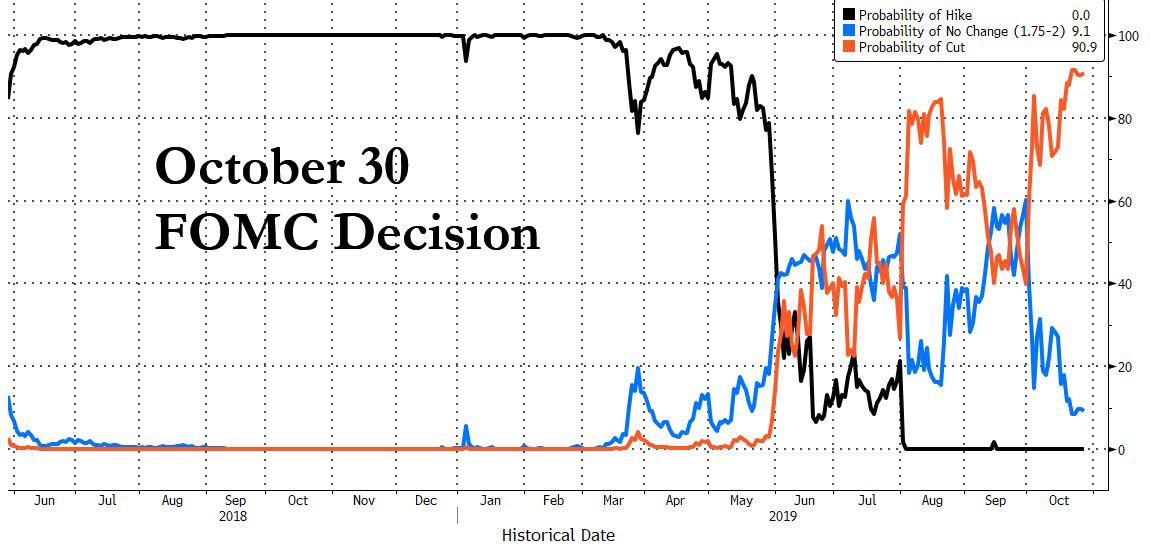

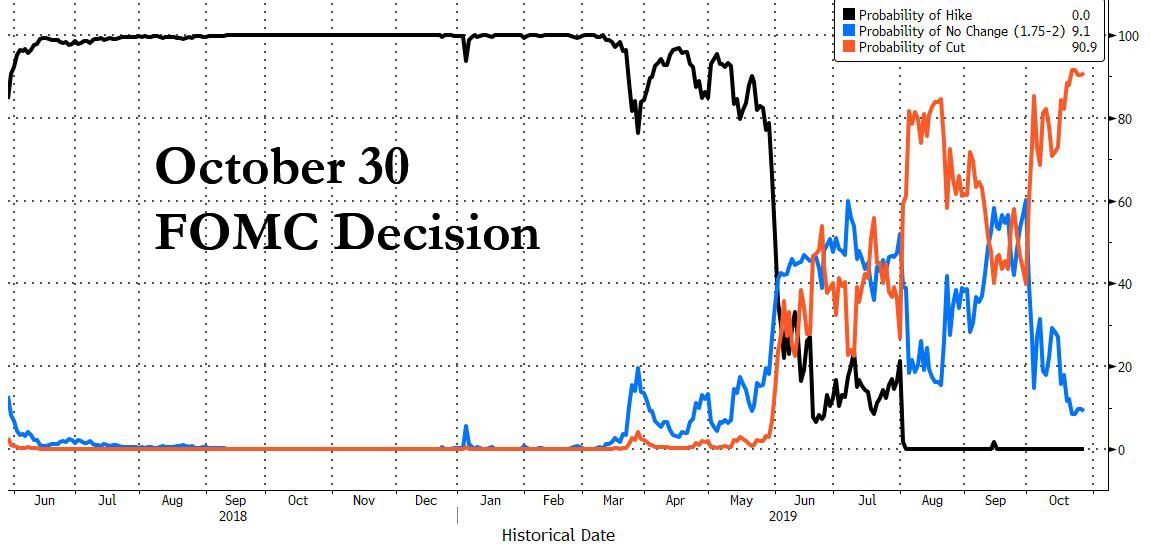

When

it comes to the Fed's next rate decision, the market has made up its

mind: as of this morning, the fed funds futures market is pricing in a

probability of 91% that the Fed announces another 25bps rate cut at 2pm

on Wednesday, with odds of no cut at just 9%.

So certain are strategists that the Fed will deliver another

"insurance" cut - the third in a row - that discussion has now firmly

shifted to what the Fed will do in its next, December, meeting with the FT writing that

the "Federal Reserve faces the thorny decision of whether to signal an

interruption to its monetary easing after it delivers what is widely

expected to be a third consecutive cut to its main interest rate this

week."

If the Federal Open Market Committee presses ahead with a new rate

reduction on Wednesday afternoon, it will have already notched up 75

basis points of monetary stimulus this year — and to some economists and

Fed officials that should be sufficient to accomplish the goal.

Needless to say, the prevailing consensus is that Powell will cut,

with Scott Anderson, chief economist at Bank of the West, summarizing it

best: "I think they will end up cutting another 25 basis points [this

week] and then pause for the rest of this year."

言うまでもなく、すでに市場合意はPowell が金利引下げを行うだろうというものだ、Bank of the WestのチーフエコノミストScott Andersonが状況をこうまとめる:「私の見解では、今週の25BP切り下げでお終いにするだろう、そして年内は金利引下げは休止となるだろう。」

Yet not everyone agrees.

ただし、だれもがこれに同意するわけではない。

According to Jefferies money-market economist Thomas Simons, the

headwinds that pushed the central bank to cut rates in July and

September have "abated somewhat" as U.S.-China trade tensions and

Brexit uncertainty have also diminished, while the gap between the Fed’s

policy stance and that of other central banks has narrowed.

Thomas SimonsのマネーマーケットエコノミストJefferiesによると、7月や9月のような中央銀行金利引下げを要求する向かい風は「幾分和らいでいる」というのも、米中貿易係争やBrexit不確実性は弱まっており、一方でFED政策スタンスと他の中央銀行のスタンスが狭まっているのだ。

As a result, Simon takes on the wildly contrarian view that the Fed

will keep rates unchanged this week while leaving a December cut on the

table; in doing so, the Fed would spark a "temper tantrum" in markets, while pushing back against aggressive Fed pricing and cement the idea of a mid-cycle policy adjustment.

"If they continue with so many consecutive rate cuts, they

can never break the cycle of market expectations thinking more are

coming,” Simons said in a Bloomberg interview, adding that "it’s

time for the Fed to take a step back and see if the prior cuts are

going to have an effect before moving forward with another one." 「もしFEDがこれだけ何度も連続で金利引下げを行うと、今後は市場の要求が更に高まりそれに抗することができなくなってしまう、」とSimonsはブルームバーグのインタビューで答えた、更にこう加える「今やFEDは一旦立ち止まるべきときであり、さらなる金利引下げを行う前にこれまでの一連の金利引下げの効果を確認すべきだ。」

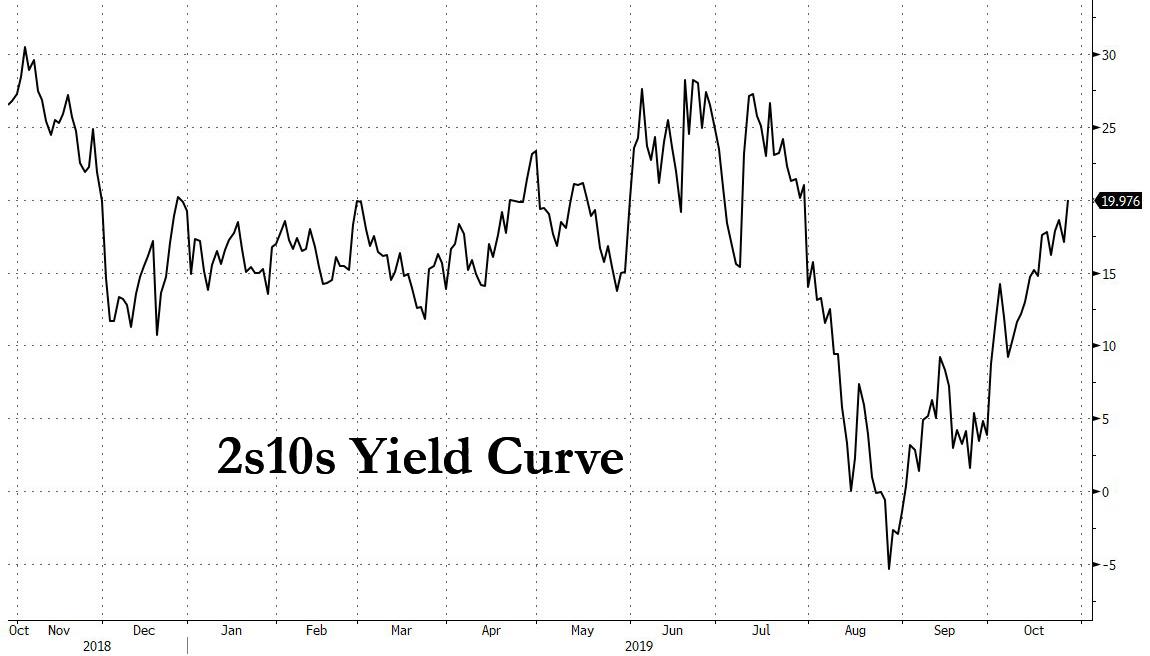

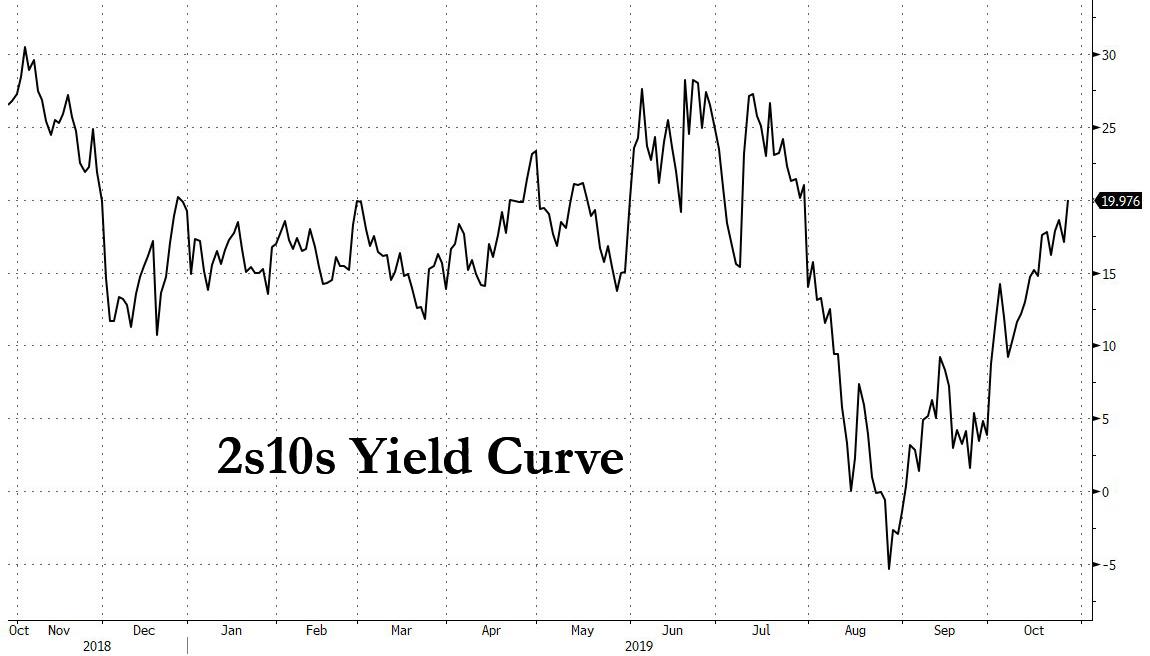

Holding fire on more rate cuts will likely have the added benefit of

further steepening the yield curve, a critical condition for US banks to

return to profit growth: with yields on the short-end depressed thanks

to the Fed's "Not QE", which will soon spill over from purchasing merely

Bills into the 2Y (if not longer maturity) sector, longer-dated yields

will likely jump should the Fed surprise markets by not cutting rates in

48 hours. This would serve to further steepen the 2s10s yield curve,

which after inverting briefly in August is back to level last seen at

the start of the year (here we ignore the discussion that it is the

re-steepening of the yield curve following an inversion that is the true

recession signal, as it is a topic we have covered extensively in the

past).

Helping the steeper yield curve is the recent rise in 10-year

Treasury yields which printed a six-week high of 1.86% on Monday as

President Trump touted trade progress and the EU granted the U.K. a

three-month Brexit delay. Meanwhile, rates on 2-year Treasuries climbed a

more modest 3 bps.

To be sure, it is unclear if Powell would be willing to risk a market

tantrum just to prove that he is not at the mercy of the market. As

Jefferies points out, a knee-jerk response to the Fed standing pat would

likely see U.S. stocks sink and the yield curve “twist." Or, as

Bloomberg explains, "while the Fed’s bill purchases and lower inflation

expectations should continue to suppress short- and long-dated yields,

3- to 7-year Treasuries may sell off, he said."

"There will be a little bit of a temper tantrum, but I think the volatility will be short-lived,” Simons said. “Stocks won’t like it, but it isn’t exactly going to set off a prolonged sell-off." 「こうなると癇癪発作の可能性は低く、ボラティリティは短期的なものになると私は思う、」とSimonsは言う。「株式市場はこうはならないだろう、しかし先延ばしされた下落がすぐに始まるというわけでもない。」

There is another reason why Simons' view is in the minority: as the

FT noted over the weekend, the drumbeat of relatively soft economic

data, and fears of a negative market reaction, could make Mr Powell and

other Fed policymakers wary of indicating that this round of “insurance”

cuts is already over. Furthermore, the latest truce in the US-China

trade war is only tentative, and even if it is signed by Trump and Xi

Jinping, in Chile next month, many of the tariffs and the tensions in

transpacific trade are set to linger.

"The Fed runs the risk of an unnecessary tightening of financial

conditions. We are hopeful that Chair Powell avoids such a mistake,"

said Natixis economist Joe Lavorgna.

As such, whereas most dismiss Jefferies' suggestion, all will be

focused on whether the FOMC statement changes it pledge to "act as

appropriate to sustain the expansion" widely seen as an indicator of

future rate cuts, to wording that appears less committed to further

easing.

“Keeping the forward guidance as is is the path of least resistance.

If they take it out they are being unintentionally hawkish,” said

Michelle Meyer, an economist at Bank of America Merrill Lynch. “The data

now is softening so I think they have to give some nod in that

direction.”

Boosting the dovish case, it is likely that just hours before the

Fed's announcement, the US will announce that Q3 GDP rose just 1.6%,

which would be the slowest pace so far this year; In fact, since the

Trump election, there has been just one quarter of GDP growth below 2%,

and analysts will be looking out for what this might mean for the

economy heading into next year’s election. And then there is the October

US jobs report on Friday, where consensus expects a paltry +90k print

following the previous month’s +136k increase. If accurate, that

would be the weakest pace of monthly jobs growth since May but the

recent GM strike complicates the analysis with a 46k hit expected from

this. Explanations aside, however, Trump will be sure to put

the squeeze on the Fed to cut rates even more after such a poor number,

and for Powell the question will be whether he wishes to do so after he

has just cut again for the third time, or after giving himself some

breathing space by not cutting rates this week, even if it means a

modest "tantrum."

While it is unknown what Powell will decide on Wednesday, the best

summary of the choices facing the Fed chair comes from the former head

of the NY Fed's market team, Brian Sack, who is currently director of

global economics at DE Shaw, and who two weeks ago told an Institute of International Finance conference that "we either stabilize with one more cut, or I think we’re going to go all the way to the lower bound." 水曜にPowllがどういう結論を出すかはわからないが、FED議長の直面する状況に関して、前NYFED市場チーム主任のBrian Sackは考えを述べている、彼は現在DE Shawの世界経済取締役だ、その彼が二週前にInstiture of International Finace 会議でこう述べた「我々は皆もう一度の金利引下げによる安定化を求めている、もしくは私自身はさらなる金利引下げをだ。」

The problem for the Fed is that even if it cuts on Wednesday, the probability of a quick "stabilization" is virtually nil,

for one simple reason: China refuses to join the global reflation

party, which has resulted in its credit impulse barely rebounding from

cycle lows.

FEDにとっての問題はたとえ水曜に金利引下げをしたとしても、直ちに「安定化」する可能性は殆どないということだ、シンプルな理由の一つが:中国は世界的なリフレ騒ぎに参加を拒んでいる、その結果中国のクレジットインパルスは今サイクル底からほとんどリバウンドしていない。

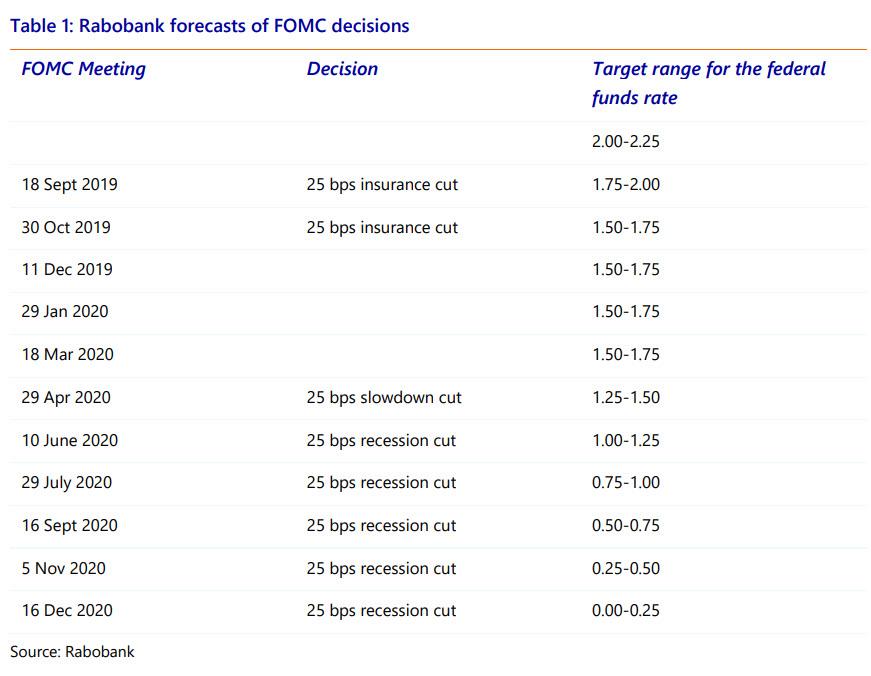

As long as Beijing refuses to lend a helping hand to the global

reflation effort, it will be up to the Fed. And should Powell use up his

last "insurance" cut for nothing - because after three cuts as Sack

said, the Fed will likely have no choice but to cut all the way to zero,

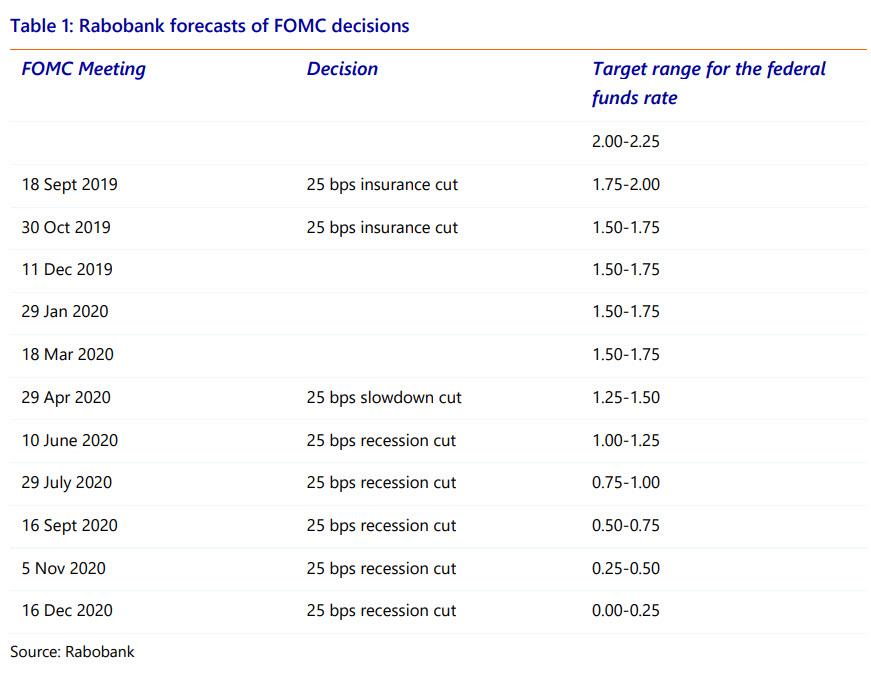

something which Rabobank predicted some time ago, the Fed chair will have no choice but to capitulate.

And, as an added consideration, this will be Trump's preferred

outcome, because what better way to ensure that the S&P is at all

time highs and the US economy avoids recession ahead of the Nov 2020

election, than the Fed cutting rates to 0% by December 2020.

Well, with "Not QE" already active, and the Fed out of ammo when it

comes to more rate cuts, what happens in 2021 will depend on one simple

choice: will the Fed follow Europe and Japan into negative rates, or

will the long delayed recession finally arrive.

Amazonで買物をしてContrarianJを応援しよう Supply and Demand in Comex Digital Gold by Sprott Money Thu, 07/04/2019 - 09:32 Supply and Demand in Comex Digital Gold Written by Craig Hemke, Sprott Money News A few years ago, we wrote the salient article on the subject of derivative supply and demand on Comex. Given the recent price breakout and sentiment change, it's likely a good idea to re-visit this topic today. 数年前のことだが、私どもはCOMXの派生商品の需給に関する注目記事を書いた。最近の価格ブレークアウトと心理変化もあり、この話題を再度今取り上げるのが良かろう。 The post from 2017 dealt with Comex silver and the original link is below. However, since it is extremely important that you understand this dynamic, I'm going to ask the folks at Sprott Money to reprint the post in its entirely at the bottom of this page. Please take the time to read and study this full article: 2017年の記事はCOMEXシルバーに関するもので、その時のリ...

「この記事が面白いと思うなら、 Amaz onで買物をしてContrarianJを応援しよう 」 September Class 8 Heavy Duty Truck Orders Collapse 71% by Tyler Durden Fri, 10/04/2019 - 13:10 Preliminary Class 8 order data for September is starting to trickle in and, like the data preceding it so far this year - it's ugly. クラス8トラック発注がことしのこれまでと同様にひどい。 Class 8 orders were crushed 71% in September, reaching 12,600 units, according to Baird and Morgan Stanley. 9月にクラス8トラック発注が71%下落し、12,600台となった、Baird and Morgan Stanleyのデータだ。 This follows a 79% plunge in August. 8月の79%下落に次ぐ悪さだ。 This makes September the 11th consecutive month of YOY order declines and the 9th consecutive month of orders below 20,000. この9月で11か月連続でYoY発注が下落している、また9か月連続で20,000台を下回った。 Class 8 orde...

Gold - Preparing For The Next Move by Tyler Durden Fri, 03/22/2019 - 05:00 Authored by Alasdair Macleod via GoldMoney.com, Note: this article is not and must not be construed as investment advice. It is analysis based purely on economic theory and empirical evidence. この記事は単なる分析であり、投資を推奨するものではない。 The global economic outlook is deteriorating. Government borrowing in the deficit countries will therefore escalate. US Treasury TIC data confirms foreigners have already begun to liquidate dollar assets, adding to the US Government’s future funding difficulties. The next wave of monetary inflation, required to fund budget deficits and keep banks solvent, will not prevent financial assets suffering a severe bear market, because the scale of monetary dilution will be so large that the purchasing power of the dollar and other currencies will ...

最後の2段落だけ訳をいれました。 Big Silver-Stock Potential Adam Hamilton February 7, 2020 2689 Words The silver miners’ stocks are looking interesting. While they really lagged silver’s surge on gold’s bull-market-breakout rally last summer, their upleg since remains intact. Gold stocks’ own upleg peaked in early September. And silver itself remains wildly undervalued relative to gold, overdue to mean revert dramatically higher. When that happens during gold’s next upleg, the silver stocks have big potential to soar. Like the global silver market is vastly smaller than gold’s, silver stocks are a proportionally-little fraction of the precious-metals miners. As a small subset of a usually-ignored contrarian sector, the silver stocks often languish in obscurity. For decades there wasn’t even a silver-stock index, making sector analysis difficult. ...