ただし債務先進国の日本では、家計300兆円、非金融法人400兆円、政府1300兆円とGDPの400%程度の債務を積み上げてもまだ問題が顕在化しません。今も毎年政府債務は30兆円増え続けており、一方GDPはほとんど増えていません。多分海外の政策立案者はこれを先例 or 目安として見ているような気がします。

When

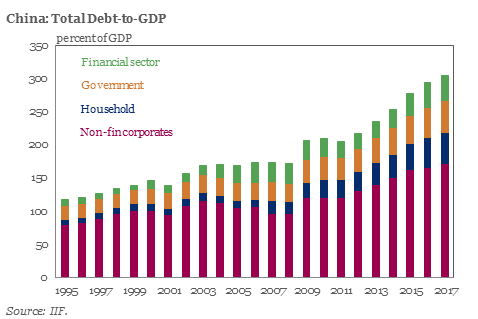

it comes to estimating China's total outstanding debt, there has long

been confusion about the real number with most putting the debt/GDP at

around 250%, while the IIF in 2017 calculated China's debt load as high

as 300% of GDP (which means that by now it is substantially higher).

Then, last year, China watchers added another 40% of debt/GDP to the total when, as S&P calculated,

China’s local governments had accumulated 40 trillion yuan ($6

trillion) - or even more - in off-balance sheet, or Local government

financing vehicles (LGFV) debt, an amount Bloomberg has dubbed China's "hidden debt bomb", suggesting the already record surge in defaults in 2018 is set to accelerate further.

昨年になり、中国ウオッチャーはさらに政務/GDPを40%追加した、S&Pの試算では、中国の地方政府は40T人民元($6T)以上の簿外債務があるとみている、Local government financing vehicles LGFV の形を取ることもある、この債務をブルームバーグは「中国の隠れ債務爆弾」と揶揄する、すでに2018年の倒産は急増しているが、これがさらに加速することを示唆している。

"The potential amount of debt is an iceberg with titanic credit risks," S&P credit analysts wrote in October 2018,

with much of the build-up related to local government financing

vehicles, which don’t necessarily have the full financial backing of

local governments themselves.

Local government debt has quickly emerged, together with "shadow

banking" debt, as one of the main risks for China's economy, because

with the national economy slowing, and as a result of a crackdown on

shadow lending and a Beijing quota for issuance of local-government

bonds not enough to fund infrastructure projects to support regional

growth, authorities across the country have resorted to LGFVs to raise

financing, according to S&P. That’s left LGFVs “walking a tightrope”

between deleveraging and transforming their businesses into more

typical state-owned enterprises, S&P warned.

So fast forward 6 months, when in China's ongoing attempt to contain

the soaring financial risks from its debt bubble, Beijing - seemingly

content with the progress it has made on containing shadow debt - is

re-focusing on the "hidden debt" owed by local governments, as officials

seek to reduce repayment pressures amid falling tax revenues.

And with Beijing adding pressure on local authorities to become more transparent with their liabilities, Bloomberg reports that provinces

and cities from Jiangsu in the east to Qinghai in the west are looking

for means to pay-off or restructure their implicit borrowings, which

include trillions in "off the books" funding via financing vehicles.

Some authorities are seeking cheap refinancing from the nation’s largest

policy lender, the China Development Bank, and others are selling off

state-owned assets such as office buildings and housing.

Efforts to deleverage the "hidden time bomb" of 40 trillion in local

government debt have gained urgency after the government recently

pledged to cut taxes by two trillion yuan ($300 billion), further

draining local coffers and adding to the possibility of missed

repayments. Meanwhile, the lack of official estimates of the total local

government debt load - S&P's CNY40 trillion estimate is just that -

which usually carries higher rates than on-book ones, makes the issue

even trickier.

There is a more pressing reason behind the rush to deleverage: as

Nomura's China economist Lu Ting said, the motive is “just that the

problem can’t be delayed anymore,” as in many places fiscal revenues and gross domestic product aren’t enough to cover the interest and principals.

In other words, China may be just months ahead of its own Minsky Moment.

言い換えると、中国はあと数ヶ月で自らのミンスキーモーメントに達するかもしれない。

With official probes now taking place to quantify the local debt, so

far they’ve shown that hidden debt in some places exceeds the on-book

borrowing, a lawmaker of the National People’s Congress Zhu Mingchun

said over the weekend, according to Bloomberg.

Meanwhile, payments due for local-government financing vehicle debt are soaring and could reach 2.3 trillion yuan this year,

according to estimates by Industrial Securities Co, which notes that

local authorities will have to carry that burden at a time of slowing

revenue growth due to tax cuts and shrinking receipts from land sales.

One possible solution is massive restructuring of the debt: in one

case in December, the CDB led a group of commercial lenders in a swap of

260.7 billion yuan of implicit debt borrowed by Shanxi province to

build highways. The debt was restructured with a tenor of up to 25

years, allowing the local authorities to save 3 billion yuan in interest

payments every year, according to Shanxi Transportation Holdings Group.

As Bloomberg notes, asset sales are also being used. For example, a

district in the northeastern city of Shenyang is planning to sell more

than 38,000 square meters of offices and government-built housing to

repay maturing debt.

Of course, since in China everything is in

some state of being a bubble, officials are simply using “the healthier

part of the balance sheet of the public sector to address some of the

hidden issues,” but they have to make sure the risky loans won’t get out

of control again in the future, because by that time the balance sheet

would be less capable of absorbing them, according to Grace Ng, a China

JPMorgan economist.

China is also taking advantage of the current euphoria involving

local capital markets: a financing platform in the eastern province of

Jiangsu, where the CDB is involved in some cases of debt restructuring,

sold a 270-day bond last week with a coupon of 4.8 percent, 150 basis points lower than a similar note the company issued in January. On

Monday, a financing and investment company owned by a city in Shanxi

province was upgraded to AA+ from AA by China Chengxin International

Credit Rating Co., which cited the better outlook for capital quality.

地方金融市場の現在のeuphoria を中国政府は有利に利用している:江蘇省西部地域での金融機関、当地ではCDBが債務再編を行っている、ここで先週270日債権を4.8パーセントクーポンで売却した、1月に発行された同様の債権よりも150BPも低い。山西省のある市が持つ金融投資会社は月曜にAAからAA+に格上げとなった、China Chengxin International Credit Rationg Coによるものだ、今後の見立ても良好と格付けしている。

"The bigger worry is the moral hazard issue,” said Zhu Ning, a

professor of finance at Tsinghua University and the author of “China’s

Guaranteed Bubble.” “Implicit government guarantees still lie at the

core of so many problems."

And nowhere is the problem of moral hazard greater than in China,

whose financial sector is approaching double the size of its US peer

even as China's GDP is years behind catching up with America's. Which

makes Beijing's choice relatively easy: keep kicking the can, or watch

as the long-overdue Minsky Moment finally arrives and topples the

biggest house of financial cards ever constructed.

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...