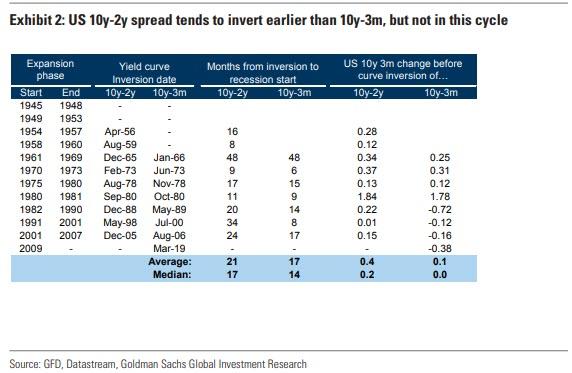

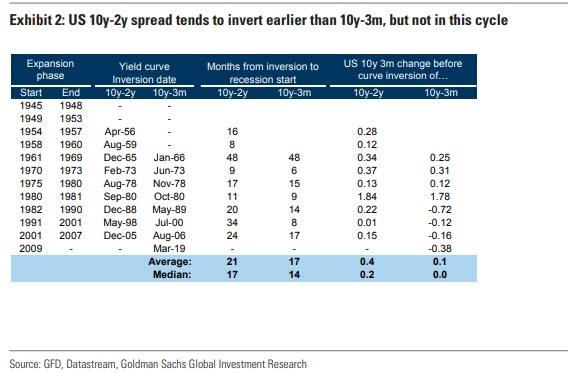

Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007...

ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・

... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions.

However, while the inversion was certainly a memorable event, the

question on everyone's lips is how do risk assets perform once the curve

flattens and/or inverts. According to backtests from Goldman, since the

mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. しかしながら、イールドカーブ反転は確かに象徴的なできごとだが、誰もが知りたいのはイールドカーブ平坦化・反転化後の株式のパフォーマンスだ。ゴールドマンのバックテストによると、1980年代なかば以来でみて、株価急落が起きるのはイールドカーブ反転後再度急峻になるときだ。

In other words, as we noted then, "Curve Inversion Is Bad, But It's The Steepening After That Kills."

Fast forward to today, when in his latest bearish missive, SocGen's

permabear Albert Edwards picks up where we left off, and in a note

titled "the final recession shoe has now fallen", he notes that while

inversion of the US yield curve is seen as a reliable precursor to US

recessions, "it has a long and variable lead time", and instead "a far more immediate and present danger of recession occurs when after inversion, a rapid steepening occurs." 現在までの状況を早送りしてみると、彼の最新の弱気記事だが、SocGenのパーマベア Albert Edwardsがこの話題を取り上げた、ただしZeroHedgeは紹介しなかった、タイトルは「景気後退劇場の最後の見せ場到来」、彼が言うには、米国イールドカーブ反転は信頼できる景気後退予兆だが、「十分なリードタイムがある」、そしてむしろ「インバージョン後に急速に急峻化が起きると、それは直ちに景気後退の危機が迫っている」。

Sound familiar?

知ってました?

In any case, as we first commented in early 2019, Edwards notes that this subsequent steepening "usually informs investors the cycle is over and it is time to flee for the hills."

Well, for those who haven't figured out the punchline yet, rapid curve steepening is now occurring, and as Edwards gleefully concludes, this "suggests recession may indeed either be imminent or else it has already arrived." そう、まだ結末を認識できない人に教えてあげよう、急速なイールドカーブ急峻化がいま起きつつ在る、そしてEdwardsが明快に結論付けるが、この状況は「景気後退がすぐそこに差し迫っている、もしくすでに景気後退入りしている」のだ。

Should Edwards be right, the implications are clearly huge, and not

just for the economy and markets - perhaps the most dramatic consequence

will be what happens with the world's most powerful institution: the

Federal Reserve.

Edwardsの言っていることは正しいのだろうか?、その影響力はあまりに大きい、そして単に経済や市場だけでなくーーたぶんもっとも劇的な結末とは世界最強の組織に起きることだ:the Federal Reserve 。

"As a long time harsh critic of the Fed (and other central banks) for

their obscenely easy money policies" Edwards writes that he is loath to

criticize President Trump’s nearly constant slams of Fed Chair Powell,

especially since President Trump has a very clear agenda: namely, he

is going to make sure the Fed gets the blame from the electorate if the

economy goes into recession and the equity market plunges ahead of the

next presidential election. 「長年FEDや世界の中央銀行には手厳しい批判がなされてきた、緩和政策に浸りすぎてきたことだ」。Edwardsはトランプ大統領を批判したくない、大統領はいつもFED議長Powellを罵る、特にトランプ大統領の意図は明確だ:すなわち、FEDが大統領選挙に責任を負っている、もし景気後退入りとな来年の大統領選挙に向けて株価が下がるとそれはFEDの責任だと。

"And by hook or by crook, Powell will be out on his ear", Edwards says.

「そしてどういう手段を撮ろうとも、Powellは聞く耳を持たないだろう」とEdwardsは言う。

Which is good news and bad news, because while Powell clearly threw

in the towel on the hawkish monster that he was perceived as less than a

year ago when he spooked markets that the Fed would keep hiking until

the mid-3's, and is now as dovish and meek as Yellen or even Bernanke,

it's not like his departure would also end the Fed.

Quite the opposite, because considering that this is what President

Trump is like now, imagine what he will be if the US leads the global

economy into another deep recession and financial crisis like 2008:

Even before the irascible Trump became President, I said the Fed

would lose its (supposed) independence if they were the midwife to

another crisis. There will be no deft, disingenuous shifting of blame to

the commercial banks this time around. The Fed will carry the can.

As a result, Trump will promptly appoint a Fed chair who is the most

dovish one can find, and here Kashkari comes to mind: after all, the

former Goldman IT banker and "architect" of the 2008 bank bailout plan

(or rather Paulson's smokescreen) not accidentally said he was hoping

for a 50bps rate cut earlier this week - he is clearly angling for

Powell's job.

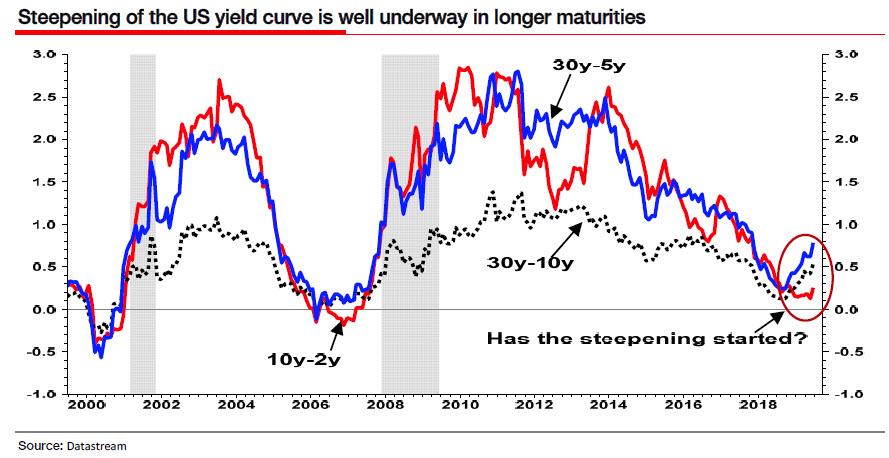

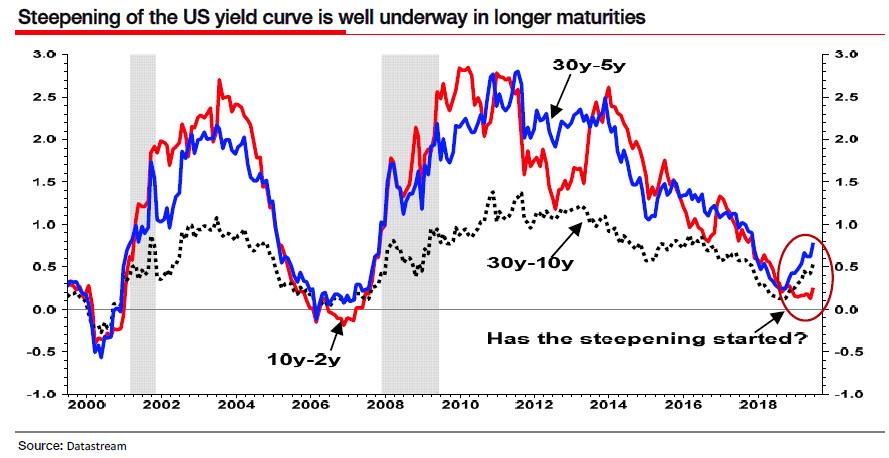

Meanwhile, and going back to the recession narrative, it's not just

the re-steepening of the 3M-10Y. As Edwards ominously concludes, there

is another key indicator that everyone is focused on: "we (and others),

have also pointed out that the alarm bells for an imminent recession

would really start ringing if the 10y-2y curve began to steepen." To be

sure, it is reassuring that this has not happenied - yet - but, as

Edwards concludes "the rest of the yield curve (which leads to 10y-2y

steepening) is now shouting recession from the rooftops."

So how long until Neel "the Chump"

Kashkari is Fed chair? The good news is that it will probably not

happen tomorrow, so readers at least have enough time to buy some more

gold and cryptos before the new Fed chair unleashes the biggest - and

last - liquidity tsunami in US history, one which culminates with the

dollar losing it reserve currency status. Whether that leaves Zuckerberg as the world's central bank, or the IMF finally digitizes the SDR in Libra's footsteps, remains to be seen.

というわけで Neel "the Chump" Kashkari がFED議長になるまでどれくらいの時間が残されているだろうか?幸いなことにそれが明日起きるわけではない、というわけで読者諸君にはまだゴールドや暗号通貨を買います十分な時間が残されている、新任FED議長が米国史上最大で最後の流動性津波を引き起こす前にだ、こうなるとついにドルは準備通貨の地位を失う。こうなるとZuckerbergが世界の中央銀行となるか、もしくはIMFがとうとうLibraの足元でSDRをデジタル化するかもしれない、これを見ることになるかもしれない。

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....

China Injects Gargantuan 1.1 Trillion In Liquidity This Week by Tyler Durden Wed, 01/16/2019 - 22:19 Following what Bloomberg calculated was a record net reverse repo liquidity injection on Wednesday, when the PBOC injected a whopping 560 billion yuan of liquidity into the financial system via open market operations, the Chinese central bank has done it again and in Thursday's open market operation, it sold 250BN yuan in 7 Day repos (slightly below yesterday's record 350BN), and 150BN in 28 Day repos, which net of maturities resulted in a whopping net 380BN yuan ($56.2BN) liquidity injection. ブルームバーグの算出によると水曜に記録的なリバースレポ流動性注入が行われた、PBOCがなんと公開市場操作で金融システムになんと560B人民元を注入した、中国中央銀行は再び木曜に公開市場操作を行った、250B人民元の7日決済レポを売却した(昨日の350B人民元よりも少し少ない)、そして28日決済のレポを150B人民元注入した、結果としてなんと380B人民元($56.2B)の流動性注入となる。 (訳注:なんか足し算すると辻褄が合いません、ブルーム...