Deutsche Bank

strategists Jim Reid and Craig Nicol wrote a report this week that

echos what I and other Austrian School economists been saying for many

years: actions taken by governments and central banks to extend

business cycles and prevent recessions lead to even more severe

recessions in the end.MarketWatch reports –

ドイツ銀行のストラテジスト Jim Reid とCraig Nicolが今週報告書を書いた、その内容は私や他のオーストリア学派経済学者が長年警鐘を告げていたものと同様だ:政府や中央銀行がビジネスサイクルを引き延ばし景気後退を回避しようとするが、これが結局もっと深刻な景気後退を引き起こす。

MarketWatchの報告ーー

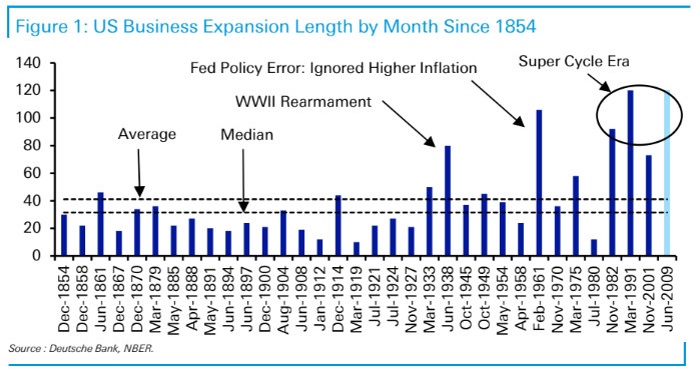

The 10-year old economic

expansion will set a record next month by becoming the longest ever.

Great news, right? Maybe not, say strategists at Deutsche Bank.

Prolonged

expansions have become the norm since the early 1970s, when the tight

link between the dollar and gold was broken. The last four expansions

are among the six longest in U.S. history .

Why so? Freed from the

constraints of gold-backed currency, governments and central banks have

grown far more aggressive in combating downturns. They’ve boosted

spending, slashed interest rates or taken other unorthodox steps to

stimulate the economy.

“This

policy flexibility and longer business cycle era has led to higher

structural budget deficits, higher private sector and government debt,

lower and lower interest rates, negative real yields, inflated financial

asset valuations, much lower defaults (ultra cheap funding), less

creative destruction, and a financial system that is prone to crises,’ they wrote in a lengthy report.

“In

fact we’ve created an environment where recessions are a global

systemic risk. As such, the authorities have become even more encouraged

to prevent them, which could lead to skewed preferences in

policymaking,” they said.“So we think cycles continue

to be extended at a cost of increasing debt, more money printing, and

increasing financial market instability.”

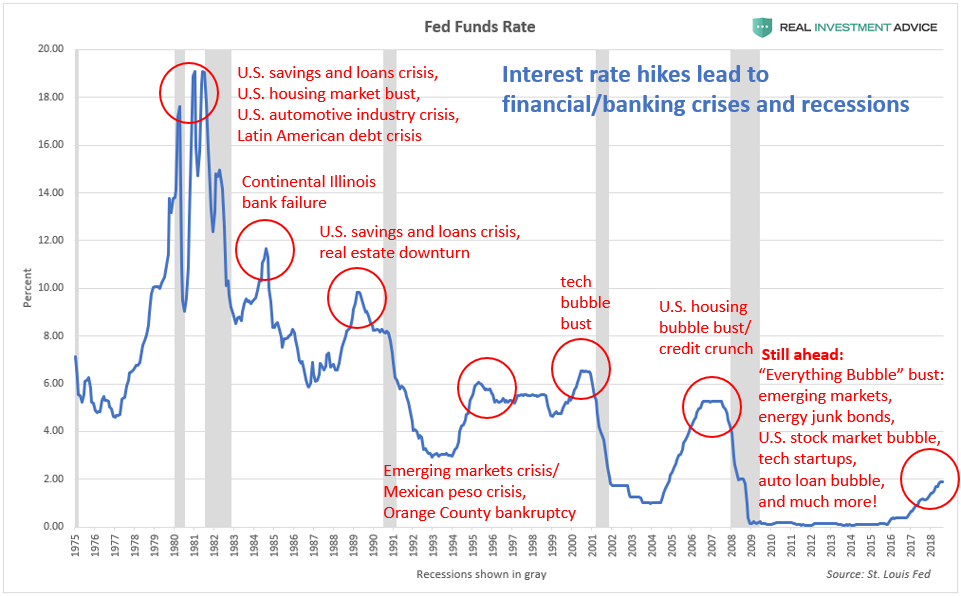

As I have explained

in the past, when central banks like the U.S. Federal Reserve cut

interest rates to low levels, they manage to create economic booms by

encouraging borrowing and higher asset prices. These economic booms are

often based on dangerous economic bubbles that burst and lead to

recessions when interest rates are normalized again. As the chart below

shows, financial crises and recessions (see the gray vertical bars)

occur after rate hike cycles, including the dot-com and U.S. housing

market crashes.

The false economic booms that occur when central banks interfere with

the business cycle trick investors and entrepreneurs into thinking that

they are organic and sustainable booms. When the booms inevitably turn

to busts, the bad investments that result are known as malinvestments – 中央銀行が景気サイクルに介入することで生み出される偽の景気ブームは投資家や起業家に誤解を引き起こす、この経済ブームは自然なもので持続的なものだと。ブームというものには必ず終焉がある、このとき、筋悪投資がはじめてmalinvestmentsとして認識されるーー

Malinvestment is a

mistaken investment in wrong lines of production, which inevitably lead

to wasted capital and economic losses, subsequently requiring the

reallocation of resources to more productive uses. “Wrong” in

this sense means incorrect or mistaken from the point of view of the

real long-term needs and demands of the economy, if those needs and

demands were expressed with the correct price signals in the free

market.

Malinvestmentとは wrong lines of production 方針を間違えた生産への誤解による投資だ、これは必ず資本の浪費となり経済的損失を伴う、その後もっと生産的な目的へと資本の再配分が必要となる。ここで言うところの「Wrong」とは長期的視点での実需を見誤ったという意味だ、自由市場ならばこのような需要には正しい(投資、債務)費用が示される。

Random, isolated entrepreneurial miscalculations and

mistaken investments occur in any market (resulting in standard

bankruptcies and business failures) but systematic, simultaneous

and widespread investment mistakes can only occur through

systematically distorted price signals, and these result in depressions

or recessions. Austrians believe systemic malinvestments occur

because of unnecessary and counterproductive intervention in the free

market, distorting price signals and misleading investors and

entrepreneurs.

For Austrians, prices are an essential information

channel through which market participants communicate their demands and

cause resources to be allocated to satisfy those demands appropriately.

If the government or banks distort, confuse or mislead

investors and market participants by not permitting the price mechanism

to work appropriately, unsustainable malinvestment will be the

inevitable result.

Because the current economic cycle has lasted for an unusually long

time due to the actions of central banks, an unprecedented amount of

malinvestment has built up globally that needs to be cleansed in the

coming recession. It’s similar to a night of drinking: the more you

drink and the later you stay out, the worse your hangover is going to

be. Globally speaking, the last decade has been the bender to

end all benders and the coming hangover is going to proportionally

severe.

Amazonで買物をしてContrarianJを応援しよう Albert Edwards: This Was The Final Recessionary Shoe, And It Has Now Fallen by Tyler Durden Thu, 06/27/2019 - 12:45 Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007... ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・ ... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions. ・・・市場は準混乱状態になった、というのも歴史的に見てイールドカーブ反転が過去7回の景気後退の前兆となっているからだ。 However, while the inversion was certainly a memorable event, the question on everyone's lips is how do risk assets perform once the curve flattens and/or inverts. According to backtests from Goldman, since the mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. ...

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...