There

was a time when in the years following the financial crisis, every

Friday the FDIC would report of one or more small and not small banks

failing, as their liabilities exceeded their assets, who were taken over

by larger peers with a taxpayer subsidy to cover the capital shortfall.

And while this weekly event, also known as "FDIC Failure Friday" has

faded from the US, for now, it has made a grand appearance in China.

China’s financial regulators said on Friday the country’s banking and

insurance regulator and the central bank, will take control of the

small, troubled inner Mongolia-based Baoshang Bank due

to the serious credit risks it poses. The regulator’s control of

Baoshang will last for a year starting on Friday, the People’s Bank of

China (PBOC) and China Banking and Insurance Regulatory Commission

(CBIRC) said on their websites.

China Construction Bank (CCB) will be entrusted to handle the

business operations of the small lender, based in the industrial city of

Baotou, the statement said.

内モンゴルの小規模貸し手に対しては中国建設銀行が救済する、とその声明に書かれている。

Such a takeover by national authorities is extremely rare, and takes

place amid gathering concerns among regulators and financial analysts

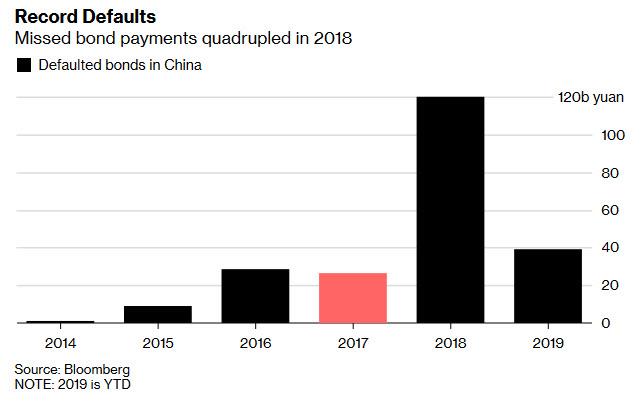

about a renewed surge in bad debts...

... a record pace of corporate defaults,

amounting to 39.2 billion yuan of domestic bond defaults in the first

four months of the year, 3.4 times the total for the same period of

2018...

Moody's analyst Yulia Wan told the WSJ that regulators likely decided

to take over Baoshang to limit any fallout to businesses in Inner

Mongolia. “The move is to reduce the risk of a shock to the local

economy,” said said, adding that the Baoshang takeover appeared

to be the first time that national authorities seized control of a bank

since Chinese lenders started listing on stock markets in the 1990s.

In the past when banks came under pressure, local authorities would

pull together funds from local state-owned firms and investors, or have

another bank stage a takeover.

As Reuters adds, this extremely rare takeover - the

first in nearly three decades - comes at a time when the PBOC has

aggressively eased financial standards and cut reserve ratios for

smaller banks to avoid just this outcome, and highlights the

long struggle of some smaller regional lenders in China, which suffer

from deteriorating asset qualities, inadequate capital buffers, and poor

internal controls and corporate governance

Baoshang Bank rose to prominence after its key stakeholder Tomorrow

Holdings was targeted in a government crackdown on systemic risks posed

by financial conglomerates. The bank was also linked to financier Xiao

Jianhua, according to the WSJ.

Xiao left Hong Kong and crossed the border into mainland China in early

2017, according to statements from Hong Kong police and his company,

and he hasn’t been heard from since.

Later that year, Baoshang "unexpectedly" reported a capital shortage.

この年の遅く、Baoshangは「突然」資金不足を開示した。

Chinese ratings agency Dagong Global Credit Rating Co. then revised its

outlook on Baoshang to negative, questioning the lender’s ability to

repay borrowings. They were right.

中国の格付会社 Dagong Global Credit Rating Coはその時 Baoshanの見通しをネガティブに格下げした、借金返済に際しての貸し手能力に疑念が持たれたのだ。

彼らの判断は正しかった。

Understandably, there is concern the Baosheng takeover "will add to

the vulnerability of country’s financial system amid the economic

slowdown." The reason: if one bank can fail, all can fail. And how long

before depositors jog, run or sprint to their own bank to yank whatever

deposits they have there, in the process beginning the terrifying bank

run domino sequence of events, that eventually collapses China's $40

trillion banking system (by comparison, the US banking system is about

$20 trillion).

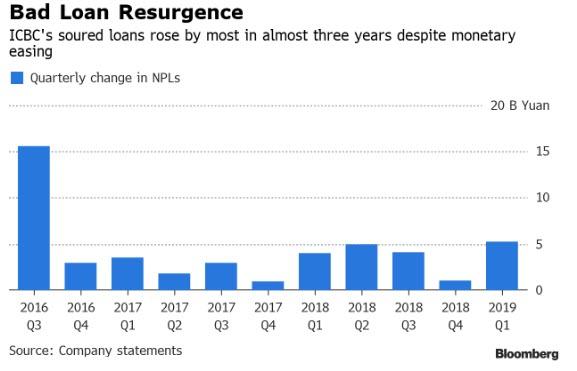

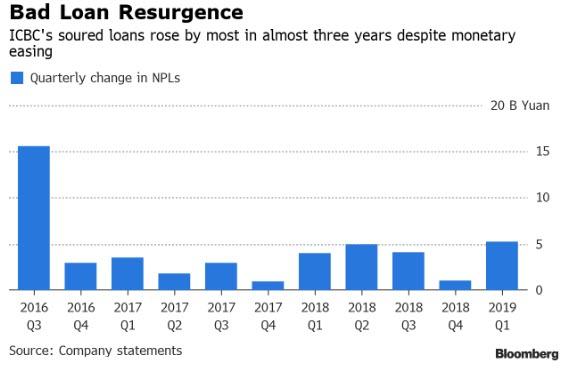

While it has been generally described as a "small" bank, Baoshang

had a total of 156.5 billion yuan ($22.68 billion) of outstanding loans

by the end of 2016, a 65% jump from the end of 2014, according

to the bank’s last filing on its assets and liabilities on its website.

What is absolutely bizarre, however, is that the bank's "official" non-performing loan ratio then was only 1.68% as of December 2016. That,

in itself, would never have been sufficient to force a takeover, and

suggests that not only was the bank's real bad debt ratio much higher,

but that China continues to chronically under-represent the true state

of its NPLs to avoid bank runs.

The last time Baoshang disclosed financial data was in the third

quarter of 2017. Then it had 576 billion yuan in assets and 543 billion

yuan in liabilities, with a net profit of 3.2 billion yuan. Based on

those 2017 numbers, analyst Long Chen with consulting firm Gavekal

Dragonomics estimated that Baoshang back then was ranked around the 50th largest bank in the nation. Baoshangが最後に金融データを開示したのは2017Q3だ。このとき資産が576B人民元で、債務は543B人民元だった、またネット利益は3.2B人民元だった。これらの2017年の数値からすると、Gavekal Dragonomicsコンサルティング会社のアナリストLong Chenの見積もりでは、当時Baoshangは50番目に大きな銀行だった。

Naturally, to avoid a panic bank run among other smaller, less

capitalized banks, the CBIRC said that principal and interest on

personal saving accounts in the bank will be fully guaranteed, and the

business operations of Baoshang bank will not be affected by the

takeover.

The takeover of the bank is the first in decades, and takes place

amid China’s crackdown on systemic financial risks, which in February

2018 resulted in the take over of former roll-up giant and conglomerate

Anbang Insurance, which in 2015-2016 made eyebrow-raising investments in

overseas property, including the Waldorf Astoria hotel in New York.

Anbang’s chairman, Wu Xiaohui, was sentenced to 18 years in prison later

that year after being convicted of fraud and abuse of power. Wu

expressed remorse, according to the court that sentenced him, but he

also said he doubted he violated any laws. He hasn’t made a public

statement since.

The question now is whether bank investors, having seen first hand

for the first time in nearly 30 years, that a Chinese bank can fail (and

be taken over by the state), will jog at a leisurely pace, or not so

leisurely, to their own local bank and pull out their deposits in a

cool, calm and collected manner... or not so cool, calm and collected.

If so, the trade with between the US and China will have a clear winner

in the very near future.

Amazonで買物をしてContrarianJを応援しよう Silver Outperforming Gold 2 Adam Hamilton July 26, 2019 3232 Words Silver has blasted higher in the last couple weeks, far outperforming gold. This is certainly noteworthy, as silver has stunk up the precious-metals joint for years. This deeply-out-of-favor metal may be embarking on a sea-change sentiment shift, finally returning to amplifying gold’s upside. Silver is not only radically undervalued relative to gold, but investors are aggressively buying. Silver’s upside potential is massive. ここ2週シルバーは急騰した、ゴールドを遥かに凌ぐものだ。これは注目すべきことだ、もう何年もシルバーはひどいものだった。この極端に嫌われた金属が大きく心理を買えている、とうとうゴールド上昇を増幅するに至った。シルバーは対ゴールドで極端に過小評価されているだけでなく、投資家は積極的に買い進んでいる。シルバーの潜在上昇力は巨大なものだ。 Silver’s performance in recent years has been brutally bad, repelling all but the most fanatical contrarians. Historically silver prices have been mostly ...

結局、中国は隣国日本で20年前に起きたことを学んでいなかったということでしょう、というかどの国もどの政府も十分成熟するまでは「わかっちゃいるけどやめられない」ということでしょうね、きっと。 Spooked By Apple? Wait ‘Til China’s Bubble Bursts Written by Jesse Colombo | Jan, 3, 2019 Apple stock plunged nearly 10% on Thursday after the company cut its revenue forecast due to slowing iPhone sales in China. Apple’s woes dragged U.S. stock indices lower by more than 2% as fears of a more extensive China-driven slowdown spread. アップルの株価は火曜に約10%下落した、同社が中国でのiPhone売上原則を予想したためだ。アップルの弱さが米国株式指数を2%以上押し下げた、中国主導でさらなる原則が広がるのではという懸念からだ。 From the New York Times : ニューヨークタイムスによると: For years, no matter what was happening elsewhere, global companies bet billions upon billions of dollars that China’s consumers would keep spending money. 長年、他国で何が起きようとも多国籍企業は中国消費は巨額を維持することに賭けてきた。 Now, just when the world economy could use their financial firepower, they are no longer so quick to open their wallets. 今や、世界経済が金融弾薬を用いてももはや彼らの財布を緩めることはできない。 The latest sign of a slowdown in...

多量のオピオイドを米国に送り込み、米国で深刻な麻薬中毒問題を引き起こしています。現代版「阿片戦争」です。あのトヨタ初の女性取締役もオピオイド中毒で逮捕解任されましたよね。 US Is Dependent On China For Almost 80% Of Its Medicine by Tyler Durden Fri, 05/31/2019 - 12:55 Experts are warning that the U.S. has become way too reliant on China for all our medicine , our pain killers, antibiotics, vitamins, aspirin and many cancer treatment medicine. 専門家はこう警告する、米国はすべての医薬品、痛み止め、抗生物質、ビタミン、アスピリン、各種抗がん剤で、中国依存度が高すぎる。 Fox Business reports that according to FDA estimates at least 80 percent of active ingredients found in all of America’s medicine come from abroad, primarily from China . And it’s not just the ingredients, China wants to become the world’s dominant generic drug maker. So far Chinese companies are making generic for everything from high blood pressure to chemotherapy drugs. 90 percent of America’s prescriptions a...

Barrick’s average quarterly production since Q4’16 plunged an astounding 8.6% YoY. The reason Barrick’s management blew $6.5b in stock buying Randgold is they desperately needed more production to mask the precipitous drop in their own. Barrick’s total 2018 production of 4525k ounces was 18.0% below the 5516k it mined only a couple years earlier in 2016. At best adding Randgold just regains those losses. Barrickの平均四半期生産は2016Q4以来なんとYoYで8.6%下落している。Barrickの取締役が$6.5Bも投じてRandgoldの株式を購入した理由は、彼らはなんとしても急落する自らの生産量を隠すために生産量増加としたかったからだ。Barrickの2018全生産量は4525Kオンスで、わずか2年前の5516kオンスから18.0%も少ない。Randgoldを買収したところでこの下落を補うに過ぎない。 And GOLD has been suffering the same production struggles as ABX. Over its past 4 reported quarters, Randgold’s gold mined has fallen an average of 7.4% YoY. Can bringing two rapidly-depleting major gold miners together magically make a stronger one? I doubt it. Barrick’s reported production will enjoy a big temporary boost...

S&P Surges To Key Technical Level - Now What? by Tyler Durden Tue, 02/12/2019 - 12:03 Having failed twice last week, the S&P 500 is once again testing its 200DMA as hopes of a border/shutdown deal, a lack of collusion, China trade dreams, and an easy Fed are prompting stocks to new post-Xmas dip highs... 先週二回失敗し、S&P500がまたもや200日移動平均に挑戦している、国境の壁/政府閉鎖問題解決、ロシア疑惑解消、中国貿易改善そしてFEDのハト派姿勢、これらがクリスマス下落後の高値を推進している・・・ The S&P 500 is at its highest since Dec 4th... S&P500は12月4日以来の高値だ・・・ What happens next? では次はどうなる? Earnings recession? Meh, don't worry about it... 収益による景気後退? 別に心配することではない・・・・ Oh and don't worry - Fed Chair Powell just told everyone that he "doe...