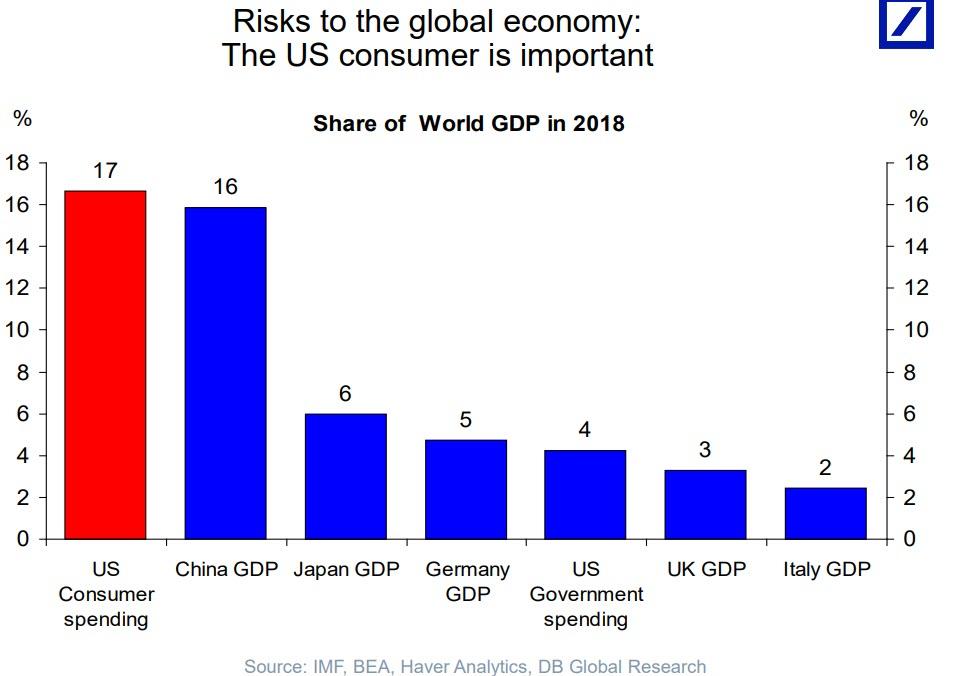

When

it comes to the growth dynamo behind the global economy, nobody can

match the US consumer - not even China: accounting for trillions in

annual spending, the US consumer, who represents roughly 70% of US GDP,

is also responsible for roughly 17% of global GDP, slightly ahead of the entire country of China.

世界経済の成長エンジンを議論する時、米国消費以上のものはないーー中国ではない:年間トリリオンドルを米国消費者は使っている、これが米国GDPの70%、そして世界GDPの17%を占める、中国全GDPよりも大きい。

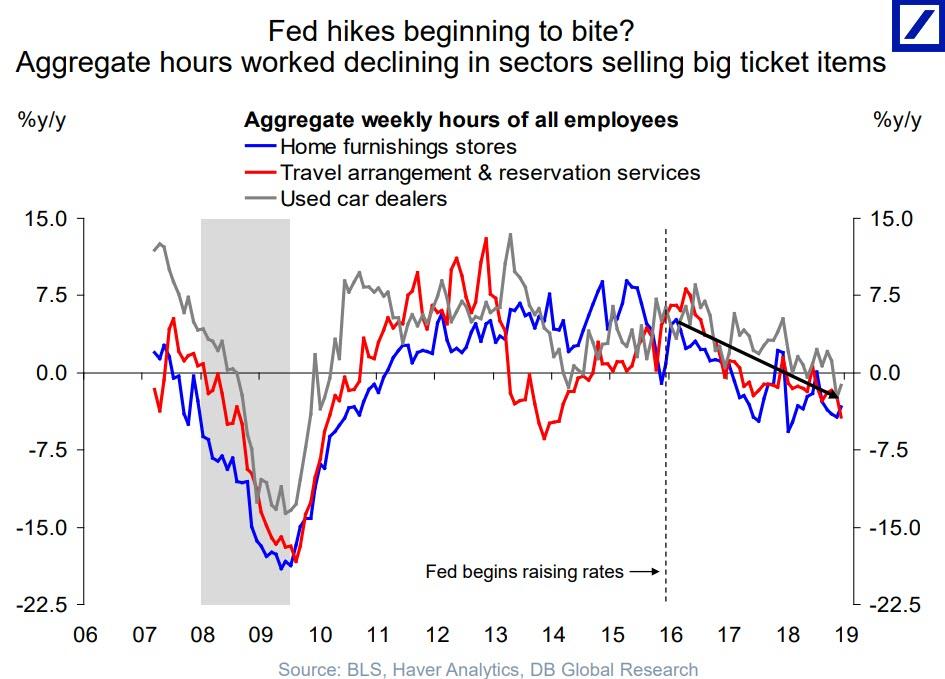

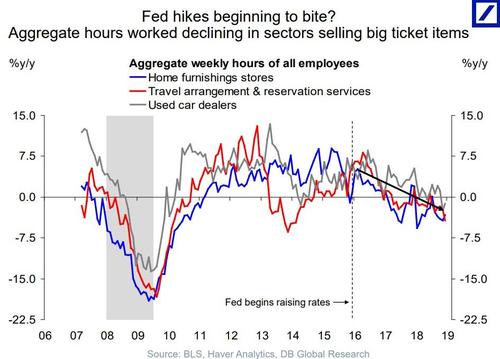

However, as recent economic data has shown, the future of the US

consumer is suddenly looking ominously cloudy, for two big reasons:

rising interest rates, which as Deutsche Bank notes are "beginning to

bite" as observed in the number of working hours in sector selling big

ticket items...

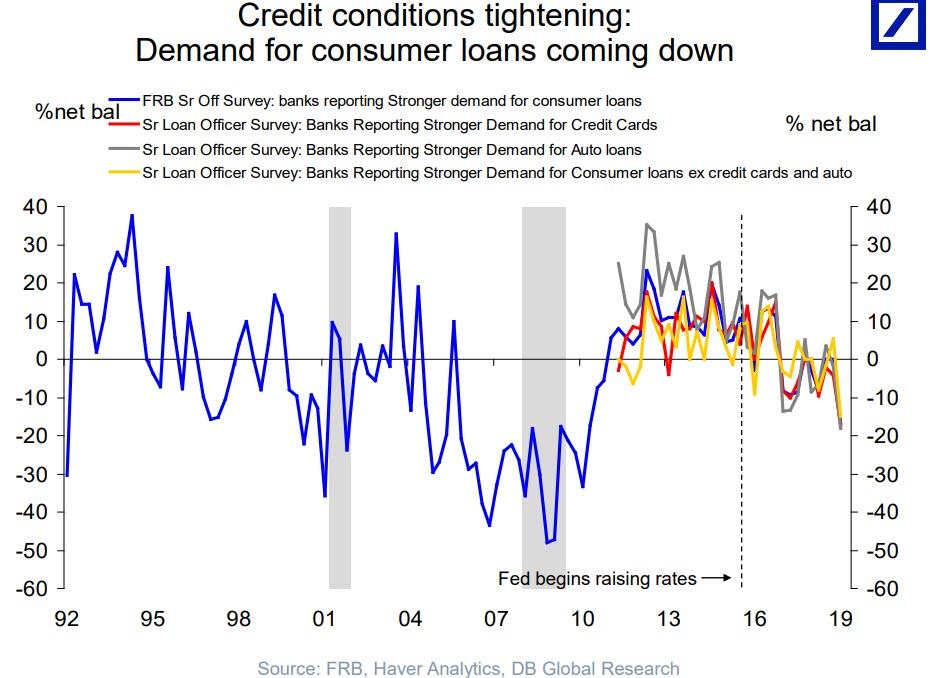

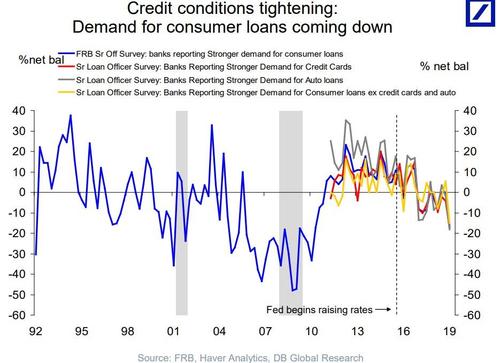

... and increasingly tighter loan terms, which coupled with softer

loan demand, means that the purchasing power of the US consumer is

suddenly facing a very troubling air pocket.

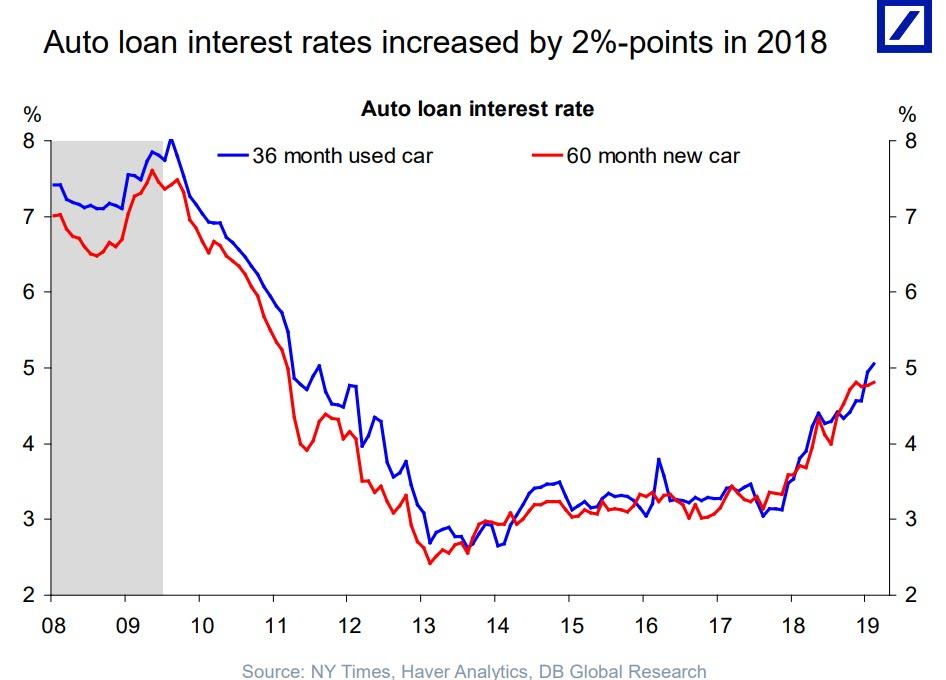

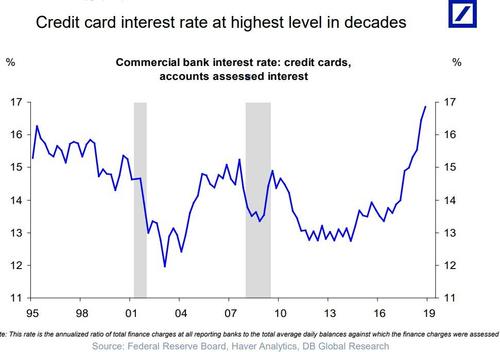

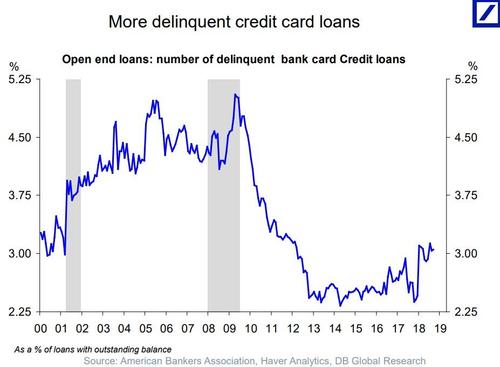

One driver behind the sudden drop in loan demand may also be the most

obvious one: interest rates on credit cards have soared to the highest

in over two decades...

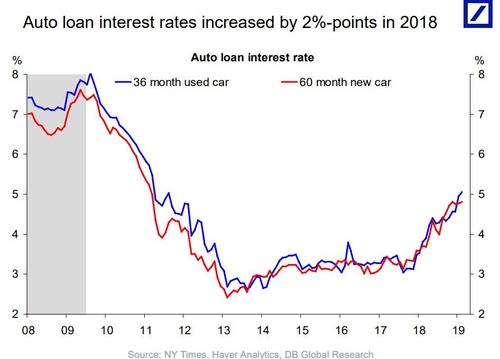

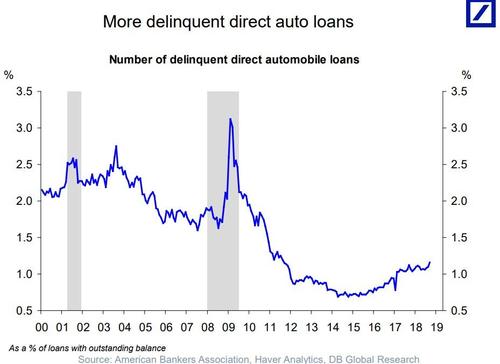

... while auto loan interest rates are now the highest since 2011,

and rapidly rising, making the average auto loan payment the highest on

record as discussed recently.

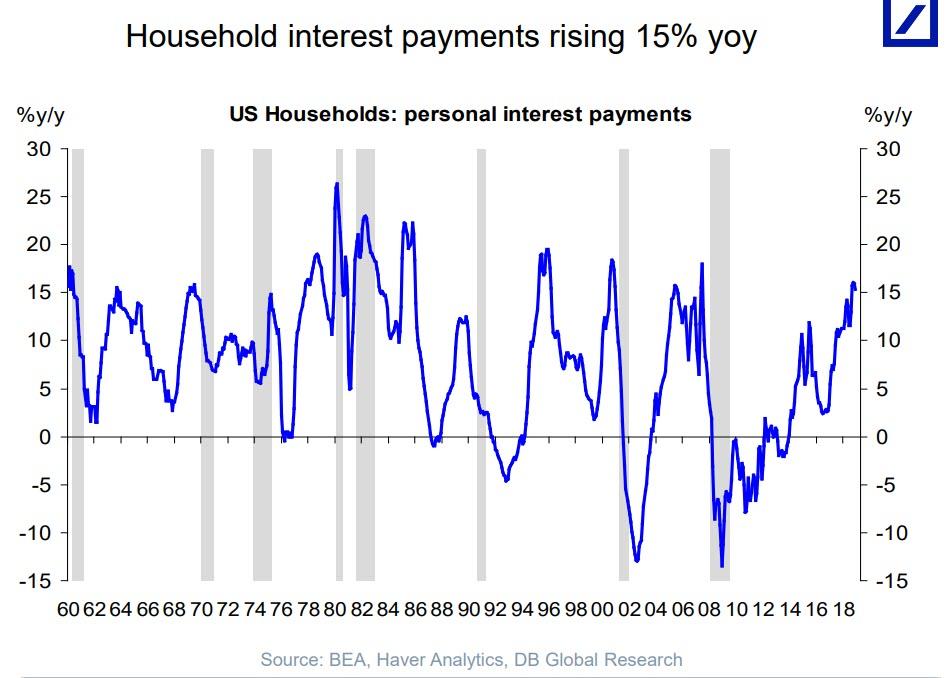

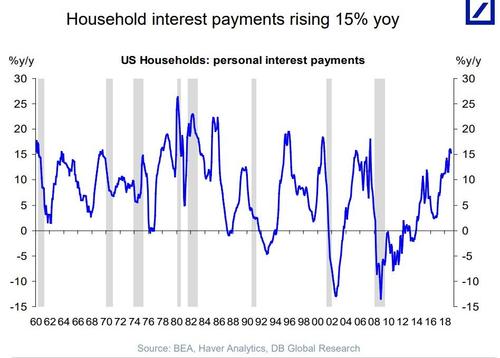

It's not just credit cards and auto loans: the aggregate household

interest payment has soared at a 15% Y/Y rate. Virtually every prior

time when interest payments spiked this much, a recession promptly

followed.

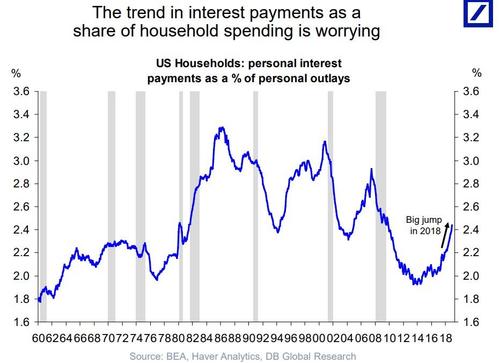

And while not quite at "redline levels" just yet, interest payments

as a share of total household spending has jumped to the highest level

since the financial crisis.

そしてまだ「赤線レベル」にはなっていないが、家計に占める利払い率は金融危機以来で最高レベルだ。

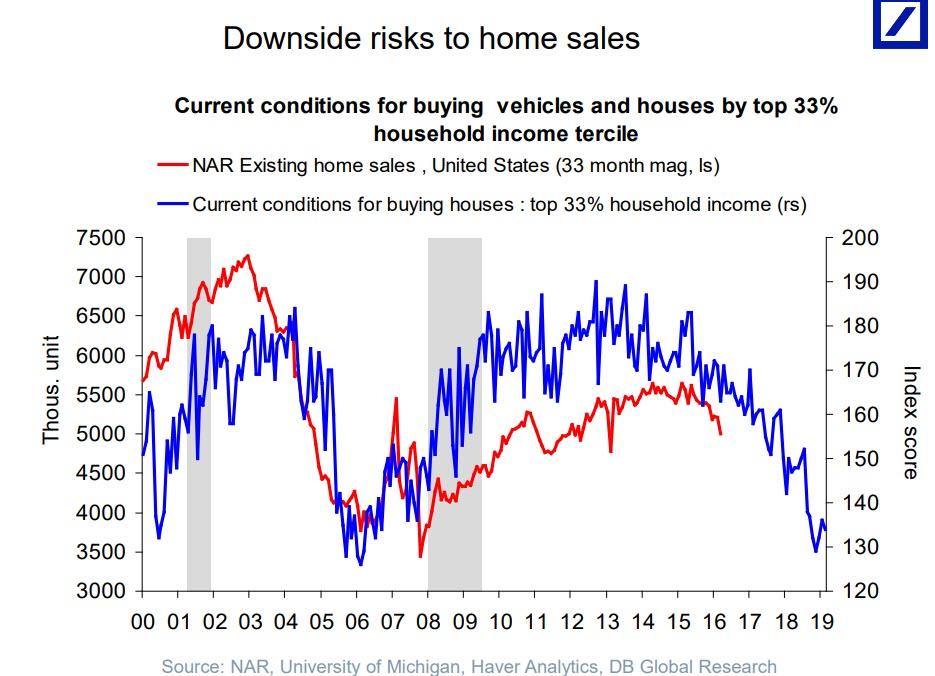

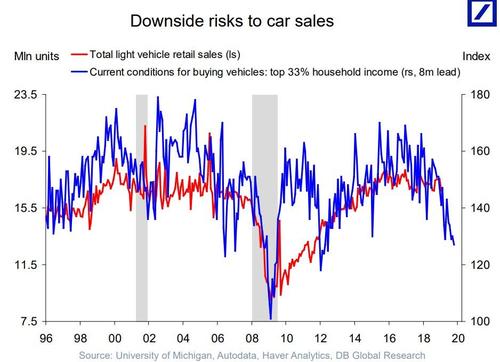

Meanwhile, as US purchasing power shrinks, so do intentions to purchase both cars...

それと同時に、米国の購買力は縮小している、自動車と・・・・

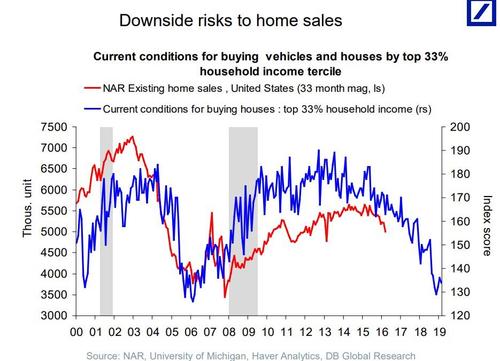

... and houses.

・・・・そして住宅だ。

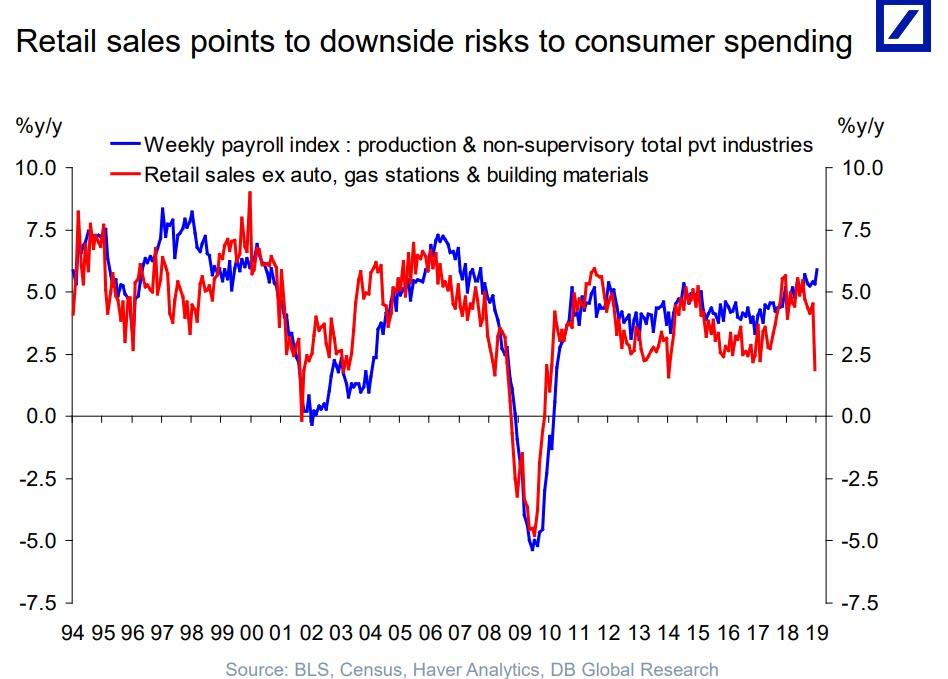

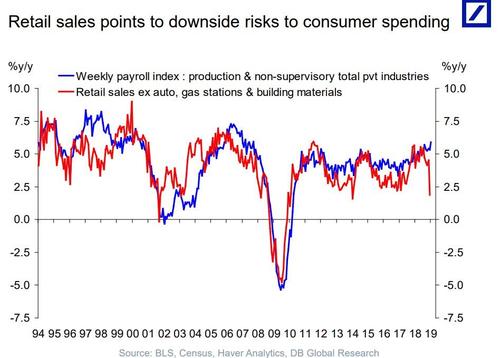

And while many legacy economists and pundits have said to ignore the

dismal December retail sales print, considering the collapse in spending

intentions for most other goods and services, it is only a matter of

time before consumer spending slides into recession (and the latest

retail sales print is confirmed as the accurate one).

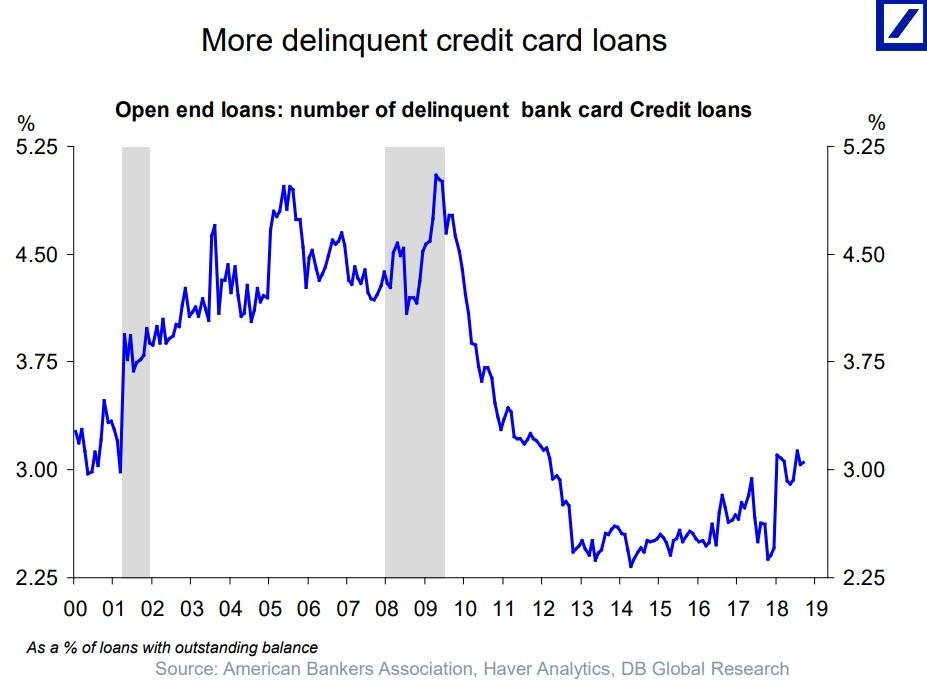

With rates rising, and with ever greater monthly payments, both credit card...

金利上昇に伴い、クレジットカードの毎月の支払いが大きくなり・・・・

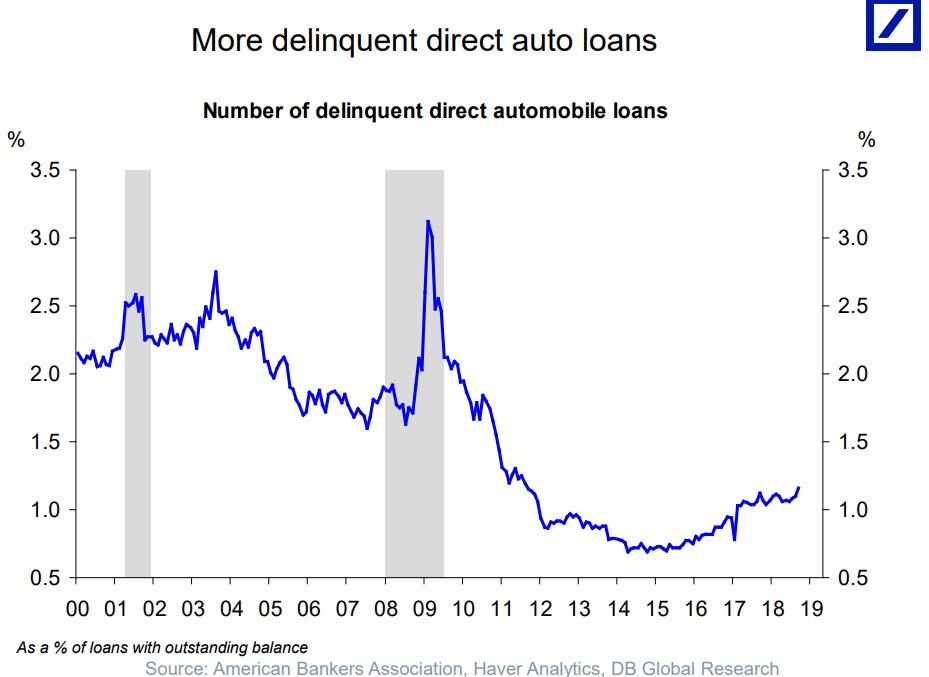

... and auto delinquencies are surging.

・・・自動車ローン返済遅延が上昇している。

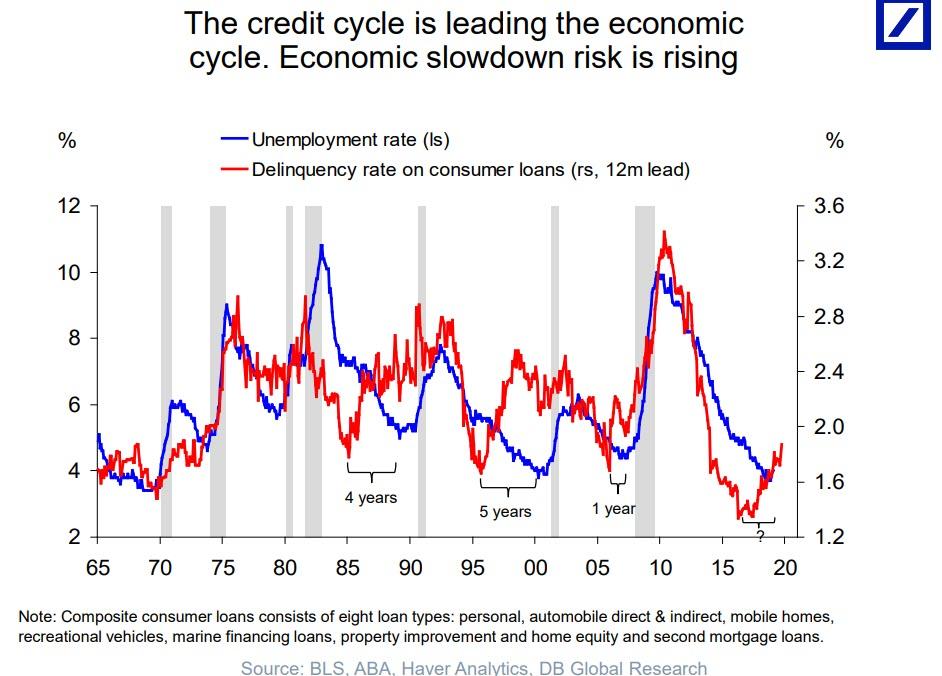

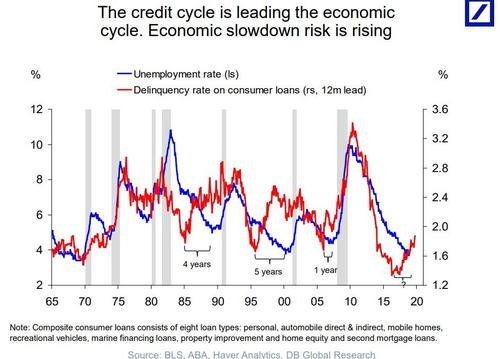

And so, with the credit cycle having peaked and absent rate cuts (and

QE) by the Fed, only set to make life for US consumers even more

difficult, it is just a matter of time before the economic slowdown

follows.

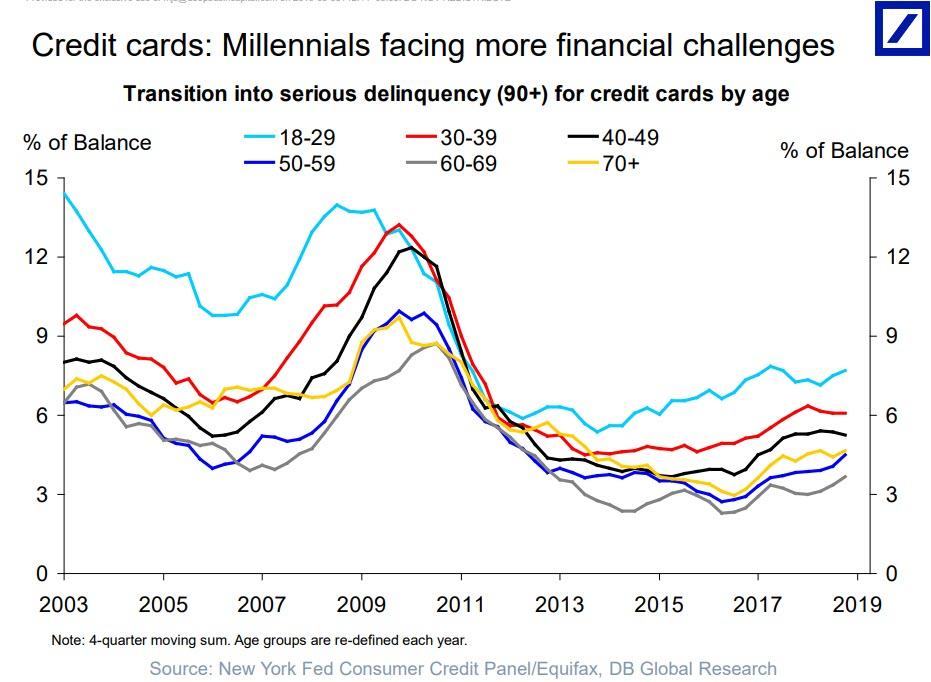

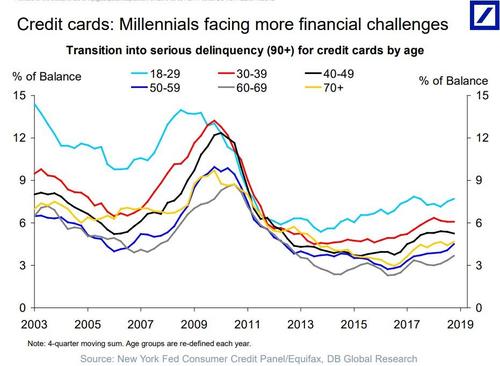

As usually happens, one generation is especially exposed to the

upcoming period of economic weakness: the millennials, whose delinquency

rate is already the highest among all age cohorts.

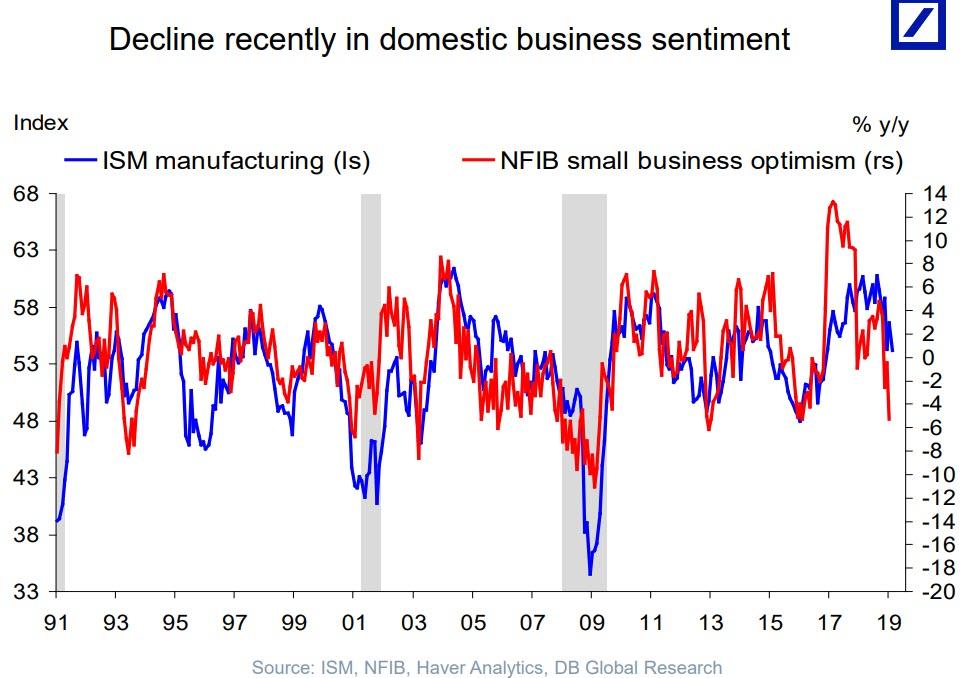

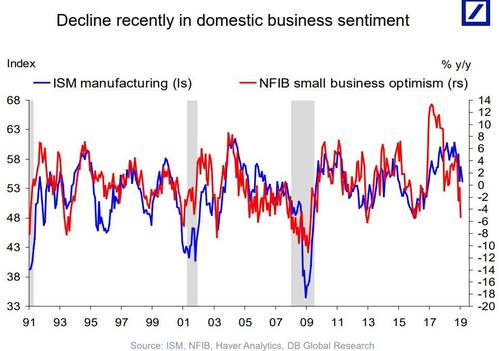

Finally, while all of the above have yet to hit the US economy where

GDP recently printed at a solid 2.6% in Q4, in Q1 GDP is expected to

plunge below 1% (Atlanta Fed has it at a paltry 0.3%); once that

happens, US small business confidence which is already plunging at the

fastest rate since the financial crisis after having soared higher after

the Trump election, will crater sending the US economy into a steep

recession if not worse.

Amazonで買物をしてContrarianJを応援しよう Albert Edwards: This Was The Final Recessionary Shoe, And It Has Now Fallen by Tyler Durden Thu, 06/27/2019 - 12:45 Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007... ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・ ... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions. ・・・市場は準混乱状態になった、というのも歴史的に見てイールドカーブ反転が過去7回の景気後退の前兆となっているからだ。 However, while the inversion was certainly a memorable event, the question on everyone's lips is how do risk assets perform once the curve flattens and/or inverts. According to backtests from Goldman, since the mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. ...

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...

今の地球地球温暖化モデルはどれも地球が受ける太陽エネルギーが一定と仮定しています。たとえスーパーコンピュータを利用しようともモデルを超えた計算はできません。しかし太陽の輻射エネルギーは時間とともに変動していますし、太陽と地球の距離は他の惑星の影響で変動、摂動しているのです。過去の温暖化寒冷化はこの摂動でとてもよく説明できます。月の明かりの変化を引き起こすスーパームーン現象も他の惑星の摂動効果による地球・月間距離変動によるものです。こちらはテレビでも解説するのに太陽・地球間距離の摂動変化は決してテレビで解説されることがありません。 いまテレビを賑わしているあの女の子もちゃんと学校に言って科学を勉強すれば自らの愚かさを理解するでしょうに。 Martin Armstrong: The First Clean Air Act Was In 535AD by Tyler Durden Sat, 09/28/2019 - 12:30 Authored by Martin Armstrong via ArmstrongEconomics.com, To me, all this propaganda that humans are responsible for climate change implies that somehow the climate is static and would not be changing but for human activity. This may make great headlines and inspire youth to create strikes and march upon the institutions of capitalism demanding their closure. However, any unbiased review of history reveals a shocking fact – the climate has...