In

at least one important way, President Trump's decision to browbeat the

Fed into pausing its program of interest-rate hikes is paying off bigly

for America's most vulnerable corporate borrowers.

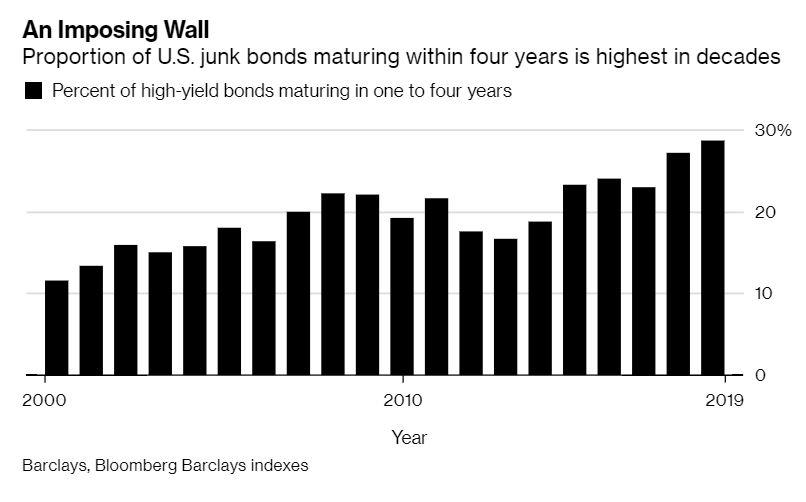

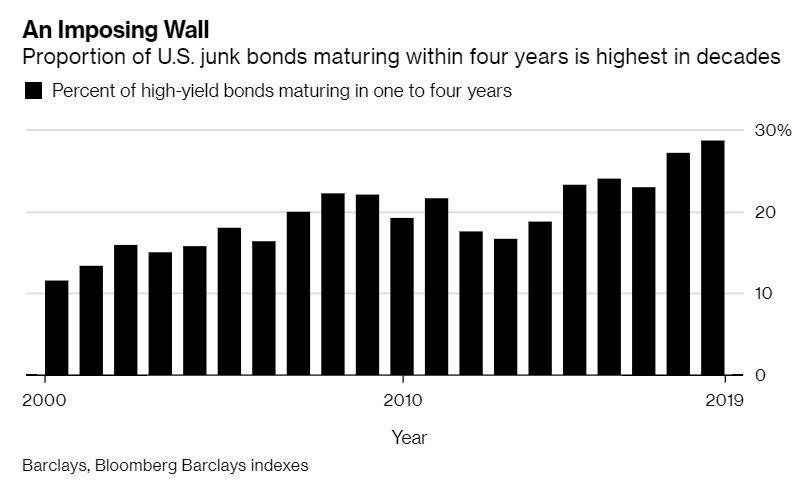

The Fed's decision to 'pause' interest rate hikes comes as nearly

one-third of the entire $1.2 trillion US high-yield market is slated for

maturity over the next four years. That's a record proportion,

according to a team of strategists at Barclays led by Bradley Rogoff,

and compares with a post-2000 average of just 20%. And after the

historic market 'freeze' late last year where not a single high-yield

bond was issued, corporate America has apparently got the message: Now

is the time to strike while the iron is hot. The more speculative-grade the rating, the more important it is for companies to act now to refinance that debt. $1.2Tにもなる米国高金利債権の1/3が今後4年で満期を迎えようとするなかで、FEDが金利引き上げを「中断」することを決めた。Bradley RogoffをリーダーとするBarclaysのストラテジストによると、この割合はとても大きなもので、比較として示すと、2000以降での平均満期割合はわずか20%にすぎなかった。そして昨年遅くに歴史的なこの市場の「凍結」が生じ、まったく高金利債権は発行されなかった、米国全体が明らかにこういうメッセージを発している:今こそ、鉄は熱いうちに打て、ということだ。周囲で投機的企業格付が増えるほどに、多くの企業にとってはいまいそいで債務の借り換えをすることがさらに大切になる。

Though many companies have years to plan on refinancing (almost none

will pay off their debt tabs entirely), many are choosing to refinance

now, while rates are low, and demand for higher-yielding debt is high.

Junk bonds tanked last week as markets shunned risky assets, but this

didn't dampen buyers' appetite: Last week was the biggest week for

issuance in nearly two years, with junk issuers selling $12 billion. So

far this year, more than $80 billion of bonds that listed refinancing in

the prospectus have been issued. That has accounted for more than 70%

of the issuance so far this year, according to Bloomberg.

And while credit analysts at some of the bigger fund managers insist

that this is 'healthy', they seem to have neglected the fact that the

president has effectively given corporations a green light to continue

on their debt binge by effectively putting off their day of reckoning

until the Democrats take back control of the White House.

"Companies are extending maturities out, and that’s healthy," said

Scott Roberts, head of high-yield debt at Invesco Ltd. Refinancing is a

better use of debt than buying back shares, he added. "I’ve seen frothy

before and this is not it."

"I feel good about this high-yield market and we are trying to push issuers to take advantage of it,"

said Richard Zogheb, global head of debt capital markets at Citigroup

Inc. "Investors are so excited now that the underlying rate environment

is more dovish, and that’s really good news for high-yield borrowers."

Companies that backed out of their issuance plans late last year

during the sudden market drought are beginning to realize that 'market

conditions' probably aren't going to get much better than they are now.

"We had half a dozen companies that were planning to go as early as

nine or 10 months ago, then the market started weakening and we never

got to the point where we could do those deals," said John Gregory, head

of leveraged-finance syndicate at Wells Fargo & Co., referring to

when junk bond prices fell late last year. "Now we’re finally getting to that point."

What's more, floating-rate leveraged loans have become less

attractive thanks to the Fed's capitulation, creating something of a

perfect storm for the junk-bond market, which is great for heavily

indebted companies hoping to lock in the lowest possible interest rate. 更に言うと、変動金利レバレッジドローンはそれほど魅力的にならなくなった、FEDが罠に陥ったためだ、これがジャンクボンド市場に何らかの嵐を引き起こしつつある、債務過多の企業にとって最低金利を得ることを期待している。

"I can’t remember when $5 billion worth of deals came in one day," said Matt Eagan, a portfolio manager at Loomis Sayles & Co.

"The market is generally wide open for issuers," said Jenny Lee,

co-head of leveraged loan and high-yield capital markets at JPMorgan

Chase & Co. "We’re advising issuer clients to look harder at doing

high-yield bonds."

Even if borrowers truly can't afford it, the longer they can delay

their day of reckoning, the greater the chance that the Fed takes care

of their obligations for them when the central bank inevitably pivots to

buying corporate debt - as former Fed Chairwoman Janet Yellen recently

suggested - during QE4.

Amazonで買物をしてContrarianJを応援しよう Albert Edwards: This Was The Final Recessionary Shoe, And It Has Now Fallen by Tyler Durden Thu, 06/27/2019 - 12:45 Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007... ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・ ... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions. ・・・市場は準混乱状態になった、というのも歴史的に見てイールドカーブ反転が過去7回の景気後退の前兆となっているからだ。 However, while the inversion was certainly a memorable event, the question on everyone's lips is how do risk assets perform once the curve flattens and/or inverts. According to backtests from Goldman, since the mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. ...

China Injects Gargantuan 1.1 Trillion In Liquidity This Week by Tyler Durden Wed, 01/16/2019 - 22:19 Following what Bloomberg calculated was a record net reverse repo liquidity injection on Wednesday, when the PBOC injected a whopping 560 billion yuan of liquidity into the financial system via open market operations, the Chinese central bank has done it again and in Thursday's open market operation, it sold 250BN yuan in 7 Day repos (slightly below yesterday's record 350BN), and 150BN in 28 Day repos, which net of maturities resulted in a whopping net 380BN yuan ($56.2BN) liquidity injection. ブルームバーグの算出によると水曜に記録的なリバースレポ流動性注入が行われた、PBOCがなんと公開市場操作で金融システムになんと560B人民元を注入した、中国中央銀行は再び木曜に公開市場操作を行った、250B人民元の7日決済レポを売却した(昨日の350B人民元よりも少し少ない)、そして28日決済のレポを150B人民元注入した、結果としてなんと380B人民元($56.2B)の流動性注入となる。 (訳注:なんか足し算すると辻褄が合いません、ブルーム...

"Clueless Wizards" - Don't Worry, The Fed Has "Belts & Suspenders" by Tyler Durden Tue, 05/26/2020 - 12:25 Authored by Mike Shedlock via MishTalk, The Fed's balance sheet is approaching $7 trillion dollars. This is what Bernanke meant by suspenders. FEDのバランスシートは$7Tに迫っている。これこそBernankeがサスペンダーにたとえたものだ。 On February 27, 2013, Ben Bernanke spoke to US Congress about how the Fed would unwind its balance sheet. 2013年2月27日に、Ben Bernankeは米国議会証言でFEDが如何にバランスシート巻き戻しをするかの証言を行った。 Bernanke said, We Have “Belts, Suspenders” to Unwind Balance Sheet . Bernankeが言うには、我々はバランスシート巻き戻しのための「ベルトもサスペンダー」も有るという。 Bernanke’s vague answer to Sen. Richard Shelby, R-AL, when asked how the Fed will deleverage the balance sheet, was this: “ In terms of e...