And yet, Regan's less than prescient headline notwithstanding, he made an accurate point in his teaser, namely that "regular investors are leaving."

That, as we have pounded the table week after week after week, has been the real story of 2019 -

not the relentless, artificial melt-up in the market on the back of a

dovish reversal by central banks and the daily US-China trade talk

"optimism" which we now know is not happening.

Confirming that this trend continued for one more week, even as the

S&P hit new all time highs, Bank of America's strategist Jill Carey

Hall writes that last week, during which the S&P 500 was up +0.2%,

virtually everyone sold stocks, as "Institutional clients, hedge funds

and private clients sold the highs in equities last week." And yet,

somehow the S&P hit a new all time high. How? The answer: "Corporate buybacks ramped up."

このトレンドが更にもう一週続くことを確認して、S&Pが新高値となっても、BoAストラテジストのJill Carey Hallは先週こういう記事を書いた、S&P500が0.2%上昇しほとんど誰もが株式を売る中でこういう記事を書いたのだ、「法人顧客、ヘッジファンド、個人顧客は先週の高値で株式を売った」。それでもS&Pは新高値をつけた。どうしてか?その答えは:「自社株買いが積み上がった。」

As BofA elaborates, "buying was led by corporate buybacks, as

all other groups (hedge funds, institutional and retail clients) were

net sellers of equities for the second consecutive week." This

means that for one more week, traditional investors were - as Regan

noted above - boycotting stocks, and were delighted to sell stock back

to the companies that were once again aggressively buying back their own

stock with the S&P hitting all time highs, to wit:

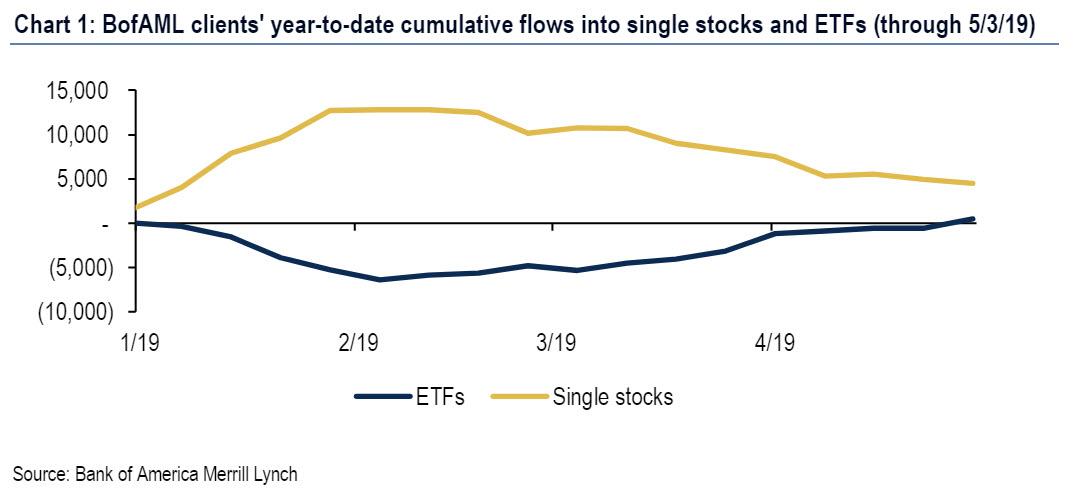

Clients were net sellers of single stocks (2nd straight week), but continued to buy ETFs (8th straight week). Cumulative flows into ETFs YTD turned positive, reversing outflows seen earlier this year (Chart 1).

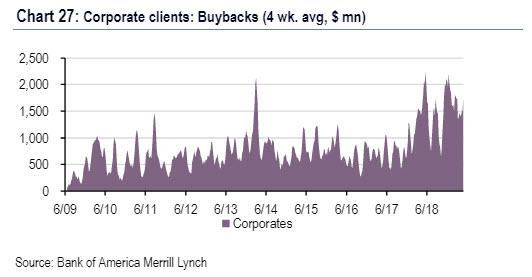

Buybacks last week were their highest since early Feb: they tend to

be strong during earnings seasons and seasonally peak in mid/late May. Buybacks YTD are +20% YoY, though the growth rate continues to decline.

But if everyone else was selling, how did buybacks offset the selling

avalanche? Simple: according to BofA's stock repurchase desk, "buybacks

last week were their highest since early Feb: they tend to be strong

during earnings seasons and seasonally peak in mid/late May. Buybacks YTD are +20% YoY, though the growth rate continues to decline."

While this means that we can once and for all forget about the

recurring lie of a buyback blackout period - which as we explained

before applies only to a very narrow subset of stock repurchases - it

also means that we have reached a level of market lethargy where stock

buybacks are powerful enough to offset all other selling. .

Amazonで買物をしてContrarianJを応援しよう Supply and Demand in Comex Digital Gold by Sprott Money Thu, 07/04/2019 - 09:32 Supply and Demand in Comex Digital Gold Written by Craig Hemke, Sprott Money News A few years ago, we wrote the salient article on the subject of derivative supply and demand on Comex. Given the recent price breakout and sentiment change, it's likely a good idea to re-visit this topic today. 数年前のことだが、私どもはCOMXの派生商品の需給に関する注目記事を書いた。最近の価格ブレークアウトと心理変化もあり、この話題を再度今取り上げるのが良かろう。 The post from 2017 dealt with Comex silver and the original link is below. However, since it is extremely important that you understand this dynamic, I'm going to ask the folks at Sprott Money to reprint the post in its entirely at the bottom of this page. Please take the time to read and study this full article: 2017年の記事はCOMEXシルバーに関するもので、その時のリ...

The Message From The Jobs Report – The Economy Is Slowing Written by Lance Roberts | Apr, 8, 2019 Last week, the Bureau of Labor Statistics (BLS) published the March monthly “employment report” which showed an increase in employment of 196,000 jobs. As Mike Shedlock noted on Friday: 先週、BLSが3月の月例「雇用統計」を発表した、雇用が196,000増えたという。Mike Shedlockは金曜にこう書いた: “The change in total non-farm payroll employment for January was revised up from +311,000 to +312,000, and the change for February was revised up from +20,000 to +33,000. With these revisions, employment gains in January and February combined were 14,000 more than previously reported. After revisions, job gains have averaged 180,000 per month over the last 3 months. 「1月全非農業雇用は+311,000から+312,000に改定された、2月のデータは+20,000から+33,000に改定された。これらの改定で1月と2月を合算した雇用増は以前の報告よりも14,000多くなった。改定後でみると、雇用増は直近三ヶ月で平均180,000/月となる。 BLS Jobs Statistics at a Glance BLS 雇用統計概観 Nonfarm Payroll : +196,000 – Establishment Survey Emp...

「この記事が面白いと思うなら、 Amaz onで買物をしてContrarianJを応援しよう 」 September Class 8 Heavy Duty Truck Orders Collapse 71% by Tyler Durden Fri, 10/04/2019 - 13:10 Preliminary Class 8 order data for September is starting to trickle in and, like the data preceding it so far this year - it's ugly. クラス8トラック発注がことしのこれまでと同様にひどい。 Class 8 orders were crushed 71% in September, reaching 12,600 units, according to Baird and Morgan Stanley. 9月にクラス8トラック発注が71%下落し、12,600台となった、Baird and Morgan Stanleyのデータだ。 This follows a 79% plunge in August. 8月の79%下落に次ぐ悪さだ。 This makes September the 11th consecutive month of YOY order declines and the 9th consecutive month of orders below 20,000. この9月で11か月連続でYoY発注が下落している、また9か月連続で20,000台を下回った。 Class 8 orde...