First it was Baoshang Bank , then it was Bank of Jinzhou, then, two months ago, China's Heng Feng Bank with

1.4 trillion yuan in assets, quietly failed and was just as quietly

nationalized. Today, a fourth prominent Chinese bank was on the verge of

collapse under the weight of its bad loans, only this time the failure

was far less quiet, as depositors of the rural lender swarmed the bank's

retail outlets, demanding their money in an angry demonstration of what

Beijing is terrified of the most: a bank run. 最初はBaoshang Bankだった、次はBank of Jinzhou,そしてその二か月後1.4T人民元の資産規模となる中国のHeng Feng Bankが密かに倒産し密かに国有化された。今日、4番めの著名な中国銀行が倒産の極みにいる、多額の不良債権のためだ、今回の破綻はこれまでほど物静かではない、当地の預金者たちが窓口に殺到したのだ、北京政府が最も恐れていることで預金者が自らの預金を引き出そうと怒りのデモンストレーションをおこなった:取り付け騒ぎだ。

Local business leaders, political cadres and banking executives

rallied Thursday at the main branch of Henan Yichuan Rural Commercial

Bank, just outside the central Chinese city of Luoyang, where they stood

one by one before a microphone to pledge their backing for the bank, as

smiling employees brandished wads of cash before television cameras to

demonstrate just how much cash, literally, the bank had.

It was China's latest, and most desperate attempt yet to project

stability and reassure the public that all is well after rumors spread

that the bank’s chairman was in trouble and the bank was on the brink of

insolvency. However, as the WSJ reports,

it wasn’t enough for 31-year-old Li Xue, who showed up for the third

day Thursday to withdraw thousands of yuan of her mother’s life savings

after hearing from fellow villagers that Yichuan Bank - which is the

largest lender in Yichuan county by the number of branches and capital,

and it is also a member of PBOC’s deposit insurance system, according to

the local government - was going under.

Just like any self-respecting Ponzi scheme, the bank's branch

managers tried to persuade her to keep her money with them until March,

when her mother’s three-year deposits would mature, yielding more than

10,000 yuan in interest. And then, just like any Ponzi scheme, to

sweeten the offer, the bank managers also offered her even

higher-yielding products, plus supermarket gift cards, just to keep her

money there..

"Our bank is state-backed, and your money is insured by deposit insurance," one female manager told her, but Ms. Li refused, her confidence in the state's lies crushed.

“We really can’t afford to lose the money,” she said.

「私達は本当にそのお金をなくすことはできないのです」と彼女は訴えた。

The bank run at Yichuan Bank, located in China's landlocked province

of Henan, makes it at least the fourth bank that authorities have rushed

to rescue this year. It won't be the last.

As we have documented previously,

in recent month China’s banking sector has been dogged by a sudden

surge in liquidity concerns, particularly among smaller regional banks

that had expanded aggressively in recent years, and were now suffering a

surge in bad loans, threatening their viability.

In May, regulators bailed out Baoshang Bank,

in the country’s first bank bailout since the 1990s. That move led to

widespread concerns about the health of other small lenders and

financial institutions, squeezing liquidity in China’s interbank market.

It also led to similar failures - and rescues - of Bank of Jinzhou and Heng Feng Bank,

both smallish regional banks, yet big enough to convince the local

population that something was very rotten with China's financial system.

5月には、監督当局がBaoshang Bank を救済した、1990年以来初めてとなる銀行救済だった。この出来事で他の小規模銀行、金融機関の健全性に懸念が持たれるようになり、中国のインターバンク市場の流動性を押し込めた。同様の破綻と救済が行われた、Bank of Jinzhou とHeng Feng Bankだ、どちらも小規模地方銀行だが、当地の人にとって中国の金融システムが腐っていることを確信させるには十分だった。

Prudently, Beijing has been careful not to announce any takeovers,

although it has quietly brought in state-owned banks and asset

management firms, as well as an arm of the nation’s sovereign-wealth

fund, to inject fresh capital and stabilize wobbly banks, as it did most

recently in the case of Heng Feng.

Try as Beijing might, however, the bailouts have not gone unnoticed,

and culminated in what today has been a three-day bank run at Yichuan

Bank.

Like with everything else in China, there is good and bad news.

The good news is that troubled banks accounted for just 4% of total

assets in China’s banking system, according to a recent estimate by

S&P Global that included poor quality rural institutions flagged by

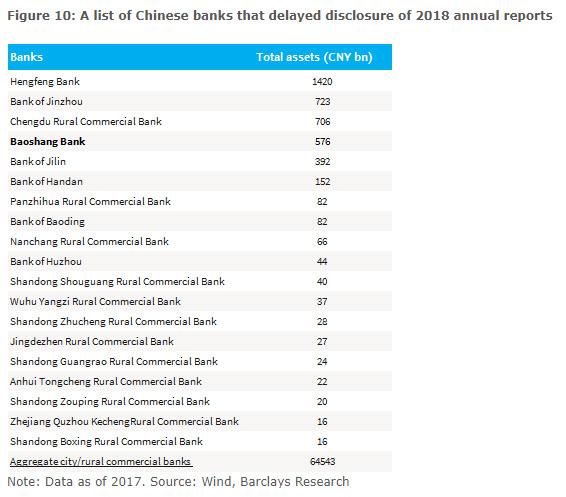

the Chinese central bank. An analysis by Barclays listed those banks

that had delayed to disclose their 2018 annual reports: a clear

indicator of imminent collapse. Three of the top four banks have already

been nationalized or bailed out.

However, in this case size really does not matter, and the aggressive

response from regulators to the developments at Yichuan Bank, a small

lender with just 62.65 billion yuan ($8.9 billion) in assets, underscores

the heightened concerns of contagion and social instability amid the

loss of confidence in bank deposits, as the WSJ notes. しかしながら、ここでは銀行の規模は問題ではない、Yichuan Bankの成り行きに監督当局は積極的に体操しており、わずか$8.9Bの資産規模の小銀行にも積極対応している、これが連鎖して社会不安を引き起こすことをとても懸念している、銀行預金に対する信頼性をだ、とWSJは伝える。

The bad news is that small banks are just the start of a wave that

could eventually topple some of China's biggest SOEs. Yichuan Bank is

emblematic of the thousands of banks and cooperatives in China’s

countryside that in recent years had scaled up its ambitions. In 2009,

the rural cooperative became a commercial lender, attracting deposits

primarily from farmers and county locals, according to the bank. It then

kept growing at a tremendous pace, raking up billions in bad loans,

until one day - like all Ponzi schemes - the new money stopped trickling

in and the bank's day of reckoning had arrived.

While Yichuan Bank has plenty of competition, including large

state-owned banks in nearby Luoyang, an ancient capital of China known, Yichuan

Bank accounted for 71% of deposits and 82% of loans in its county as of

September 2018, according to China Chengxin International Rating

Agency. Yichuan Bankにも多くの競合企業がある、その中には大規模国有銀行もある、洛陽市の近くにだ、中国では著名な古い首都だ、2018年9月時点でYichauna Bankは当地の預金の71%、貸し出しの82%を占めていた、とChina Chengxin Internationa Rating Agencyのデータが示す。

The problem, as hinted above, is that like most other small Chinese

banks, Yichuan Bank suffered from a buildup of bad loans as the economy

slowed in recent years, and struggled to retain deposits amid

intensified competition from its peers.

That was the proverbial Minsky moment when every Ponzi scheme ends.

Then the warnings came: in July, analysts at China Chengxin flagged

the bank for its lack of stable deposits and a rapid buildup of overdue

and bad loans. Bad loans ballooned to 1 billion yuan at the end of 2018,

a 10-fold increase in just three years, according to its financial

statements. Overdue loans, meantime, grew to 28% of its total credit at the end of September 2018, the credit rating agency said. こうして警告が発せられる:6月に中国新華社のアナリストが銀行リストを示した、定常的に預金獲得ができず不良債権を急速に増やしている銀行だ。2018年末には不良債権は1B人民元まで膨れ上がった、わずか3年で10倍増だ、と同社の金融報告書は告げる。2018年9月末には、返済延期ローンが全貸し出しの28%にもなった、と格付会社は言う。

That number, incidentally, is orders of magnitude higher than what

the PBOC discloses as China's average bad loan percentage, which in the

past decade has stubbornly, and erroneously, been stuck in the mid-1%

range. The true number is far, far higher, but Beijing guards it with

its life, as the alternative is a bank run on the world's largest bank

system, which with $40 trillion in assets, is roughly double that of the

US.

So far Beijing has been lucky, in that people tend to be notoriously

bad with numbers. Ironically, what brought the bank down was news of

trouble with Yichuan’s senior management that initially caught locals’

attention. Immediately thereafter, depositors started demanding their

money back earlier this month; as speculation circulated on social media

that the bank was on the verge of insolvency, the crowds at bank

branches grew thicker, and so the bank run began. 北京政府は幸運なことに、これまで人々は数値に疎かった。皮肉なことに、当行悪化を知らしめたのは、Yichauanの上級管理職のせいだ、彼がこの地域で耳目を集めた。その直後の今月始めに、預金者が預金引き出しを求め始めた;当行が支払不能の瀬戸際にあるというソーシャルメディアでの噂が広まったためだ、銀行支店に人が押し寄せ、取り付け騒ぎが始まった。

By Wednesday, the problem - and its media coverage - was too big to

avoid, and local authorities moved swiftly to stabilize the situation.

In typical Chinese fashion, however, instead of fixing the underlying

problem, they blamed the messenger and announced they had detained two

women whom they accused of spreading false rumors; they also brought in

the county’s deputy party secretary to take charge.

And since explaining to the people that China's entire financial

system is one giant house of cards, the authorities needed a scapegoat.

They got it when they announced an investigation into the bank’s former

chairman, citing a violation of discipline, a charge commonly used in

corruption cases.

Meanwhile, having received a few truckloads full of cash, county

authorities tried to ease depositor panic saying they had tens of

billions of yuan in funds available, which the bank had already begun

tapping, according to the bank.

So far this approach has failed to restore confidence, and bank officers, overwhelmed with withdrawal requests, put stacks of cash on display behind bank windows. They

dangled various inducements, "including boxes of tissue, plastic

chairs, tea thermoses and loose leaf tea" according to the WSJ, to

persuade customers to keep their deposits with Yichuan.

And why not: cheap bribes almost worked in Spain in 2012, when the then-insolvent Bankia handed out Spiderman towels in exchange for a €300 deposit.

Surprisingly, it did not work in China, as people continued to show up, adamant about withdrawing their funds; the bank run was accelerating, and nothing officials did could halt, or reverse it. どうしてそんなことをするかというと:2012年のスペインの取り付け騒ぎでは安物のおまけがうまく機能した、そのとき支払不能となったBankiaは€300預金と引き変えにスパイダーマンタオルを渡し、ことを収めた。驚くことに、中国ではうまくゆかなかった、次々と預金者が殺到し、断固として引き出しを求めた;取り付け騒ぎは拡大し、騒ぎを収めることはできなかった。

Zhang Yanting, a 51-year-old farmer, decided after several days of

trying to pull his money out of the bank that he would keep his account

open to collect the few dollars in grain subsidies he receives each year

from the government. But Zhang still wanted most of his 13,000 yuan in deposits back. Zhang Yanting,51歳農家、は数日間預金を引き出そうとしたが、その後政府からの援助金を受け取るために口座をそのままにした。しかしZhangはそれでもみずからの13,000人民元の預金の払い出しを望んでいる。

After hours in line Thursday, the bank cashier handed him a wad of

cash, which he happily stuffed into his bag. Zhang was unmoved by the

promise of gifts, save for a bottle of water that he sipped from while

waiting.

Amazonで買物をしてContrarianJを応援しよう Silver Outperforming Gold 2 Adam Hamilton July 26, 2019 3232 Words Silver has blasted higher in the last couple weeks, far outperforming gold. This is certainly noteworthy, as silver has stunk up the precious-metals joint for years. This deeply-out-of-favor metal may be embarking on a sea-change sentiment shift, finally returning to amplifying gold’s upside. Silver is not only radically undervalued relative to gold, but investors are aggressively buying. Silver’s upside potential is massive. ここ2週シルバーは急騰した、ゴールドを遥かに凌ぐものだ。これは注目すべきことだ、もう何年もシルバーはひどいものだった。この極端に嫌われた金属が大きく心理を買えている、とうとうゴールド上昇を増幅するに至った。シルバーは対ゴールドで極端に過小評価されているだけでなく、投資家は積極的に買い進んでいる。シルバーの潜在上昇力は巨大なものだ。 Silver’s performance in recent years has been brutally bad, repelling all but the most fanatical contrarians. Historically silver prices have been mostly ...

Amazonで買物をしてContrarianJを応援しよう Junk Bond Bubble In Pictures: Deflation Up Next by Tyler Durden Fri, 07/19/2019 - 14:37 Authored by Mike Shedlock via MishTalk, The widely discussed "everything bubble" is, in reality, a corporate junk bond bubble on steroids sponsored by the Fed ... 幅広く議論されている「everything bubble」は実際に企業ジャンク・ボンドバブルにも言えることであり、これはFEDによりドーピング注入されている・・・ The highest grade AAA corporate bonds yield 2.75%. BBB-rated corporate bonds, just one step above junk, 3.5%. BB-rated bonds yield just 4.28%. 最高級ランクAAA企業債権の金利は2.75%だ。あとひとランク悪化でジャンク・ボンド入りするBBB債権金利は3.5%。BB格付け債権の金利でもわずか4.28%でしかない。 Corporate Bond Spreads 企業債権金利のスプレッド The spread between Prime AAA bonds and lower-medium grade bonds (see chart below) is just 0.77 percentage points. 最上位AAA債権と低中ランク債権のスプレッドがわずか0.77%しかない。 The spre...

結局、中国は隣国日本で20年前に起きたことを学んでいなかったということでしょう、というかどの国もどの政府も十分成熟するまでは「わかっちゃいるけどやめられない」ということでしょうね、きっと。 Spooked By Apple? Wait ‘Til China’s Bubble Bursts Written by Jesse Colombo | Jan, 3, 2019 Apple stock plunged nearly 10% on Thursday after the company cut its revenue forecast due to slowing iPhone sales in China. Apple’s woes dragged U.S. stock indices lower by more than 2% as fears of a more extensive China-driven slowdown spread. アップルの株価は火曜に約10%下落した、同社が中国でのiPhone売上原則を予想したためだ。アップルの弱さが米国株式指数を2%以上押し下げた、中国主導でさらなる原則が広がるのではという懸念からだ。 From the New York Times : ニューヨークタイムスによると: For years, no matter what was happening elsewhere, global companies bet billions upon billions of dollars that China’s consumers would keep spending money. 長年、他国で何が起きようとも多国籍企業は中国消費は巨額を維持することに賭けてきた。 Now, just when the world economy could use their financial firepower, they are no longer so quick to open their wallets. 今や、世界経済が金融弾薬を用いてももはや彼らの財布を緩めることはできない。 The latest sign of a slowdown in...

Gold Stocks Surge Higher Adam Hamilton February 22, 2019 2932 Words The gold miners’ stocks surged strongly this week, blasting to new upleg highs. The mounting gains are naturally driving more interest in this small contrarian sector, shifting sentiment towards bullish. Despite their accelerating rally, gold stocks still remain fairly low technically and deeply undervalued relative to gold. So their strengthening upleg likely has plenty of room to run considerably higher in coming months. 今週金鉱株は力強く上昇し新高値となった。上昇が積み上がりこの小さなコントラリアンセクターはさらに注目を集めている、これが心理を強気なものにする。ラリーが加速するが、金鉱株はテクニカル的にはまだ安値で、対ゴールドでとても過小評価されている。というわけで力強い上昇は今後数ヶ月まだかなりな上昇余地がある。 The gold miners’ stocks are ultimately leveraged plays on gold, which overwhelmingly drives their profits. The much-maligned yellow metal has enjoyed a strong upleg since mid-August, when record gold-futures s...

最後の2段落だけ訳をいれておきました。 Fed’s Risky QE4 Stock Ramp Adam Hamilton January 31, 2020 3567 Words The US stock markets dramatically surged mostly in a straight line since mid-October. This extraordinary rally started when the Federal Reserve announced it would resume expanding its balance sheet for the first time in years. The deluge of new liquidity from that quantitative-easing bond buying has again acted like rocket fuel for stock markets. After shooting vertically they are in real trouble when the Fed pulls back. In early October the flagship US S&P 500 stock index (SPX) slumped to 2888. That was a mild 4.6% pullback from late July’s latest record high. The SPX was still having a great year though, up 15.2% year-to-date at that point thanks to extreme Fed easing . After the SPX had plunged 19.8% mostly in Q4’18 in a severe near-bear cor...