あれから2週間で次の取り付け騒ぎ、中国の銀行は「自滅ループ」に陥る

3週前にZeroHedgeは中国Henan Yichuan Rural Commercial Bankについて報告した、洛陽の郊外の銀行だ、これが最新の中国中小銀行でのひどい取り付け騒ぎだった、預金者は長蛇の列を成した、銀行経営が行き詰まるという噂のためだ。この銀行が4行めだった、破綻直前に国有化された銀行だ、Baoshang Bank,Bank of JinzhouそしてHeng Feng Bankに次ぐものだ。

Now yet another Chinese bank has found itself scrambling to prevent a collapse: Yingkou Coastal Bank was forced to stack bundles of yuan notes high behind the counters of its branches earlier this month, as the northeast China lender fought off a run on deposits while onsite government officials battled rumors of a funding crunch.

今度はもう一つの中国の銀行が破綻回避で緊急事態を迎えている:Yigkou Coastal Bank は銀行窓口の背後に人民元札束を山積みせざるを得なくなった、今後初めのことだ、中国北西部の貸しては取り付けに加わらなかったが、派遣された政府職員は財政危機の噂と格闘している。

As Reuters reports, Yingkou was the latest small bank to have its deposit-reliant funding base undermined by a flash mob of "running" depositors, spooked by the funding crunch that led to the shock state-led rescue of regional lender Baoshang Bank first which in turn prompted a cascade of small bank bailouts.

ロイターの報告によると、Yingkouは資金不足懸念による預金者の「殺到」に見舞われた、当初はBaoshang Bankで起きた資金不足による政府救済が連鎖的に小規模銀行に生じている。

To avoid an almost instant death, Yingkou had no choice but to engage in what we have hence dubbed a self-destructive "doom loop: to help repair the damage and to keep the deposits from being pulled, the bank hiked its already high deposit interest rates to entice depositors. Alas by doing so, the bank - which can not possibly find investing opportunities to offset the higher deposit rates - has just accelerated its eventual insolvency.

銀行の即死を回避するため、Yingkouは我々が『自滅ループ』と呼ぶ方策を取らざるを得なかった:預金引き出しを回避するために、当行はすでに高かった預金利息をさらに引き上げ預金者を引き止めた。そうでもしないと、当行はーー高利息を払えるだけの投資先を見つけることが出来ないわけでーーやがて支払不能破産を加速するだけだ。

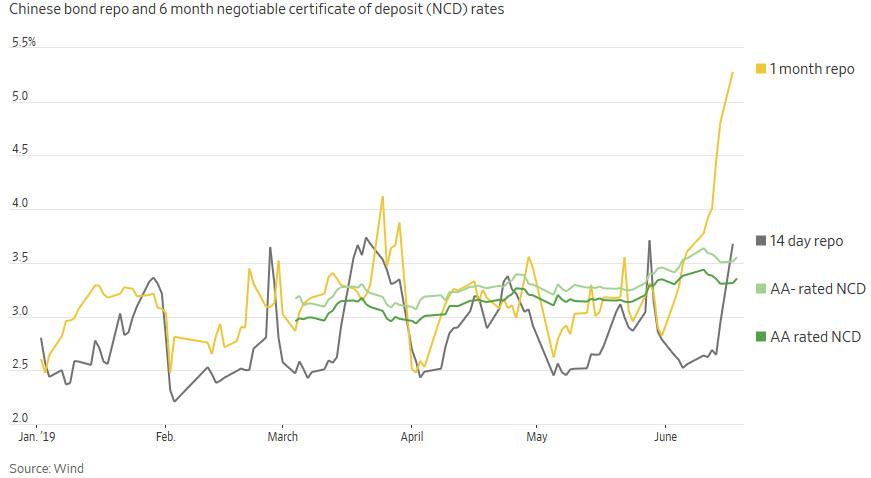

Baoshang救済以降インターバンク金利がスパイク状に急騰し、YingKouの取り付け騒ぎは今年小型銀行への信頼がなくなる中で起きた、インターバンク金利急騰で債務コストが上昇し、ZeroHedgeが6月に伝えたように短期的な資金調達がほとんどできなくなった。

To be sure, bank funding was already under pressure for most but the biggest bank following government efforts to de-leverage the financial system starting in 2016. Meanwhile, small but deadly cuts in key lending rates since August to stimulate up a slowing economy have only exacerbated the pressure on banks.

確実に言えるが、政府が金融システムのレバレッジ解消を2016年から初めており、多くの銀行ですでに資金調達が圧力を受けている。それと同時に、8月以来減速する経済刺激のために小規模だが金利が切り下げられた、これが銀行への圧力を悪化させている。

With less income from lending and without the full suite of funding options available to much larger peers, the interest rates that China’s legion of small banks may have to offer to attract deposits could further undermine their stability, analysts said. The irony is that to preserve their critical deposit base, small banks have to hike deposit rates even higher to stand out, in the process sapping their own lifeblood and ensuring their self-destruction. Hence "doom loop."

大手銀行ほどに運用選択の余地が無く、また貸し出し収入が少ない中国の地方小銀行は高利息で預金を集めざるを得ずこれがさらに安定性を弱体化している、とアナリストは分析する。皮肉なことに、最低限の預金を維持するために、小銀行は突出して利息を上げざるを得ない、自らに不可欠な活力源を失い自己破綻への道を歩んでいる。だからこそ「自滅ループ」なのだ。

Dai Zhifeng、Zhongtai Securitiesの銀行アナリストがロイターに言うには、資金不足が危険な小銀行の行動を歪めている、さらに破綻の可能性が増している:「コア競争力を失い、これらの銀行の中にはさらにリスク選好戦略へと向かわざるを得ない、短期運用だ、」と彼は言う、さらに流動性欠如が重なっている銀行もある。

Institutions such as Yingkou, where "untruthful rumors about the bank’s deep financial crisis spread online", the city police said, triggering a run on deposits on Nov. 6 when a Reuters witness saw piles of cash behind counters at six city-centre branches.

Yingkouのような銀行では、「深刻な金融危機がおきているという嘘の噂がオンライで広がる」、当市警察は述べた、これが11月6日に取り立て騒ぎのきっかけとなった、ロイター記者も当行6支店窓口の後ろに札束の山を見た。

Just like at Yichuan Rural Bank, the local government stepped in to allay concerns, placing officials at Yingkou’s biggest branch to help calm depositors, and hanging notices saying the bank had sufficient assets and that its operations and management were in good standing.

Yichuan Rural Bankと同様に、地方政府は懸念を払拭しようとした、預金者をなだめるためにYingkouの大きな支店には役人を配置した、そして看板を掲示し、当行には十分な資金があり営業運用は正常だと伝えた。

Why the panic to avoid outflows? Because as of June-end deposits made up 58% of Yingkou’s funding. In the wake of the run, it raised its rate for one-year time deposits to 4.4% from 4.2% and kept the rate on its flagship three-month wealth management product above 5%. By comparison, the popular money market fund Yu’ebao backed by e-commerce giant Alibaba Group Holding Ltd offers a modest 2% annualized rate, while China’s benchmark rate for a one-year time deposit is 1.75%; this means that the troubled bank has to offer interest rates more than double the prevailing ones just to keep depositors from fleeing.

資金流出回避でどうしてパニックになったか?その理由は6月末にYingkouの資金の58%が預金となったからだ。資金不足となり、当行は1年もの定期預金の利息をこれまでの4.2%から4.4%に引き上げた、主力の3ヶ月もの理財商品の利息を5%以上とした。比較のために示すと、一般的なマネー・マーケット・ファンドYu'ebao、アリババの子会社だが、の利息は2%に過ぎない、一方でベンチマークとなる中国の一年もの定期預金利息は1.75%だ;というわけで問題を抱える銀行は預金流出を回避するために一般的な金利の倍を提供せざるを得ない。

"I thought about the risks of smaller lenders, but an interest rate of 4%-plus on deposits was too attractive for me," said Sun Wensheng, a perfect example of the gullible depositors the bank is desperately in need of, and a futures trader who deposited 420,000 yuan ($59,772.86) with Yingkou just before the bank run. Sun is in for a big surprise when in a few weeks that bank shuts down, this time for good, and his entire deposit is gone... all gone.

典型的な騙されやすい預金者Sun Wenshengはこう言う、「この銀行にはリスクがあるが4%超の利息は魅力的だ」、当行はもうやむにやまれずやけくそになっている、彼は先物トレーダーで取り付け騒ぎ前にYingkouに$59,772.86を預金していた。数週前に銀行が閉鎖されたときSunはとても驚いた、彼の預金はまったく戻ってくることはなかった。

Though small, problems at China’s more than 4,500 local banks matter because of their close ties to larger lenders and huge base of mom-and-pop savers; put enough banks under and suddenly you have a "Lehman moment", as the interbank market freezes.

小規模とはいえ、中国の問題地方銀行は4,500以上ある、問題は、これらの銀行は大きな貸し手とつながっており、預金者は街のおじさんおばさんであることだ;一定の数の銀行が急に「レーマンモメント」を迎えると、インターバンク市場が凍結される。

Yingkou was the second bank run in less than two weeks, following the previously discussed panic at Yichuan Rural Commercial Bank in central Henan province amid a corruption investigation into a former boss. But in contrast to the May rescue of Inner Mongolia lender Baoshang Bank, when a takeover by the central government sent interbank lending rates sharply higher, local governments took the lead in managing both of the latest scares.

この2週でYingkouは2回目の取り付け騒ぎ銀行となった、前回は河南省のYichuan Rural Commercal Bankだった、あのときは元社長に対する不正融資が原因だった。しかし5月に起きた内モンゴルのBaoshang Bankの際には、中央政府救済でインターバンク金利が急騰した、今回は地方政府が先導して処理を行った。

According to Reuters, the change in approach was deliberate and is

now based on the specific situation of the bank in question, said an

official at the Shanghai branch of the CBIRC. In both runs,

funding from other local banks was swiftly brought in to allay liquidity

fears under instruction from the authorities.

ロイターによると、この変更は慎重に検討されたものだ、個別銀行の状況に依存する、とCBIRCの上海支局職員が答えた。どちらの取り付け騒ぎも当局の監督のもと他行から速やかな流動性支援を受けた。

「現在小規模銀行は高レバレッジと小流動性で脆弱なものだ、」と別のCBIRC職員は言う、彼は地方銀行を監督している。

Ah yes, "contagion risks" - the doomsday alarm for any authoritarian regime, such as China's. And precisely for that reason, regulators have refrained from cracking down on the high-return time deposits offered by small banks due to fear of squeezing their only remaining funding lifeline.

そう「伝染リスク」だーーどの独裁体制も「最後の審判の日」警告があり、中国も例外ではない。その理由を分析すると、監督当局は、小規模銀行が提供する高利息定期預金の取締を回避してきた、残された生命線資金が流出してしまうのではないかという恐れからだ。

Local intervention should help contain problems and cut the cost of any rescue, said Rory Green, an economist covering China at independent investment research firm TS Lombard.

地方政府の介入に際しては問題解決と救済コスト低減が求められる、とRory Greenは言う、彼は独立系投資分析企業TS Lombardの中国部門エコノミストだ。

"That is long-term positive for China, but will create a lot of risks when local authorities don’t have enough capital and don’t act quickly enough to stabilize the situation," he said.

「中国では長年これでうまく言っていた、しかし地方当局に十分な資金がなくなると多くのリスクを生み出すだろう、彼らはもはや素早く状況安定化のための行動を取れないのだ、」と彼は言う。

Regulators are also looking at recapitalization, mergers and other forms of support. On Nov. 18, another previously bailed out bank, Harbin Bank - a midsize lender with links to Baoshang stakeholder Tomorrow Holdings - saw its shares jump 9% after two local state-controlled groups became its key shareholders, paying an above-market price to do so. Because why not make a few shareholders richer if all it takes to prevent systemic collapse is what is an almost daily bailout of one of China's thousands of insolvent banks. The alternative? It's took scary to even consider.

監督当局は資本再構成を視野に入れている、合併等だ。11月18日にもう一つの銀行救済があった、Harbin BankだーーBaoshanのステークホルダーTomorrow Holdingsとも関連する中規模銀行だーー省が運営する2金融機関が主要株主になった後株価は9%上昇した、2社が相場以上の株価で買収したのだ。システム的崩壊を回避するためにどの場合も同様の手法を取るなら少数の株主だけでなく他の株主にも恩恵が受けれるように出来ないかって、それは中国の数千の破産銀行救済が毎日のようにおきているからだ。他の救済方法はないのか?もうそれは考えるだけでも恐ろしい。

ロイターによると、この変更は慎重に検討されたものだ、個別銀行の状況に依存する、とCBIRCの上海支局職員が答えた。どちらの取り付け騒ぎも当局の監督のもと他行から速やかな流動性支援を受けた。

"The current smaller banking industry is fragile due to (its) high leverage and poor liquidity management,” said another regional CBIRC official who oversees local rural banks.

「現在小規模銀行は高レバレッジと小流動性で脆弱なものだ、」と別のCBIRC職員は言う、彼は地方銀行を監督している。

"Smaller banks need to be treated carefully and problems rectified as they emerge, such as corporate governance, to avoid contagion risks."「小規模銀行に関しては問題発生時に注意深く解決せねばならない、企業統治に目をむけ、他行への伝搬を回避せねばならない。」

Ah yes, "contagion risks" - the doomsday alarm for any authoritarian regime, such as China's. And precisely for that reason, regulators have refrained from cracking down on the high-return time deposits offered by small banks due to fear of squeezing their only remaining funding lifeline.

そう「伝染リスク」だーーどの独裁体制も「最後の審判の日」警告があり、中国も例外ではない。その理由を分析すると、監督当局は、小規模銀行が提供する高利息定期預金の取締を回避してきた、残された生命線資金が流出してしまうのではないかという恐れからだ。

Local intervention should help contain problems and cut the cost of any rescue, said Rory Green, an economist covering China at independent investment research firm TS Lombard.

地方政府の介入に際しては問題解決と救済コスト低減が求められる、とRory Greenは言う、彼は独立系投資分析企業TS Lombardの中国部門エコノミストだ。

"That is long-term positive for China, but will create a lot of risks when local authorities don’t have enough capital and don’t act quickly enough to stabilize the situation," he said.

「中国では長年これでうまく言っていた、しかし地方当局に十分な資金がなくなると多くのリスクを生み出すだろう、彼らはもはや素早く状況安定化のための行動を取れないのだ、」と彼は言う。

Regulators are also looking at recapitalization, mergers and other forms of support. On Nov. 18, another previously bailed out bank, Harbin Bank - a midsize lender with links to Baoshang stakeholder Tomorrow Holdings - saw its shares jump 9% after two local state-controlled groups became its key shareholders, paying an above-market price to do so. Because why not make a few shareholders richer if all it takes to prevent systemic collapse is what is an almost daily bailout of one of China's thousands of insolvent banks. The alternative? It's took scary to even consider.

監督当局は資本再構成を視野に入れている、合併等だ。11月18日にもう一つの銀行救済があった、Harbin BankだーーBaoshanのステークホルダーTomorrow Holdingsとも関連する中規模銀行だーー省が運営する2金融機関が主要株主になった後株価は9%上昇した、2社が相場以上の株価で買収したのだ。システム的崩壊を回避するためにどの場合も同様の手法を取るなら少数の株主だけでなく他の株主にも恩恵が受けれるように出来ないかって、それは中国の数千の破産銀行救済が毎日のようにおきているからだ。他の救済方法はないのか?もうそれは考えるだけでも恐ろしい。