While

the western world (and much of the eastern) has been preoccupied with

predicting the consequences of Trump's accelerating global trade/tech

war and whether the Fed will launch QE before or after it sends rates

back to zero, Beijing has quietly had its hands full with avoiding a

bank run in the aftermath of Baoshang Bank's failure and keeping the

interbank market - which has been on the verge of freezing - alive.

Unfortunately for the PBOC, Beijing was racing against time to

prevent a widespread panic after it opened the Pandora's box when it

seized Baoshang Bank, the first official bank failure in an odd replay

of what happened with Bear Stearns back in 2008, when JPMorgan was

gifted the historic bank for pennies on the dollar.

As a reminder, back in May, shortly after the shocking failure of

China's Baoshang Bank (BSB), and its subsequent seizure by the

government - the first takeover of a commercial bank since the Hainan

Development Bank 20 years ago - the PBOC panicked and injected a

whopping 250 billion yuan via an open-market operation, the largest

since January. Alas, as we said at the time, it was too little to late,

and with the interbank market roiling, with Negotiable Certificates of

Deposit (NCD) and repo rates soaring (in some occult cases as high as 1000%) we said that it's just a matter of time before another major Chinese bank collapses.

5月末のことを思い起こすと、中国のBaoshang Bank (BSB)破綻とその後の国有化後ーーこれは20年前の海南開発銀行以来初めての商業銀行国有化だったーーPBOCはパニクってなんと250B人民元を公開市場操作で金融システムに注入した、今年最大の量だった。なんということか、当時ZeroHedgeが書いたが、これは too little to lateであり、インターバンク市場を揺るがした(金利がオカルト的な数字1000%にもなった)ZeroHedgeはこれをみて次の中国での大型銀行倒産は時間の問題だと書いた。

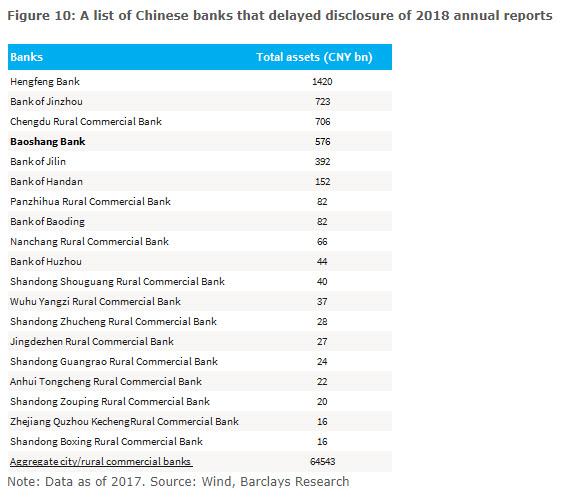

And, in order to present the list of the most likely candidates, will

picked those names that - just like Baoshang - had delayed publishing

their latest annual reports, the biggest red flag suggesting an upcoming

solvency "event." The list is below.

We were right, because not even two months later, the second biggest bank on the list, Bank of Jinzhou has crawled in Baoshang's foosteps and is about to be seized by the government. ZeroHedgeは正しかった、というのもその二月後に、この表の二番手の銀行、錦州銀行がBaoshangの後をたどっている、まさに国有化されんとしている。

According to Reuters and Bloomberg,

Bank of Jinzhou recently met financial institutions in its home

Liaoning province to discuss measures to deal with liquidity problems,

and in a parallel bailout to that of Baoshang, the bank was in talks to

"introduce strategic investors" after a report that China’s financial

regulators are seeking to resolve its liquidity problems sent its

dollar-denominated debt plunging.

Officials including those from the People’s Bank of China and China

Banking and Insurance Regulatory Commission recently held a meeting with

financial institutions in Bank of Jinzhou’s home province of Liaoning

to discuss measures to resolve the lender’s liquidity issues, Reuters

reported Wednesday.

In response to market fears the bank issued a statement on Thursday

that "currently, Bank of Jinzhou’s business operations are normal

overall,” which however did not refer to its liquidity situation. "Recently,

the bank’s board of directors and some major shareholders have been in

talks with several institutions that wish to and have the ability to to

become strategic investors" adding that talks have been “going smoothly.”

By strategist investors it of course meant banks, backstopped by the

government, who would "absorb" the bank, effectively nationalizing it a

la what happened with Baoshang. The only question is whether

stakeholders would also be impaired.

As we reported in June, Jinzhou’s Hong Kong-listed shares have been

suspended since April after it failed to disclose its 2018 financial

statements; adding to its woes, its auditors Ernst & Young Hua Ming LLP and Ernst & Young resigned. As the bank - which first got in hot water in 2015 over its exposure to the scandal-ridden Hanergy Group -

wrote in a filing on the Hong Kong Stock Exchange, E&Y was first

appointed as the auditors of the Bank at the last annual general meeting

of the Bank held on 29 May 2018 to hold office until the conclusion of

the next annual general meeting of the Bank. That never happened,

because on 31 May 2019, out of the blue, the board and its audit

committee received a letter from EY tendering their resignations as the

auditors of the Bank with immediate effect.

6月にZeroHedgeが報告したように、錦州銀行の香港上場株は2018年決算開示をしていないために4月以降売買停止状態だ;さらに残念なことに、監査法人、 Ernst & Young Hua Ming LLP and Ernst & Young、は監査を辞退した。当行によると、ーー最初は2015年にスキャンダルまみれのHanergy Groupに巻き込まれて煮え湯を飲んだーー香港証券取引所の記録によると、E&Yは当行の監査法人として2018年5月29日に指名されその後一年間の監査を任された。しかしこれはかなわなかった、というのも2019年5月31日、突然、取締役会と監査委員会はEYから直ちに監査法人を辞退するという通告を受け取った。

The reason for the resignation: the bank refused to provide

E&Y with documents to confirm the bank's clients were able to

service loans, amid indications that the use of proceeds of certain

loans granted by the Bank to its institutional customers were not

consistent with the purpose stated in their loan documents.

As a result, "after numerous discussions and as at the date of this

announcement, no consensus was reached between the Bank and EY on the

Outstanding Matters and the proposed timetable for the completion of

audit." At this time, the bank also requested the trading in the H

shares (which was frozen on April 1) on The Stock Exchange of Hong Kong

Limited to be suspended until the publication of the 2018 Annual

Results, which will likely never come.

There is another reason why this particular failure is notable: Bank

of Jinzhou is the second-most reliant on interbank financing,

particularly non-bank financial institutions’ deposits, among more than

200 local banks, according to UBS analyst Jason Bedford said when

reached by phone on Thursday.

Which explains its failure: just last month we reported that China's interbank market, especially for smaller banks, had effectively frozen.

It was therefore only a matter of time before other banks reliant on it

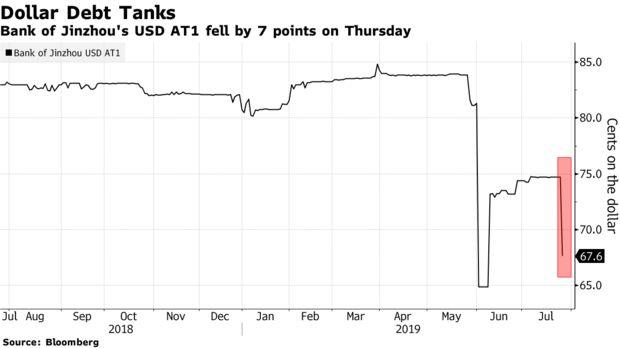

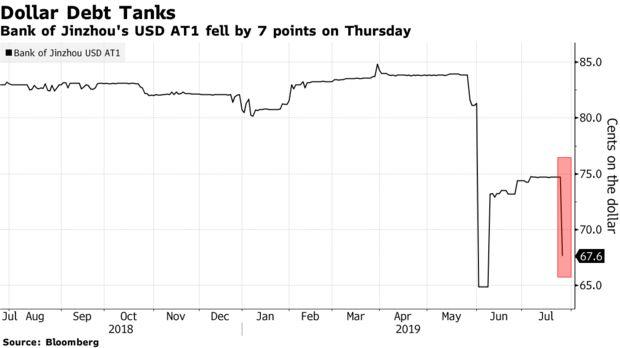

for funding threw in the towel, as Jinzhou has now done. To wit,

Jinzhou's Its dollar-denominated loss-absorbing debt instruments, known

as AT1 bonds, plunged near all time low...

... while the bank’s seven negotiable certificates of deposits -

which would be taken over by another, bigger bank when (if) the bank is

seized and bailed out, were indicated at yields ranging from 3%-5.5% on

Thursday, higher than valuations of 2.8%-3.45%.

Incidentally, back in early June when first reporting on the

resignation of the bank's auditors, we said that "the real question

facing Beijing now is how quickly will Bank of Jinzhou collapse,

how will Beijing and the PBOC react, and what whether the other banks

on the list above now suffer a raging bank run, on which will certainly not be confined just to China's small and medium banks."

The answer: less than 2 months.

Unfortunately for China, it won't stop there. As a reminder, China’s

smaller lenders have been under growing scrutiny since Baoshang Bank's

failure and takeover which led to a sharp repricing of risk for much of

China’s banking system which had long operated under an assumption that

policy makers would support firms in trouble.

"We expect the regulators to step up their support if more financial

institutions run into liquidity issues,” said Becky Liu, head of China

macro strategy at Standard Chartered Plc, who declined to comment

directly about Bank of Jinzhou. "Over time, the cost of funding between

the stronger and weaker financial institutions will see further

divergence."

Amazonで買物をしてContrarianJを応援しよう Albert Edwards: This Was The Final Recessionary Shoe, And It Has Now Fallen by Tyler Durden Thu, 06/27/2019 - 12:45 Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007... ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・ ... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions. ・・・市場は準混乱状態になった、というのも歴史的に見てイールドカーブ反転が過去7回の景気後退の前兆となっているからだ。 However, while the inversion was certainly a memorable event, the question on everyone's lips is how do risk assets perform once the curve flattens and/or inverts. According to backtests from Goldman, since the mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. ...

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...

China Injects Gargantuan 1.1 Trillion In Liquidity This Week by Tyler Durden Wed, 01/16/2019 - 22:19 Following what Bloomberg calculated was a record net reverse repo liquidity injection on Wednesday, when the PBOC injected a whopping 560 billion yuan of liquidity into the financial system via open market operations, the Chinese central bank has done it again and in Thursday's open market operation, it sold 250BN yuan in 7 Day repos (slightly below yesterday's record 350BN), and 150BN in 28 Day repos, which net of maturities resulted in a whopping net 380BN yuan ($56.2BN) liquidity injection. ブルームバーグの算出によると水曜に記録的なリバースレポ流動性注入が行われた、PBOCがなんと公開市場操作で金融システムになんと560B人民元を注入した、中国中央銀行は再び木曜に公開市場操作を行った、250B人民元の7日決済レポを売却した(昨日の350B人民元よりも少し少ない)、そして28日決済のレポを150B人民元注入した、結果としてなんと380B人民元($56.2B)の流動性注入となる。 (訳注:なんか足し算すると辻褄が合いません、ブルーム...