As Goldman's Andrew Tilton (Chief Asia Economist) suggested:

ゴールドマンサックスのAndrew Tilton(アジアエコノミスト主任)はこう示唆する:

"There are reasons to be concerned [that easing is becoming less effective].

Local government officials who typically implement infrastructure

spending and other forms of stimulus are facing conflicting pressures.

The emphasis in recent years on reducing off-balance-sheet borrowing,

selecting only higher-value projects, and eliminating corruption has

made local officials more cautious. But at the same time, the

authorities are now encouraging local officials to do more to support

growth, like accelerate infrastructure projects. President Xi himself

recently acknowledged the incentive problems and administrative burdens

facing local officials."

And Nomura's Ting Lu has an explanation for why China stimulus i snot working... Chinese easing- / stimulus- escalation being a likely

requirement for any sort of “reflation” theme to work beyond a tactical

trade:

そしてノムラのTing Luはこう解説する、どうして中国の刺激策が機能しないかについて・・。中国の緩和/刺激策拡大にはある種の「リフレーション」が必要で戦略的な功罪が伴う:

yes, more RRR cuts are coming eventually (a better way for Chinese

banks to obtain liquidity vs borrowing from MLF or TMLF, bc it’s cheaper

and more stable)... ...but that the timing of such a cut is primarily dependent on the Chinese stock market, asthe

“re-bubbling” happening real-time in Chinese Equities (CSI 300 +26.8%

YTD; SHCOMP +24.4%; SZCOMP +34.0%) likely then constrains the room and

pace of Beijing’s policy easing / stimulus

This “Chinese Equities rally effectively holding further RRR cuts

hostage” then could become a serious “fly in the ointment” for near-term

/ tactical “reflation” (or bear-steepening) themes, as Q2 is on-pace to

see a significant liquidity shortage.

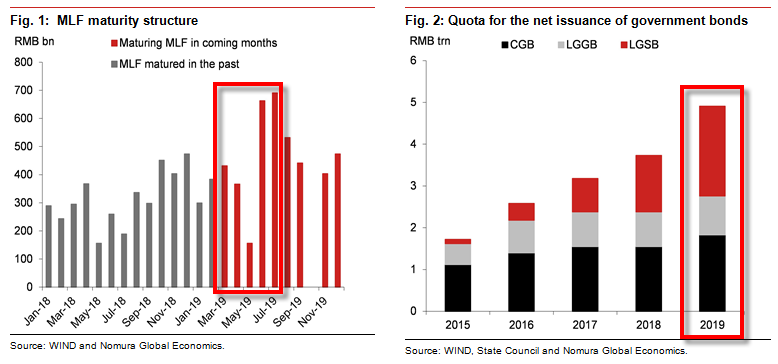

Ting estimates the liquidity gap could reach ~ RMB 1.7T in Q2 due to the following factors:

The size of the upcoming MLF maturities (est to be ~RMB 1.2T in Q2); 今後のMLF中期債権満期規模(Q2にRMB1.2Tと見積もられている);

The size and pace of (both central and local) government bond issuance (Nomura ests a target of ~ RMB 1T for Q2); 中央地方政府債券発行の規模とペース(ノムラはQ2にRMB1Tと見積もる);

Tax season effects; and 納税時期効果;そして

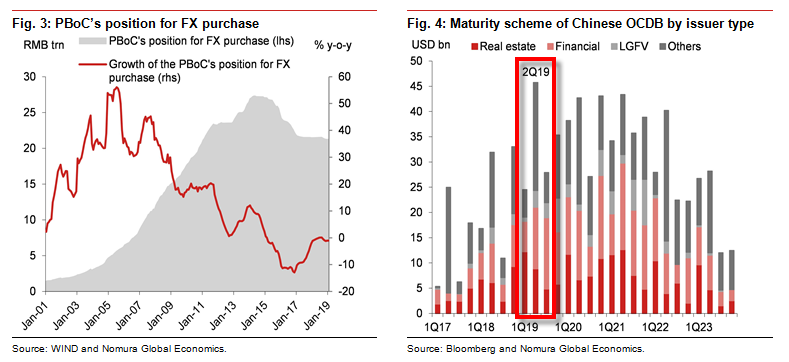

The shortage of money supply through the PBoC’s FX purchases 中国人民銀行の為替取引でのマネーサプライ不足

CHINA’S COMING Q2 LIQUIDITY-SHORTAGE:

So, simply put, China is merely refilling a rapidly leaking bucket of liquidity, as opposed to sloshing more into the bath of global risk - even if Chinese stocks were embracing it.

Amazonで買物をしてContrarianJを応援しよう Albert Edwards: This Was The Final Recessionary Shoe, And It Has Now Fallen by Tyler Durden Thu, 06/27/2019 - 12:45 Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007... ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・ ... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions. ・・・市場は準混乱状態になった、というのも歴史的に見てイールドカーブ反転が過去7回の景気後退の前兆となっているからだ。 However, while the inversion was certainly a memorable event, the question on everyone's lips is how do risk assets perform once the curve flattens and/or inverts. According to backtests from Goldman, since the mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. ...

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...