While

the western world (and much of the eastern) has been preoccupied with

predicting the consequences of Trump's accelerating global trade/tech

war, Beijing has had its hands full with avoiding a bank run in the

aftermath of Baoshang Bank's failure, scrambling to inject massive

amounts of liquidity last week in the form of a 250 billion yuan net

open market operation to thaw the interbank market which was on the

verge of freezing, and sent overnight funding rates spiking and bond

yields and NCD rates higher.

Unfortunately for the PBOC, Beijing is now racing against time to

prevent a widespread panic after it opened the Pandora's box when it

seized Baoshang Bank two weeks ago, the first official bank failure in a

odd replay of what happened with Bear Stearns back in 2008, when

JPMorgan was gifted the historic bank for pennies on the dollar.

PBOCにとって残念なことに、北京政府は今や、2周間前のBaoshang Bank 吸収でパンドラの箱を開いた後の混乱拡大を収束させることで手一杯だ、公式に銀行倒産を認めたことが2008年のベア・スターンズを思い起こさせる、当時JPMorgaは棚ぼたでこの伝統ある銀行を手中に納めた。

And with domino #1 down, the question turns to who is next, and will they be China's Lehman.

ドミノ#1に伴い、問題は次に起こることだ、それは中国のレーマン銀行となるだろう。

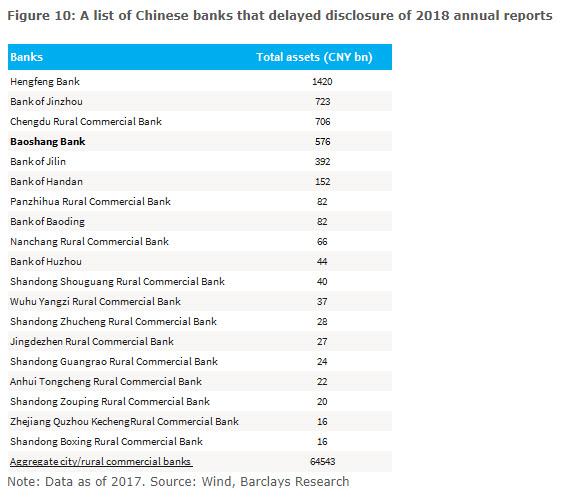

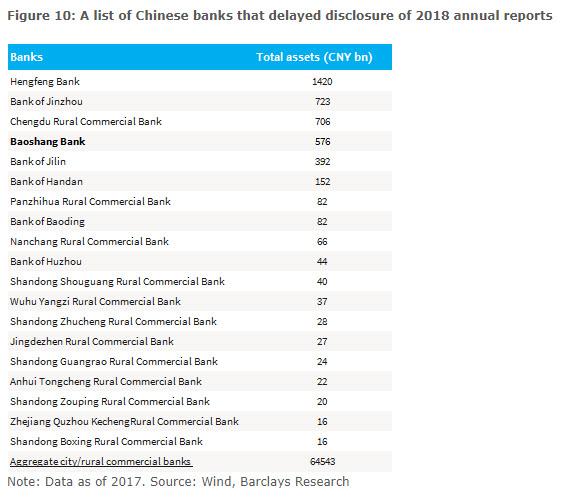

This was the question we asked last Thursday,

when we published a list of regional banks that have delayed publishing

2018 reports, the biggest red flag suggesting an upcoming bank solvency

"event."

One day later we may have gotten our answer, when the Bank of

Jinzhou, a city commercial bank in Liaoning Province, the second name

in the list above, and with some $105 billion in assets, notably bigger

than Baoshang, announced that its auditors Ernst & Young Hua Ming

LLP and Ernst & Young had resigned, not long after the bank

announced it would delay the publication of its annual reports.

その翌日に我々は答えを得たかもしれない、それはBank of Jinzhou 錦州銀行、遼寧省の商業銀行だ、この表では二番目に書かれている、資産規模は$105B、Baoshangよりもずっと大きい、この銀行の広報によると、監査法人Ernst & Young Hua Ming LLP and Ernst & Young が辞退した、当行が年次報告開示遅延を広報してからそう遅くない時期にだ。

For those confused, the delay of an annual report and the resignation of an auditor, means a bank failure is not only virtually certain but practically imminent.

As the bank - which first got in hot water in 2015 over its exposure to the scandal-ridden Hanergy Group -

writes in a filing on the Hong Kong Stock Exchange, E&Y was first

appointed as the auditors of the Bank at the last annual general meeting

of the Bank held on 29 May 2018 to hold office until the conclusion of

the next annual general meeting of the Bank. That never happened,

because on 31 May 2019, out of the blue, the board and its audit

committee received a letter from EY tendering their resignations as the

auditors of the Bank with immediate effect.

The reason for the resignation: the bank refused to provide E&Y

with documents to confirm the bank's clients were able to service loans,

amid indications that the use of proceeds of certain loans granted by

the Bank to its institutional customers were not consistent with the

purpose stated in their loan documents.

As a result, "after numerous discussions and as at the date of this announcement, no

consensus was reached between the Bank and EY on the Outstanding

Matters and the proposed timetable for the completion of audit." As a result, after a clear breakdown in relations with its own auditor, the

Board decided to appoint Crowe (HK) CPA Limited as the new auditors of

the Bank to fill the casual vacancy following the Resignation and to

hold the office until the conclusion of the 2018 annual general meeting

of the Bank (we are taking the under with lots of leverage as Crowe will

likewise quit in the coming weeks if not days).

And confirming that not even the bank's management believes this

"justification" will be enough to avoid a rout in the stock, the bank

reported that it has requested the trading in the H shares (which was

frozen on April 1) on The Stock Exchange of Hong Kong Limited to be

suspended until the publication of the 2018 Annual Results. For anyone

who hopes that these shares will ever be unfrozen for trading, there are

a few bridges in Brooklyn that are for sale.

The real question facing Beijing now is how quickly will Bank of

Jinzhou collapse, how will Beijing and the PBOC react, and what whether

the other banks on the list above now suffer a raging bank run, on which

will certainly not be confined just to China's small and medium banks.

当行取締役はこの出来事を「正当化」することで株価下落を回避するのに十分と考えている一方、香港証券取引所での売買は2018年次決算開示までサスペンドとされている(すでに4月1日から売買凍結となっている)。ただし株式売買再開は望み薄だ。現在北京政府が直面している疑念は、 Bank of Jinzhou 倒産までにどれだけの時間があるか、またその時如何に北京政府とPBOCが対応するかだ、そしてこの表の他の銀行も倒産となる銀行等産の嵐がおきるかどうか、どうなるかだ、さらにはそれが中小銀行にとどまるかも懸念される。

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....