While

the western world (and much of the eastern) has been preoccupied with

predicting the consequences of Trump's accelerating global trade/tech

war and whether the Fed will launch QE before or after it sends rates

back to zero, Beijing has quietly had its hands full with avoiding a

bank run in the aftermath of Baoshang Bank's failure and keeping the

interbank market - which has been on the verge of freezing - alive.

Unfortunately for the PBOC, Beijing was racing against time to

prevent a widespread panic after it opened the Pandora's box when it

seized Baoshang Bank, the first official bank failure in an odd replay

of what happened with Bear Stearns back in 2008, when JPMorgan was

gifted the historic bank for pennies on the dollar.

As a reminder, back in May, shortly after the shocking failure of

China's Baoshang Bank (BSB), and its subsequent seizure by the

government - the first takeover of a commercial bank since the Hainan

Development Bank 20 years ago - the PBOC panicked and injected a

whopping 250 billion yuan via an open-market operation, the largest

since January. Alas, as we said at the time, it was too little to late,

and with the interbank market roiling, with Negotiable Certificates of

Deposit (NCD) and repo rates soaring (in some occult cases as high as 1000%) we said that it's just a matter of time before another major Chinese bank collapses.

5月末のことを思い起こすと、中国のBaoshang Bank (BSB)破綻とその後の国有化後ーーこれは20年前の海南開発銀行以来初めての商業銀行国有化だったーーPBOCはパニクってなんと250B人民元を公開市場操作で金融システムに注入した、今年最大の量だった。なんということか、当時ZeroHedgeが書いたが、これは too little to lateであり、インターバンク市場を揺るがした(金利がオカルト的な数字1000%にもなった)ZeroHedgeはこれをみて次の中国での大型銀行倒産は時間の問題だと書いた。

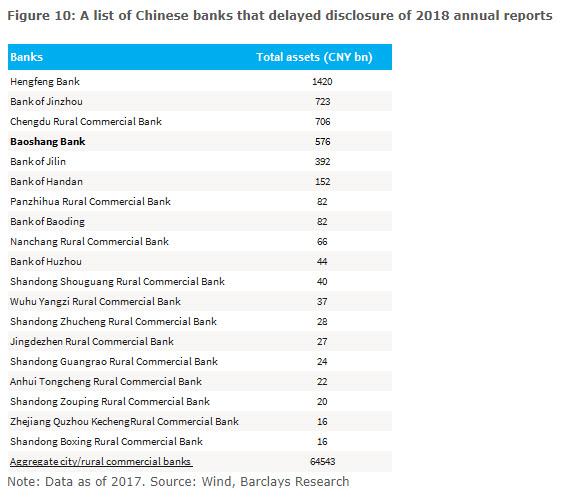

And, in order to present the list of the most likely candidates, will

picked those names that - just like Baoshang - had delayed publishing

their latest annual reports, the biggest red flag suggesting an upcoming

solvency "event." The list is below.

We were right, because not even two months later, the second biggest bank on the list, Bank of Jinzhou has crawled in Baoshang's foosteps and is about to be seized by the government. ZeroHedgeは正しかった、というのもその二月後に、この表の二番手の銀行、錦州銀行がBaoshangの後をたどっている、まさに国有化されんとしている。

According to Reuters and Bloomberg,

Bank of Jinzhou recently met financial institutions in its home

Liaoning province to discuss measures to deal with liquidity problems,

and in a parallel bailout to that of Baoshang, the bank was in talks to

"introduce strategic investors" after a report that China’s financial

regulators are seeking to resolve its liquidity problems sent its

dollar-denominated debt plunging.

Officials including those from the People’s Bank of China and China

Banking and Insurance Regulatory Commission recently held a meeting with

financial institutions in Bank of Jinzhou’s home province of Liaoning

to discuss measures to resolve the lender’s liquidity issues, Reuters

reported Wednesday.

In response to market fears the bank issued a statement on Thursday

that "currently, Bank of Jinzhou’s business operations are normal

overall,” which however did not refer to its liquidity situation. "Recently,

the bank’s board of directors and some major shareholders have been in

talks with several institutions that wish to and have the ability to to

become strategic investors" adding that talks have been “going smoothly.”

By strategist investors it of course meant banks, backstopped by the

government, who would "absorb" the bank, effectively nationalizing it a

la what happened with Baoshang. The only question is whether

stakeholders would also be impaired.

As we reported in June, Jinzhou’s Hong Kong-listed shares have been

suspended since April after it failed to disclose its 2018 financial

statements; adding to its woes, its auditors Ernst & Young Hua Ming LLP and Ernst & Young resigned. As the bank - which first got in hot water in 2015 over its exposure to the scandal-ridden Hanergy Group -

wrote in a filing on the Hong Kong Stock Exchange, E&Y was first

appointed as the auditors of the Bank at the last annual general meeting

of the Bank held on 29 May 2018 to hold office until the conclusion of

the next annual general meeting of the Bank. That never happened,

because on 31 May 2019, out of the blue, the board and its audit

committee received a letter from EY tendering their resignations as the

auditors of the Bank with immediate effect.

6月にZeroHedgeが報告したように、錦州銀行の香港上場株は2018年決算開示をしていないために4月以降売買停止状態だ;さらに残念なことに、監査法人、 Ernst & Young Hua Ming LLP and Ernst & Young、は監査を辞退した。当行によると、ーー最初は2015年にスキャンダルまみれのHanergy Groupに巻き込まれて煮え湯を飲んだーー香港証券取引所の記録によると、E&Yは当行の監査法人として2018年5月29日に指名されその後一年間の監査を任された。しかしこれはかなわなかった、というのも2019年5月31日、突然、取締役会と監査委員会はEYから直ちに監査法人を辞退するという通告を受け取った。

The reason for the resignation: the bank refused to provide

E&Y with documents to confirm the bank's clients were able to

service loans, amid indications that the use of proceeds of certain

loans granted by the Bank to its institutional customers were not

consistent with the purpose stated in their loan documents.

As a result, "after numerous discussions and as at the date of this

announcement, no consensus was reached between the Bank and EY on the

Outstanding Matters and the proposed timetable for the completion of

audit." At this time, the bank also requested the trading in the H

shares (which was frozen on April 1) on The Stock Exchange of Hong Kong

Limited to be suspended until the publication of the 2018 Annual

Results, which will likely never come.

There is another reason why this particular failure is notable: Bank

of Jinzhou is the second-most reliant on interbank financing,

particularly non-bank financial institutions’ deposits, among more than

200 local banks, according to UBS analyst Jason Bedford said when

reached by phone on Thursday.

Which explains its failure: just last month we reported that China's interbank market, especially for smaller banks, had effectively frozen.

It was therefore only a matter of time before other banks reliant on it

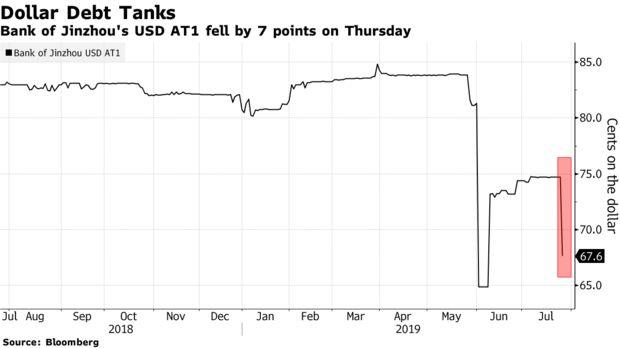

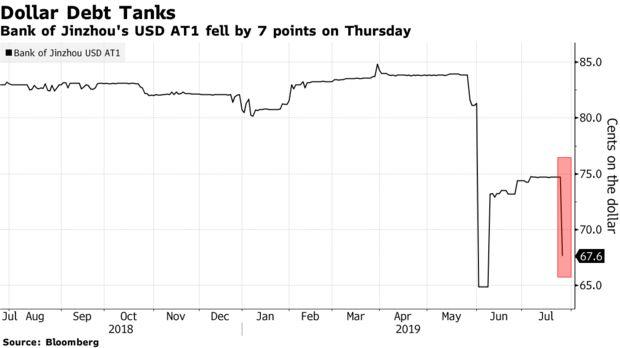

for funding threw in the towel, as Jinzhou has now done. To wit,

Jinzhou's Its dollar-denominated loss-absorbing debt instruments, known

as AT1 bonds, plunged near all time low...

... while the bank’s seven negotiable certificates of deposits -

which would be taken over by another, bigger bank when (if) the bank is

seized and bailed out, were indicated at yields ranging from 3%-5.5% on

Thursday, higher than valuations of 2.8%-3.45%.

Incidentally, back in early June when first reporting on the

resignation of the bank's auditors, we said that "the real question

facing Beijing now is how quickly will Bank of Jinzhou collapse,

how will Beijing and the PBOC react, and what whether the other banks

on the list above now suffer a raging bank run, on which will certainly not be confined just to China's small and medium banks."

The answer: less than 2 months.

Unfortunately for China, it won't stop there. As a reminder, China’s

smaller lenders have been under growing scrutiny since Baoshang Bank's

failure and takeover which led to a sharp repricing of risk for much of

China’s banking system which had long operated under an assumption that

policy makers would support firms in trouble.

"We expect the regulators to step up their support if more financial

institutions run into liquidity issues,” said Becky Liu, head of China

macro strategy at Standard Chartered Plc, who declined to comment

directly about Bank of Jinzhou. "Over time, the cost of funding between

the stronger and weaker financial institutions will see further

divergence."

Amazonで買物をしてContrarianJを応援しよう Silver Outperforming Gold 2 Adam Hamilton July 26, 2019 3232 Words Silver has blasted higher in the last couple weeks, far outperforming gold. This is certainly noteworthy, as silver has stunk up the precious-metals joint for years. This deeply-out-of-favor metal may be embarking on a sea-change sentiment shift, finally returning to amplifying gold’s upside. Silver is not only radically undervalued relative to gold, but investors are aggressively buying. Silver’s upside potential is massive. ここ2週シルバーは急騰した、ゴールドを遥かに凌ぐものだ。これは注目すべきことだ、もう何年もシルバーはひどいものだった。この極端に嫌われた金属が大きく心理を買えている、とうとうゴールド上昇を増幅するに至った。シルバーは対ゴールドで極端に過小評価されているだけでなく、投資家は積極的に買い進んでいる。シルバーの潜在上昇力は巨大なものだ。 Silver’s performance in recent years has been brutally bad, repelling all but the most fanatical contrarians. Historically silver prices have been mostly ...

結局、中国は隣国日本で20年前に起きたことを学んでいなかったということでしょう、というかどの国もどの政府も十分成熟するまでは「わかっちゃいるけどやめられない」ということでしょうね、きっと。 Spooked By Apple? Wait ‘Til China’s Bubble Bursts Written by Jesse Colombo | Jan, 3, 2019 Apple stock plunged nearly 10% on Thursday after the company cut its revenue forecast due to slowing iPhone sales in China. Apple’s woes dragged U.S. stock indices lower by more than 2% as fears of a more extensive China-driven slowdown spread. アップルの株価は火曜に約10%下落した、同社が中国でのiPhone売上原則を予想したためだ。アップルの弱さが米国株式指数を2%以上押し下げた、中国主導でさらなる原則が広がるのではという懸念からだ。 From the New York Times : ニューヨークタイムスによると: For years, no matter what was happening elsewhere, global companies bet billions upon billions of dollars that China’s consumers would keep spending money. 長年、他国で何が起きようとも多国籍企業は中国消費は巨額を維持することに賭けてきた。 Now, just when the world economy could use their financial firepower, they are no longer so quick to open their wallets. 今や、世界経済が金融弾薬を用いてももはや彼らの財布を緩めることはできない。 The latest sign of a slowdown in...

Gold Stocks Surge Higher Adam Hamilton February 22, 2019 2932 Words The gold miners’ stocks surged strongly this week, blasting to new upleg highs. The mounting gains are naturally driving more interest in this small contrarian sector, shifting sentiment towards bullish. Despite their accelerating rally, gold stocks still remain fairly low technically and deeply undervalued relative to gold. So their strengthening upleg likely has plenty of room to run considerably higher in coming months. 今週金鉱株は力強く上昇し新高値となった。上昇が積み上がりこの小さなコントラリアンセクターはさらに注目を集めている、これが心理を強気なものにする。ラリーが加速するが、金鉱株はテクニカル的にはまだ安値で、対ゴールドでとても過小評価されている。というわけで力強い上昇は今後数ヶ月まだかなりな上昇余地がある。 The gold miners’ stocks are ultimately leveraged plays on gold, which overwhelmingly drives their profits. The much-maligned yellow metal has enjoyed a strong upleg since mid-August, when record gold-futures s...

Barrick’s average quarterly production since Q4’16 plunged an astounding 8.6% YoY. The reason Barrick’s management blew $6.5b in stock buying Randgold is they desperately needed more production to mask the precipitous drop in their own. Barrick’s total 2018 production of 4525k ounces was 18.0% below the 5516k it mined only a couple years earlier in 2016. At best adding Randgold just regains those losses. Barrickの平均四半期生産は2016Q4以来なんとYoYで8.6%下落している。Barrickの取締役が$6.5Bも投じてRandgoldの株式を購入した理由は、彼らはなんとしても急落する自らの生産量を隠すために生産量増加としたかったからだ。Barrickの2018全生産量は4525Kオンスで、わずか2年前の5516kオンスから18.0%も少ない。Randgoldを買収したところでこの下落を補うに過ぎない。 And GOLD has been suffering the same production struggles as ABX. Over its past 4 reported quarters, Randgold’s gold mined has fallen an average of 7.4% YoY. Can bringing two rapidly-depleting major gold miners together magically make a stronger one? I doubt it. Barrick’s reported production will enjoy a big temporary boost...

Gold Miners’ Profits to Soar Adam Hamilton October 18, 2019 2741 Words The gold miners are likely to report blowout profits in this spinning-up Q3’19 earnings season. Higher production, stable costs, and much-higher gold prices should combine for some super-impressive results. That’s going to leave the still-undervalued gold miners much more attractive fundamentally, supporting bigger capital inflows and much-higher stock prices. Q3 should prove the gold miners’ best quarter in years. 金鉱会社は2019Q3決算で巨額の収益を報告する可能性が高い。生産量が高く、コストは安定し、ゴールド価格高騰が重なり、素晴らしい決算報告となりはずだ。まだ過小評価の金鉱株がファンダメンタルズ的により魅力的になりつつある、こうなるとさらなる資金を呼び込み株価は高まるだろう。Q3は一年でもっとも良い四半期となるはずだ。 Stock prices are ultimately dependent on underlying corporate earnings. Over the long term all stock prices gravitate towards some reasonable multiple of their underlying companies’ profits. Herd greed and fea...