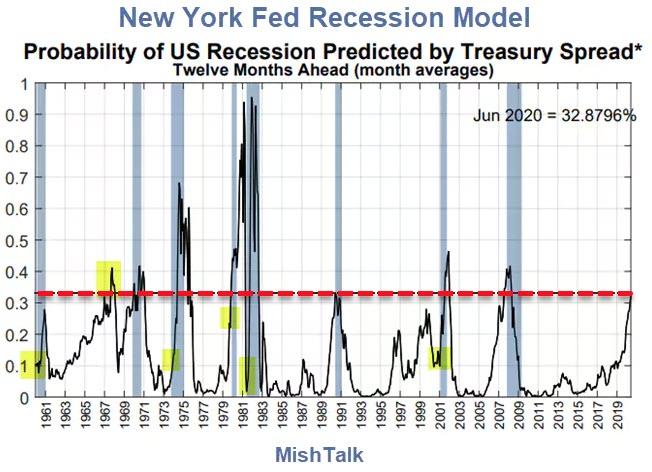

I added the highlights in yellow and the dashed red line.

私はもとのチャートに黄色と赤点線で強調した。

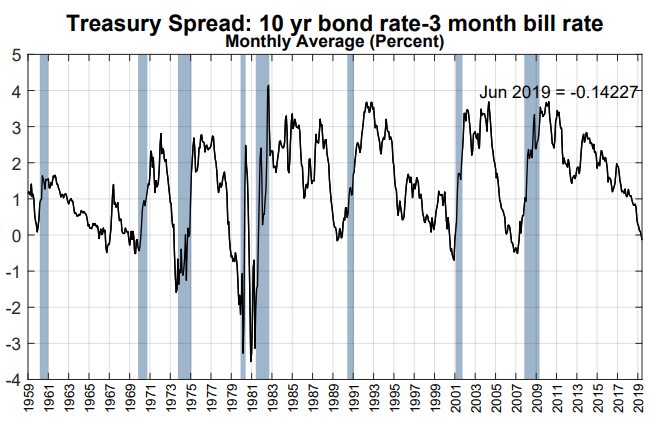

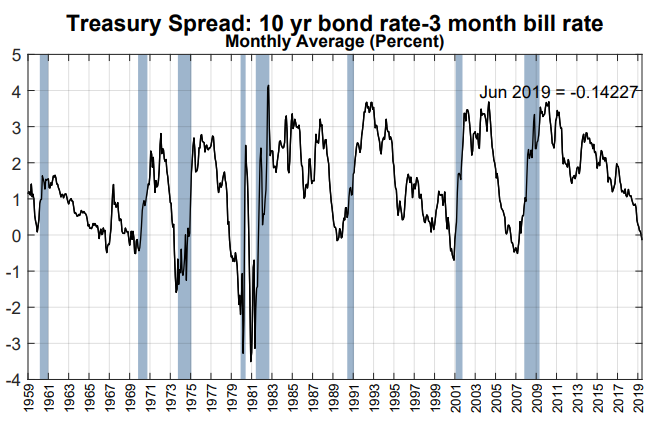

The New York Fed Recession Model is based on yield curve inversions between the 10-year Treasury Note and the 3-Month Treasury Bill.

the New York FED 景気後退モデルは米国債10Y3Mの金利スプレッド反転に基づいている。

The model uses monthly averages.

このモデルは毎月の平均値を採用している。

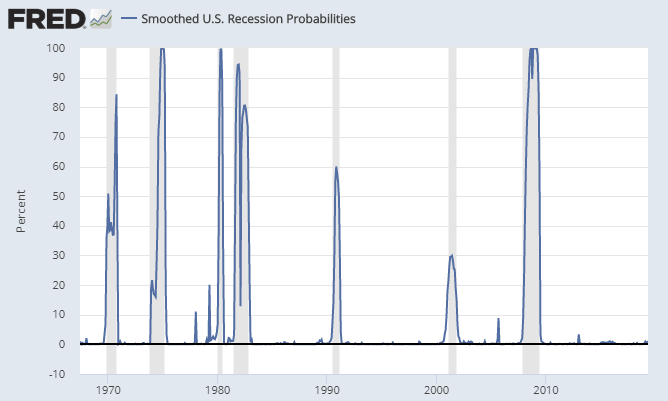

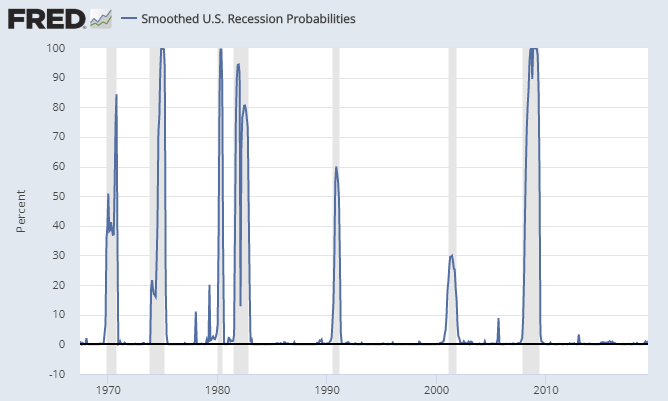

Smoothed Recession Odds

平滑化された景気後退可能性

I do not know the makeup of the smoothed recession chart but it is

clearly useless. The implied odds hover around zero, and are frequently

under 20% even in the middle of recession.

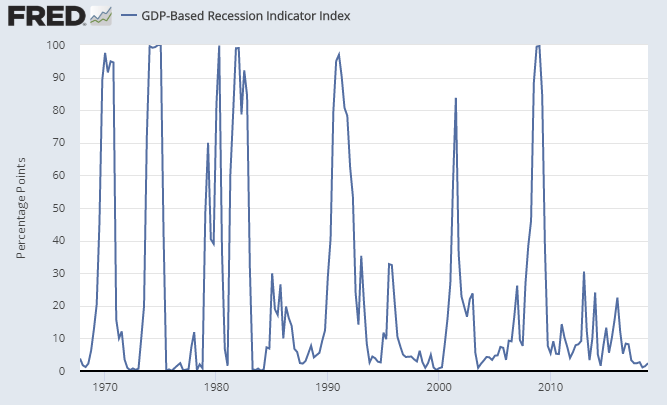

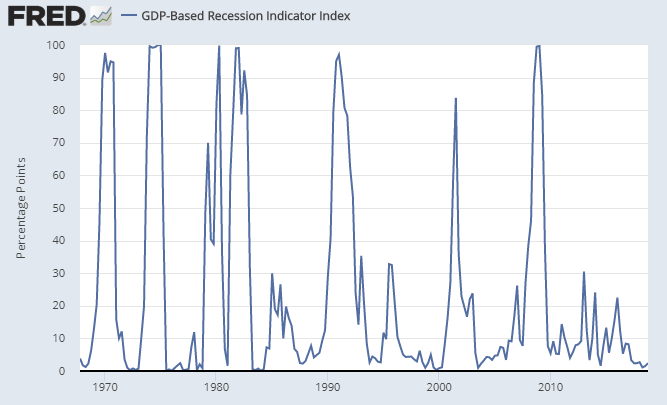

The GDP-based recession model is hugely lagging. The current estimate

is 2.4%. This model will not spike until there is at least one quarter

of negative or near-zero GDP.

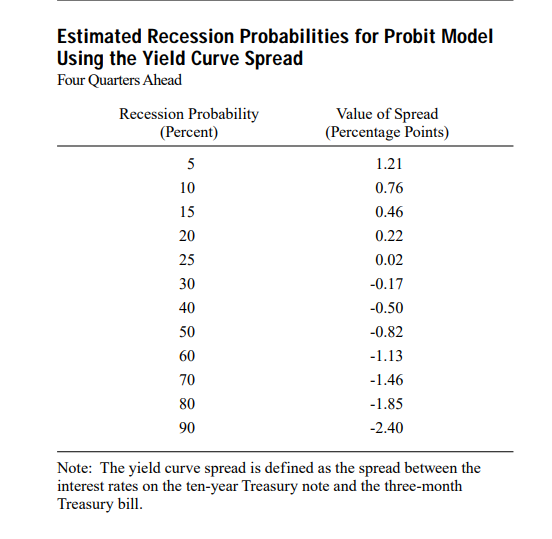

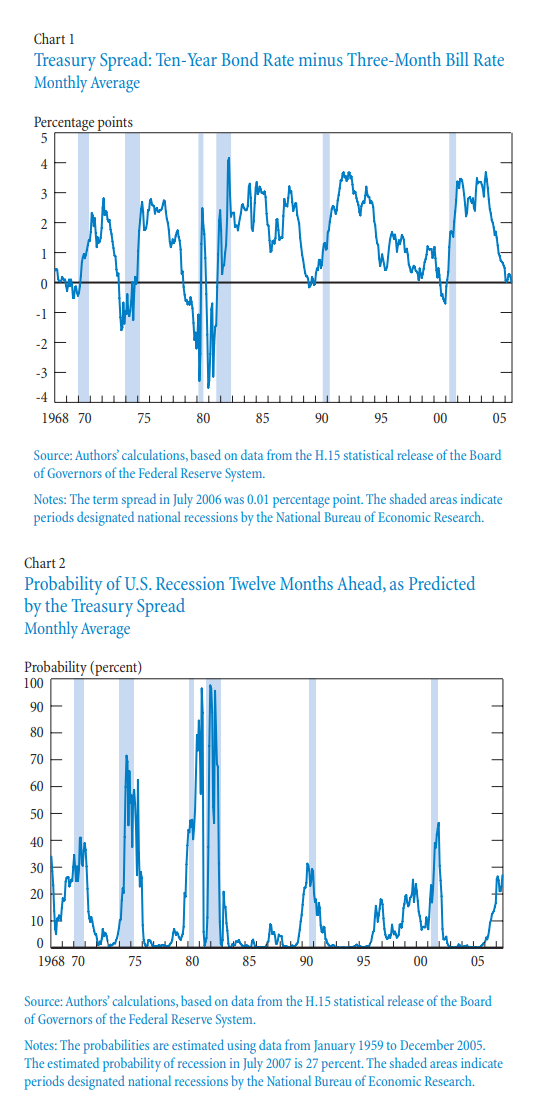

With regard to the short-term rate, earlier research suggests that

the three-month Treasury rate, when used in conjunction with the

ten-year Treasury rate, provides a reasonable combination of accuracy

and robustness in predicting U.S. recessions over long periods.

Maximum accuracy and predictive power are obtained with the secondary

market three-month rate expressed on a bond-equivalent basis, rather

than the constant maturity rate, which is interpolated from the daily

yield curve for Treasury securities.

Spreads based on any of the rates mentioned are highly correlated

with one another and may be used to predict recessions. Note, however,

that the spreads may turn negative—that is, the yield curve may

invert—at different points and with different frequencies.

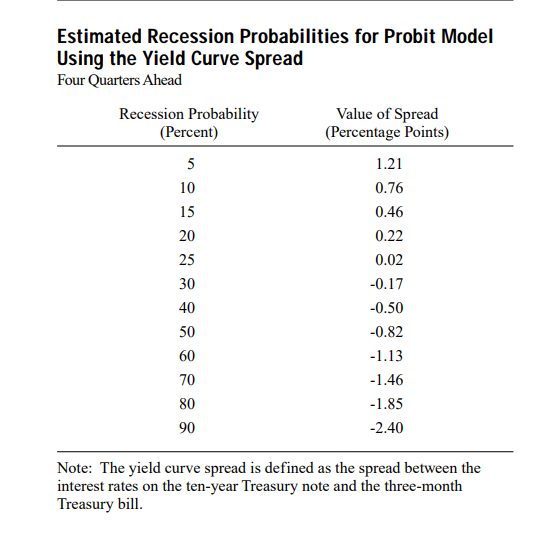

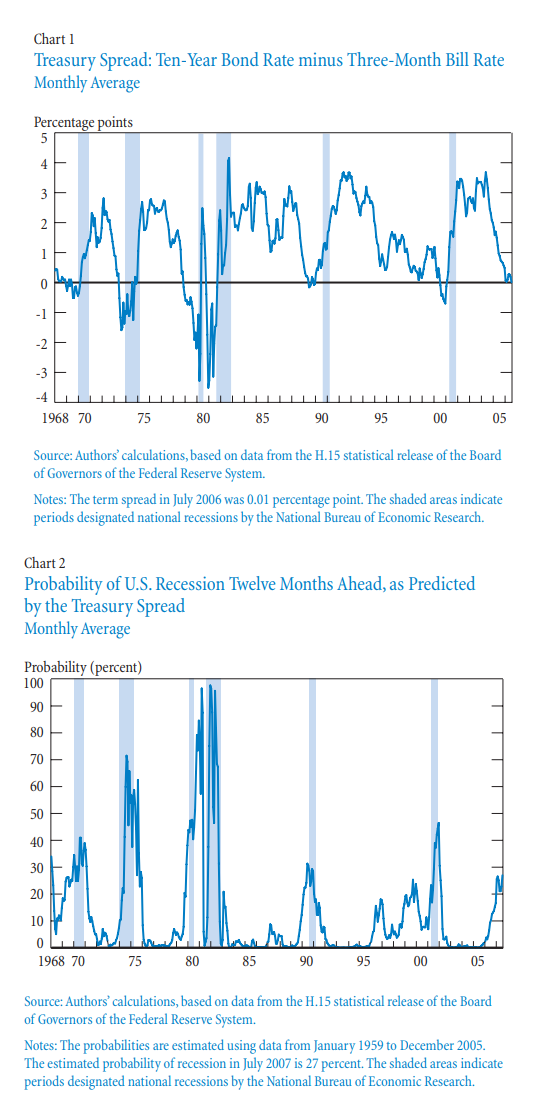

Our preferred combination of Treasury rates proves very successful in

predicting the recessions of recent decades. The monthly average spread

between the ten-year constant maturity rate and the three-month

secondary market rate on a bond equivalent basis has turned negative

before each recession in the period from January 1968 to July 2006

(Chart1). If we convert this spread into a probability of recession

twelve months ahead using the probit model described earlier (estimated

with Treasury data from January 1959 to December 2005), we can match the

probabilities with the recessions (Chart 2). The chart shows that the

estimated probability of recession exceeded 30 percent in the case of

each recession and ranged as high as 98 percent in the 1981-82

recession.

The article mentions "The ten-year minus two-year spread tends to

turn negative earlier and more frequently than the ten-year minus

three-month spread, which is usually larger."

こういう記事もある「10Y2Yのほうが10Y3Mよりももっと早期に反転し頻度も多い」。

That is certainly not the case today.

現在の状況はこれには当てはまらない。

The 2-year yield is 1.882 whereas the 10-year yield is 2.041.

2年ものの金利は1.882であり10年ものの金利は2.041だ。

Chalk this up to QE, Fed manipulation, taper tantrums, and hedge funds front-running expected rate cut moves. この手法で、QEもFED市場操作、テーパータンタラム、そしてヘッジファンドの金利カット先行予想もすべてうまく取り込めている。

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...