調整が来つつある、でもブル派には告げるな・・・まだだ。

Technically Speaking: A Correction Is Coming, Just Don’t Tell The Bulls…Yet.

Written by Lance Roberts | Nov 12, 2019

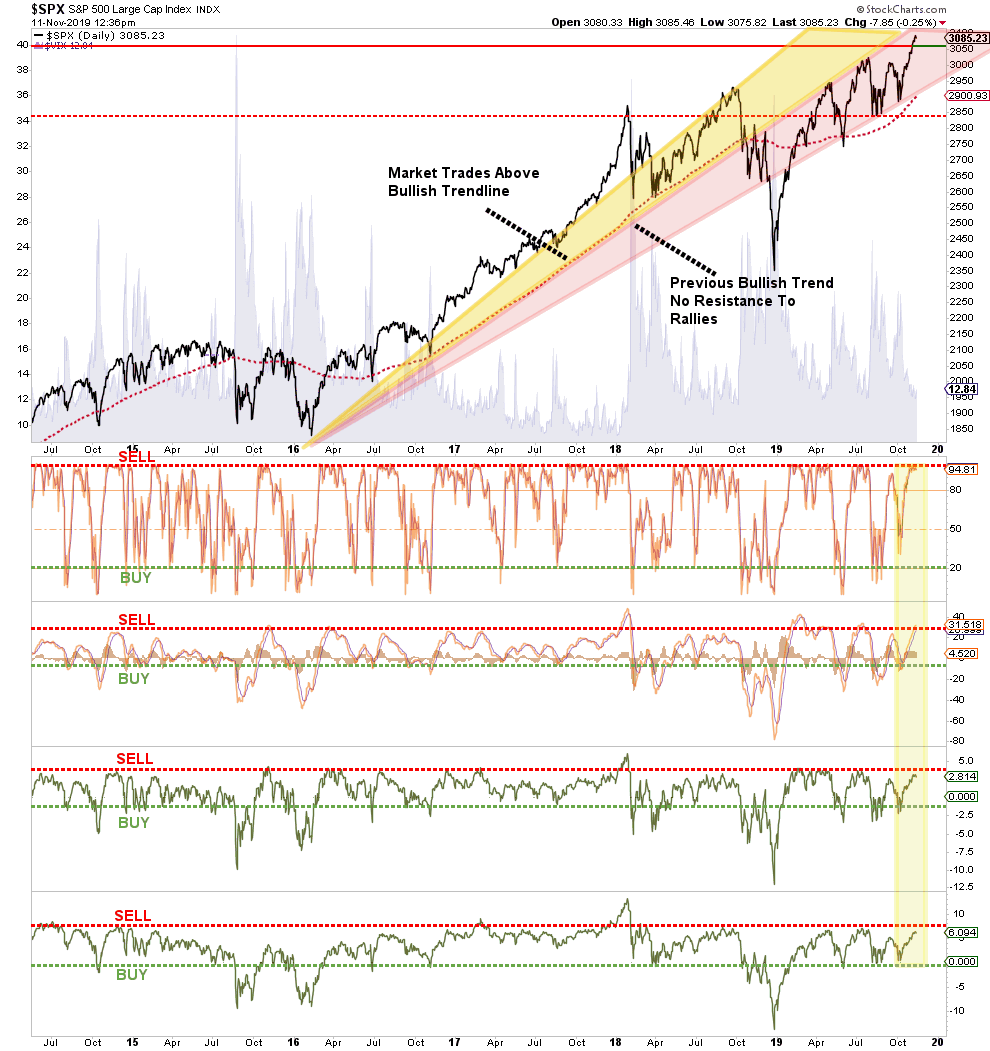

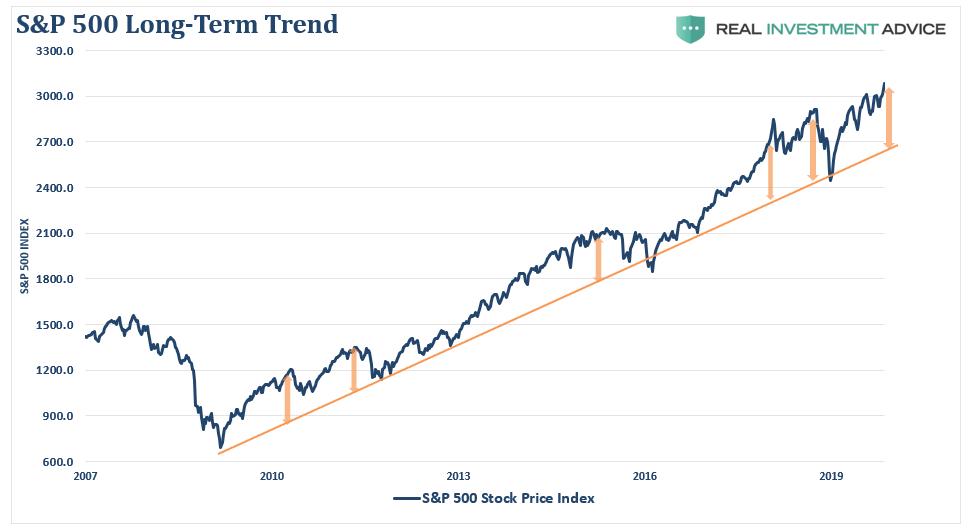

In this past weekend’s newsletter, I discussed the rather severe extensions of the market above both the longer-term bullish trend and the 200-dma. To wit:

この週末のニュースレターで、私は相場が長期的ブルトレンドや200DMAから大きく乖離していることを議論した。見てみよう:

「現在、年末が近づき我々は我慢強く耐えなければならないだろう。決算発表が終わり、経済データはQ4に向けて弱いものだ、ここ数週買い進まれている。

But it isn’t just the more extreme advance of the market over the past 5-weeks which has us a bit concerned in the short-term, but a series of other indications which typically suggest short- to intermediate-terms corrections in the market.

Not surprisingly, whenever I discuss the potential of a market correction, it is almost always perceived as being “bearish.” Therefore, by extension, such must mean I am either all in cash or shorting the market. In either case, it is assumed I “missed out” on the previous advance.

ここ5週、短期的には相場はちょっと行すぎが懸念される、一連の指標を見ると中短期的な調整を示唆している。驚くことではないが、ずっと私は市場の調整を議論してきた、これはいつも「ベア派」のように見えるかもしれない。それは私がすべて現金化しているとかショートポジションを取っているということを意味している。こういう行動をとると私はこれまでの相場進展を「掴みそこねたことになる」。

If you have been reading our work for long, you already know we have remained primarily invested in the markets, but hedge our risk with fixed income and cash, despite our “bearish” views. I am reminded of something famed Morgan Stanley strategist Gerard Minack said once:

長年私どもの記事を読んできた人にとっては、御存知の通り、私どもはまだ相場にとどまっている、ただし現金や金利商品でリスクヘッジをしている、「弱気」の味方にもかかわらずだ。私は著名なモルガン・スタンレーのストラテジストGerard Minackがかつて言ったことを思い出す:

While the mainstream media continues to misalign individual’s expectations by chastising them for “not beating the market,” which is actually impossible to do, the job of a portfolio manager is to participate in the markets with a preference toward capital preservation. This is an important point:

主要メディアはいつも個人投資家の期待を間違って誘導する、「市場成績を上回っていないのでは」と攻め立てる、これは実際に無理筋だ、ポートフォリオマネジャーの仕事とは市場のなかで顧客資産を失わないようにすることだ。これが大切なことだ:

「長期的なポートフォリオパフォーマンスにおいては、相場が下落するときに資金を食いつぶしてしまうと大変なことになる。」

It is from that view, as a portfolio manager, the idea of “fully invested bears” defines the reality of the markets that we live with today. Despite this understanding, the markets are overly bullish, extended, and overvalued and portfolio managers must stay invested or suffer potential “career risk” for underperformance. What the Federal Reserve’s ongoing interventions have done is push portfolio managers to chase performance despite concerns of potential capital loss.

こういう視点からすると、ポートフォリオマネージャとしてみると、「ベア相場ですべて投資する」というのが現在の相場だ。この状況を理解しながらも、市場は過剰に強気だ、それが長引いており、過剰バリュエーションであり、それでもポートフォリオマネージャーは投資したままで居ざるを得ない、さもなくばアンダーパフォーマンスとなり潜在的に「自らの仕事を失う」可能性がある。FEDが今行っている介入とは、ポートフォリオマネージャにパフォーマンスを追いかけさせ、一方で資金を失う懸念を抱えている。

Managing portfolios for both risk adjusted returns while protecting capital is a delicate balance. Each week in the Real Investment Report (click here for free weekly e-delivery) we discuss the risks and challenges of the current market environment and report on how we are adjusting our exposures to the market over time.

ポートフォリオ管理としては、リスクを勘案しながらリターンを得る一方で資産を守るというのは微妙なバランスだ。毎週のReal Investment Reportでは、私どもはリスクと、現在の市場環境への挑戦、そして時間とともに露出をどう調整しているかを議論している。

In this past weekend’s missive, we discussed how to “play” the latest round of the Fed’s QE program, along with what sectors and markets tend to perform the best.

However, I wanted to share a few charts which suggests that being patient currently, will likely yield a much better entry point for investors in the not-so-distant future.

先週の記事では、FED QEプログラムの最終局面でとう「プレイ」するかということを議論した、最良のパフォーマンスを示す市場・セクターに関してだ。しかしながら、私は数枚のチャートをみなさんと共有したい、現在は我慢のときだ、そう遠くない先に市場に参加する良いタイミングが生じるだろう。

By the majority of measures that we track from momentum, to price,

and deviation, the market’s sharp advance has pushed the totality of

those indicators back to overbought.

我々がモメンタムを追いかけているという大きな指標は、株価と乖離だ、相場が急激に進むとこれらの指標が買われすぎとなる。

Historically, when all of the indicators are suggesting the market has likely encompassed the majority of its price advance, a correction to reverse those conditions is often not far away. Regardless of the timing of that correction, it is unlikely there is much upside remaining in the current advance, and taking on additional equity exposure at these levels will likely yield a poor result.

歴史を振り返ると、すべての指標が株価の進み過ぎを示すと、反転調整がそう遠くない。この調整のタイミングはさておき、現在ほどに株価が進むとこれ以上に進む余地はあまりない、この時点でのさらなる露出増加はあまり良い結果を産まないだろう。

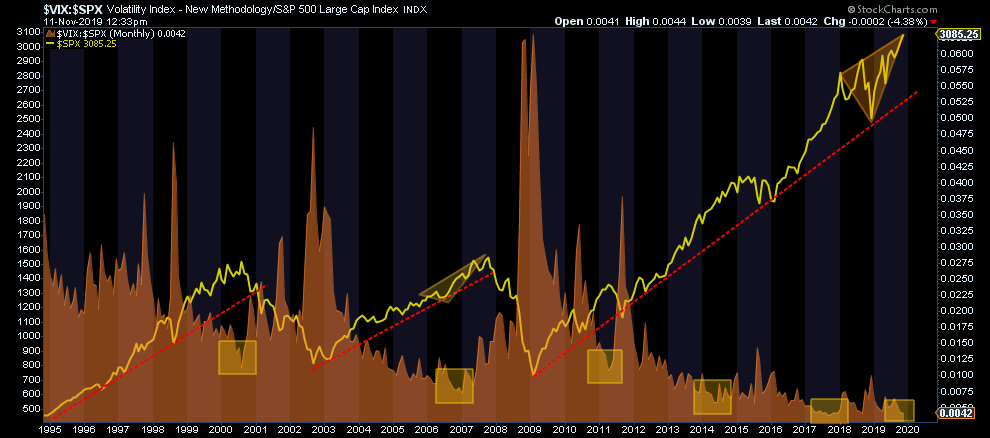

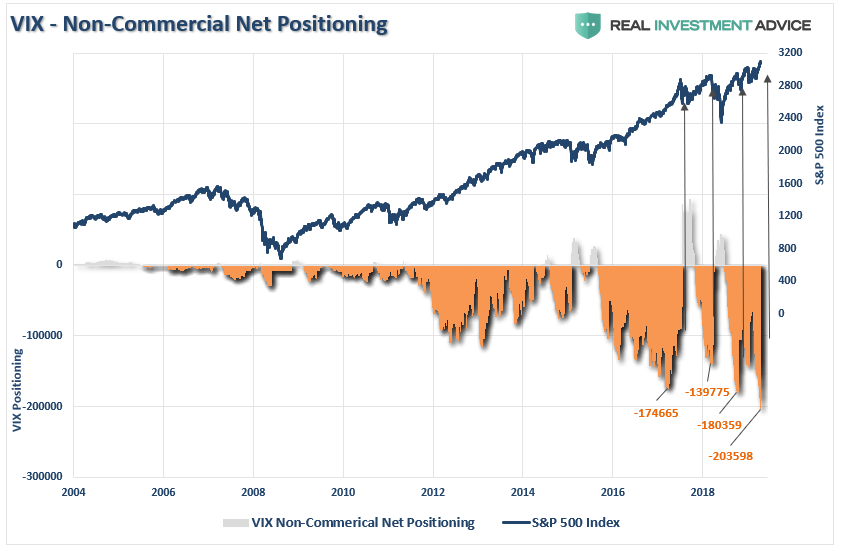

The post-Fed rate cut and QE driven advance in the market has also pushed investors back to levels of extreme complacency.

FED金利引下げ後、そしてQEに裏付けられた市場は投資家を極端な安心感に引き戻した。

Such extremely low levels of volatility, combined with investors piling into record “short positions” on the VIX, provides all the “fuel” necessary for a fairly sharp 3-5% correction given the proper catalyst.

このように極端な低ボラティリティ、さらには投資家はVIXに記録的な「空売りポジション」を積み上げている、こういう状況では何らかのきっかけで3−5%の調整急落が必要だ。

Given that investors are “all in,” as discussed last week, there is plenty of room for investors to get forced out of holdings and push markets lower over the next few weeks. However, it isn’t just individual investors that are “all in,” but professionals as well.

先週議論したように投資家は現在「all in」の状態だ、今後数週で投資家は強制的なポジション解消と株価押し下げの余地が大いにある。しかしながら、「all in 」状態なのは個人投資家だけではない、専門家も同様なのだ。

Eurodollar positioning is also sending a major warning. (“Eurodollar” refers to U.S. dollar-denominated deposits at foreign banks, or at the overseas branches of American banks.)

ユーロダラーのポジションも大きな警告を発している。(「ユーロダラー」とは海外銀行におけるドル建て預金のことだ、もしくは米国銀行の海外支店の預金だ。)

When the ECB launched QE following the 2016 selloff, foreign banks liquidated Eurodollar deposits as it was deemed less risky to hold foreign denominated deposits. Currently, that view has reversed sharply as the global economy slows, and foreign banks are “hedging” their risk by flooding money into U.S. dollar denominated deposits. Historically, when you have an extremely sharp reversal in Eurodollars, it has preceded more troubling market events.

2016年の下落後にECBがQEを開始した時、海外銀行はユーロダラー預金を解消した、海外通貨預金のほうがよりリスクが少ないと思われたからだ。現在では、この見方が急激に反転している、世界経済鈍化のためだ、そして海外銀行は自らのリスクを「ヘッジ」すうるために米ドル預金に殺到している。歴史を振り返ると、ユーロダラーの極端に急な逆転があるとき、市場に問題が生じる予兆となっている。

With Eurodollar deposits at record levels, do foreign banks know something we don’t?

ユーロダラーが記録的な量になっているわけで、海外銀行は何か我々が知り得ないことを知っているのだろうか?

The deviation between corporate GAAP earnings and corporate profits

is currently at record levels. It is also entirely unsustainable. Either

corporate profits will catch up with earnings, or vice-versa.

Historically, profits have never caught up with earnings, it is always

the other way around.

企業のGAAP earnings と企業 profits の間の乖離は現在記録的なレベルになっている。この状況は持続可能なものではない。企業 profits が earnings に追いつくか、その逆かどちらかだ。歴史を振り返ると、profits がearningsに追いついたことはない、いつもその逆だ。

Expectations for corporate earnings going forward are still way to elevated, and with corporate share buybacks slowing, this leaves lots of room for disappointment.

GAAP収益増加期待が大きくなりすぎている、そして企業の自社株 buybacksは鈍化している、ということは失望の可能性が大きい。

I have written many times in the past that the financial markets are not immune to the laws of physics.

私はこれまで何度も書いてきたが、金融市場は物理法則から逃れることができない。

There is a simple rule for markets:

市場にはシンプルなルールがある:

The example I use most often is the resemblance to “stretching a rubber-band.” Stock prices are tied to their long-term trend which acts as a gravitational pull. When prices deviate too far from the long-term trend they will eventually, and inevitably, “revert to the mean.”

私が最もよく例えにつかのは「ゴムバンドの引き伸ばし」だ。株価というのは長期的なトレンドに縛られており、これがまるで重力のように引き込む。株価が長期トレンドから大きく乖離するほどに、やがてそしてかならず、「平均回帰」する。

See Bob Farrell’s Rule #1

Bob Farrellのルール#1を見よ

Currently, the market is not only more than 6% above its 200-dma, as shown in the opening of this missive, but is currently more than 15% above its 3-year moving average.

現在のところ、市場は200DMAから6%上方乖離しているだけでなく、この記事の最初にも書いたが、3年移動平均から15%以上乖離している。

More importantly, the market is currently extremely deviated above it long-term bullish trend. During this entire decade-long bull market advance, the trendline is retested with some regularity from such extreme extensions.

もっと大切なことは、市場は長期ブルトレンドから極端に乖離していることだ。もう10年もブル相場が続いているが、これほど極端な乖離があるときには何度もテストされてきた。

Lastly, is sentiment. When sentiment is heavily skewed toward those willing to “buy,” prices can rise rapidly and seemingly “climb a wall of worry.” However, the problem comes when that sentiment begins to change and those willing to “buy” disappear.

最後に投資心理について議論しよう。投資心理が「買いたい」に極端に歪んだ時、株価は急激に上昇しまるで「懸念の壁をよじ登る」状態になる。しかしながら、問題が生じるのはその心理が変化し始めその「買いたい」心理が消え失せるときだ。

This “vacuum” of buyers leads to rapid reductions in prices as sellers are forced to lower their price to complete a transaction. The problem is magnified when prices decline rapidly. When sellers panic, and are willing to sell “at any price,” the buyers that remain gain almost absolute control over the price they will pay. This “lack of liquidity” for sellers leads to rapid and sharp declines in price, which further exacerbates the problem and escalates until “sellers” are exhausted.

この買い手の「真空地帯」が株価急落を引き起こし、売り手が株価を押し下げる。株価が急落したときには、問題が増幅される。売り手がパニックになると、「株価がどうあれ」売りたいと思い、残された買い手が株価を自由に操作でき、支払い能力に応じるレベルにする。この売り手の「流動性の欠如」が株価急落を引き起こす、これがさらに問題を悪化させ、「売り手」が居なくなるまで問題は続く。

Currently, there is a scarcity of “bears.”

今の所、「ベア派」がほとんど居ない。

See Bob Farrell’s Rule #6

Bob Farrell のRule #6を見よ

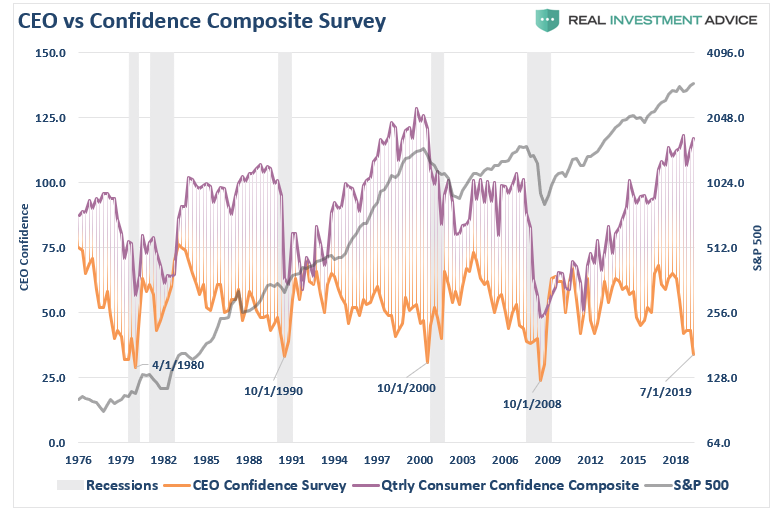

As we discussed just recently, consumer and investor confidence are both closely tied and are extremely elevated. However, CEO confidence is pushing record lows. A quick look at history shows this level of disparity is not unusual around market peaks and recessionary onsets.

最近私どもが議論したが、消費者信頼指数と投資家信頼指数は密接に関連しているが、どちも極端に高くなっている。しかしながら、CEO信頼指数は記録的な低位だ。歴史を振り返ると、このレベルの乖離は尋常ではなく、相場のピークや景気後退の始まりでしか見られないことだ。

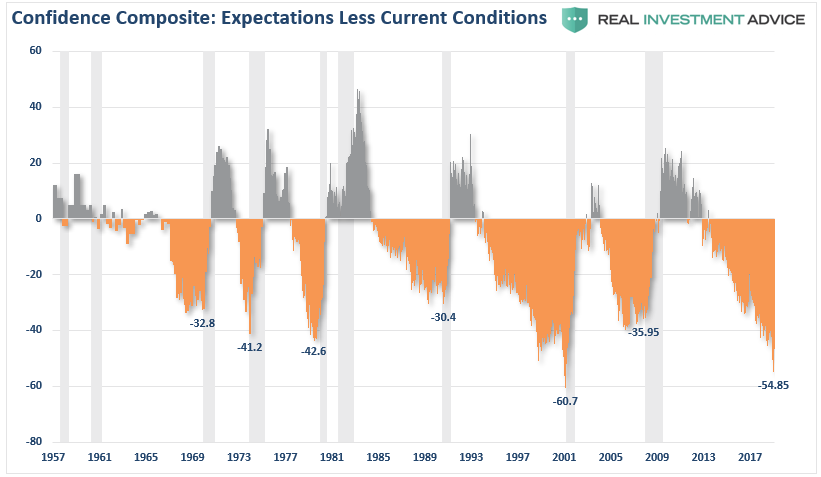

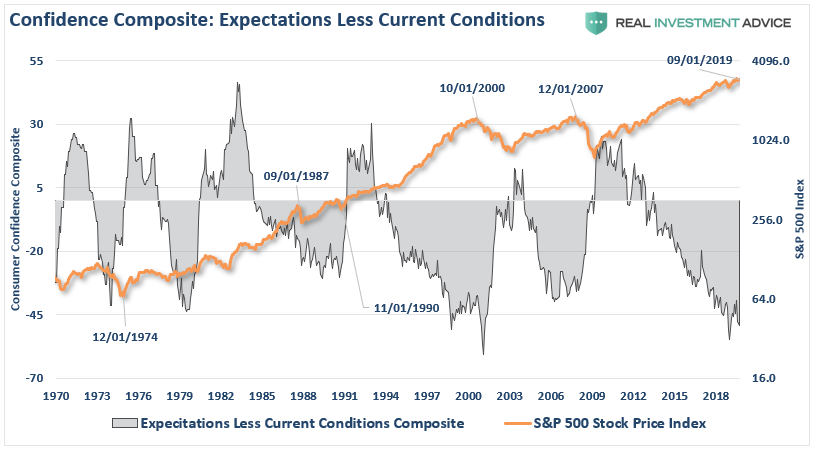

Another way to analyze confidence data is to look at the consumer expectations index minus the current situation index in the consumer confidence report.

This measure also is signaling a correction/recession is coming. The differential between expectations and the current situation, as you can see below, is worse than the last cycle, and only slightly higher than prior to the “dot.com” crash. Recessions start after this indicator bottoms, which has already started happening.

もう一つの信頼できるデータ分析は消費者信頼指数で将来指数から現在指数を引いたものだ。この指標もまた調整/景気後退が来ていることを知らしている。将来予想と現在地の歳を下のチャートで見ることができる、これが前回の景気サイクル時よりも悪化している、「ドットコム」暴落時よりはまだマシだ。この指標が底をついた後に景気後退が始まる、すでに始まっている。

Currently, the bottoming process, and potential turn higher, which signals a recession and bear market, appears to be in process.

現在の状態は、ボトミングプロセス中だ、そして今後数値が上昇すると、それは景気後退とベア相場となる、そのプロセスの最中だ。

None of this should be surprising as we head into 2020. With near-record low levels of unemployment and jobless claims, combined with record high levels of sentiment, job openings, and record asset prices, it seems to be just about as “good as it can get.”

2020年に向かいこれはちっとも驚くことではない。記録的な低失業率と低失業保険申請であり、さらには記録的に高いセンチメント、求人、そして記録的株価、これはまるで「もうこれ以上はないほどに良い状態」というわけだ。

Does this mean the current bull market is over?

この状況は現在のブル相場の終わりを示すということだろうか?

No.

いやそうではない。

However, it does suggest the “risk” to investors is currently to the downside, and some caution with respect to equity-based exposure should be considered.

しかしながら、これが示唆するのは投資家に対する下落「リスク」だ、そして株式露出に対する何らかの注意が喚起させるということだ。

Given the fact that the short, intermediate, and long-term indicators have all aligned, the risk of running portfolios without a hedge is no longer optimal. As such, we added an “inverse” S&P 500 position to all of our portfolios late yesterday afternoon.

中短期、そして長期指数はどれも勢揃いしている、ヘッジなしのポートフォリオを持つのは好ましくない。その一環として私どもはS&P500に「逆行」するポジションを昨日午後に加えた。

While none of the charts above necessarily mean the next “great bear market” is coming, they do suggest a modest correction is likely. The reason we hedge against declines is that one day, and we never know when, a modest correction will turn into a more significant decline.

これまで示したチャートはどれひとつとして次の「大型ベア相場」が来ているとは言っていない、それらが示すのはある程度の調整がありそうだということだ。私どもが下落に対するヘッジをする理由は、ある日、その日がいつかは誰も知ることができない、穏やかな調整がもっと深刻な下落となるということだ。

Remaining fully invested in the financial markets without a thorough understanding of your “risk exposure” will likely not have the desirable end result you have been promised. All of the charts above have linkages to each other, and when one breaks, they all break.

自らの「リスク露出」を理解しないままに金融市場に全力投資したままにするということは望んだ結果を得ることは無いだろう。ここで示したチャートはどれもが互いに相関しており、どれかが破綻すると、全てが破綻する。

So pay attention to the details.

というわけで詳細にこだわることだ。

As I stated above, my job, like every portfolio manager, is to participate when markets are rising. However, it is also my job to keep a measured approach to capital preservation.

これまで述べてきたことは、私の職務だ、どのポートフォリオマネージャも同様だ、相場が上昇しているときには参加する。しかしながら、もう一つの私の職務・責務は顧客の資産を保全する対策を講じることだ。

この週末のニュースレターで、私は相場が長期的ブルトレンドや200DMAから大きく乖離していることを議論した。見てみよう:

“Currently, it will likely pay to remain patient as we head into the end of the year. With a big chunk of earnings season now behind us, and economic data looking weak heading into Q4, the market has gotten a bit ahead of itself over the last few weeks.

「現在、年末が近づき我々は我慢強く耐えなければならないだろう。決算発表が終わり、経済データはQ4に向けて弱いものだ、ここ数週買い進まれている。

On a short-term basis, the market is now more than 6% above its 200-dma. These more extreme price extensions tend to denote short-term tops to the market, and waiting for a pull-back to add exposures has been prudent..”短期的には、相場は200DMAを6%上回っている。このように極端な相場の進展は短期的な天井となりやすい、そして露出を増やすなら押し目を狙うのが規律ある行動だ・・・」

But it isn’t just the more extreme advance of the market over the past 5-weeks which has us a bit concerned in the short-term, but a series of other indications which typically suggest short- to intermediate-terms corrections in the market.

Not surprisingly, whenever I discuss the potential of a market correction, it is almost always perceived as being “bearish.” Therefore, by extension, such must mean I am either all in cash or shorting the market. In either case, it is assumed I “missed out” on the previous advance.

ここ5週、短期的には相場はちょっと行すぎが懸念される、一連の指標を見ると中短期的な調整を示唆している。驚くことではないが、ずっと私は市場の調整を議論してきた、これはいつも「ベア派」のように見えるかもしれない。それは私がすべて現金化しているとかショートポジションを取っているということを意味している。こういう行動をとると私はこれまでの相場進展を「掴みそこねたことになる」。

If you have been reading our work for long, you already know we have remained primarily invested in the markets, but hedge our risk with fixed income and cash, despite our “bearish” views. I am reminded of something famed Morgan Stanley strategist Gerard Minack said once:

長年私どもの記事を読んできた人にとっては、御存知の通り、私どもはまだ相場にとどまっている、ただし現金や金利商品でリスクヘッジをしている、「弱気」の味方にもかかわらずだ。私は著名なモルガン・スタンレーのストラテジストGerard Minackがかつて言ったことを思い出す:

“The funny thing is there is a disconnect between what investors are saying and what they are doing. No one thinks all the problems the global financial crisis revealed have been healed. But when you have an equity rally like you’ve seen for the past four or five years, then everybody has had to participate to some extent.「とても奇妙なことだが投資家は言うことと行動に乖離がある。だれも金融危機で明らかになった問題が癒やされているとは考えていない。しかしこの4,5年で生じているラリーを目の当たりにすると、誰もが幾ばくかは参加しなくちゃという気分になる。みなさんが今やっていることはベア見込みながら全力投資しているということだ。」

What you’ve had are fully invested bears.”

While the mainstream media continues to misalign individual’s expectations by chastising them for “not beating the market,” which is actually impossible to do, the job of a portfolio manager is to participate in the markets with a preference toward capital preservation. This is an important point:

主要メディアはいつも個人投資家の期待を間違って誘導する、「市場成績を上回っていないのでは」と攻め立てる、これは実際に無理筋だ、ポートフォリオマネジャーの仕事とは市場のなかで顧客資産を失わないようにすることだ。これが大切なことだ:

“It is the destruction of capital during market declines that have the greatest impact on long-term portfolio performance.”

「長期的なポートフォリオパフォーマンスにおいては、相場が下落するときに資金を食いつぶしてしまうと大変なことになる。」

It is from that view, as a portfolio manager, the idea of “fully invested bears” defines the reality of the markets that we live with today. Despite this understanding, the markets are overly bullish, extended, and overvalued and portfolio managers must stay invested or suffer potential “career risk” for underperformance. What the Federal Reserve’s ongoing interventions have done is push portfolio managers to chase performance despite concerns of potential capital loss.

こういう視点からすると、ポートフォリオマネージャとしてみると、「ベア相場ですべて投資する」というのが現在の相場だ。この状況を理解しながらも、市場は過剰に強気だ、それが長引いており、過剰バリュエーションであり、それでもポートフォリオマネージャーは投資したままで居ざるを得ない、さもなくばアンダーパフォーマンスとなり潜在的に「自らの仕事を失う」可能性がある。FEDが今行っている介入とは、ポートフォリオマネージャにパフォーマンスを追いかけさせ、一方で資金を失う懸念を抱えている。

Managing portfolios for both risk adjusted returns while protecting capital is a delicate balance. Each week in the Real Investment Report (click here for free weekly e-delivery) we discuss the risks and challenges of the current market environment and report on how we are adjusting our exposures to the market over time.

ポートフォリオ管理としては、リスクを勘案しながらリターンを得る一方で資産を守るというのは微妙なバランスだ。毎週のReal Investment Reportでは、私どもはリスクと、現在の市場環境への挑戦、そして時間とともに露出をどう調整しているかを議論している。

In this past weekend’s missive, we discussed how to “play” the latest round of the Fed’s QE program, along with what sectors and markets tend to perform the best.

However, I wanted to share a few charts which suggests that being patient currently, will likely yield a much better entry point for investors in the not-so-distant future.

先週の記事では、FED QEプログラムの最終局面でとう「プレイ」するかということを議論した、最良のパフォーマンスを示す市場・セクターに関してだ。しかしながら、私は数枚のチャートをみなさんと共有したい、現在は我慢のときだ、そう遠くない先に市場に参加する良いタイミングが生じるだろう。

Overbought And Extended

買われすぎ、そしてそれが続いている

我々がモメンタムを追いかけているという大きな指標は、株価と乖離だ、相場が急激に進むとこれらの指標が買われすぎとなる。

Historically, when all of the indicators are suggesting the market has likely encompassed the majority of its price advance, a correction to reverse those conditions is often not far away. Regardless of the timing of that correction, it is unlikely there is much upside remaining in the current advance, and taking on additional equity exposure at these levels will likely yield a poor result.

歴史を振り返ると、すべての指標が株価の進み過ぎを示すと、反転調整がそう遠くない。この調整のタイミングはさておき、現在ほどに株価が進むとこれ以上に進む余地はあまりない、この時点でのさらなる露出増加はあまり良い結果を産まないだろう。

Overly Complacent

過剰な安心感

FED金利引下げ後、そしてQEに裏付けられた市場は投資家を極端な安心感に引き戻した。

Such extremely low levels of volatility, combined with investors piling into record “short positions” on the VIX, provides all the “fuel” necessary for a fairly sharp 3-5% correction given the proper catalyst.

このように極端な低ボラティリティ、さらには投資家はVIXに記録的な「空売りポジション」を積み上げている、こういう状況では何らかのきっかけで3−5%の調整急落が必要だ。

Given that investors are “all in,” as discussed last week, there is plenty of room for investors to get forced out of holdings and push markets lower over the next few weeks. However, it isn’t just individual investors that are “all in,” but professionals as well.

先週議論したように投資家は現在「all in」の状態だ、今後数週で投資家は強制的なポジション解消と株価押し下げの余地が大いにある。しかしながら、「all in 」状態なのは個人投資家だけではない、専門家も同様なのだ。

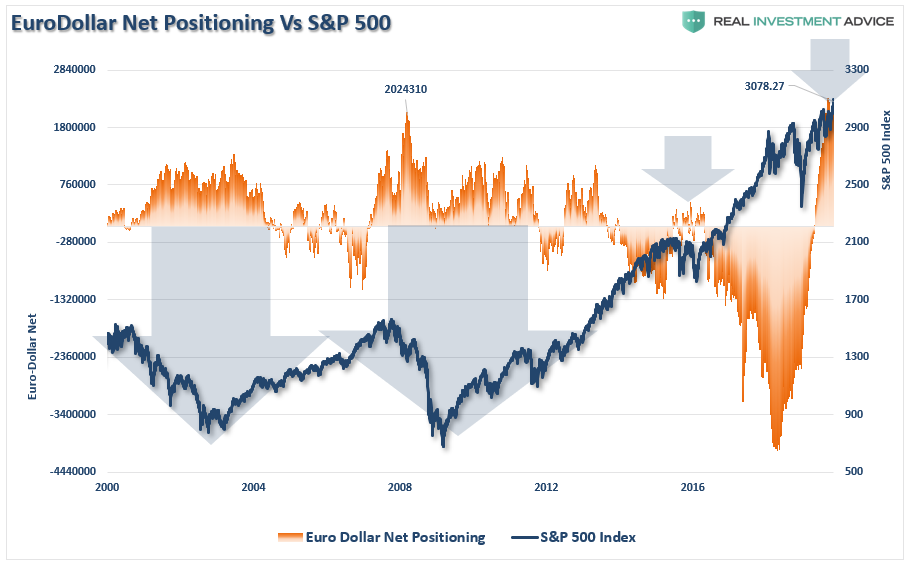

Eurodollar Sends A Warning

ユーロダラーが警告を発する

ユーロダラーのポジションも大きな警告を発している。(「ユーロダラー」とは海外銀行におけるドル建て預金のことだ、もしくは米国銀行の海外支店の預金だ。)

When the ECB launched QE following the 2016 selloff, foreign banks liquidated Eurodollar deposits as it was deemed less risky to hold foreign denominated deposits. Currently, that view has reversed sharply as the global economy slows, and foreign banks are “hedging” their risk by flooding money into U.S. dollar denominated deposits. Historically, when you have an extremely sharp reversal in Eurodollars, it has preceded more troubling market events.

2016年の下落後にECBがQEを開始した時、海外銀行はユーロダラー預金を解消した、海外通貨預金のほうがよりリスクが少ないと思われたからだ。現在では、この見方が急激に反転している、世界経済鈍化のためだ、そして海外銀行は自らのリスクを「ヘッジ」すうるために米ドル預金に殺到している。歴史を振り返ると、ユーロダラーの極端に急な逆転があるとき、市場に問題が生じる予兆となっている。

With Eurodollar deposits at record levels, do foreign banks know something we don’t?

ユーロダラーが記録的な量になっているわけで、海外銀行は何か我々が知り得ないことを知っているのだろうか?

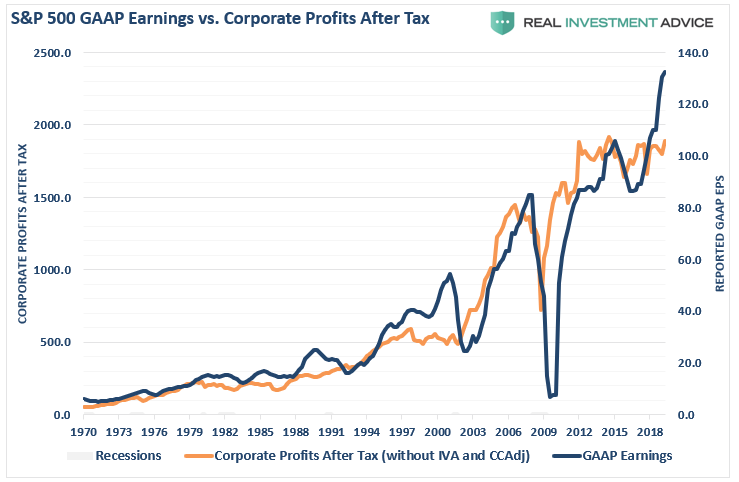

Earnings Vs. Profits

GAAP収益 vs. 税引き後利益

企業のGAAP earnings と企業 profits の間の乖離は現在記録的なレベルになっている。この状況は持続可能なものではない。企業 profits が earnings に追いつくか、その逆かどちらかだ。歴史を振り返ると、profits がearningsに追いついたことはない、いつもその逆だ。

Expectations for corporate earnings going forward are still way to elevated, and with corporate share buybacks slowing, this leaves lots of room for disappointment.

GAAP収益増加期待が大きくなりすぎている、そして企業の自社株 buybacksは鈍化している、ということは失望の可能性が大きい。

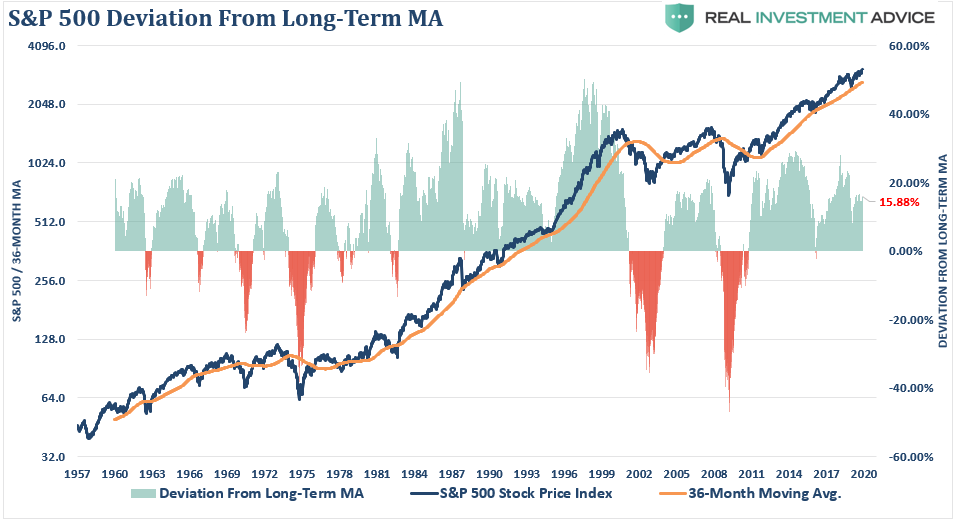

Deviation

乖離

私はこれまで何度も書いてきたが、金融市場は物理法則から逃れることができない。

There is a simple rule for markets:

市場にはシンプルなルールがある:

“What goes up, must, and will, eventually comes down.”「相場が上昇すると、やがて必ず、下落する。」

The example I use most often is the resemblance to “stretching a rubber-band.” Stock prices are tied to their long-term trend which acts as a gravitational pull. When prices deviate too far from the long-term trend they will eventually, and inevitably, “revert to the mean.”

私が最もよく例えにつかのは「ゴムバンドの引き伸ばし」だ。株価というのは長期的なトレンドに縛られており、これがまるで重力のように引き込む。株価が長期トレンドから大きく乖離するほどに、やがてそしてかならず、「平均回帰」する。

See Bob Farrell’s Rule #1

Bob Farrellのルール#1を見よ

Currently, the market is not only more than 6% above its 200-dma, as shown in the opening of this missive, but is currently more than 15% above its 3-year moving average.

現在のところ、市場は200DMAから6%上方乖離しているだけでなく、この記事の最初にも書いたが、3年移動平均から15%以上乖離している。

More importantly, the market is currently extremely deviated above it long-term bullish trend. During this entire decade-long bull market advance, the trendline is retested with some regularity from such extreme extensions.

もっと大切なことは、市場は長期ブルトレンドから極端に乖離していることだ。もう10年もブル相場が続いているが、これほど極端な乖離があるときには何度もテストされてきた。

Sentiment

心理

最後に投資心理について議論しよう。投資心理が「買いたい」に極端に歪んだ時、株価は急激に上昇しまるで「懸念の壁をよじ登る」状態になる。しかしながら、問題が生じるのはその心理が変化し始めその「買いたい」心理が消え失せるときだ。

This “vacuum” of buyers leads to rapid reductions in prices as sellers are forced to lower their price to complete a transaction. The problem is magnified when prices decline rapidly. When sellers panic, and are willing to sell “at any price,” the buyers that remain gain almost absolute control over the price they will pay. This “lack of liquidity” for sellers leads to rapid and sharp declines in price, which further exacerbates the problem and escalates until “sellers” are exhausted.

この買い手の「真空地帯」が株価急落を引き起こし、売り手が株価を押し下げる。株価が急落したときには、問題が増幅される。売り手がパニックになると、「株価がどうあれ」売りたいと思い、残された買い手が株価を自由に操作でき、支払い能力に応じるレベルにする。この売り手の「流動性の欠如」が株価急落を引き起こす、これがさらに問題を悪化させ、「売り手」が居なくなるまで問題は続く。

Currently, there is a scarcity of “bears.”

今の所、「ベア派」がほとんど居ない。

See Bob Farrell’s Rule #6

Bob Farrell のRule #6を見よ

As we discussed just recently, consumer and investor confidence are both closely tied and are extremely elevated. However, CEO confidence is pushing record lows. A quick look at history shows this level of disparity is not unusual around market peaks and recessionary onsets.

最近私どもが議論したが、消費者信頼指数と投資家信頼指数は密接に関連しているが、どちも極端に高くなっている。しかしながら、CEO信頼指数は記録的な低位だ。歴史を振り返ると、このレベルの乖離は尋常ではなく、相場のピークや景気後退の始まりでしか見られないことだ。

Another way to analyze confidence data is to look at the consumer expectations index minus the current situation index in the consumer confidence report.

This measure also is signaling a correction/recession is coming. The differential between expectations and the current situation, as you can see below, is worse than the last cycle, and only slightly higher than prior to the “dot.com” crash. Recessions start after this indicator bottoms, which has already started happening.

もう一つの信頼できるデータ分析は消費者信頼指数で将来指数から現在指数を引いたものだ。この指標もまた調整/景気後退が来ていることを知らしている。将来予想と現在地の歳を下のチャートで見ることができる、これが前回の景気サイクル時よりも悪化している、「ドットコム」暴落時よりはまだマシだ。この指標が底をついた後に景気後退が始まる、すでに始まっている。

Currently, the bottoming process, and potential turn higher, which signals a recession and bear market, appears to be in process.

現在の状態は、ボトミングプロセス中だ、そして今後数値が上昇すると、それは景気後退とベア相場となる、そのプロセスの最中だ。

None of this should be surprising as we head into 2020. With near-record low levels of unemployment and jobless claims, combined with record high levels of sentiment, job openings, and record asset prices, it seems to be just about as “good as it can get.”

2020年に向かいこれはちっとも驚くことではない。記録的な低失業率と低失業保険申請であり、さらには記録的に高いセンチメント、求人、そして記録的株価、これはまるで「もうこれ以上はないほどに良い状態」というわけだ。

Does this mean the current bull market is over?

この状況は現在のブル相場の終わりを示すということだろうか?

No.

いやそうではない。

However, it does suggest the “risk” to investors is currently to the downside, and some caution with respect to equity-based exposure should be considered.

しかしながら、これが示唆するのは投資家に対する下落「リスク」だ、そして株式露出に対する何らかの注意が喚起させるということだ。

What Are We Doing About It?

私どもはこの状況でどう対処しているか?

中短期、そして長期指数はどれも勢揃いしている、ヘッジなしのポートフォリオを持つのは好ましくない。その一環として私どもはS&P500に「逆行」するポジションを昨日午後に加えた。

While none of the charts above necessarily mean the next “great bear market” is coming, they do suggest a modest correction is likely. The reason we hedge against declines is that one day, and we never know when, a modest correction will turn into a more significant decline.

これまで示したチャートはどれひとつとして次の「大型ベア相場」が来ているとは言っていない、それらが示すのはある程度の調整がありそうだということだ。私どもが下落に対するヘッジをする理由は、ある日、その日がいつかは誰も知ることができない、穏やかな調整がもっと深刻な下落となるということだ。

Remaining fully invested in the financial markets without a thorough understanding of your “risk exposure” will likely not have the desirable end result you have been promised. All of the charts above have linkages to each other, and when one breaks, they all break.

自らの「リスク露出」を理解しないままに金融市場に全力投資したままにするということは望んだ結果を得ることは無いだろう。ここで示したチャートはどれもが互いに相関しており、どれかが破綻すると、全てが破綻する。

So pay attention to the details.

というわけで詳細にこだわることだ。

As I stated above, my job, like every portfolio manager, is to participate when markets are rising. However, it is also my job to keep a measured approach to capital preservation.

これまで述べてきたことは、私の職務だ、どのポートフォリオマネージャも同様だ、相場が上昇しているときには参加する。しかしながら、もう一つの私の職務・責務は顧客の資産を保全する対策を講じることだ。

SO, why shouldn’t you show these charts to the bulls?

というわけで、どうしてこれらのチャートをブル派に見せるべきではないか?

というわけで、どうしてこれらのチャートをブル派に見せるべきではないか?

Because you need someone to “sell to” first.

それはまずはあなたが「売りつける相手」が必要だからだ。

それはまずはあなたが「売りつける相手」が必要だからだ。