Authored by Jesse Colombo via RealInvestmentAdvice.com,

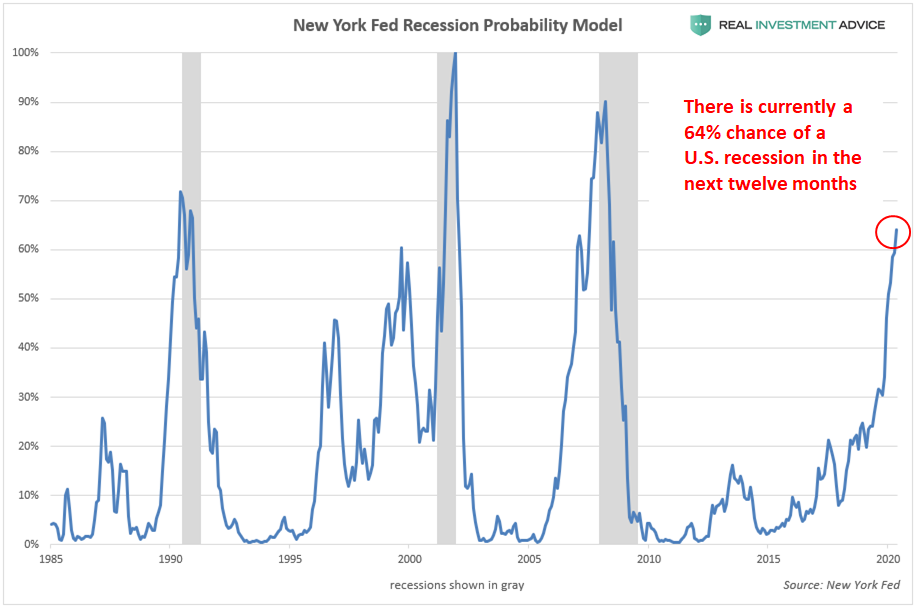

As the probability of a U.S. recession in the next year grows rapidly (it

may be as high as 64%), many bullish economists and financial

commentators are unsurprisingly downplaying this risk. One of their main

arguments is that interest rates have not been hiked aggressively

enough to tip the economy over into a recession. While it is true that

U.S. interest rates are still very low by historic standards, the reality is that rates do not have to rise anywhere near as high as

they did in the past to cause recessions due to America’s debt load

that has grown dramatically over the past several decades. 来年の米国景気後退入り可能性は急速に増しているなかで(可能性は64%)、多くの強気はエコノミストや金融コメンテーターは驚くことにこのリスクを過小評価している。彼らが主に主張することの一つが金利は積極的に引き上げられておらず景気後退を引き起こすほどのレベルではない、というものだ。歴史的に見て米国金利ははまだとても低いのは確かだが、現実には、過去に景気後退を引き起こしたレベルまで金利を引き上げることができないというのが本当のところだ、というのもここ数十年米国の債務負荷が劇的に増えたためだ。

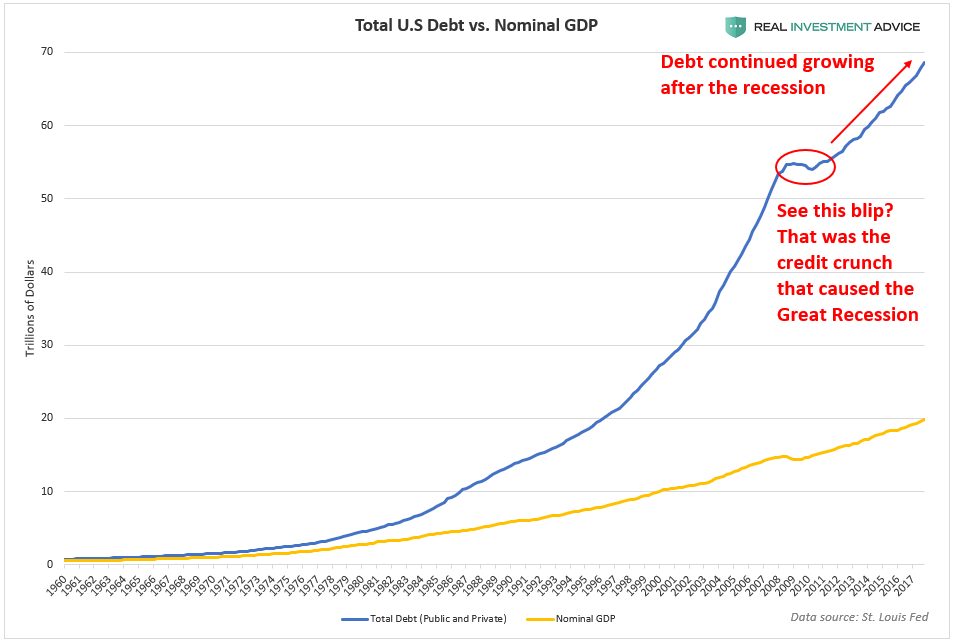

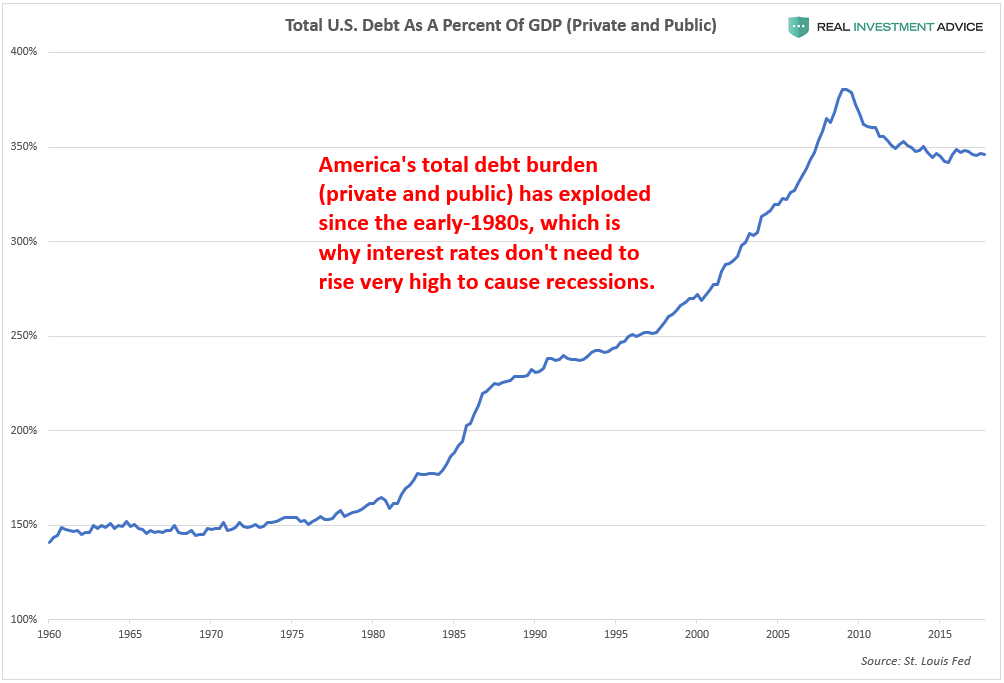

Since the early-1980s, total U.S. debt – both public and private –

has been growing at a faster rate than the underlying economy, as

measured by the nominal GDP:

As a result of debt growing faster than our underlying economy,

America’s debt as a percent of GDP soared from just over 150% in the

early-1980s to approximately 350% in recent years. This higher debt

burden is the reason why our economy simply cannot handle interest rates as high as they were before 2008.

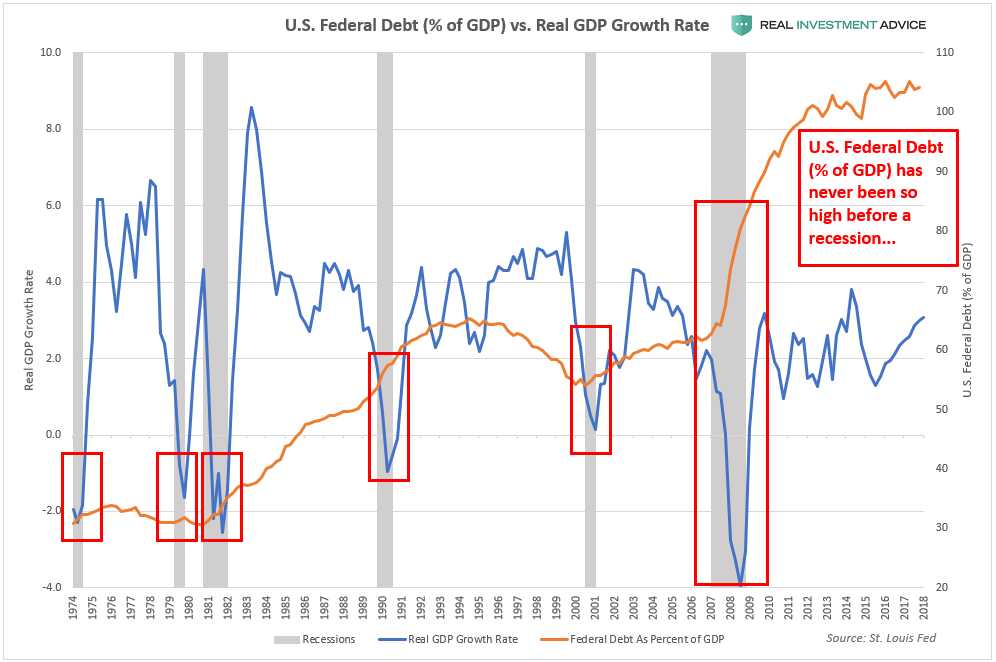

Particularly worrisome is the fact that U.S. federal debt is at a

record of over 100% of the GDP (vs. 62% before the Great Recession),

which will make it a much greater challenge to keep the economy afloat

in the coming recession:

Market strategist Sven Henrich described our conundrum quite well:

市場ストラテジストSven Henrichは今我々が抱える難問を的確に表現した:

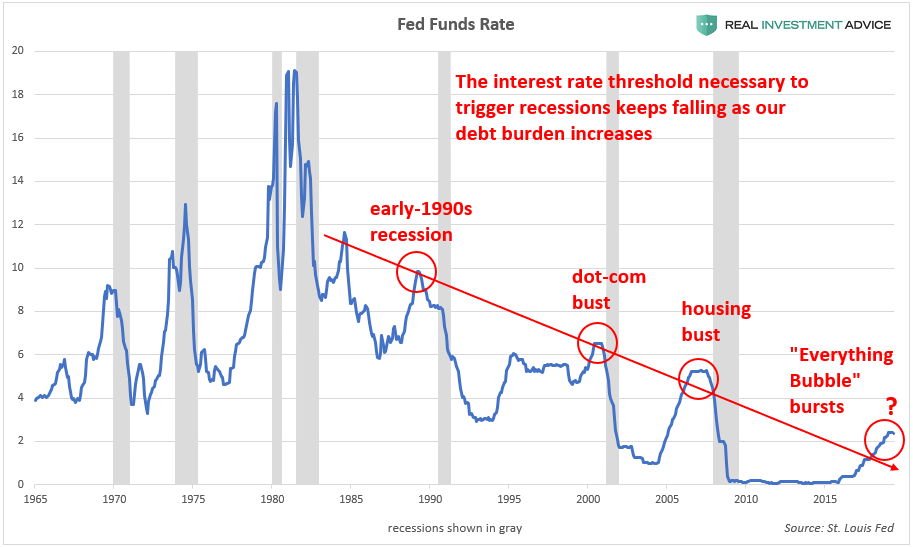

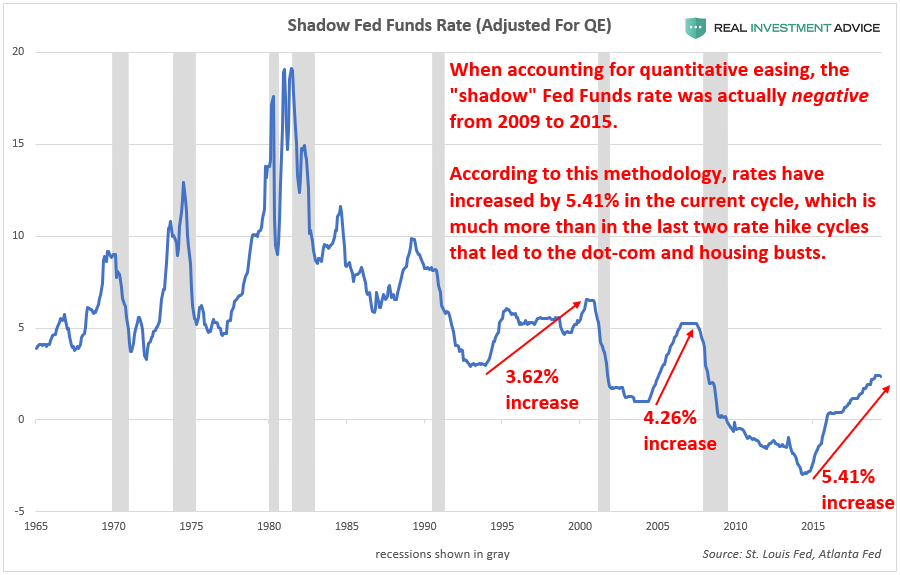

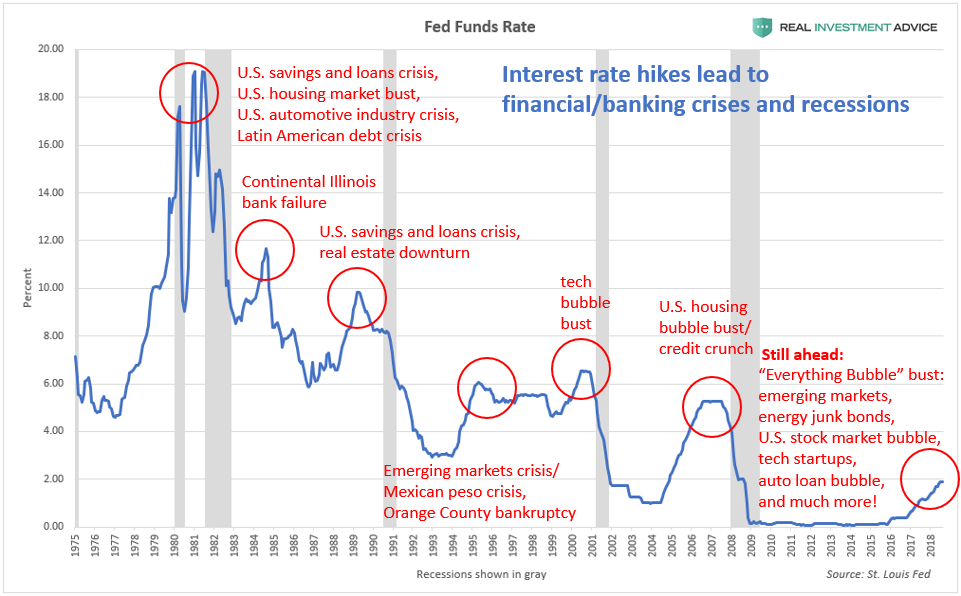

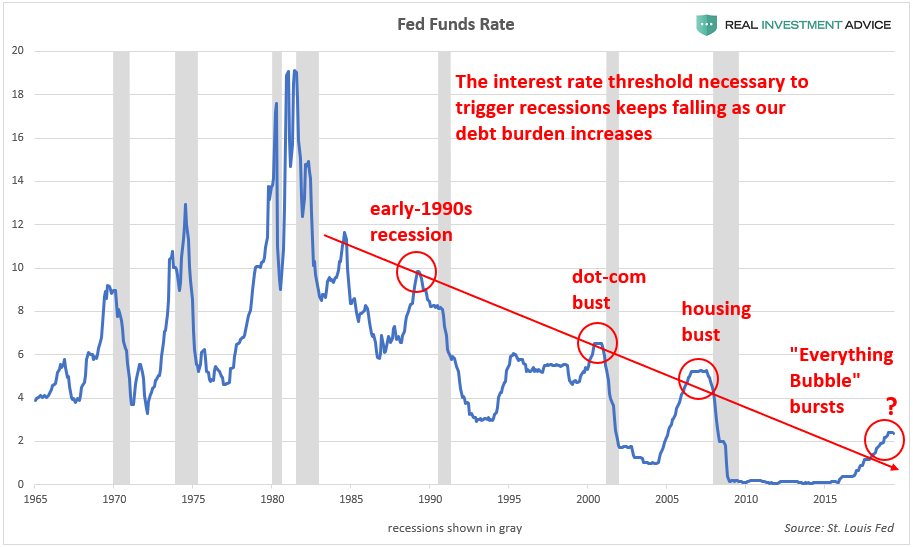

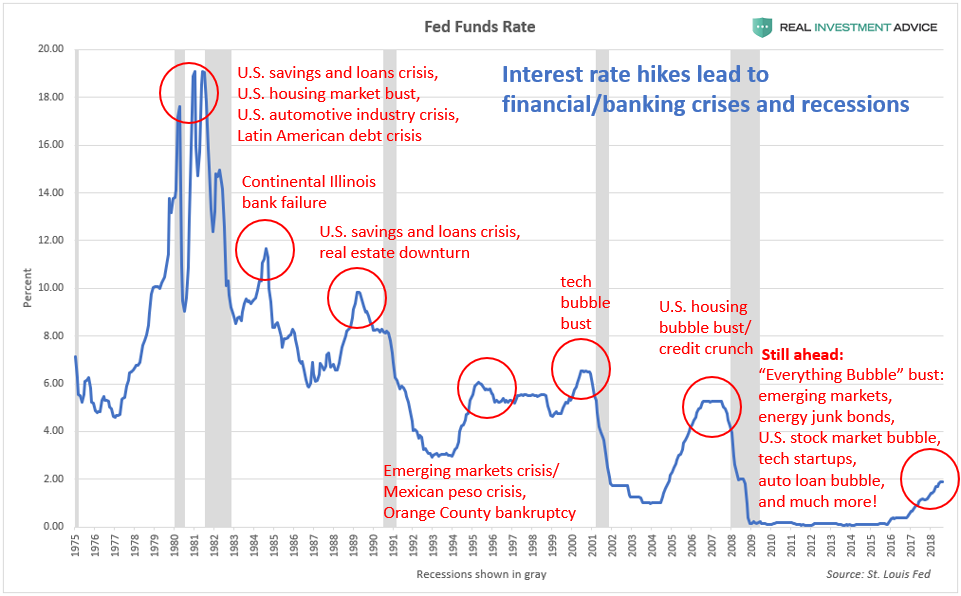

As the Fed Funds rate chart below shows, the interest rate threshold

necessary to trigger recessions (recessions are designated by the gray

bars) keeps falling as our debt burden increases:

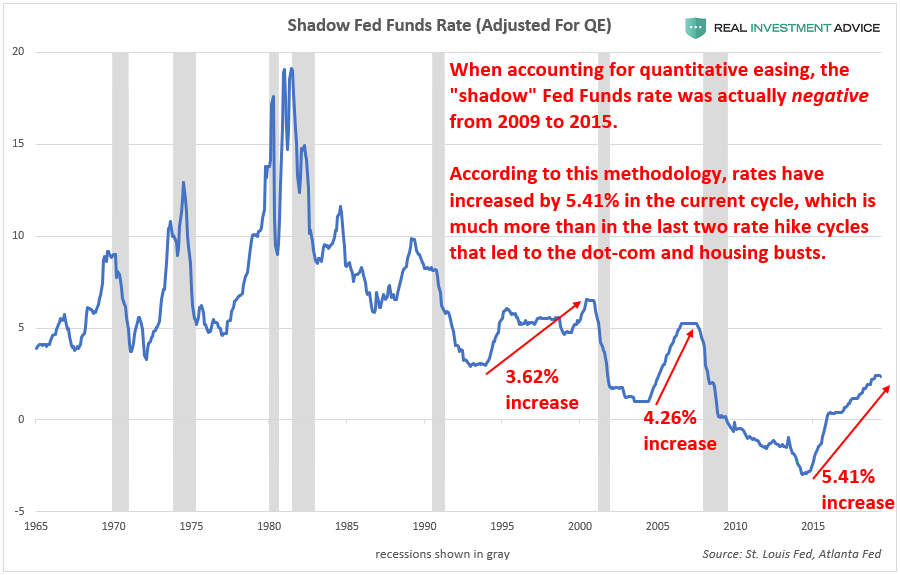

Though many optimists are quick to point out that the benchmark Fed

Funds rate was only increased from 0% to 2.5% during the current

tightening cycle, the reality is that the current tightening cycle is even more aggressive than the past several cycles when the Fed Funds rate is adjusted for quantitative easing(this is known as the shadow Fed Funds rate – learn more).

According to this methodology, interest rates have increased by the

equivalent of 5.41% in the current cycle versus just 3.62% before the

2001 recession and 4.26% before the Great Recession of 2007 to 2009:

多くの楽観主義者の指摘では、今回の引き締めサイクルでFFRは0%から2.5%に増えたに過ぎないという、しかしながら、現実には現在の金利引き締めは過去数回の引き締めよりももっと積極的なものだ、というのもFFRは量的緩和を考慮すべきだからだ(このことはシャドーFFRとしてしられているーーくわしくはこちら)。この手法を適用すると、現在の金利引き上げはすでに過去の引き上げなら5.41%に相当するものである、一方2001年の景気後退前の引き上げは3.62%であり、2007から2009年のthe Great Recession前では4.26%だった:

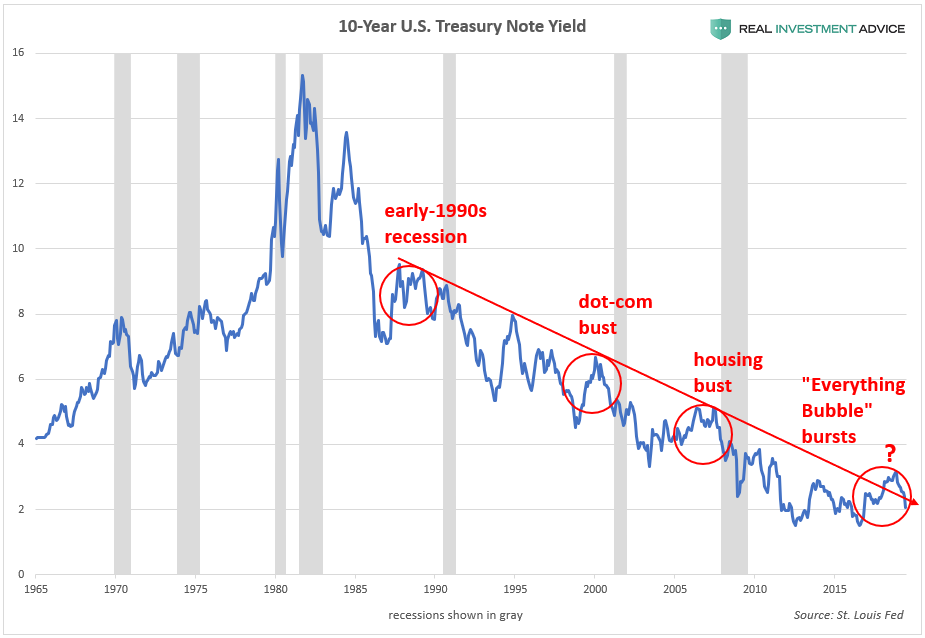

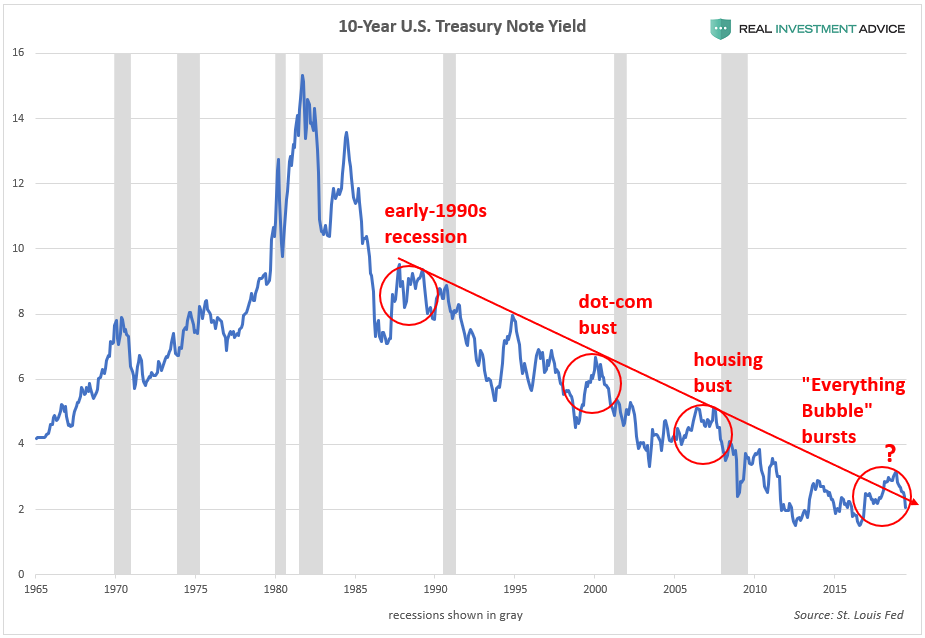

The 10-year U.S. Treasury note yield also confirms the message given

by the Fed Funds rate: the U.S. economy has become increasingly

sensitive to higher interest rates:

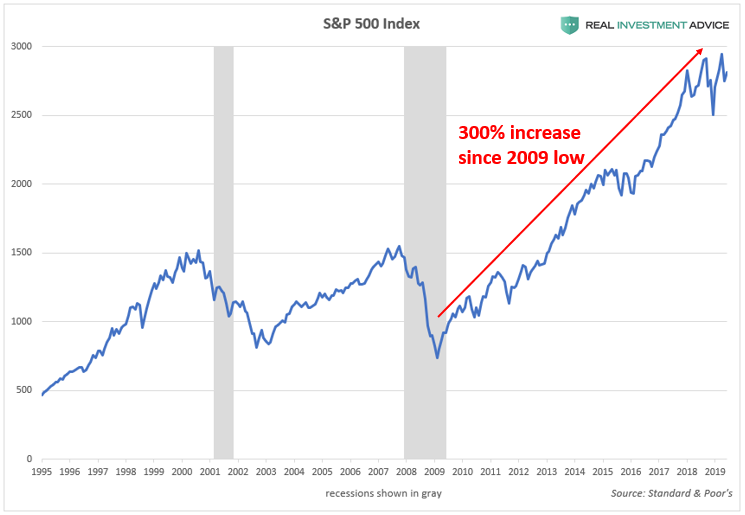

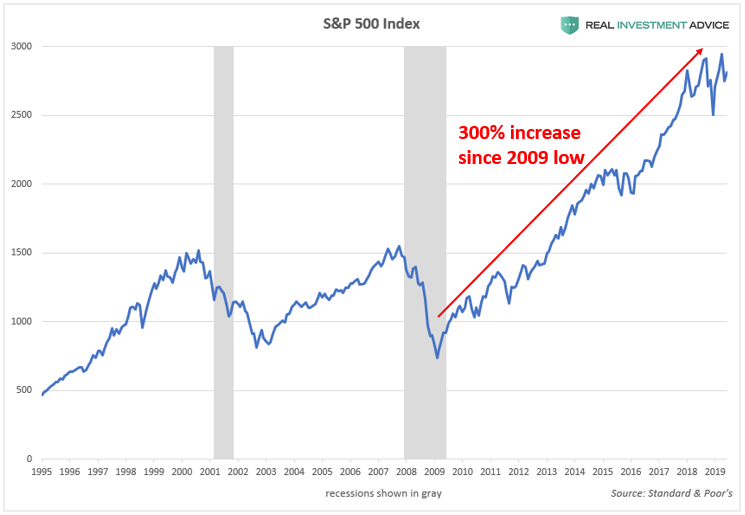

The rapidly-approaching recession poses a serious risk to the

extremely inflated U.S. stock market, which is up 300% since its 2009

low. The U.S. stock market is experiencing an unsustainable bubble due

to the aggressive actions of the Fed (see my detailed explanation).

To summarize, interest rates do not need to rise much to throw the heavily-indebted U.S. economy into a recession now; furthermore, interest rates have likely already risen to the levels that are necessary to tip our feeble economy over into a recession, as evidenced by rapidly weakening economic data. At

this stage of the game, everyone needs to be realistic – we can’t

expect to have a full decade of unprecedented central bank stimulus

without a tremendous bust. Central banks can only create temporary

economic booms by borrowing from the future rather than sustainable,

organic economic booms. Anyone who does not believe in that truth right

now, or is not aware of it, will inevitably become a firm believer in

the coming bust.

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....