Back

in the days of the Fed's QE, much of thinking analyst world (the

non-thinking segment would merely accept everything that the Fed did

without question, after all their livelihood depended on it), was

focused on how massive, and shocking, the Fed's direct intervention in

capital markets had become. And while that was certainly true, what we

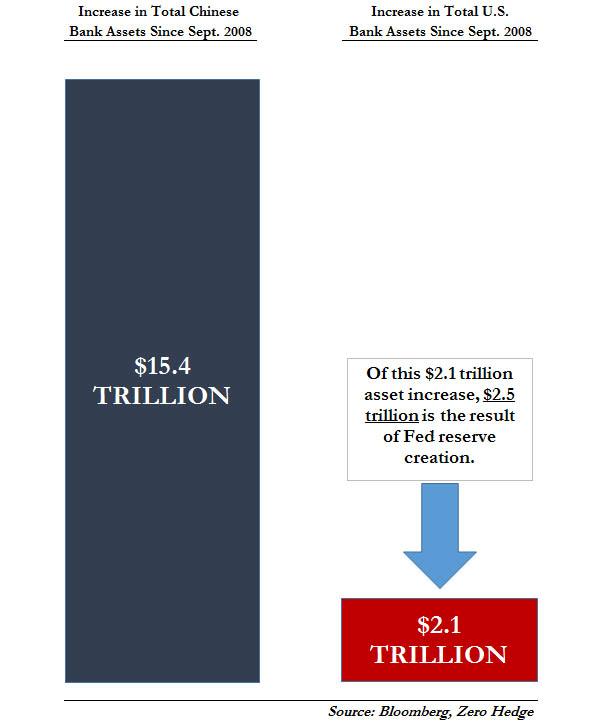

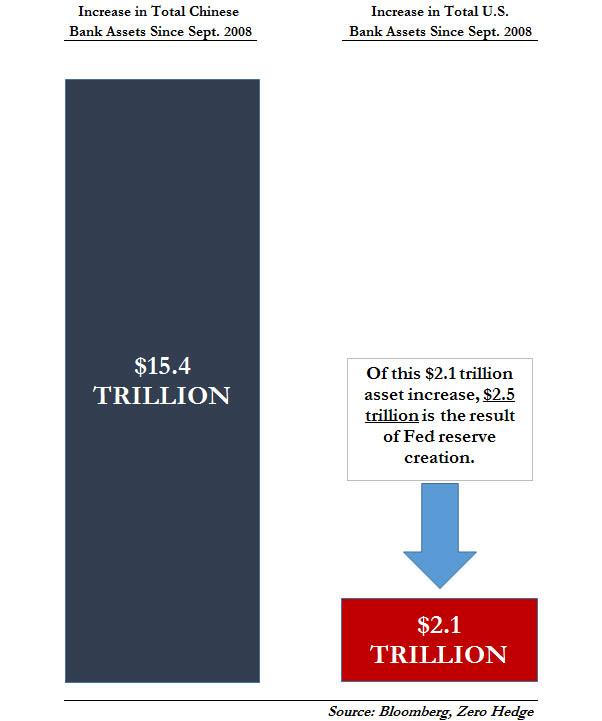

showed back in November 2013 in "Chart Of The Day: How China's Stunning $15 Trillion In New Liquidity Blew Bernanke's QE Out Of The Water"

is that whereas the Fed had injected some $2.5 trillion in liquidity in

the US banking system, China had blown the US central bank out of the

water, with no less than $15 trillion in increases to Chinese bank

assets, all at the behest of a juggernaut of new credit creation - be it

new yuan loans, shadow debt, corporate bonds, or any other form of debt

that makes up China's broad Total Social Financing aggregate.

FEDがQEを行っていた頃、思慮深いアナリストは(何も考えない人たちは疑問を持つことなくFEDのすることをすべて受け入れていた、結局彼らの生計はFEDに依存しているにすぎない)、それが如何に大きいか、またショッキングな出来事であるかに注目していた、FEDが直接資本市場に介入してきたわけなので。そしてそれはたしかに本当だったが、ZeroHedgeは2013年11月にこういう記事を示した「Chart of the Day: 中国はなんと$15Tの新規流動性を投入しBernankeのQEを打ちのめした」、FEDの流動性注入はわずか$2.5Tだったが、中国は米国中央銀行を打ちのめして、なんと$15Tもの流動性注入を行っった、圧倒的な新規与信生成によるものだったーー新たな人民元貸付、シャードー債務、企業債権、そのたあらゆる方法を駆使して中国の幅広い「社会融資総量 Total Social Financing」を積み上げた。

Now, almost six years later, others are starting to figure out what

we meant, and in an Op-Ed in the FT, Arthur Budaghyan, chief EM

strategist at BCA Research writes about this all important topic of

China's "helicopter" money - which far more than the Fed, ECB and BOJ -

has kept the world from sliding into a depression, and yet is blowing

the world's biggest asset bubble.

Budaghyan picks up where we left off, and notes that over the past decade, Chinese

banks have been on a credit and money creation binge, and have created

RMB144Tn ($21Tn) of new money since 2009, more than twice the amount of

money supply created in the US, the eurozone and Japan combined over the

same period. In total, China’s money supply stands at Rmb192tn, equivalent to $28 TRILLION.

Why does this matter? Because Chine money's supply is the size of broad

money supply in the US and the eurozone put together, yet China’s

nominal GDP is only two-thirds that of the US.

This, as the BCA analyst explains, is a major problem.

BCAアナリストの解説では、これが大きな問題だ。

Below we repost his latest FT Op-Ed, which explains why - as we said

in the 2019 year ahead post - we remain confident that the spark for

the next global financial crisis will be in China.

* * * China’s ‘helicopter money’ is blowing up a bubble, authored by Arthur Budaghyan is chief emerging market strategist at BCA Research, and first published in the FT. 中国の「ヘリコプターマネー」がバブルを膨らませている、著者 Arthur Budaghyan BCAリサーチ主任新興市場ストラテジスト、FTでの最初の記事。

The escalation of the trade conflict between the US and China has

raised the likelihood of greater stimulus by Beijing to prop up the

economy. While China’s excessive debt isn’t news, investors must wake up to the reality of “helicopter money” — enormous money creation by Chinese banks “out of thin air”.

While this sugar rush may provide short and medium-term cover for

investors, the long-term effects will exacerbate China’s credit bubble.

China, like any nation, faces constraints on frequent and large

stimulus, and its vast and still rapidly expanding money supply will

produce growing devaluation pressures on the renminbi.

When a bubble emerges we are often told that this bubble is

different. Many economists justify China’s credit and money bubble and

continuing stimulus by pointing to the nation’s high savings rate. But

this narrative is false. At its root is the idea that banks are

channelling or intermediating deposits into loans. This is not how banks

operate.

When a bank expands its balance sheet, it simultaneously creates an

asset (say, a loan) and a liability (a deposit, or money supply). No one

needs to save for this loan and money to be originated. The bank does not transfer someone else’s deposits to the borrower; it creates a new deposit when it lends.

In all economies, neither the amount of deposits nor the money supply

hinge on national or household savings. When households and companies

save, they do not alter the money supply.

Banks also create deposits/money out of thin air when they buy securities from non-banks. As banks in China buy more than 80 per cent of government bonds, fiscal stimulus also leads to substantial money creation. In short, when banks engage in too much credit origination — as they have done in China — they generate a money bubble.

Over the past 10 years, Chinese banks have been on a credit

and money creation binge. They have created Rmb144tn ($21tn) of new

money since 2009, more than twice the amount of money supply created in

the US, the eurozone and Japan combined over the same period. In total, China’s money supply stands at Rmb192tn, equivalent to $28tn. It

equals the size of broad money supply in the US and the eurozone put

together, yet China’s nominal GDP is only two-thirds that of the US.

In a market-based economy constraints are in place, such as the

scrutiny of bank shareholders and regulators, which prevent this sort of

excess. In a socialist system, such constraints do not exist.

Apparently, the Chinese banking system still operates in the latter.

There are clear downsides. Helicopter money discourages innovation

and breeds capital misallocation, which reduces productivity growth.

Slowing productivity and strong money growth ultimately lead to rising

inflation — the dynamics inherent to socialist systems.

Air show in Tianjin, China shows off China's helicopters. Getty Images.

In the long run, more stimulus in China will entail more money

creation and will heighten devaluation pressures on the renminbi. As we

all know, when the supply of something surges, its price typically

drops. In this case, the drop will take the form of currency

devaluation.

As it stands, China’s money bubble is like a sword of Damocles over the nation’s exchange rate.

Chinese households and businesses have become reluctant to hold this

ballooning amount of local currency. Continuous helicopter money will

increase their desire to diversify their renminbi deposits into foreign

currencies and assets. Yet, there is no sufficient supply of

foreign currency to accommodate this conversion. China’s current account

surplus has almost vanished.

As to the central bank’s foreign exchange reserves, at $3tn

they are less than a ninth of the amount of renminbi deposits and cash

in circulation. It is inconceivable that China can open its capital

account in the foreseeable future.

If China chooses the path of unrelenting stimulus, investors should

recognise the long-term negative outlook for the renminbi. Continuous

stimulus will beef up investment returns in local currency terms, but

currency depreciation will substantially erode returns in US dollars or

euros in the long run.

The investment implications go beyond Chinese markets. Market

volatility over the past few months as the talk of stimulus picked up

has given us a peek into the future. As the renminbi has

depreciated by 12 per cent since early 2018, the pain has reverberated

across Asian and other emerging markets. The MSCI Asia and MSCI

EM equities indices have each fallen 24 per cent in dollar terms since

their peak in January 2018. Long-term pressures could play out even more

dramatically.

Fortunately, Chinese authorities recognise these issues. Yet they

face an immense task of stabilising growth while containing credit and

money expansion. This will be hard to achieve in an economy that has

become addicted to credit creation.

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...