Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007...

ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・

... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions.

However, while the inversion was certainly a memorable event, the

question on everyone's lips is how do risk assets perform once the curve

flattens and/or inverts. According to backtests from Goldman, since the

mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. しかしながら、イールドカーブ反転は確かに象徴的なできごとだが、誰もが知りたいのはイールドカーブ平坦化・反転化後の株式のパフォーマンスだ。ゴールドマンのバックテストによると、1980年代なかば以来でみて、株価急落が起きるのはイールドカーブ反転後再度急峻になるときだ。

In other words, as we noted then, "Curve Inversion Is Bad, But It's The Steepening After That Kills."

Fast forward to today, when in his latest bearish missive, SocGen's

permabear Albert Edwards picks up where we left off, and in a note

titled "the final recession shoe has now fallen", he notes that while

inversion of the US yield curve is seen as a reliable precursor to US

recessions, "it has a long and variable lead time", and instead "a far more immediate and present danger of recession occurs when after inversion, a rapid steepening occurs." 現在までの状況を早送りしてみると、彼の最新の弱気記事だが、SocGenのパーマベア Albert Edwardsがこの話題を取り上げた、ただしZeroHedgeは紹介しなかった、タイトルは「景気後退劇場の最後の見せ場到来」、彼が言うには、米国イールドカーブ反転は信頼できる景気後退予兆だが、「十分なリードタイムがある」、そしてむしろ「インバージョン後に急速に急峻化が起きると、それは直ちに景気後退の危機が迫っている」。

Sound familiar?

知ってました?

In any case, as we first commented in early 2019, Edwards notes that this subsequent steepening "usually informs investors the cycle is over and it is time to flee for the hills."

Well, for those who haven't figured out the punchline yet, rapid curve steepening is now occurring, and as Edwards gleefully concludes, this "suggests recession may indeed either be imminent or else it has already arrived." そう、まだ結末を認識できない人に教えてあげよう、急速なイールドカーブ急峻化がいま起きつつ在る、そしてEdwardsが明快に結論付けるが、この状況は「景気後退がすぐそこに差し迫っている、もしくすでに景気後退入りしている」のだ。

Should Edwards be right, the implications are clearly huge, and not

just for the economy and markets - perhaps the most dramatic consequence

will be what happens with the world's most powerful institution: the

Federal Reserve.

Edwardsの言っていることは正しいのだろうか?、その影響力はあまりに大きい、そして単に経済や市場だけでなくーーたぶんもっとも劇的な結末とは世界最強の組織に起きることだ:the Federal Reserve 。

"As a long time harsh critic of the Fed (and other central banks) for

their obscenely easy money policies" Edwards writes that he is loath to

criticize President Trump’s nearly constant slams of Fed Chair Powell,

especially since President Trump has a very clear agenda: namely, he

is going to make sure the Fed gets the blame from the electorate if the

economy goes into recession and the equity market plunges ahead of the

next presidential election. 「長年FEDや世界の中央銀行には手厳しい批判がなされてきた、緩和政策に浸りすぎてきたことだ」。Edwardsはトランプ大統領を批判したくない、大統領はいつもFED議長Powellを罵る、特にトランプ大統領の意図は明確だ:すなわち、FEDが大統領選挙に責任を負っている、もし景気後退入りとな来年の大統領選挙に向けて株価が下がるとそれはFEDの責任だと。

"And by hook or by crook, Powell will be out on his ear", Edwards says.

「そしてどういう手段を撮ろうとも、Powellは聞く耳を持たないだろう」とEdwardsは言う。

Which is good news and bad news, because while Powell clearly threw

in the towel on the hawkish monster that he was perceived as less than a

year ago when he spooked markets that the Fed would keep hiking until

the mid-3's, and is now as dovish and meek as Yellen or even Bernanke,

it's not like his departure would also end the Fed.

Quite the opposite, because considering that this is what President

Trump is like now, imagine what he will be if the US leads the global

economy into another deep recession and financial crisis like 2008:

Even before the irascible Trump became President, I said the Fed

would lose its (supposed) independence if they were the midwife to

another crisis. There will be no deft, disingenuous shifting of blame to

the commercial banks this time around. The Fed will carry the can.

As a result, Trump will promptly appoint a Fed chair who is the most

dovish one can find, and here Kashkari comes to mind: after all, the

former Goldman IT banker and "architect" of the 2008 bank bailout plan

(or rather Paulson's smokescreen) not accidentally said he was hoping

for a 50bps rate cut earlier this week - he is clearly angling for

Powell's job.

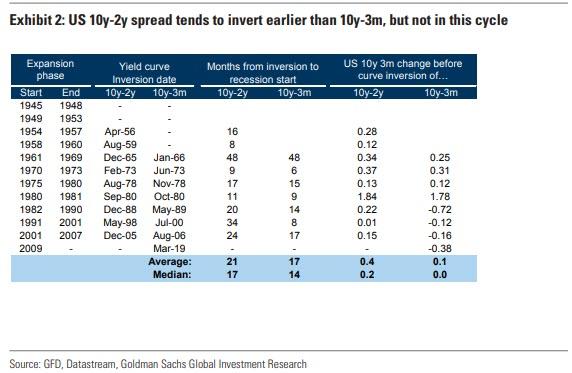

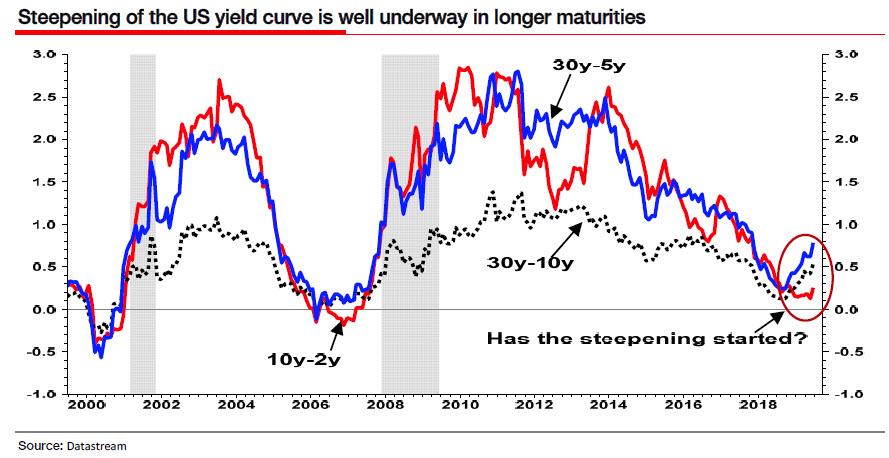

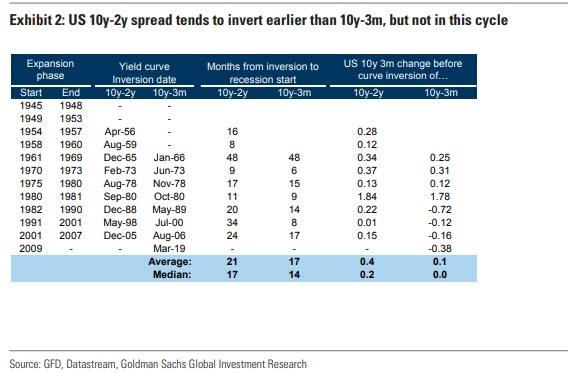

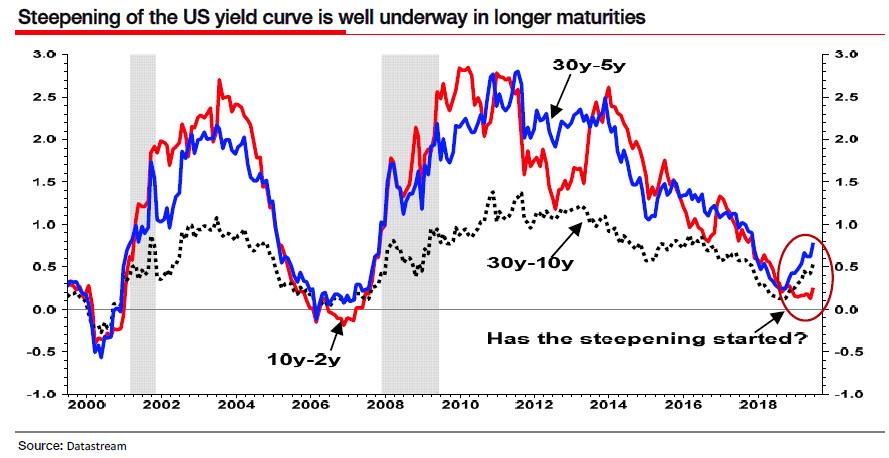

Meanwhile, and going back to the recession narrative, it's not just

the re-steepening of the 3M-10Y. As Edwards ominously concludes, there

is another key indicator that everyone is focused on: "we (and others),

have also pointed out that the alarm bells for an imminent recession

would really start ringing if the 10y-2y curve began to steepen." To be

sure, it is reassuring that this has not happenied - yet - but, as

Edwards concludes "the rest of the yield curve (which leads to 10y-2y

steepening) is now shouting recession from the rooftops."

So how long until Neel "the Chump"

Kashkari is Fed chair? The good news is that it will probably not

happen tomorrow, so readers at least have enough time to buy some more

gold and cryptos before the new Fed chair unleashes the biggest - and

last - liquidity tsunami in US history, one which culminates with the

dollar losing it reserve currency status. Whether that leaves Zuckerberg as the world's central bank, or the IMF finally digitizes the SDR in Libra's footsteps, remains to be seen.

というわけで Neel "the Chump" Kashkari がFED議長になるまでどれくらいの時間が残されているだろうか?幸いなことにそれが明日起きるわけではない、というわけで読者諸君にはまだゴールドや暗号通貨を買います十分な時間が残されている、新任FED議長が米国史上最大で最後の流動性津波を引き起こす前にだ、こうなるとついにドルは準備通貨の地位を失う。こうなるとZuckerbergが世界の中央銀行となるか、もしくはIMFがとうとうLibraの足元でSDRをデジタル化するかもしれない、これを見ることになるかもしれない。

中国が債務増加していることはたしかです。ただ日本の例を日銀資金循環報告でみると家計、320兆円、民間非金融機関1,785兆円、一般政府 1,284兆円となります。合算すると3,300兆円にもなり、GDPの600%を超えています。 https://www.boj.or.jp/statistics/sj/sjexp.pdf この記事の統計と同じ考え方で数値を採用しているのかどうか気になります。 加えて、この資金循環報告に書かれている海外資産というのが内数なのか外数なのか?私にはよくわかりません。当然海外債務も結構な額になります。一度日銀資金循環 図表1を見てください。詳しい方に教えていただければ。 この中国のたどる道は昔のソ連とかMMTと同様で、自国通貨ならいくら発行しても倒産はしない、というか為政者が痛みに耐えることができず緩和を続けるというものです。でも最終的には限界点に達します。ソ連は建国から崩壊まで70年かかりました。 自由主義経済なら立ち行かなくなった企業は退場してもらうというのが減速なのですが、これがうまくゆかないわけです。 でも日本は中国のはるか先を言っているように見えます。ちょっと検索したのですが、日本の債務に関しては政府債務に言及したものばかりで、この記事のように民間、個人まで総合的に記載しているのは日銀の資金循環統計しか見つけることができませんでした。 China Continues To Pile Debt On Top Of More Debt Written by Jesse Colombo | Feb, 27, 2019 Like many countries, China attempted to rein in its debt growth over the past couple years, but ultimately gave up and is now back to piling on even more debt. Bloomberg reports – 多くの国と同様に、中国もここ2年ほど債務増加を抑えようとしてきた、しかし結局の所諦めてしまい、今や更に債務を積み上げている。ブルームバーグ記事ーー For almost two years,...

Class 8 Heavy Truck Orders Crash 68% in January by Tyler Durden Wed, 02/06/2019 - 17:25 Among the latest dismal news about the strength of the US economy, on Tuesday ACT Research released preliminary truck orders for January 2019 which showed that Class 8 truck orders collapsed an astounding 68% for January. The decline is being attributed to a 300,000+ vehicle backlog potentially prompting fleets to halt purchases in the near term. 米国経済に関し最近憂鬱なニュースが多い中で、火曜にACT researchが2019年1月のトラック発注を開示した、1月にClass 8のトラック発注がなんと68%も急落した。この発注減は短期的に300,000台超の潜在在庫を生み出す。 Specifically, in January Class 8 net orders were 15,800 units (14,700 SA; 176,400 SAAR), down 68% YoY and down 26% MoM. Class 5- 7 January net orders were 23,400...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...