There

was a time when in the years following the financial crisis, every

Friday the FDIC would report of one or more small and not small banks

failing, as their liabilities exceeded their assets, who were taken over

by larger peers with a taxpayer subsidy to cover the capital shortfall.

And while this weekly event, also known as "FDIC Failure Friday" has

faded from the US, for now, it has made a grand appearance in China.

China’s financial regulators said on Friday the country’s banking and

insurance regulator and the central bank, will take control of the

small, troubled inner Mongolia-based Baoshang Bank due

to the serious credit risks it poses. The regulator’s control of

Baoshang will last for a year starting on Friday, the People’s Bank of

China (PBOC) and China Banking and Insurance Regulatory Commission

(CBIRC) said on their websites.

China Construction Bank (CCB) will be entrusted to handle the

business operations of the small lender, based in the industrial city of

Baotou, the statement said.

内モンゴルの小規模貸し手に対しては中国建設銀行が救済する、とその声明に書かれている。

Such a takeover by national authorities is extremely rare, and takes

place amid gathering concerns among regulators and financial analysts

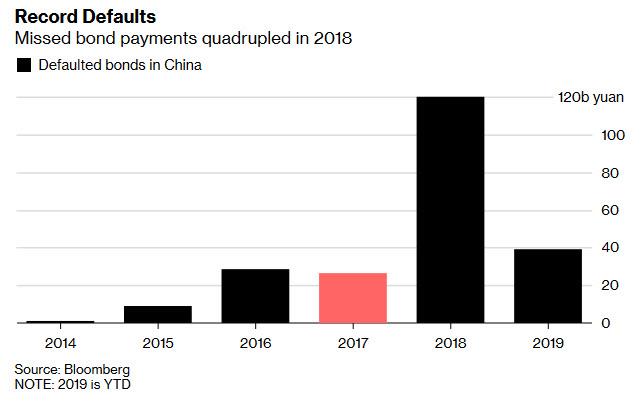

about a renewed surge in bad debts...

... a record pace of corporate defaults,

amounting to 39.2 billion yuan of domestic bond defaults in the first

four months of the year, 3.4 times the total for the same period of

2018...

Moody's analyst Yulia Wan told the WSJ that regulators likely decided

to take over Baoshang to limit any fallout to businesses in Inner

Mongolia. “The move is to reduce the risk of a shock to the local

economy,” said said, adding that the Baoshang takeover appeared

to be the first time that national authorities seized control of a bank

since Chinese lenders started listing on stock markets in the 1990s.

In the past when banks came under pressure, local authorities would

pull together funds from local state-owned firms and investors, or have

another bank stage a takeover.

As Reuters adds, this extremely rare takeover - the

first in nearly three decades - comes at a time when the PBOC has

aggressively eased financial standards and cut reserve ratios for

smaller banks to avoid just this outcome, and highlights the

long struggle of some smaller regional lenders in China, which suffer

from deteriorating asset qualities, inadequate capital buffers, and poor

internal controls and corporate governance

Baoshang Bank rose to prominence after its key stakeholder Tomorrow

Holdings was targeted in a government crackdown on systemic risks posed

by financial conglomerates. The bank was also linked to financier Xiao

Jianhua, according to the WSJ.

Xiao left Hong Kong and crossed the border into mainland China in early

2017, according to statements from Hong Kong police and his company,

and he hasn’t been heard from since.

Later that year, Baoshang "unexpectedly" reported a capital shortage.

この年の遅く、Baoshangは「突然」資金不足を開示した。

Chinese ratings agency Dagong Global Credit Rating Co. then revised its

outlook on Baoshang to negative, questioning the lender’s ability to

repay borrowings. They were right.

中国の格付会社 Dagong Global Credit Rating Coはその時 Baoshanの見通しをネガティブに格下げした、借金返済に際しての貸し手能力に疑念が持たれたのだ。

彼らの判断は正しかった。

Understandably, there is concern the Baosheng takeover "will add to

the vulnerability of country’s financial system amid the economic

slowdown." The reason: if one bank can fail, all can fail. And how long

before depositors jog, run or sprint to their own bank to yank whatever

deposits they have there, in the process beginning the terrifying bank

run domino sequence of events, that eventually collapses China's $40

trillion banking system (by comparison, the US banking system is about

$20 trillion).

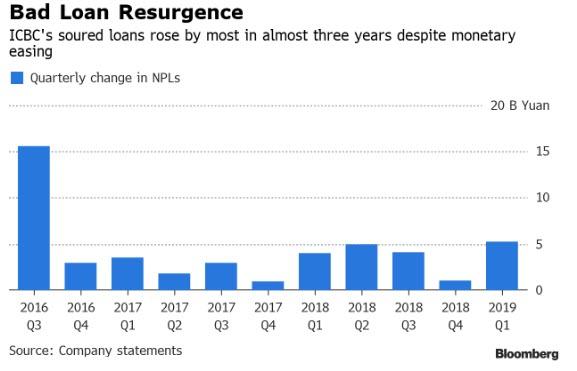

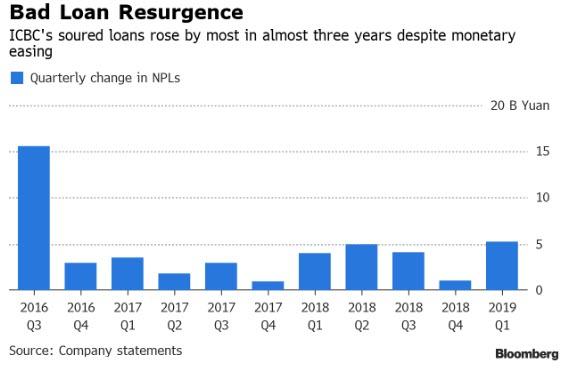

While it has been generally described as a "small" bank, Baoshang

had a total of 156.5 billion yuan ($22.68 billion) of outstanding loans

by the end of 2016, a 65% jump from the end of 2014, according

to the bank’s last filing on its assets and liabilities on its website.

What is absolutely bizarre, however, is that the bank's "official" non-performing loan ratio then was only 1.68% as of December 2016. That,

in itself, would never have been sufficient to force a takeover, and

suggests that not only was the bank's real bad debt ratio much higher,

but that China continues to chronically under-represent the true state

of its NPLs to avoid bank runs.

The last time Baoshang disclosed financial data was in the third

quarter of 2017. Then it had 576 billion yuan in assets and 543 billion

yuan in liabilities, with a net profit of 3.2 billion yuan. Based on

those 2017 numbers, analyst Long Chen with consulting firm Gavekal

Dragonomics estimated that Baoshang back then was ranked around the 50th largest bank in the nation. Baoshangが最後に金融データを開示したのは2017Q3だ。このとき資産が576B人民元で、債務は543B人民元だった、またネット利益は3.2B人民元だった。これらの2017年の数値からすると、Gavekal Dragonomicsコンサルティング会社のアナリストLong Chenの見積もりでは、当時Baoshangは50番目に大きな銀行だった。

Naturally, to avoid a panic bank run among other smaller, less

capitalized banks, the CBIRC said that principal and interest on

personal saving accounts in the bank will be fully guaranteed, and the

business operations of Baoshang bank will not be affected by the

takeover.

The takeover of the bank is the first in decades, and takes place

amid China’s crackdown on systemic financial risks, which in February

2018 resulted in the take over of former roll-up giant and conglomerate

Anbang Insurance, which in 2015-2016 made eyebrow-raising investments in

overseas property, including the Waldorf Astoria hotel in New York.

Anbang’s chairman, Wu Xiaohui, was sentenced to 18 years in prison later

that year after being convicted of fraud and abuse of power. Wu

expressed remorse, according to the court that sentenced him, but he

also said he doubted he violated any laws. He hasn’t made a public

statement since.

The question now is whether bank investors, having seen first hand

for the first time in nearly 30 years, that a Chinese bank can fail (and

be taken over by the state), will jog at a leisurely pace, or not so

leisurely, to their own local bank and pull out their deposits in a

cool, calm and collected manner... or not so cool, calm and collected.

If so, the trade with between the US and China will have a clear winner

in the very near future.

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...