人民元を公開市場操作で注入した、今年1月以来最大のものだった。

And while the bank first failure of a Chinese bank resulted in some

notable turmoil in China's interbank market, where the issuance of

Negotiable Certificates of Deposit was partially frozen as overnight

funding rates spiked, dragging prices of both corporate and sovereign

bonds briefly lower, we warned that "Baoshang is just the tip of the

iceberg."

中国のインターバンク市場が停滞するなかで銀行倒産が生じ、一夜物金利がスパイク急上昇するなかで、Negotiable Certificates of Depositが部分的に凍結された、これが企業債権と中国債をともに短期的に押し下げた、ZeroHedgeはこれを見てこう警告した「Baoshangは氷山の一角に過ぎない」と。

According to UBS analyst Jason Bedford, who in 2017 was the first to

highlight Baoshang’s troubles, there are several other banks that have

“identical leading risk indicators” to Baoshang. Hengfeng Bank, Jinzhou

Bank Co. and Chengdu Rural Commercial Bank all failed to publish their

latest financial statements, have a large portion of their balance

sheets invested in “loan-like investment assets” and are subject to

negative local media coverage.

UBSのアナリストJason Bedfordによると、彼は2017年に最初にBaoshangの抱える問題に注目した人物だ、「Baoshangと同様のリスク指標を持つ銀行がいくつかある」。これらの銀行はまだ最新決算を開示していない、Hengfeng Bank, Jinzhou Bank Co. そしてChengdu Rural Commercial Bankだ、バランスシートのかなりの部分は「ローンに見せかけた投資資産」だ、そして現地のメディアはこの状況をマイナスと捉えて報道している。

To be sure, storm clouds had been gathering above for quite some

time. Here is a quick primer on how BSB was unique, and why it was

especially at risk, courtesy of Barclays.

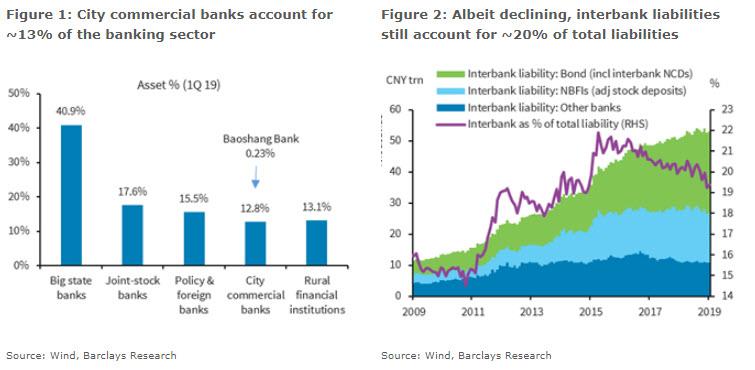

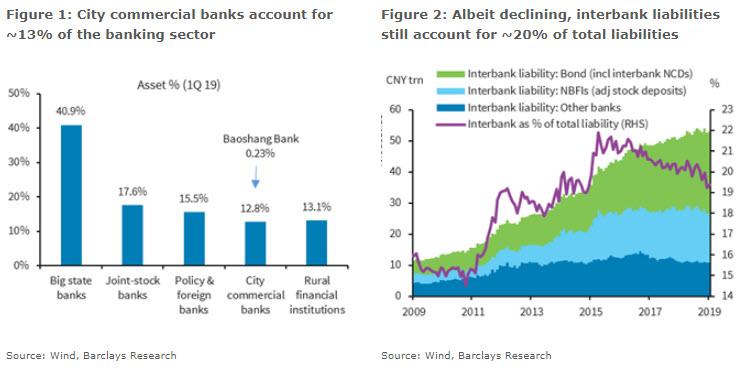

BSB is a city commercial bank (Figure 1), with a AA+ credit rating

from Dagong Credit Rating Group. However, it has faced more problems and

financial difficulties than banks with a similar credit rating. BSB has

not published its annual report since 2016, which to us suggests

significant asset quality stress. Its ratio of 90-day overdue loans to

NPL stood at ~180% in 2016, versus an average of ~110% for similar sized

banks. Meanwhile, its key stakeholder (~30%), Tomorrow Group, has been

under an anti-graft investigation with its founder Xiao Jianhua missing

since 2017.

It has been a notably aggressive player in China’s interbank market, with

~40% of its funding from wholesale sources, compared with a ~25%

average for smaller regional banks, and ~20% for all banks in April 2019 (see Figure 2). As a result, BSB has been hit hard by the deleveraging drive and tightening of the interbank funding channels.

Most of the above was already well-known, at least in the aftermath

of the BSB collapse. What investors are far more curious about is i)

will the failure become systemic, and ii) who will fail next.

Addressing the first question, Barclays analyst Jian Chang writes

that the bank doesn't expect the BSB takeover to cause a systemic crisis

(many would disagree). The reason: the bank's total assets/outstanding

loans/deposits only accounted for 0.23%/0.18%/0.14% of China’s whole

banking system (as of Q3 2017, the latest available data on BSB), and

the PBoC is committed to “keeping eye on the liquidity situation of

medium-to-small banks, and make use of various tools such as OMOs to

ensure reasonably ample liquidity in the system and maintain stability

in the money market rates”.

That said, Barclays admits that the takeover of BSB "highlights

the difficulties and challenges facing some medium-to-small sized banks

arising from China’s deleveraging campaign of the past several years

and a slowing economy." Specifically, during the first phase of

“deleveraging the financial system” (August 2016 - October 2017),

interbank lending, a major funding source facilitating the aggressive

expansion of medium/small banks before, was significantly tightened.

Then as the financial deleveraging extended to the real economy (Nov 17 –

May 18), the resulting rise in corporate delinquency and defaults added

to banks’ credit risks. Then, during the period of policy easing since

the second half of 2018, banks’ asset quality has not been helped by the

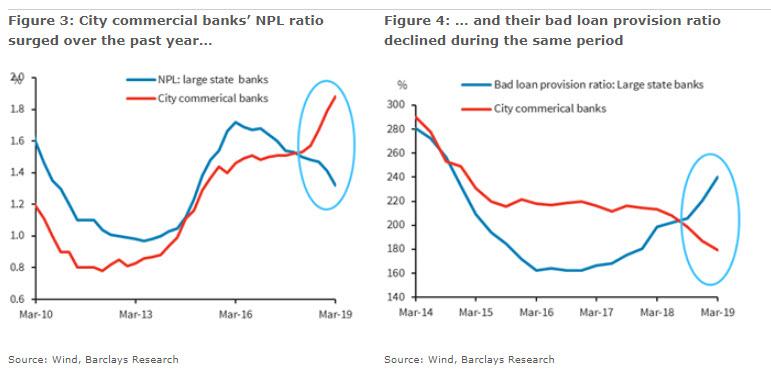

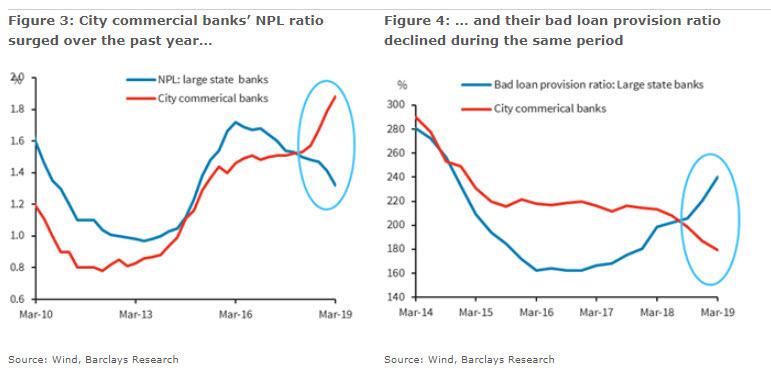

regulator’s push for more SME lending, "as the NPL ratio of

urban commercial banks as a whole rose notably by ~30bp to 1.9% in Q1

19, from 1.6% Q2 18, while their bad-loan provision ratio declined by

30pp to ~180% over the same period (Figures 3-4)." ということで、バークレイ銀行はBSBの国有化をこう解釈している「ここ数年の中国政府の債務削減キャンペーンと景気減速で中小銀行の中には困難が生じている銀行もあることを顕在化せさた」。特に「金融システムの債務削減」の第一フェーズ(2016年8月−2017年10月)においては、かつては中小銀行が積極的に拡大してきた銀行間貸出が大きく引き締められた。その後この金融業界での債務削減が実経済にも拡張された(2018年11月−2018年5月)、結果として企業の返済不能や倒産が銀行の与信リスクを増やした。そして、2018年後半以降は緩和的政策になり、資産の質を監督当局から問われなくなり、小規模銀行の貸出を拡大した、「都市商業銀行の不良債権率は2018Q2の1.6%から30BP増えて2019Q1には1.9%になった、bad loan provision ratio 不良債権引当率(?)は30パーセントポイント減って同じ期間に180%になった(Figure 3-4)。」

As such, Barclays expects more "exits" (read "failures") of smaller

banks or NBFIs (Non-bank financial institutions) either through

takeovers or M&A with bigger parties, most likely with some regional significance (eg.

urban or rural commercial banks. However, in keeping an optimistic

outlook, Barclays does not view a few more bank failures as a systemic

risk, "as the total >130 urban and >1300 rural commercial banks only account for ~10% of the banking sector." というわけで、バークレーは小型銀行やNBFI(ノンバンク金融体、シャドーバンク)においてさらなる「処理」(「損失」)が増えると見ている、処理に際しては大手銀行によるM&Aが伴う。しかしながら、バークレーは楽観的で、さらなる銀行倒産は無いと見ている、「都市銀行は130行を超える中で、1300を超える地方商業銀行の資産規模は銀行セクター全体の10%程度にすぎないからだ」。

Meanwhile, the analyst notes the regulators’ efforts to help banks

replenish their capital through various channels (eg. the recently

introduced perpetual bonds which are a form of quasi QE) as "indicated by the government’s attempts to prevent systemic risks from materializing before they become too great to contain."

Furthermore, the official remarks (listed below) suggest that, even if some FIs are allowed to "experiment"

with bankruptcy, this would only go forward in a controlled and

manageable manner (ie. mainly through mergers and restructuring) to

ensure the government’s bottom line of no systemic risks being created.

Below is a list of selected comments by a Chinese official, in this

case Xiao Yuanqi, the Chief Risk Officer of the CBIRC, in February 2019,

which help understand the regulators’ thinking on smaller FIs, NPL risk

exposure, and planned resolutions:

He said that regulators will continue encouraging smaller and

private players to join the market to expand access to credit for SMEs,

meanwhile they will also work out measures to contain risks associated

with smaller financial institutions (FIs).

While some institutions will be allowed to experiment with

bankruptcy, regulators will mainly use mergers and restructuring to

defuse risks and force unqualified players out of the market.

The authorities will also encourage lenders to step up efforts to

offload their non-performing loans (NPLs). The banking sector has

disposed of CNY3.48trn of bad loans over the past two years, according

to CBIRC data, but commercial banks still have CNY2trn of NPLs on their

balance sheets.

Improving the supply of financing will involve shifting

“inefficient” credit from industries suffering from overcapacity to

areas with greater needs, such as SMEs in innovative and strategic

sectors. Poorly performing companies with little prospect of improvement

will be guided to exit the market through reorganization or bankruptcy.

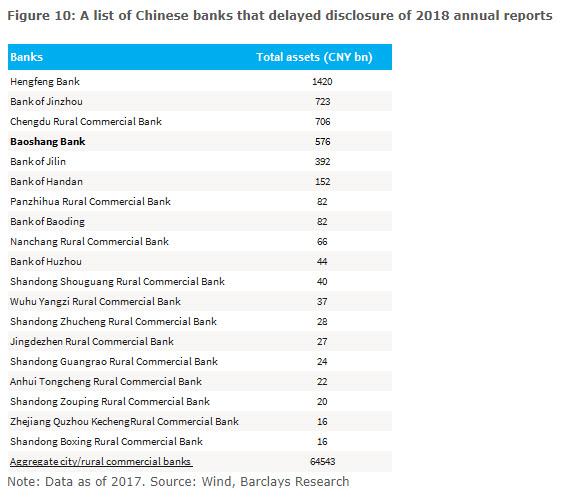

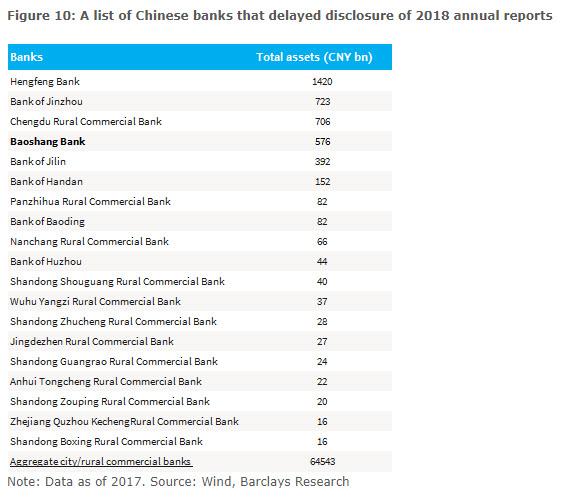

Finally, for those curious which banks are most likely to follow

in Baoshang's footsteps, and fail next, Barclays has compiled a list of regional banks that have delayed publishing 2018 reports, the biggest red flag suggesting an upcoming solvency "event."

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...