With

the trade war between the US and China re-escalating once more,

investors are again casting frightened glances at declining global trade

volumes, which as Bloomberg writes today, "threaten to upend the global

economy’s much-anticipated rebound and could even throw its decade-long

expansion into doubt if the conflict spirals out of control."

"Just as tentative signs appeared that a recovery is taking hold,

trade tensions have re-emerged as a credible and significant threat to

the business cycle," said Morgan Stanley's chief economist, Chetan Ahya,

highlighting a “serious impact on corporate confidence" from the tariff

feud.

To be sure, even before the latest trade war round, global growth and trade were already suffering,

confirmed most recently by last night's dismal China economic data,

which showed industrial output, retail sales and investment all sliding

in April by more than economists forecast.

A similar deterioration was observed in the US, where retail sales

unexpectedly declined in April while factory production fell for the

third time in four months. Meanwhile, over in Europe even though

Germany’s economy emerged from stagnation to grow by 0.4% in the first

quarter, "the outlook remains fragile amid a manufacturing slump that

will be challenged anew by the trade war." As a result, investor

confidence in Europe’s largest economy unexpectedly weakened this month

for the first time since October.

Framing the threat, a study by Bloomberg Economics calculated that

about 1% of global economic activity is at stake in goods and services

traded between the US and China. Almost 4% of Chinese output is exported

to the U.S. and any hit to its manufacturers would reverberate through

regional supply chains with Taiwan and South Korea among those at risk.

U.S. shipments to China are more limited, though 5.1% of its

agricultural production heads there as does 3.3% of its manufactured

goods.

米国から中国への出荷がさらに制限されており、農業生産の5.1%、製造業の3.3%は中国向けだ。

The macro fears are once again trickling down to the micro level, and

last week chip giant Intel tumbled after it guided to a "more cautious

view of the year," and Italian drinks maker Davide Campari-Milano SpA

this month noted the “uncertain geopolitical and macro economic

environment.”

“The world economy has been in a significant slowdown for a period,’’

said James Bevan, chief investment officer at CCLA Investment

Management. “People just have to wake up and look at the trade data.’’

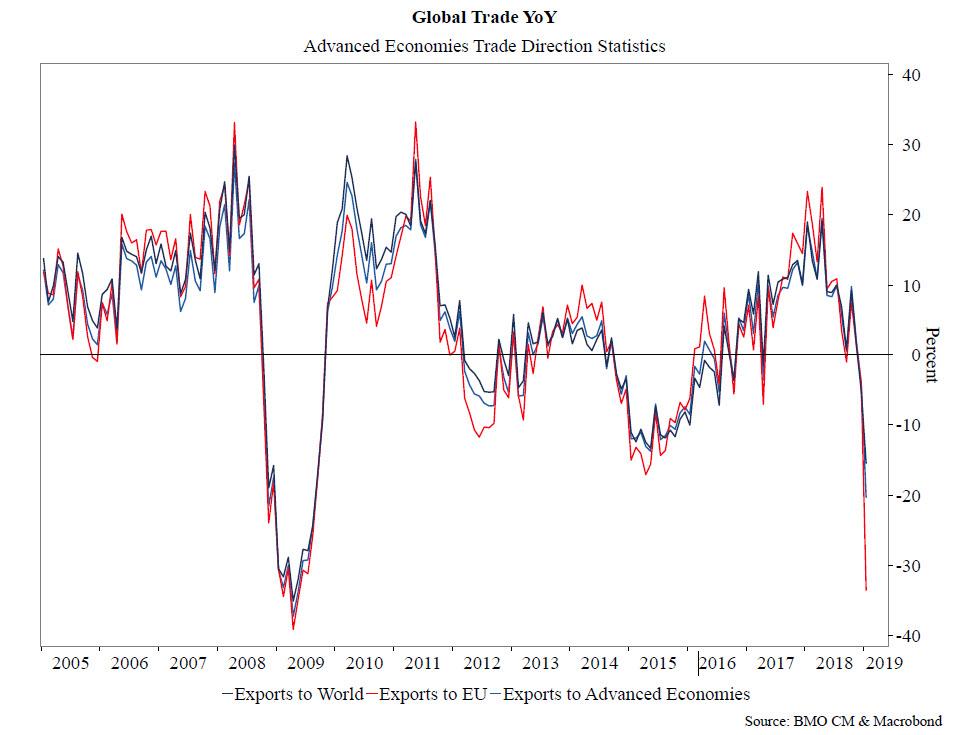

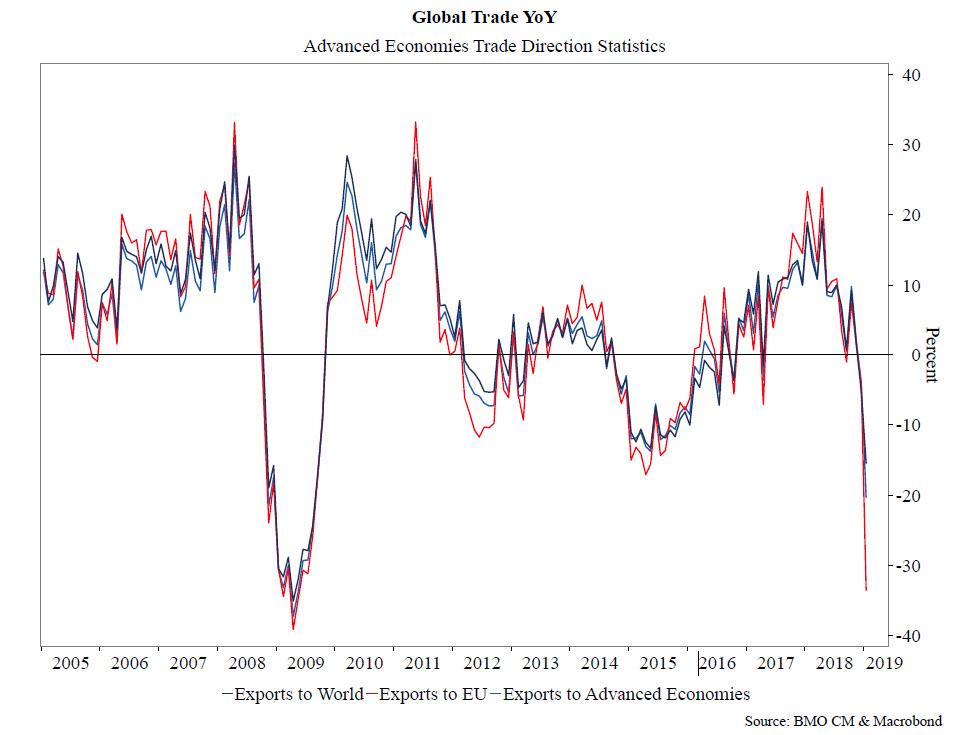

But the best way to visualize just how serious the threat to global

flow of trade, and the world economy in general, below is a chart on the

year-over-year changes in global trade as measured by the IMF's

Direction of Trade Statistics, courtesy of BMO's Ian Lyngern. It shows

the absolutely collapse in global exports as broken down into three

categories:

そこで世界貿易や世界経済がどれほど深刻であるかを目の当たりにする方法は、下のチャートのYoY世界貿易変化を見ることだ、IMFのDirection of Trade Sataisticsが発表したデータだ、BMOの Ian Lyngernが提供してくれた。これを見ると世界輸出が急落しており、その内訳を3分類している:

Exports to the world (weakest since 2009),

Exports to advances economies (also lowest since 2009), and

Exports to the European Union (challenging 2009 lows).

In short, even before the latest round of trade escalation,

global trade had tumbled to levels last seen during the financial crisis

depression. One can only wonder what happens to global trade after the

latest escalation in US-China trade war...

簡単に言うと、直近の貿易係争の高まり前に、すでに世界貿易は急落しており、前回の金融危機恐慌レベルにまで下落している。直近の米中貿易戦争の加熱を見ると世界貿易がどうなるかを誰でも心配するだろう・・・

Commenting on the chart above, Lyngen writs that "as estimates of the

fallout from the renewed Trade War begin to reflect the growing

apprehension in a variety of markets, we're struck by the extent of the

drop in exports."

On Wednesday, markets were clearly not struck by the drop in exports,

or any other negative news for that matter, with the Dow ripping,

reversing its entire morning drop, and trading over 100 points in the

green at last check.

Amazonで買物をしてContrarianJを応援しよう Silver Outperforming Gold 2 Adam Hamilton July 26, 2019 3232 Words Silver has blasted higher in the last couple weeks, far outperforming gold. This is certainly noteworthy, as silver has stunk up the precious-metals joint for years. This deeply-out-of-favor metal may be embarking on a sea-change sentiment shift, finally returning to amplifying gold’s upside. Silver is not only radically undervalued relative to gold, but investors are aggressively buying. Silver’s upside potential is massive. ここ2週シルバーは急騰した、ゴールドを遥かに凌ぐものだ。これは注目すべきことだ、もう何年もシルバーはひどいものだった。この極端に嫌われた金属が大きく心理を買えている、とうとうゴールド上昇を増幅するに至った。シルバーは対ゴールドで極端に過小評価されているだけでなく、投資家は積極的に買い進んでいる。シルバーの潜在上昇力は巨大なものだ。 Silver’s performance in recent years has been brutally bad, repelling all but the most fanatical contrarians. Historically silver prices have been mostly ...

結局、中国は隣国日本で20年前に起きたことを学んでいなかったということでしょう、というかどの国もどの政府も十分成熟するまでは「わかっちゃいるけどやめられない」ということでしょうね、きっと。 Spooked By Apple? Wait ‘Til China’s Bubble Bursts Written by Jesse Colombo | Jan, 3, 2019 Apple stock plunged nearly 10% on Thursday after the company cut its revenue forecast due to slowing iPhone sales in China. Apple’s woes dragged U.S. stock indices lower by more than 2% as fears of a more extensive China-driven slowdown spread. アップルの株価は火曜に約10%下落した、同社が中国でのiPhone売上原則を予想したためだ。アップルの弱さが米国株式指数を2%以上押し下げた、中国主導でさらなる原則が広がるのではという懸念からだ。 From the New York Times : ニューヨークタイムスによると: For years, no matter what was happening elsewhere, global companies bet billions upon billions of dollars that China’s consumers would keep spending money. 長年、他国で何が起きようとも多国籍企業は中国消費は巨額を維持することに賭けてきた。 Now, just when the world economy could use their financial firepower, they are no longer so quick to open their wallets. 今や、世界経済が金融弾薬を用いてももはや彼らの財布を緩めることはできない。 The latest sign of a slowdown in...

多量のオピオイドを米国に送り込み、米国で深刻な麻薬中毒問題を引き起こしています。現代版「阿片戦争」です。あのトヨタ初の女性取締役もオピオイド中毒で逮捕解任されましたよね。 US Is Dependent On China For Almost 80% Of Its Medicine by Tyler Durden Fri, 05/31/2019 - 12:55 Experts are warning that the U.S. has become way too reliant on China for all our medicine , our pain killers, antibiotics, vitamins, aspirin and many cancer treatment medicine. 専門家はこう警告する、米国はすべての医薬品、痛み止め、抗生物質、ビタミン、アスピリン、各種抗がん剤で、中国依存度が高すぎる。 Fox Business reports that according to FDA estimates at least 80 percent of active ingredients found in all of America’s medicine come from abroad, primarily from China . And it’s not just the ingredients, China wants to become the world’s dominant generic drug maker. So far Chinese companies are making generic for everything from high blood pressure to chemotherapy drugs. 90 percent of America’s prescriptions a...

Barrick’s average quarterly production since Q4’16 plunged an astounding 8.6% YoY. The reason Barrick’s management blew $6.5b in stock buying Randgold is they desperately needed more production to mask the precipitous drop in their own. Barrick’s total 2018 production of 4525k ounces was 18.0% below the 5516k it mined only a couple years earlier in 2016. At best adding Randgold just regains those losses. Barrickの平均四半期生産は2016Q4以来なんとYoYで8.6%下落している。Barrickの取締役が$6.5Bも投じてRandgoldの株式を購入した理由は、彼らはなんとしても急落する自らの生産量を隠すために生産量増加としたかったからだ。Barrickの2018全生産量は4525Kオンスで、わずか2年前の5516kオンスから18.0%も少ない。Randgoldを買収したところでこの下落を補うに過ぎない。 And GOLD has been suffering the same production struggles as ABX. Over its past 4 reported quarters, Randgold’s gold mined has fallen an average of 7.4% YoY. Can bringing two rapidly-depleting major gold miners together magically make a stronger one? I doubt it. Barrick’s reported production will enjoy a big temporary boost...

S&P Surges To Key Technical Level - Now What? by Tyler Durden Tue, 02/12/2019 - 12:03 Having failed twice last week, the S&P 500 is once again testing its 200DMA as hopes of a border/shutdown deal, a lack of collusion, China trade dreams, and an easy Fed are prompting stocks to new post-Xmas dip highs... 先週二回失敗し、S&P500がまたもや200日移動平均に挑戦している、国境の壁/政府閉鎖問題解決、ロシア疑惑解消、中国貿易改善そしてFEDのハト派姿勢、これらがクリスマス下落後の高値を推進している・・・ The S&P 500 is at its highest since Dec 4th... S&P500は12月4日以来の高値だ・・・ What happens next? では次はどうなる? Earnings recession? Meh, don't worry about it... 収益による景気後退? 別に心配することではない・・・・ Oh and don't worry - Fed Chair Powell just told everyone that he "doe...