Authored by Mike Shedlock via MishTalk,

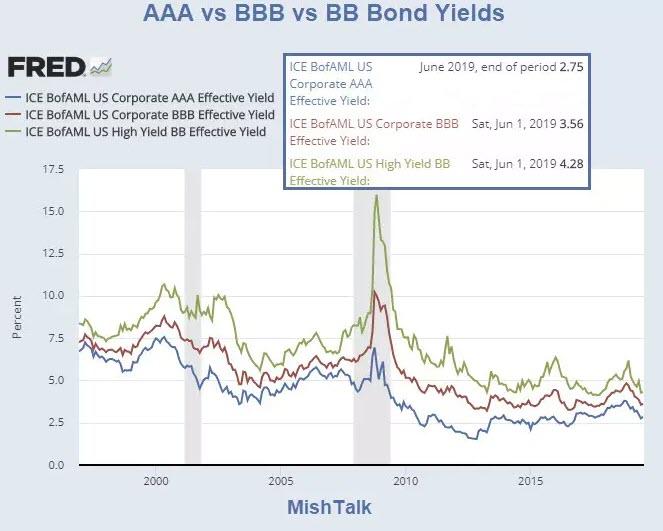

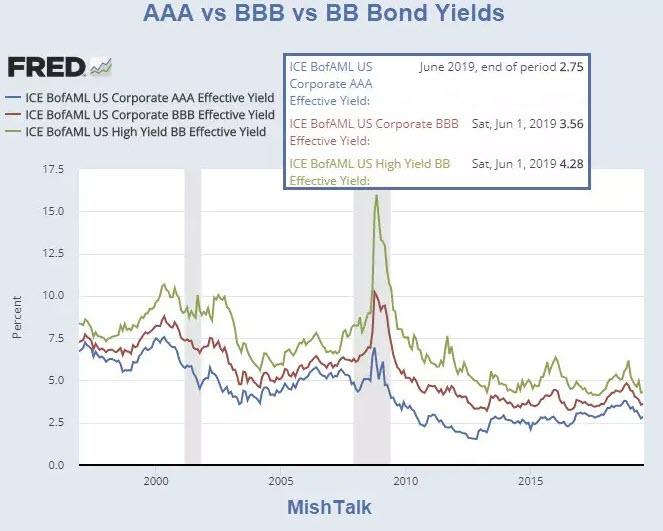

The widely discussed "everything bubble" is, in reality, a corporate junk bond bubble on steroids sponsored by the Fed...

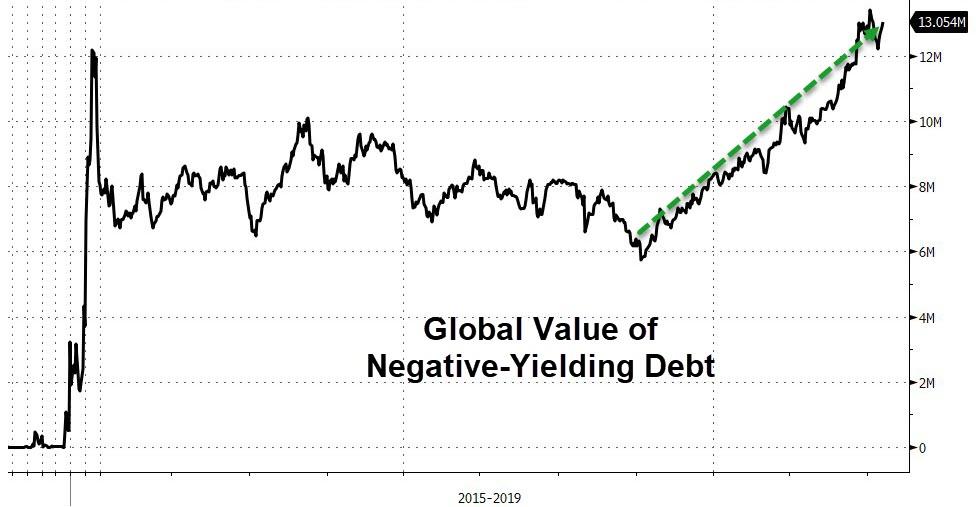

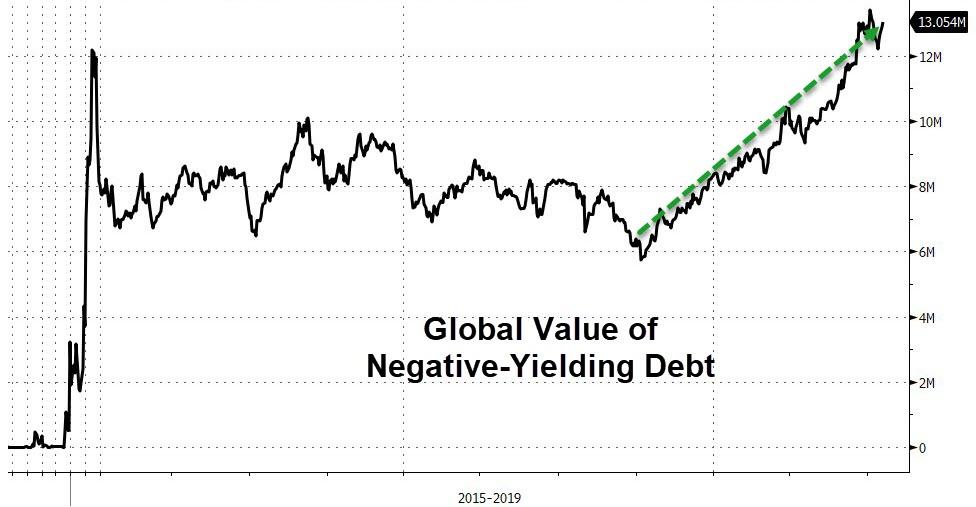

From a low last October of just under USD 6 trillions the value of

the Bloomberg Barclays Global Aggregate Negative-Yielding Debt Index has

more than doubled, increasing in value by over USD 7 trillions over the

last 8 months to establish an all-time record of USD 13.2 trillions

earlier in late June.

昨年10月の最小時にはマイナス金利債権の量はUSD 6T以下であった、このデータはBloomberg Barclays Global Aggregate Negative-Yielding Debt Indexによるものだ、これが現在倍になっている、過去8か月でUSD7Tも増えたのだ、その結果6月遅くには過去最高の USD 13.2Tになった。

The current situation is a manifestation of the inability of global

financial markets to emerge from the era of ultra-low bond yields that

central banks engineered in the wake of the global financial crisis.

Non-conventional policies pursued by central banks in recent years

have lead neither to a rise in sluggish rates of economic growth nor to

an end in the disinflationary trends within the global economy.

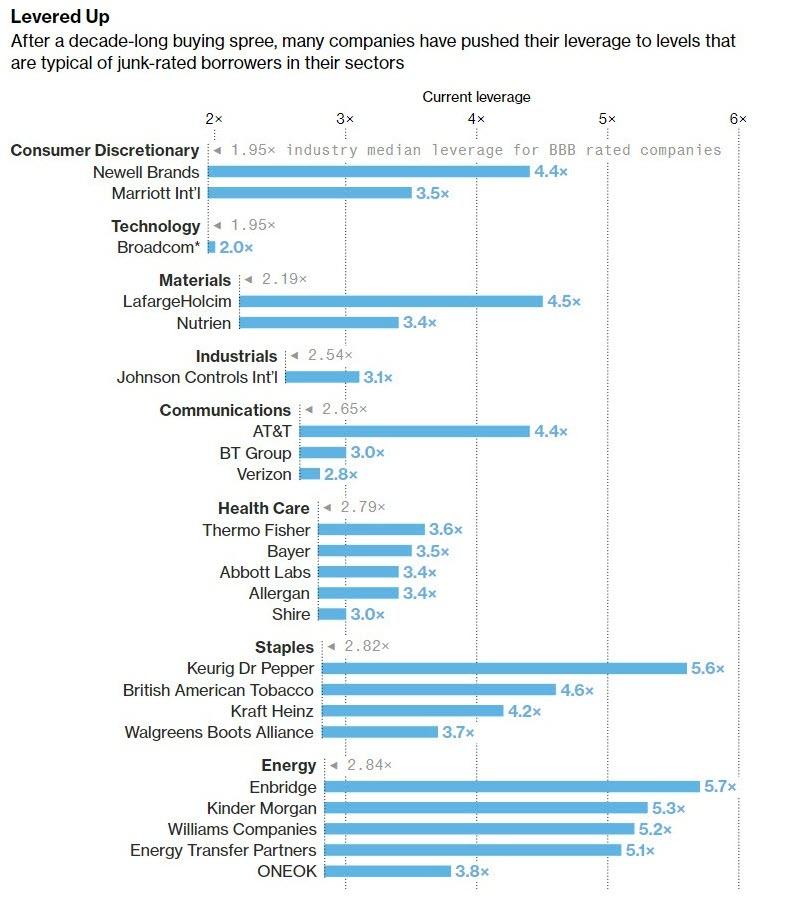

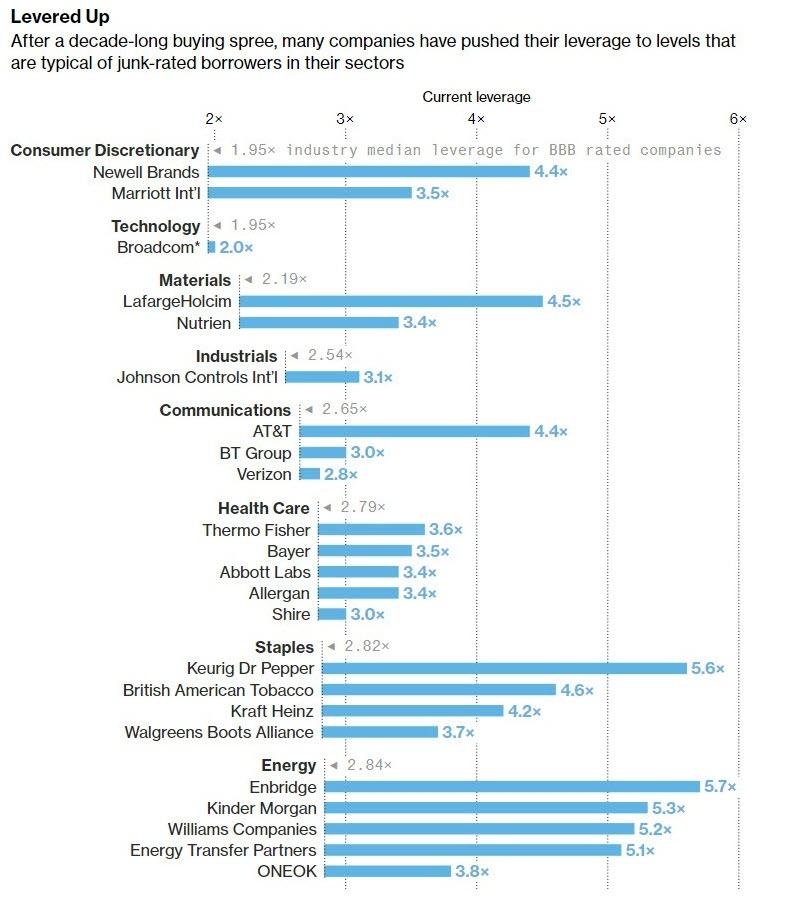

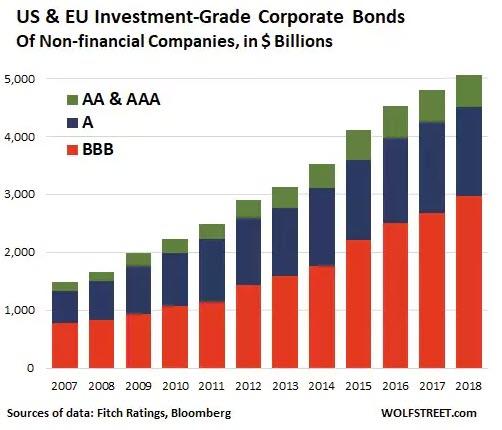

After a decade-long buying spree, many companies have pushed their

leverage to levels that are typical of junk-rated borrowers in their

sectors.

もう10年も買いの度が過ぎて、多くの企業は自らの債権をそのセクタのジャンク級にまでしている。

Bloomberg News delved into 50 of the biggest corporate acquisitions

over the last five years, and found more than half of the acquiring

companies pushed their leverage to levels typical of junk-rated peers.

But those companies, which have almost $1 trillion of debt, have been

allowed to maintain investment-grade ratings by Moody’s Investors

Service and S&P Global Ratings.

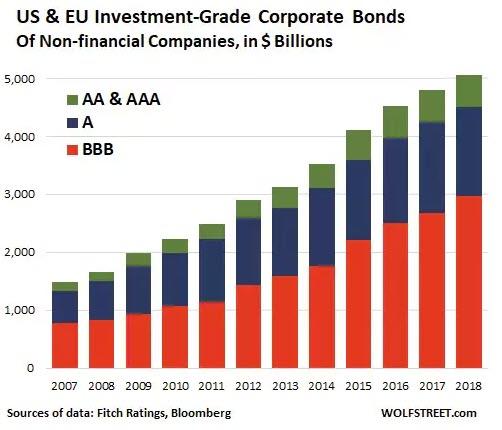

This M&A-fueled leveraging of corporate balance sheets

contributed to a surge in debt rated in the bottom investment-grade tier

and now represents almost half of the outstanding market, Bloomberg

Barclays index data show.

Wolf Richterはこう解説する、BBB格付け企業が「ジャンク級」への格下げ回避を試みたときに何が起きるか。

In the next downturn, many bonds in the BBB-category will transition

to junk, and many junk bonds but also some investment-grade bonds – if

the past is any guide – will transition to default. Two-notch downgrades

are not uncommon: one day you wake up, and your “BBB” investment-grade

bond is a “BB+” junk bond.

To avoid a downgrade to junk, companies will try to shore up their

balance sheet. This means curtailing or stopping share buybacks and

slashing dividends.

This is a process GE went through. After blowing nearly $14 billion

on share buybacks in the four years through 2017 to prop up its shares,

GE stopped on a dime and transitioned to dismembering itself to pay down

debts. The share buybacks stopped cold. Then it slashed its dividends

to near-zero. And its shares have plunged.

GE now sports a credit rating of “BBB+” with negative outlook, three

notches from junk, after getting hit by a round of two-notch downgrades

late last year. Despite having already cut off some major limbs to

reduce its debts, GE still has $97 billion in long-term debt. And GE is

still trying hard to dodge further downgrades.

In the latest sign of financial markets going into uncharted

territory, more than a dozen junk bonds, which usually carry high

yields, now trade in Europe with a negative yield.

There are about 14 companies with junk bonds worth more than €3

billion ($3.38 billion) that are trading with negative yields, according

to Bank of America Merrill Lynch. They include telecom giant Altice

Europe NV and tech-equipment company Nokia Corp.

マイナス金利のジャンク・ボンドが14社で€3B($3.38B)にもなる、Bank of America Merrill Lynchのデータによる。その中には、テレコム巨人のAltice Europe NVやテック企業Nokiaも含まれる。

Everything Bubble

なんでもバブル

Stocks 株式

Bonds 債権

Consumer Confidence 消費者信頼

Buybacks 自社株買い

Faith in Central Banks 中央銀行への信頼

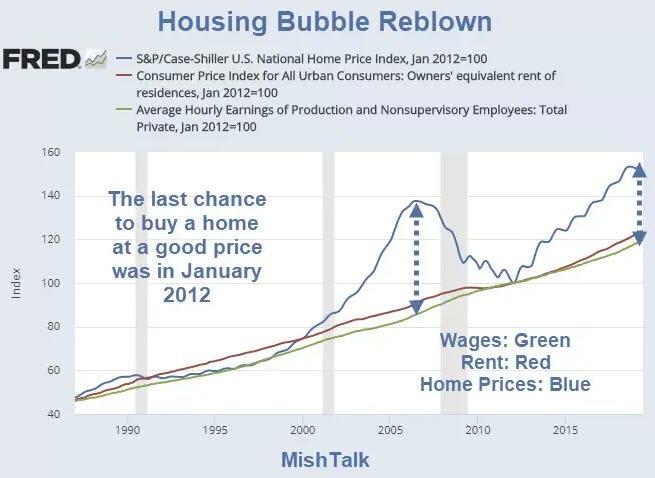

The "everything bubble" has at its roots central bank policy of yield suppression.

Central banks made it easy for corporations to borrow money for

leverage buyouts, to buy back shares, and for zombie corporations to get

enough funding to stay alive.

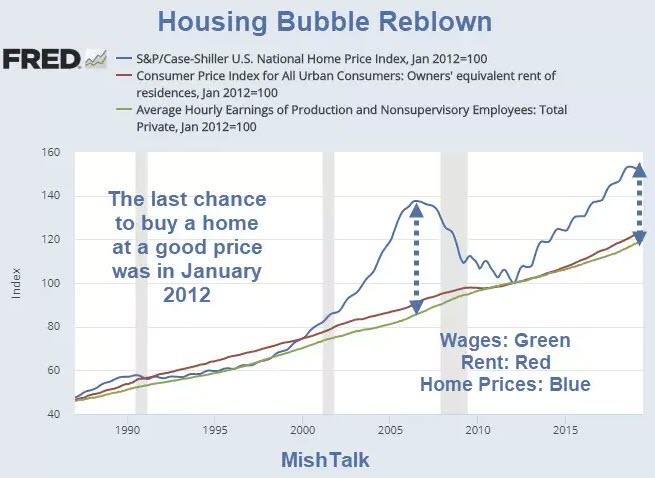

Investors (speculators actually), especially retiring boomers, are as

optimistic as they were in 2007 when they viewed their own house as a

retirement vehicle, not a place to live.

Investor faith in central banks has never been higher.

投資家の中央銀行への信頼がここまで高かったことはない。

At the individual level, baby boomers see the stock market is up so they buy a car and have a nice vacation.

個人レベルで見ても、団塊の世代は株式は上昇するものだと思い込み、車を買いバケーションを享受する。

Corporations borrow money to buy back their own shares or to make insanely leveraged buyouts.

企業は借金して自社株買いを買う、もしくは不健全なレバレッジドバイアウトを行う。

Hedge funds buy low-yielding junk bonds in belief yields will get even more ridiculous.

ヘッジファンドは低金利のジャンク・ボンドを買う、もっと高値で買う人がいると信じてのことだ。

Deflation Coming

収縮が来る

The Fed is hell bent on producing inflation. The sad part is they do

not now how to measure it. Inflation is all around us: In junk bonds, in

equities, and in home prices.

Class 8 Heavy Truck Orders Crash 68% in January by Tyler Durden Wed, 02/06/2019 - 17:25 Among the latest dismal news about the strength of the US economy, on Tuesday ACT Research released preliminary truck orders for January 2019 which showed that Class 8 truck orders collapsed an astounding 68% for January. The decline is being attributed to a 300,000+ vehicle backlog potentially prompting fleets to halt purchases in the near term. 米国経済に関し最近憂鬱なニュースが多い中で、火曜にACT researchが2019年1月のトラック発注を開示した、1月にClass 8のトラック発注がなんと68%も急落した。この発注減は短期的に300,000台超の潜在在庫を生み出す。 Specifically, in January Class 8 net orders were 15,800 units (14,700 SA; 176,400 SAAR), down 68% YoY and down 26% MoM. Class 5- 7 January net orders were 23,400...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...

中国が債務増加していることはたしかです。ただ日本の例を日銀資金循環報告でみると家計、320兆円、民間非金融機関1,785兆円、一般政府 1,284兆円となります。合算すると3,300兆円にもなり、GDPの600%を超えています。 https://www.boj.or.jp/statistics/sj/sjexp.pdf この記事の統計と同じ考え方で数値を採用しているのかどうか気になります。 加えて、この資金循環報告に書かれている海外資産というのが内数なのか外数なのか?私にはよくわかりません。当然海外債務も結構な額になります。一度日銀資金循環 図表1を見てください。詳しい方に教えていただければ。 この中国のたどる道は昔のソ連とかMMTと同様で、自国通貨ならいくら発行しても倒産はしない、というか為政者が痛みに耐えることができず緩和を続けるというものです。でも最終的には限界点に達します。ソ連は建国から崩壊まで70年かかりました。 自由主義経済なら立ち行かなくなった企業は退場してもらうというのが減速なのですが、これがうまくゆかないわけです。 でも日本は中国のはるか先を言っているように見えます。ちょっと検索したのですが、日本の債務に関しては政府債務に言及したものばかりで、この記事のように民間、個人まで総合的に記載しているのは日銀の資金循環統計しか見つけることができませんでした。 China Continues To Pile Debt On Top Of More Debt Written by Jesse Colombo | Feb, 27, 2019 Like many countries, China attempted to rein in its debt growth over the past couple years, but ultimately gave up and is now back to piling on even more debt. Bloomberg reports – 多くの国と同様に、中国もここ2年ほど債務増加を抑えようとしてきた、しかし結局の所諦めてしまい、今や更に債務を積み上げている。ブルームバーグ記事ーー For almost two years,...

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...