Since the post-financial

crisis era began more than a decade ago, record low-interest rates and the

Fed’s acquisition of $4 trillion of the highest quality fixed-income assets has

led investors to scratch and claw for any asset, regardless of quality,

offering returns above the rate of inflation.

Financial media

articles and Wall Street research discussing this dynamic are a dime-a-dozen.

What we have not heard a peep about, however, are the inherent risks within the

corporate bond market that have blossomed due to the way many corporate debt

investors are managed and their somewhat unique strategies, objectives, and legal

guidelines.

This article

offers insight and another justification for moving up in credit within the

corporate bond market. For our prior recommendation to sell junk debt based on

yields, spreads, and the economic cycle, we suggest reading our subscriber-only

article Time To Recycle Your Junk. If

you would like access to that article and many others, you can sign up for RIA Pro and

enjoy all the site has to offer with a 30-day free trial period.

By and large,

equity investors do not have guidelines regulating whether or not they can buy companies

based on the strength or weakness of their balance sheets and income statements.

Corporate bond investors, on the other hand, are typically handcuffed with legal

and/or self-imposed limits based on credit quality. For instance, most bond

funds and ETFs are classified and regulated accordingly by the SEC as

investment grade (rated BBB- or higher) or as high yield (rated BB+ or lower). Most

other institutions, including endowments and pension funds, are limited by

bylaws and other self-imposed mandates. The large majority of corporate bond

investors solely traffic in investment grade, however, there is a contingency

of high-yield investors such as certain mutual funds, ETFs (HYG/JNK), and other

specialty funds.

Often

overlooked, the bifurcation of investor limits and objectives makes an analysis

of the corporate bond market different than that of the equity markets. The

differences can be especially interesting if a large number of securities

traverse the well-defined BBB-/BB+ “Maginot” line, a metaphor for expensive

efforts offering a false line of security.

The U.S. corporate

bond market is approximately $6.4 trillion in size. Of that, over 80% is currently

rated investment grade and 20% is junk-rated.This number does not include bank loans, derivatives, or other

forms of debt on corporate balance sheets.

Since 2000,

the corporate bond market has changed drastically in size and, importantly, in credit

composition. Over this period, the corporate bond market has grown by 378%,

greatly outstripping the 111% growth of GDP.

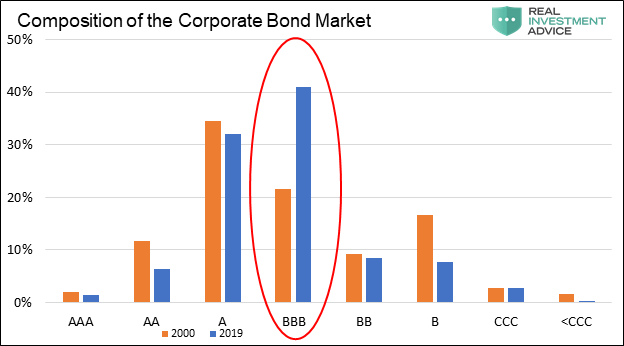

The bar chart below shows how the credit composition of the corporate

bond market shifted markedly with the surge in debt outstanding.

As circled,

the amount of corporate bonds currently rated BBB represents over 40% of corporate

bonds outstanding, doubling its share since 2000. Every other rating category constitutes

less of a share than it did in 2000. Over that time period, the size of the BBB

rated sector has grown from $294 billion to $2.61 trillion or 787%.

To recap, there

is a large proportion of investment grade investors piled into securities that are

rated BBB and one small step away from being downgraded to junk status. Making

this situation daunting, many investment grade investors are not allowed to

hold junk-rated securities. If only 25% of the BBB-rated bonds were downgraded

to junk, the size of the junk sector would increase by $650 billion or by over

50%. Here are some questions to ponder in the event downgrades on a

considerable scale occur to BBB-rated corporate bonds:

If

a recession causes BBB to BB downgrades, as is typical, will junk investors

retain their current holdings, let alone buy the new debt that has entered

their investment arena?

Will

retail investors that are holding the popular junk ETFs (HYG and JNK) and not

expecting large losses from a fixed income investment, continue to hold these

ETFs?

Will

forced selling from ETF’s, funds, and other investment grade holders result in

a market that essentially temporarily shuts down similar to the sub-prime

market in 2008?

We pose

those questions to help you appreciate the potential for a liquidity issue,

even a bond market crisis, if enough BBB paper is downgraded. If such an event were

to occur, we have no doubt someone would eventually buy the newly rated junk

paper. What concerns us is, at what

price will buyers step up? 私どもはこういう疑念を示し皆さんに潜在的な流動性の問題として捉えてほしい、BBB債権の多くが格下げとなると債券市場でも流動性問題が顕在化する。こういう状況になっても、疑いなくやがて誰かが新規格下げ債権を買うことだろう。ただし、我々の懸念は、どの価格で買い手が現れるかということだ。

Implied Risk 積み上がるリスク

Given that downgrades are a real and present danger and there is real

potential for a massive imbalance between the number of buyers and

sellers of junk debt, we need to consider how close we may be to such an

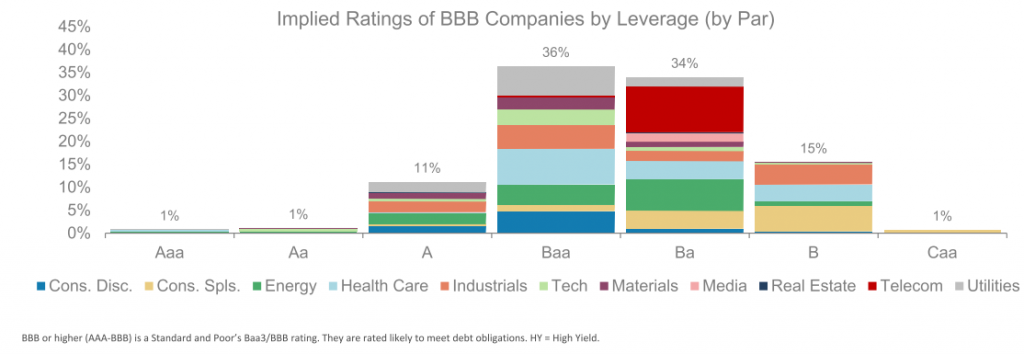

event. To provide perspective, we present a graph courtesy of Jeff

Gundlach of DoubleLine.

The graph shows

the implied ratings of all BBB companies based solely on the amount of leverage

employed on their respective balance sheets. Bear in mind, the rating agencies

use several metrics and not just leverage. The graph shows that 50% of BBB companies,

based solely on leverage, are at levels typically associated with lower rated

companies.

If 50% of

BBB-rated bonds were to get downgraded, it would entail a shift of $1.30

trillion bonds to junk status. To put

that into perspective, the entire junk market today is less than $1.25 trillion,

and the subprime mortgage market that caused so many problems in 2008 peaked at

$1.30 trillion. Keep in mind, the subprime mortgage crisis and the ensuing

financial crisis was sparked by investor concerns about defaults and resulting

losses.

As mentioned,

if only a quarter or even less of this amount were downgraded we would still

harbor grave concerns for corporate bond prices, as the supply could not easily

be absorbed by traditional buyers of junk.

Investors

should stay ahead of what might be a large event in the corporate bond market.

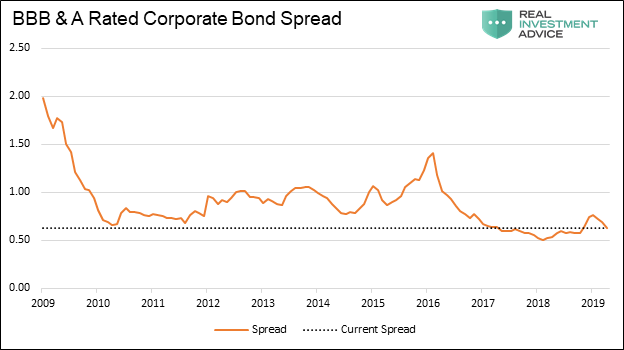

We recommend corporate bond investors focus on A-rated or solid BBB’s that are less

likely to be downgraded. If investment grade investors are forced to sell, they

will need to find replacement bonds which should help the performance of better

rated corporate paper. What makes this recommendation particularly easy is the

fact that the current yield spread between BBB and A-rated bonds are so tight. The

opportunity cost of being wrong is minimal. At the same time, the benefits of

avoiding major losses are large.

With the current

spread between BBB and A-rated corporate bonds near the tightest level since

the Financial Crisis, the yield “give up” for moving up in credit to A or

AA-rated bonds is a low price to pay given the risks. Simply, the market is begging

you not to be a BBB hero.

Data Courtesy St. Louis Federal

Reserve Summary 要約

The most

important yet often overlooked aspect of investing is properly recognizing and

quantifying the risk and reward of an investment. At times such as today, the

imbalance between risk and reward is daunting, and the risks and/or

opportunities beg for action to be taken.

We believe

investors are being presented with a window to sidestep risk while giving up

little to do so. If a great number of BBB-rated corporate bonds are downgraded,

it is highly likely the prices of junk debt will plummet as supply will

initially dwarf demand. It is in these

types of events, as we saw in the sub-prime mortgage market ten years ago, that

investors who wisely step aside can both protect themselves against losses and

set themselves up to invest in generational value opportunities. 私どもはこう信じている、投資家にとってリスクを回避する余地は十分にある、一方でそれを諦めることはない。もしBBB格付け債権の多くが格下げとなると、ジャンクボンドの価格は急落するだろう、当初供給が需要を圧倒するからだ。こういう出来事を、我々は10年前にサブプライム住宅再建で目の当たりにした、懸命にも回避した投資家は自らの資産を損失から守るだけでなく人生で一度の投資機会を得ることもできる。

While the

topic for another article, a large reason for the increase in corporate debt is

companies’ willingness to increase leverage to buy back stock and pay larger

dividends. Investors desperate for “safer but higher yielding” assets are more

than willing to fund them. Just as the French were guilty of a false confidence

in their Maginot Line to prevent a German invasion, current investors gain

little at great expense by owning BBB-rated corporate bonds.

The

punchline that will be sprung upon these investors is that the increase of debt,

in many cases, was not widely used for productive measures which could have

strengthened future earnings making the debt easier to pay off. Instead, the

debt has weakened a great number of companies.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for Clarity Financial, LLC. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research. Follow Michael on Twitter or go to 720global.com for more research and analysis.

Amazonで買物をしてContrarianJを応援しよう Silver Outperforming Gold 2 Adam Hamilton July 26, 2019 3232 Words Silver has blasted higher in the last couple weeks, far outperforming gold. This is certainly noteworthy, as silver has stunk up the precious-metals joint for years. This deeply-out-of-favor metal may be embarking on a sea-change sentiment shift, finally returning to amplifying gold’s upside. Silver is not only radically undervalued relative to gold, but investors are aggressively buying. Silver’s upside potential is massive. ここ2週シルバーは急騰した、ゴールドを遥かに凌ぐものだ。これは注目すべきことだ、もう何年もシルバーはひどいものだった。この極端に嫌われた金属が大きく心理を買えている、とうとうゴールド上昇を増幅するに至った。シルバーは対ゴールドで極端に過小評価されているだけでなく、投資家は積極的に買い進んでいる。シルバーの潜在上昇力は巨大なものだ。 Silver’s performance in recent years has been brutally bad, repelling all but the most fanatical contrarians. Historically silver prices have been mostly ...

結局、中国は隣国日本で20年前に起きたことを学んでいなかったということでしょう、というかどの国もどの政府も十分成熟するまでは「わかっちゃいるけどやめられない」ということでしょうね、きっと。 Spooked By Apple? Wait ‘Til China’s Bubble Bursts Written by Jesse Colombo | Jan, 3, 2019 Apple stock plunged nearly 10% on Thursday after the company cut its revenue forecast due to slowing iPhone sales in China. Apple’s woes dragged U.S. stock indices lower by more than 2% as fears of a more extensive China-driven slowdown spread. アップルの株価は火曜に約10%下落した、同社が中国でのiPhone売上原則を予想したためだ。アップルの弱さが米国株式指数を2%以上押し下げた、中国主導でさらなる原則が広がるのではという懸念からだ。 From the New York Times : ニューヨークタイムスによると: For years, no matter what was happening elsewhere, global companies bet billions upon billions of dollars that China’s consumers would keep spending money. 長年、他国で何が起きようとも多国籍企業は中国消費は巨額を維持することに賭けてきた。 Now, just when the world economy could use their financial firepower, they are no longer so quick to open their wallets. 今や、世界経済が金融弾薬を用いてももはや彼らの財布を緩めることはできない。 The latest sign of a slowdown in...

Gold Stocks Surge Higher Adam Hamilton February 22, 2019 2932 Words The gold miners’ stocks surged strongly this week, blasting to new upleg highs. The mounting gains are naturally driving more interest in this small contrarian sector, shifting sentiment towards bullish. Despite their accelerating rally, gold stocks still remain fairly low technically and deeply undervalued relative to gold. So their strengthening upleg likely has plenty of room to run considerably higher in coming months. 今週金鉱株は力強く上昇し新高値となった。上昇が積み上がりこの小さなコントラリアンセクターはさらに注目を集めている、これが心理を強気なものにする。ラリーが加速するが、金鉱株はテクニカル的にはまだ安値で、対ゴールドでとても過小評価されている。というわけで力強い上昇は今後数ヶ月まだかなりな上昇余地がある。 The gold miners’ stocks are ultimately leveraged plays on gold, which overwhelmingly drives their profits. The much-maligned yellow metal has enjoyed a strong upleg since mid-August, when record gold-futures s...

Amazonで買物をしてContrarianJを応援しよう Junk Bond Bubble In Pictures: Deflation Up Next by Tyler Durden Fri, 07/19/2019 - 14:37 Authored by Mike Shedlock via MishTalk, The widely discussed "everything bubble" is, in reality, a corporate junk bond bubble on steroids sponsored by the Fed ... 幅広く議論されている「everything bubble」は実際に企業ジャンク・ボンドバブルにも言えることであり、これはFEDによりドーピング注入されている・・・ The highest grade AAA corporate bonds yield 2.75%. BBB-rated corporate bonds, just one step above junk, 3.5%. BB-rated bonds yield just 4.28%. 最高級ランクAAA企業債権の金利は2.75%だ。あとひとランク悪化でジャンク・ボンド入りするBBB債権金利は3.5%。BB格付け債権の金利でもわずか4.28%でしかない。 Corporate Bond Spreads 企業債権金利のスプレッド The spread between Prime AAA bonds and lower-medium grade bonds (see chart below) is just 0.77 percentage points. 最上位AAA債権と低中ランク債権のスプレッドがわずか0.77%しかない。 The spre...

最後の2段落だけ訳をいれておきました。 Fed’s Risky QE4 Stock Ramp Adam Hamilton January 31, 2020 3567 Words The US stock markets dramatically surged mostly in a straight line since mid-October. This extraordinary rally started when the Federal Reserve announced it would resume expanding its balance sheet for the first time in years. The deluge of new liquidity from that quantitative-easing bond buying has again acted like rocket fuel for stock markets. After shooting vertically they are in real trouble when the Fed pulls back. In early October the flagship US S&P 500 stock index (SPX) slumped to 2888. That was a mild 4.6% pullback from late July’s latest record high. The SPX was still having a great year though, up 15.2% year-to-date at that point thanks to extreme Fed easing . After the SPX had plunged 19.8% mostly in Q4’18 in a severe near-bear cor...