Authored by Erik Lytikainen via RealInvestmentAdvice.com,

Mark Twain once said, “history doesn’t repeat itself, but it often rhymes.”

Since President Nixon removed the gold standard in the early 1970s,

gold has seen several significant rallies, all of which have similar

wave characteristics. Gold rallies seem to rhyme.

The first two price rallies began in 1971 and 1977, during and after

the de-linking of the U.S. dollar from gold. The most recent price rally

has its seeds in the dot-com bubble in the early 2000s. The chart

below shows two long-term monthly gold rallies, with the second rally

appearing to be an amplified but similar version of the first. I have

overlaid Fibonacci sequence numbers to demonstrate how the price of gold

has spiked upward in expanding, fractal waves during these prior

surges.

In the 1970s, gold traveled through four Fibonacci levels (by this

measure) in less than a decade after the removal of the gold standard.

From 2000 through 2012, amid the dot-com and housing bubbles, gold also

traveled through four Fibonacci levels on the way to $1,900.

If history rhymes again, and I believe it will, then the price of

gold will again spike upward through three or four Fibonacci extensions

to the upside, but then re-trace 50% to 70% of that upward move. If so, then the next upward spike could peak in the range between $7,000 and $11,000 per ounce. もし歴史がまたもや韻を踏むと言うなら、私はそれを信じているが、ゴールド価格はまたもや3度か4度フィボナッチレベルを超えて上昇するだろう、しかしその後その上昇も50%から70%後退するだろう。もしそうなるなら、次の上昇スパイクは$7,000から$11,000の間ということになる。

Investors tend to make rash decisions based on fear and greed. These

emotions are typically amplified during times of financial stress. It is

during such times that gold solicits fear and greed motivated buyers.

During a crisis, fear investors will rotate into gold to hold value, and

greed investors see the upward momentum and jump on the train. The

upward momentum of the next gold rally might feel like the Bitcoin surge

in 2017.

In baseball, its “three strikes and you’re out.” After the 1970’s

surge and blow-off top in 1980, gold failed three key technical tests.

After these failures, the gold market floundered for another decade.

Let’s take a closer look at those three technical failures.

First, in early 1983, gold failed to retake and hold the

psychologically important $500/oz price level. This rejection resulted

in sideways to lower movement for another year before gold failed again,

breaking below its upward trend line near $360/oz. After falling to a

low in early 1985, gold moved higher over the next three years, only to

fail a third key resistance test near $500/oz in late 1987. After

“striking out” in the 1980s, gold fell throughout the next decade back

to $250/oz.

Unlike the gold bear market of the 1980s, gold has been passing

periodic tests of support and resistance since its sharp decline in

2013. Gold’s price retracement from a high above $1,900 to a low near

$1,040 kept the price above a 61.8% Fibonacci retracement level as well

as the psychologically important $1,000 per ounce level.

The monthly wave structure of gold is bullish, and the price is now

trading above key resistance levels, with solid support at $1,379 and

$1,250. Even if the price of gold falls back to support at $1,250 per

ounce, the long term technical picture remains bullish. I view the

recent breakout over $1,380 to be significant and has likely opened the

door towards the $1,580 resistance area.

To the downside, technical breakdowns below $1,250 could lead the way

to $1,211 and $1,043. If history does indeed rhyme, a breakdown below

$1,043 could lead to another decade of futility. This downside scenario

does not appear likely, especially not with the uber-accommodative

interest rate policies worldwide. High U.S. dollar interest rates broke

the back of the gold rally in the 1980s, and there does not appear to

be any such risk of this happening again anytime soon.

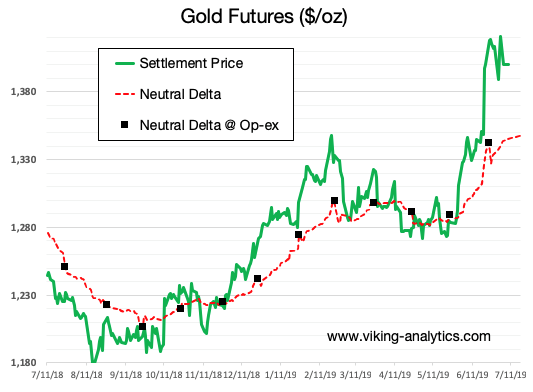

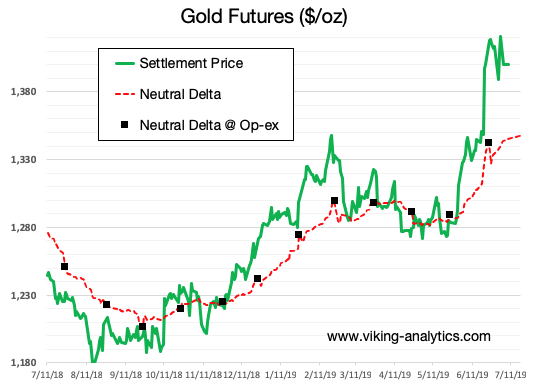

In addition to my longer-term view on gold, I also track shorter-term

price signals to locate areas of accumulation and/or hedging. An

indicator I developed shows a mean-reversion relationship between price

and the point of Neutral Delta in the options market. Essentially, the

point of Neutral Delta shows where the options market participants have

placed their bets and hedges. At the moment, Neutral Delta is near

$1,345 per ounce for the options which expire on July 25th.

When the price is over-bought in relation to Neutral Delta (as it is

now), we tend to see headwinds for further price increases.

Interpreting the current data, I am led to believe that the price of

gold will re-test the $1,380 price level before July 25th, and this will

give the options hedgers an opportunity to optimize their hedge book

ahead of the next few option expirations. A lower probability event

would be a price spike again towards $1,450 which would like force a

short-covering rally by the call option sellers who may already be

out-of-the-money.

If we are in the opening innings of a new rally in gold, a retest of

$1,380 or even $1,250 will represent great opportunities to buy or add

to your gold positions. You can learn more about my research by clicking this link: Introduction to Options Sentiment.

Gold can be best viewed as financial insurance. If you believe that

you should own insurance, then you should also own gold. In terms of

investment performance, gold will do best during times of international

financial stress. In the past, the price of gold has moved

exponentially higher during these periods as demand for the ultimate

safe haven goes viral.

The world is slowly but steadily transitioning from a U.S.

dollar-backed financial system to a multi-currency, multi-polar system.

One day, the leaders of our world will let the rest of us know the plan

for a modified financial system, and we will have to admit that we were

warned many times in advance. I expect that the gold price spike will

happen before, during, and after a new Bretton Woods-type conference.

While there are many signs that a new financial order is imminent, the

transition to this new financial order could take more time than many

have been led to believe.

From a short-term perspective, I use gold puts to protect my current

precious metal allocations. This is like purchasing insurance on the

value of my current insurance policy. It also helps preserve my wealth

allowing me to buy more gold if prices do in fact, drop to $1,380 or

$1,250.

Amazonで買物をしてContrarianJを応援しよう Albert Edwards: This Was The Final Recessionary Shoe, And It Has Now Fallen by Tyler Durden Thu, 06/27/2019 - 12:45 Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007... ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・ ... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions. ・・・市場は準混乱状態になった、というのも歴史的に見てイールドカーブ反転が過去7回の景気後退の前兆となっているからだ。 However, while the inversion was certainly a memorable event, the question on everyone's lips is how do risk assets perform once the curve flattens and/or inverts. According to backtests from Goldman, since the mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. ...

China Injects Gargantuan 1.1 Trillion In Liquidity This Week by Tyler Durden Wed, 01/16/2019 - 22:19 Following what Bloomberg calculated was a record net reverse repo liquidity injection on Wednesday, when the PBOC injected a whopping 560 billion yuan of liquidity into the financial system via open market operations, the Chinese central bank has done it again and in Thursday's open market operation, it sold 250BN yuan in 7 Day repos (slightly below yesterday's record 350BN), and 150BN in 28 Day repos, which net of maturities resulted in a whopping net 380BN yuan ($56.2BN) liquidity injection. ブルームバーグの算出によると水曜に記録的なリバースレポ流動性注入が行われた、PBOCがなんと公開市場操作で金融システムになんと560B人民元を注入した、中国中央銀行は再び木曜に公開市場操作を行った、250B人民元の7日決済レポを売却した(昨日の350B人民元よりも少し少ない)、そして28日決済のレポを150B人民元注入した、結果としてなんと380B人民元($56.2B)の流動性注入となる。 (訳注:なんか足し算すると辻褄が合いません、ブルーム...

"Clueless Wizards" - Don't Worry, The Fed Has "Belts & Suspenders" by Tyler Durden Tue, 05/26/2020 - 12:25 Authored by Mike Shedlock via MishTalk, The Fed's balance sheet is approaching $7 trillion dollars. This is what Bernanke meant by suspenders. FEDのバランスシートは$7Tに迫っている。これこそBernankeがサスペンダーにたとえたものだ。 On February 27, 2013, Ben Bernanke spoke to US Congress about how the Fed would unwind its balance sheet. 2013年2月27日に、Ben Bernankeは米国議会証言でFEDが如何にバランスシート巻き戻しをするかの証言を行った。 Bernanke said, We Have “Belts, Suspenders” to Unwind Balance Sheet . Bernankeが言うには、我々はバランスシート巻き戻しのための「ベルトもサスペンダー」も有るという。 Bernanke’s vague answer to Sen. Richard Shelby, R-AL, when asked how the Fed will deleverage the balance sheet, was this: “ In terms of e...