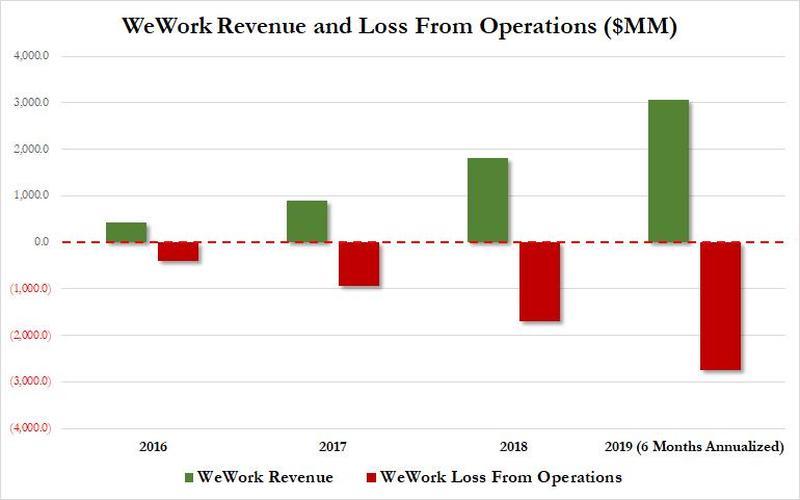

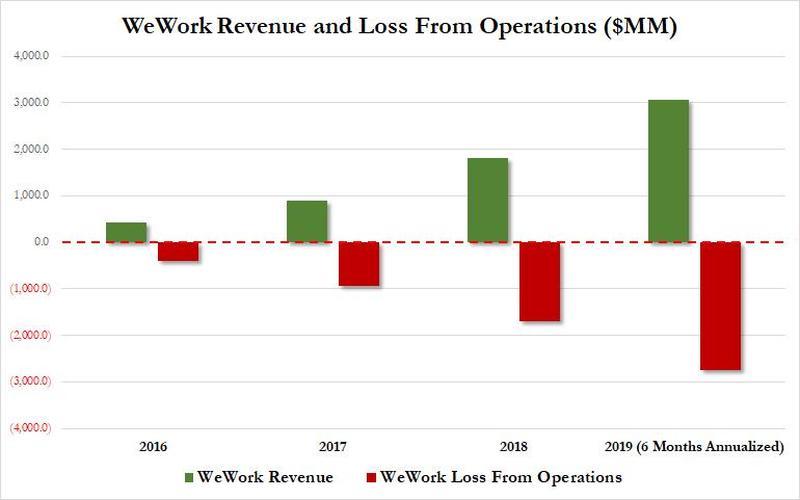

We noted last

month that the company lost $690 million in the first six months of the

year and is expected to generate a loss from operations approaching $3

billion as it burns through tens of millions in cash daily. Analyst

estimate that the company could run out of money by mid-2020.

And now Bloomberg is reporting that WeWork's cash crunch is even more acute:

今日のブルームバーグの報告によるとWeWorkの資金枯渇はもっと差し迫るという:

Analysts had previously estimated that the company would run out of money by the middle of next year.

WeWork had been counting on an initial public offering -- and a $6

billion loan contingent on a successful IPO -- to meet its cash needs,

but that plan unraveled amid questions about its future profitability...

...it needs new financing before the end of November to avoid running out of money, two people familiar with the matter said.

・・・資金枯渇を回避するには11月末までに新たな資金提供元が必要だ、二人の情報通が言う。

FT sources are now indicating that a potential lifeline, otherwise known as a bailout, could be imminent. FTの情報源は現在潜在的な救済元だ、ほかでもない緊急援助、これが差し迫っている。

The bailout of WeWork could be led by JPMorgan Chase and other Wall

Street banks. If no cash infusion by late November, WeWork could enter

into bankruptcy in 1H20, or by next summer.

Global credit rating agency Fitch Ratings downgraded WeWork's credit

rating last week by two notches to "CCC+," putting the SoftBank funded

office-sharing company very deep into junk territory.

"In the absence of an IPO and associated senior secured debt

raise, WeWork does not have sufficient funding to meet its growth plan," Fitch wrote in a note.

Last month's decision to abandon the IPO deprived the company of $3

to $4 billion in funding and $6 billion in a loan package investment

banks promised if it went public.

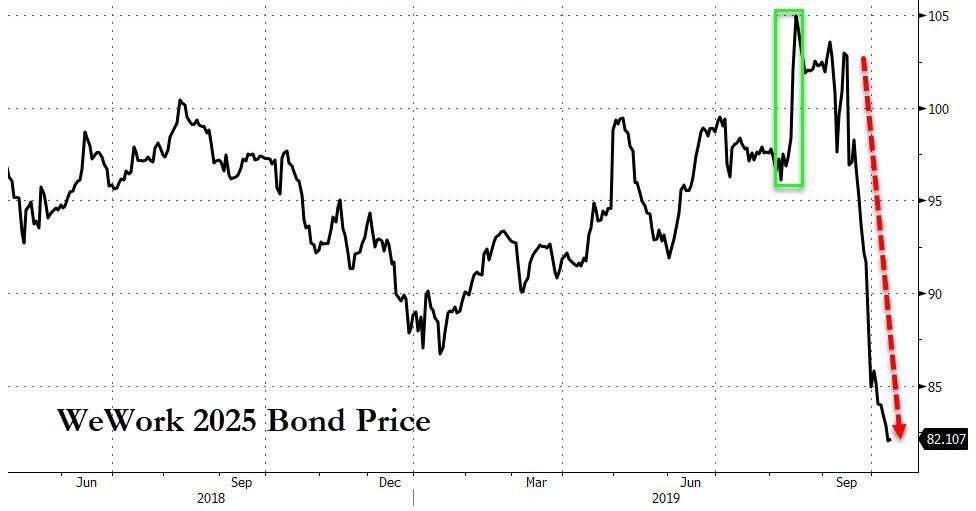

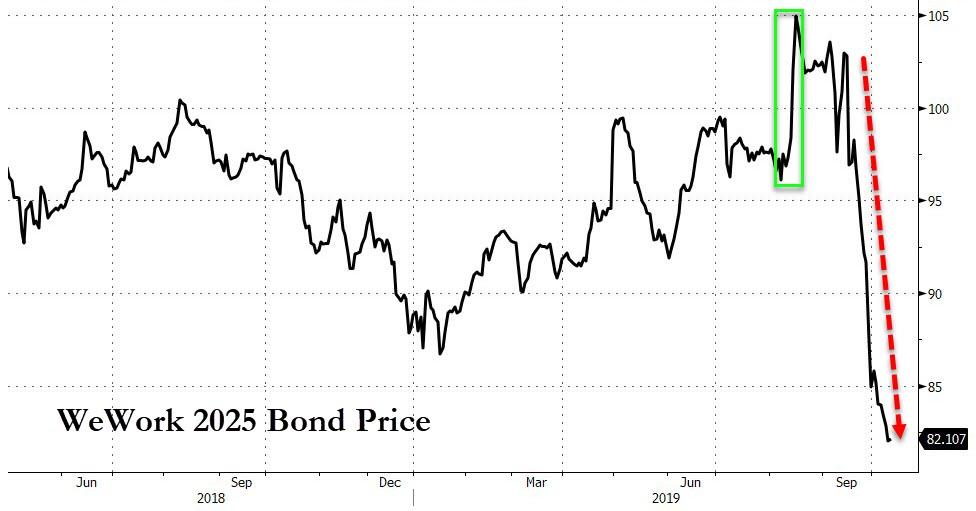

Since the IPO was pulled and valuations collapsed, WeWork's WE 7.875 01-MAY-2025 junk

bond was last trading at about 82 cents on the dollar (as of Friday 6

am est., according to Tradeweb data, a massive discount to face value,

which indicates doubts the company can repay its debts.

IPOがなくなり、格付けも崩壊し、WoWorkの WE 7.875 01-MAY-2025ジャンクボンドは直近で82セントで売買されている、額面1ドル(東部時間金曜6am、Tradewebのデータだ、額面から大幅に値引きされている、ということは当社が債務を返済できないだろうと見られている。

Without new cash, WeWork is unsustainable; the company could start

liquidating its CRE exposure as it begins the inevitable pre-bankruptcy

shrinking process -- if no cash infusion next month.

"WeWork has raised more than $12 billion to rent office space that it

renovates and then leases to companies. But that strategy has left it

in a precarious position. It has some $47 billion of future rent payments due. On

average it leases its buildings for 15 years. Yet its tenants are

committed to paying only $4 billion, and on average have leases for 15

months."

「WeWorkは$12B以上の資金を投じてオフィススペース改装を行い企業に貸し出す。しかし その戦略は心もとないものだ。将来の賃貸料収入は$47B程度だ。平均してビルを15年貸し出す。しかしながら、テナントが約束する支払いはわずか$4Bだ、そして平均貸し出しは15ヶ月に過ぎない。

With the equity market window shut, and credit markets starting to crack, something that we noted on Thursday, the next question is if WeWork gets a bailout next month.

If not, the WeWork implosion of 2020 could be a spectacular mess and a massive headache for SoftBank/Vision Fund and Wall Street banks - as the company crashes from $47 billion valuation to insolvent in 2 months...

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...