もし中国がスーパーパワーを持ちたいなら、相応の規模の自国通貨を発行せねばならず、かつ世界の為替市場に価格発見能力を持たせねばならない。 Quick history quiz: in all of recorded history, how many

superpowers pegged their currency to the currency of a rival superpower? Put another way: how many superpowers have made their own currency dependent on another superpower's currency?

Only one: China. China pegs its currency, the yuan

(RMB) to the U.S. dollar. It adjusts the peg a bit here and there, but

the yuan's value is set by the Chinese state, not by the market of

buyers and sellers.

(Yes, various nations have used gold coins minted by rival powers

(Spanish pieces of eight were money everywhere, for example) but we're

talking about fiat currencies, backed by nothing but supply and demand, not intrinsically valuable gold coins.)

Second question: is pegging your currency to a rival power's currency a sign of strength? The

obvious answer is no. It's a sign of weakness. A real financial power

issues its own currency and let's the global FX (foreign exchange)

market discover the relative price / value of the currency. The

financial power trusts the market to discover the value / price of its

currency, and it responds by raising or lowering the yields on its

government bonds and other pricing inputs. If the issuing nation won't allow users and owners of its currency price discovery, few will want the currency because they can't trust the state's arbitrary, non-market price. This

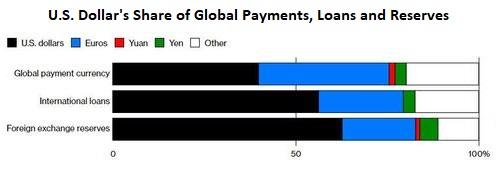

reality is reflected in the chart below of global currencies' relative

share in global payments, loans and reserves. China's currency, the yuan

(RMB) is basically signal noise: its global role in payments, loans and

reserves is near-zero.

Why does China cling to state control of its currency's valuation? The

obvious answer is that China's economy and global role are too fragile

to absorb a major revaluation of its currency up or down: a major loss

in purchasing power would raise the cost of energy and other imports,

while a major strengthening of the yuan would crush the global

competitiveness of China's goods and services. As for the idea that China will unpeg its currency when it

backs it with gold, recall that "backed by gold" means "convertible to

gold." If the yuan weakens and other nation-state owners of the

currency decide gold is the safer bet, China will have to exchange yuan

for gold if it wants to make good on its claim to be backing its

currency with gold.

どうして中国は自国通貨価値の国家支配にここまでこだわるのだろう?答えは明らかで、中国経済とその世界での役割はあまりに脆弱で通貨評価の上下を吸収できないということだ:大きく購買力が下がるとエネルギーや他の輸入コストを上げることになる、一方でRMBが大きく強くなると中国製品の世界的競争力を急落させてしまう。中国がペッグを止めてゴールド裏付けとする議論に関しては、「backed by gold」というのは「convertible to gold」ということだ。もしRMBが弱くなり他国が持つRMBをゴールドに変えたほうが安全と思うと、中国はRMBをゴールドに変えざるを得ない。

If the currency isn't convertible to gold, it isn't backed by gold at all; it's just another fiat currency backed by nothing.

ゴールド変換ができないなら、backed by gold とは全く言えない;全く裏付けのない別の管理通貨ということだ。

If China wants superpower status, it will have to issue its currency in size and let the global FX market discover its price. Anything less leaves China dependent on the U.S. and its currency, the dollar.

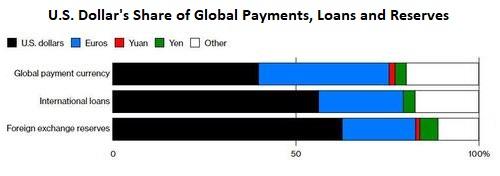

If China is so powerful, why doesn't it let its currency float on the

FX market like other trading nations? Until its currency floats freely

like other currencies and the yuan's price is discovered by supply and

demand, China's global role in currency payments, loans and reserves

will remain near-zero. That is a weakness that appears to be

insurmountable. もし中国が底まで力強いなら、どうして他国のように為替市場の変動相場通貨にしないのか?他国と同様にRMBが変動相場となりRMB価格が需給で決まるようにならないかぎり、支払い・債務・準備金における中国の通貨の役割はほとんどゼロのままだろう。これは明らかに克服できない弱さだ。

* * *

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...