Goldman On Gold:「ラストリゾート通貨として買うときだ」

ひと月前のことだ、ゴールドマン・サックスが、金利が加減に近づくと貴金属にとっては望ましい、と示唆した、ゴールドは最安全資産とみなされている。

At the start of March, Goldman's head of commodity strategy said there is one commodity that will be safe: gold "which - unlike people and our economies - is immune to the virus."

3月初めに、ゴールドマン・サックスのコモディティストラテジ主任がこういった、安全なコモディティは唯一つ:ゴールドだ、「人間や我々の経済と違いーーウイルスに感染しない。」

And now, Jeffrey Currie and Mikhail Sprogis are saying The Fed's "open ended" QE reverses funding stresses and will offset the negative impact from lower EM demand:

そして今では、Jeffery CurrieやMikhail Sprogisがこういう、FEDの「オープンエンドQE」が流動性不足状況を反転させ新興市場からの低需要を相殺するだろう。

"We are likely at an inflection point [for gold] where 'fear'-driven purchases will begin to dominate liquidity-driven selling pressure as it did in November 2008."

「我々はいまやゴールドに関する変曲点にいる、「恐怖からくる買い」が流動性確保による売りを上回るだろう、それは2008年11月にも起きたことだ。」

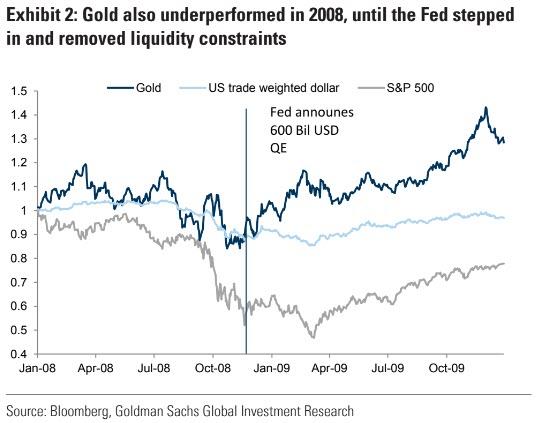

In 2008, the turning point for bullion was the announcement of $600b QE in November, after which gold began to climb despite further weakness in equities and commodities.

こういう状況で、ゴールドマンは短期長期ゴールド見通しを上げている、「とても建設的」であると言い、今後12か月の目標値を$1,800/オンスとした。2008年には、金塊のターニングポイントは11月の$600B QEだった、その後株式やコモディティの弱さにも関わらずゴールドは上昇を続けた。

A similar pattern is emerging as gold prices stabilized over the past week and rallied as the Fed introduced new liquidity injection facilities.

先週のゴールド価格安定を見ると同様のパターンが出現している、そしてFEDが新たな流動性注入宣言するにともないラリーを引き起こした。

Goldman's full note below:

ゴールドマン主張の全文はこういう具合だ:

私どもは長らくゴールドをラストリゾート通貨とみなしてきた、現在のような株価下落となったとき株価維持のために政府が通貨切り下げをするときのヘッジとして機能する。

So why has the gold price fallen? The answer is the world is short dollars.

ではどうしてゴールド価格が下落したのだろう?答えは世界中のドル不足だ。

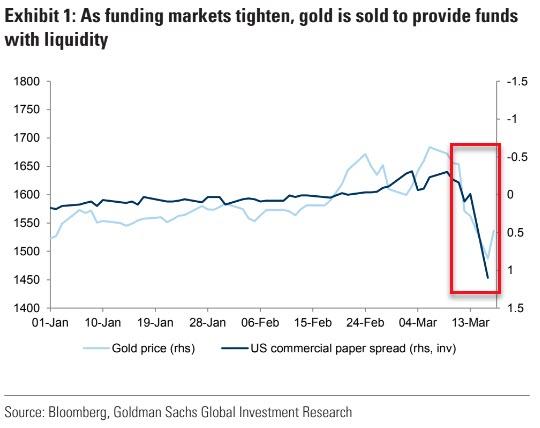

First, both physical and financial market participants face severe funding constraints; they have been forced to sell liquid positions which include gold and other commodities to generate dollars for other funding needs (see Exhibit 1).

最初に、現物市場、金融市場参加者は深刻な資金不足に直面している;彼らにとってゴールドであろうと他のコモディティであろうと流動性を得るために売らざるを得なかった、こうして得たドルで他の資産購入に利用するのだ(図1を見よ)。

Second, large falls in the price of oil have created dollar shortages for emerging market (EM) economies. This has become particularly apparent with the Russian central bank in the past several weeks as the oil price decline shifted Russia from a net buyer of gold to a possible net seller.第二に、原油価格が大きく下落したために、新興国経済ではドル不足となった。これが顕著なのがロシア中央銀行であり、ここ数週原油価格低下でロシアをこれまでのゴールド買い手から売り手に転換させた。

We believe that yesterday’s announcement from the Fed for ‘open ended’ QE reverses these funding stresses and offsets the negative impact to EM wealth and are recommending buying December 2020 gold.

昨日のFEDの「オープンエンドQE」がこの資金不足状況を反転させ新興国資産のマイナスインパクトを相殺したと、私どもは信じている、そして私どもは2020 Decmberのゴールド買いを推奨している。

2) Gold has been severely impacted by liquidity issues, correcting by $120 (-7%) from its peak.

ゴールドは深刻な流動性問題に直面してきた、直近天井から$120(−7%)の調整となった。

The situation resembles 2008, when gold also failed to act as safe-haven asset initially, falling by around 20% due to dollar strength and a run into cash. In 2008, the turning point was the announcement of $600bn QE in November, following which gold began to climb despite further weakness in equities and commodities (see Exhibit 2).

この状況は2008年と類似している、当時ゴールドは当初セーフヘブンとして機能しなかった、ドルの上昇に伴い20%程度下落した、現金不足だったのだ。2008年のターニングポイントは11月の$600BのQE発表だった、その後株式やコモディティのさらなる下落をよそ目にゴールドは上昇を始めた(図2)。

We are beginning to see a similar pattern emerge as gold prices stabilized over the past week and rallied the last two days as the Fed introduced new liquidity injection facilities with this morning’s announcement.

我々は同様のパターンを目撃し始めている、先週のゴールド価格安定とその後二日間の上昇、そして今朝のFEDの新たな流動性注入後の値動きだ。

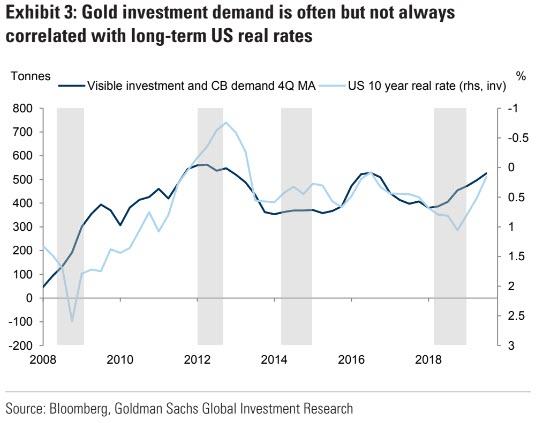

3) We analyze gold through the prism of our ‘Fear and Wealth’ framework, where ‘Fear’ of currency debasement is the primary driver of developed market (DM) investment demand while ‘Wealth’ is the primary driver of EM purchases.

私どもはゴールド価格動向を弊社独自の「Fear and Wealth」枠組みで分析している、新興国市場で通貨切り下げの「恐怖」が主要な投資需要だったが、これが次には新興国購入の目的が「資産形成」と変わる。

Debasement ‘Fear’ is often, but not al ways, correlated with US long-term real rates (see Exhibit 3).

通貨切り下げ「恐怖」はよくあるものだが、いつでもそういうわけでもない、米国の長期実金利と相関している(図3)。

With funding stresses likely eased, focus will likely shift to the large size of the Fed balance sheet expansion, increase in fiscal deficits in DM economies as well as issues around the sustainability of the European monetary union.

流動ストレスが緩和されるに連れ、FEDのバランスシート拡大が注目されるだろう、さらには先進国経済の財施赤字と欧州金融システムの持続性に関して。

We believe this will likely lead to debasement concerns similar to the post GFC period. Accordingly, we are likely at an inflection point where ‘Fear’-driven purchases will begin to dominate liquidity-driven selling pressure as it did in November 2008. As such, both the near-term and long-term gold outlook are looking far more constructive, and we are increasingly confident in our 12-month target of $1800/toz.

GFC大金融危機後に懸念されたのと同様に通貨切り下げが懸念されると私どもは信じている。さらには、私どもは「恐怖に基づく買い」から流動性を得るための売り圧力に打ち勝つ変換点を目の当たりにするだろう、これは2008年11月に経験したことだ。こうなると、短期長期的にさらに強気の見通しとなる、そして私どもは今後12か月の目標価格が$1800/オンスと固く信じている。

4) While ‘Wealth’ is likely to continue to be a headwind for gold, particularly in the near term as oil prices, EM growth and EM currencies remain under pressure, China and other parts of Asia are showing reassuring signs of recovery.

「資産効果」がゴールドに対して逆風になるだろう、特に短期的には原油価格、新興国経済成長と新興国通貨は圧力に晒せれている、しかしながら中国やその他のアジア諸国は回復の兆しが見える。

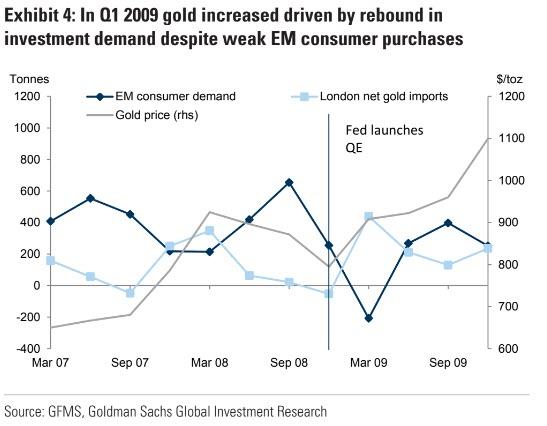

Last week we reduced our 6-month gold price target by $50/toz to $1700/toz to reflect the impact of lower EM ‘Wealth’, and we believe this has already been reflected in current gold pricing. Continuing to draw on the 2008 parallel, we believe that the increase in ‘Fear’-driven investment demand is likely to trump the negative ‘Wealth’ shock in the near term (see Exhibit 4).

先週、私どもは6ヶ月後のゴールド目標価格を$50/オンス減らし、$1700/オンスとした、新興国の「資産効果」を考慮してのものだ、そしてすでにこの効果は現在のゴールド価格に織り込み済みだと私どもは信じている。2008年との類似点を見ながら、「恐怖手動の投資需要」が短期的な「マイナス資産効果」に打ち勝つと信じている(図4)。

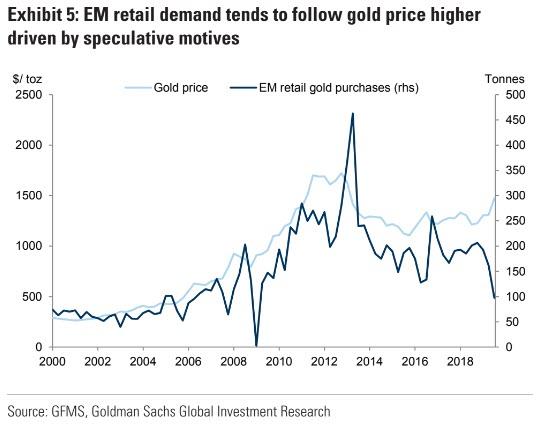

As gold demand can be deferred as opposed to permanently lost like energy demand, we expect as Asian EM economies stabilize, EM gold demand will rebound strongly as consumers make up for missed purchases, particularly for speculative purposes as they have done in the past when chasing a trending market (see Exhibit 5).

エネルギー需要のように永久に着せ去るのではなくゴールド需要後退は一時的なものだろう、私どもはアジア新興国経済の安定化を予想している、消費者が買いそびれたのを補うために新興国ゴールド需要は強く復活するだろう、特に過去にも彼らがトレンドを追いかけたように投機的な目的が増えるだろう(図5)。

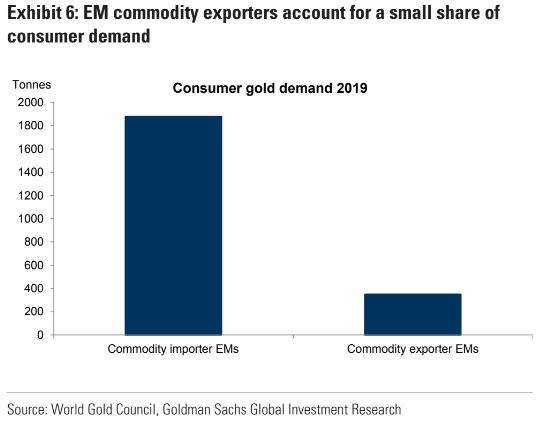

5) However, the wealth outlook for commodity-rich EMs is not as optimistic in the near term, but their demand for gold is not as large as that from the Asian EMs.

しかしながら、短期的にはコモディティ主体の新興国の資産効果はそれほど楽観視できない、しかしそれらの国のゴールド需要はアジア新興国ほどではない。

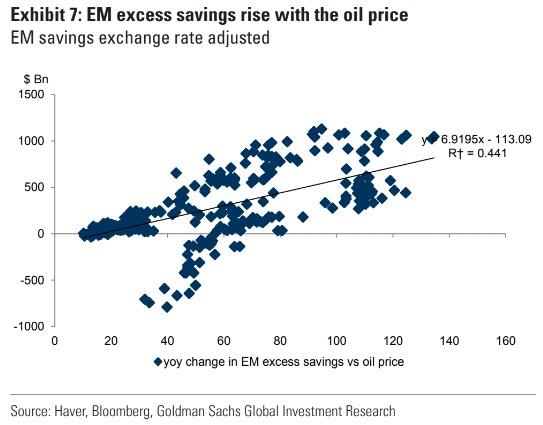

So while we are comfortable being long gold, it doesn’t mean that our FX strategists believe that the dollar shortages are behind us or that we would want to be long other commodities. As we have argued in the past, given the size of the global oil market, a drop in the oil price of recent magnitudes accentuates dollar shortages as oil and commodity prices are highly correlated with the accumulation and dissipation of EM excess savings (see Exhibit 7).

というわけで、私どもはゴールドロングとしている、しかし私どものFXストラテジストはドル不足が続くとも見ていない、他のコモディティも買い増すだろう。私どもは以前にも言ってきたが、世界原油市場の規模を見たとき、最近の原油価格下落規模はドル不足を引き起こすだろう、原油とコモディティ価格は強い相関があり、新興国の過剰貯蓄に依存する(図7)。

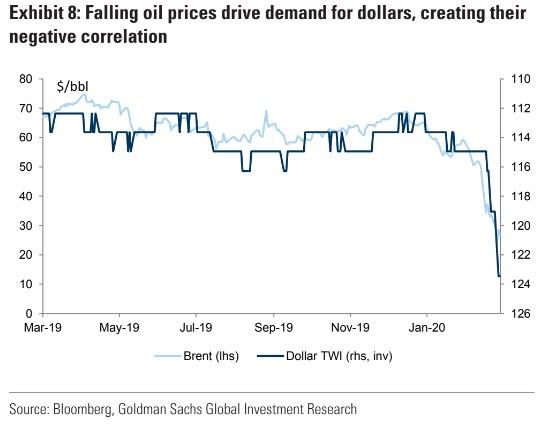

Financial markets normally transform these excess savings into greater global liquidity, supporting asset valuations and improving credit conditions globally. Hence, when weak commodity prices create a draw on EM savings they act as a drag on financial conditions and a headwind on gold prices as dollars become more scarce. Accordingly, the negative oil-dollar price correlation has been re-established (see Exhibit 8).

通常は金融市場はこのような過剰貯蓄は大きな流動性を引き起こす、世界的な資産バリュエーションや与信条件改善を伴うものだ。ところが、コモディティ価格が弱まると新興国の貯蓄が減り、金融環境が変化してゴールド価格に逆風になる、ドル不足になるからだ。それに伴い、原油ードル相関がマイナスになる(図8)。

6) Ultimately, once their GDP stabilizes, EM consumers should help prolong the current ‘Fear’-driven bull market in gold.

最終的には、GDPが安定すると、新興国消費者は「恐怖」に基づく現在のブル相場を引き伸ばすはずだ。

Drawing one last parallel to 2008, while EM wealth continues to be under pressure due to the reasons cited above, once the COVID-19 crisis abates, we see potential for sequential improvement in Asian EM growth to lead DM out of the crisis as it did in 2008/09. This China-driven growth will likely give rise to inflationary concerns given the sharp expected contraction in oil and other commodity supply like agriculture and livestock. Combined with the fiscal nature of the current policy response to COVID-19, we believe physical inflationary concerns with the dollar starting near an all-time high will for once dominate financial asset inflation that was a feature of the past decade. Such inflationary concerns should further support gold prices as the currency of last resort.

これもまた2008年の類推からすると、新興国資産に下落圧力が続くと、武漢コロナ機器が収まったとき、アジア新興国が次々と改善することで危機を脱した新興国を手助けする、これが2008/09に起きたことだ。この中国主導の成長がインフレ懸念を引き起こし原油や穀物供給に圧力をかけると思われる。現在の武漢コロナ対策経済対策と相まり、ドルが高くなり現物インフレ懸念で金融資産インフレを引き起こすだろう、これは過去10年に起きたことだ。このようなインフレ懸念がさらにゴールド価格を支持してラストリゾート通貨となるだろう。

* * *

So, Gold, which a WSJ "expert" idiotically called a "pet rock" back in 2015...

というわけで、2015年にはWSJの「専門家」に、ゴールドは愚か者の「お守り石」に過ぎないと言われた・・・

... is according to Goldman the last thing and only thing that might store value, namely "the currency of last resort and avoids the concern that paper currencies could be a medium of transfer for the virus. As a result, gold has outperformed other safe haven assets like the Japanese Yen or Swiss Franc" a trend Goldman sees continuing as long as uncertainty around the full impact of COVID-19 remains, which will be the case for a long time, and is also why gold is currently the best performing asset class YTD, a "once in a decade event" as the last time this happened was back in 2010.

・・・・これが最近ゴールドマンが考えているところだ、そしてゴールドは価値を保存する唯一のものだ、すなわち「ゴールドはラストリゾート通貨であり、紙幣のようにウイルスを運ぶ心配もない。結果として、ゴールドは安全通過といわれる日本円、スイス・フランを遥かに凌ぐものだ」ゴールドマンは武漢コロナの影響が強まる不確実な世の中が長引くと見ており、だからこそYTDでゴールドはベストパフォーマンスを示している、前回「10年に一度の同様の出来事」が生じたのは2010年のことだ。