Submitted by Joseph Carson, Former Chief Economist, AllianceBernstein,

Decisions to change official rates can no longer be made exclusively on economic growth and price considerations as the dynamics of business cycles have changed. The new business cycle consists of growth and financial leverage (debt), replacing the old cycle of growth and price leverage.

As such, decisions to provide more monetary accommodations to

sustain growth or lift inflation to the preferred target has to be

weighed against growing financial vulnerabilities associated with the

sharp rise in private sector debt. Promises by policymakers to

provide additional monetary accommodation to sustain the growth cycle is

more likely to do more long-term harm than good as it will only

increase the scale of financial vulnerabilities.

In recent decades, monetary policy through its adjustments and control of short-term interest rates has had more influence on financial transactions than economic ones

as individuals and nonfinancial corporations have engaged in active

management of the liability side of their balance sheet, taking on

record amounts of debt at relatively low rates, elevating real and

financial asset prices in the process, while providing only modest

benefits to overall economy.

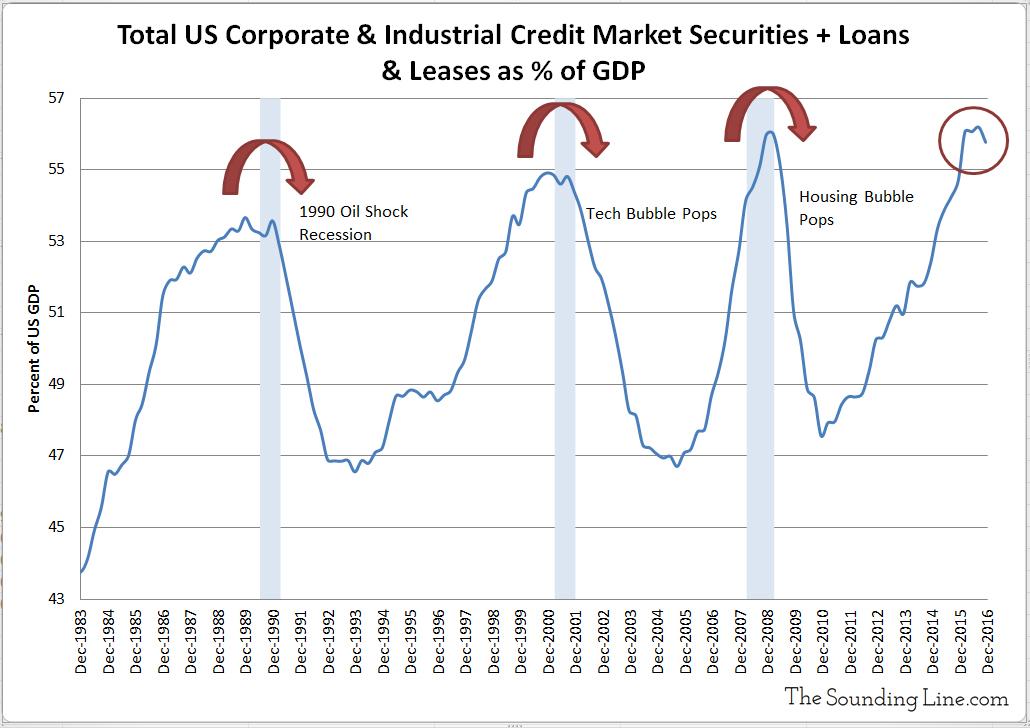

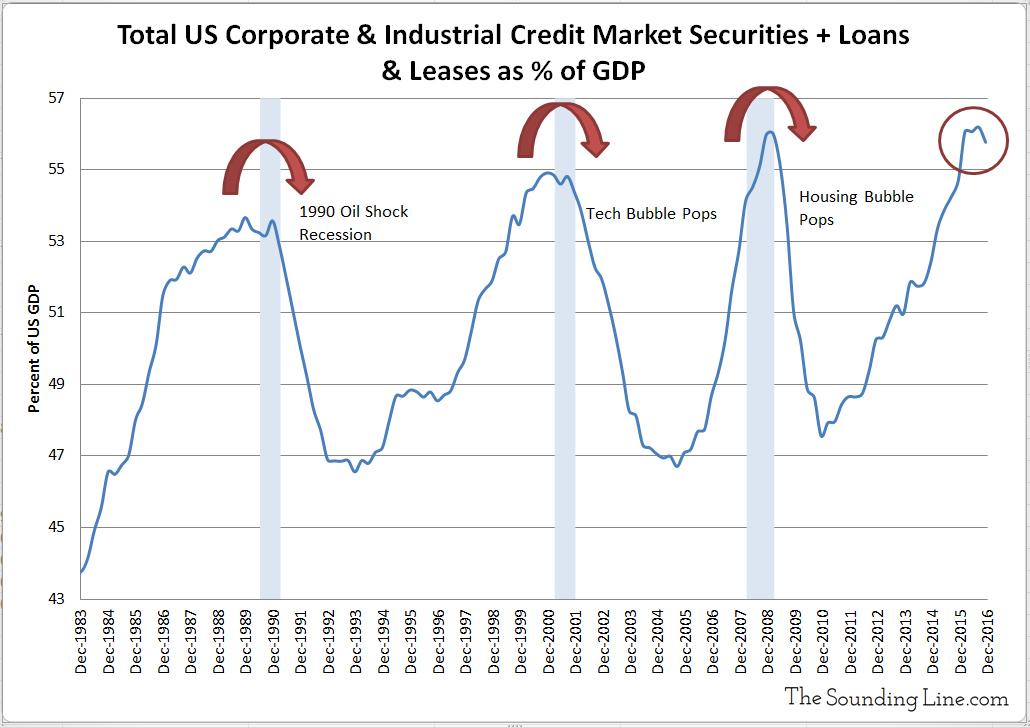

For example, since 2011 nonfinancial corporations have added to $5.2

trillion in debt to their balance sheets. Corporations used this debt

for a variety of purposes, such as acquiring other companies, purchasing

real estate, buying back their own stock, while also investing in plant

and equipment to run their regular business operations. Yet, the

incremental growth in nonresidential investment has been a little more

than $1 trillion. In other words, for every $5 borrowed by nonfinancial

corporations only $1 has found itself redeployed in the real economy.

In the 2000s cycle, households also went on a borrowing binge, adding

over $7 trillion in new debt over the span of seven years. Most of the

new debt was invested in real estate. Over the course of the 2000's

growth cycle households added $2 of debt for every $1 increase in

consumer spending and investment in housing. Much higher ratios of debt

to new investment occurred during the dot.com boom of the late 1990s and the the commercial real estate boom of the late 1980s.

All of these episodes highlight the new linkages and tradeoffs between monetary policy and financial activities. Yet,

the failure to adapt, and even recognize, the changing linkages caused

policymakers to miss, or downplay, the buildup of financial

vulnerabilities in the system and the adverse shocks to the economy and

the financial system were repeated time and again.

Each period of excessive credit and financial leverage was

followed by a long bout of debt-deleveraging forcing the Fed to engage

in a "financial engineering" campaign to cushion the economy and bring

stability to the financial system. Following the commercial

real estate crash of the early 1990s the Federal Reserve lowered

official rates 650 basis points; 550 basis points following the dot-com

bubble; and 500 basis points (and probably an extra 200 basis points of

easing occurred with the Fed’s asset purchase program) after the housing

bubble.

Today, even though the current environment has similar

characteristics---large increases in debt and elevated asset

prices--that preceded each of the past three recessions policymakers do

not seem to be concerned about the growing buildup of financial

vulnerabilities. Yet, the financial markets with Treasury yields

out to 10 years trading well below the target on the federal funds rate

suggests that the limits of the Fed's "financial engineering" have been

reached and additional monetary accommodation will have a negative

trade-off between costs and benefits. 今日では、現在の環境はそれらとよく似たものだがーー債務が大きく増え資産価格が大きく上昇しているーー過去三回の景気後退前に政策立案者は積み上がる金融システム脆弱性を懸念していなかったように見える。ただ、金融市場を見ると、10年債金利はすでにFFRよりも低くなっており、FEDの「金融工学」も限界に達し、さらなる金融緩和策はコスト・ベネフィットを考えるとマイナストレードオフとなるだろう。

In fact, it would not be a surprise if market yields stay near

current levels even if the Fed decides to lower official rates since

encouraging more debt growth would only tip the scale more so to a bad outcome down the road.

Amazonで買物をしてContrarianJを応援しよう Albert Edwards: This Was The Final Recessionary Shoe, And It Has Now Fallen by Tyler Durden Thu, 06/27/2019 - 12:45 Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007... ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・ ... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions. ・・・市場は準混乱状態になった、というのも歴史的に見てイールドカーブ反転が過去7回の景気後退の前兆となっているからだ。 However, while the inversion was certainly a memorable event, the question on everyone's lips is how do risk assets perform once the curve flattens and/or inverts. According to backtests from Goldman, since the mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. ...

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...