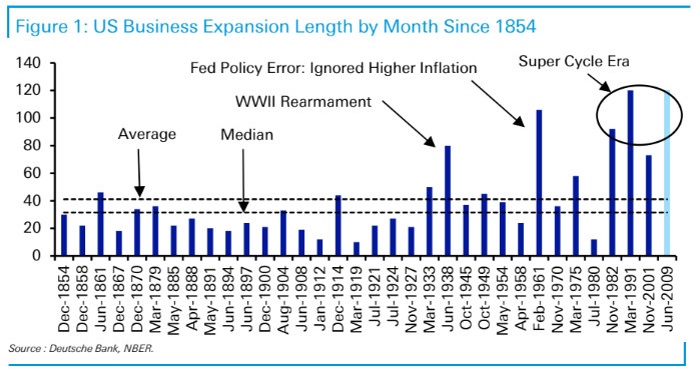

Deutsche Bank

strategists Jim Reid and Craig Nicol wrote a report this week that

echos what I and other Austrian School economists been saying for many

years: actions taken by governments and central banks to extend

business cycles and prevent recessions lead to even more severe

recessions in the end.MarketWatch reports –

ドイツ銀行のストラテジスト Jim Reid とCraig Nicolが今週報告書を書いた、その内容は私や他のオーストリア学派経済学者が長年警鐘を告げていたものと同様だ:政府や中央銀行がビジネスサイクルを引き延ばし景気後退を回避しようとするが、これが結局もっと深刻な景気後退を引き起こす。

MarketWatchの報告ーー

The 10-year old economic

expansion will set a record next month by becoming the longest ever.

Great news, right? Maybe not, say strategists at Deutsche Bank.

Prolonged

expansions have become the norm since the early 1970s, when the tight

link between the dollar and gold was broken. The last four expansions

are among the six longest in U.S. history .

Why so? Freed from the

constraints of gold-backed currency, governments and central banks have

grown far more aggressive in combating downturns. They’ve boosted

spending, slashed interest rates or taken other unorthodox steps to

stimulate the economy.

“This

policy flexibility and longer business cycle era has led to higher

structural budget deficits, higher private sector and government debt,

lower and lower interest rates, negative real yields, inflated financial

asset valuations, much lower defaults (ultra cheap funding), less

creative destruction, and a financial system that is prone to crises,’ they wrote in a lengthy report.

“In

fact we’ve created an environment where recessions are a global

systemic risk. As such, the authorities have become even more encouraged

to prevent them, which could lead to skewed preferences in

policymaking,” they said.“So we think cycles continue

to be extended at a cost of increasing debt, more money printing, and

increasing financial market instability.”

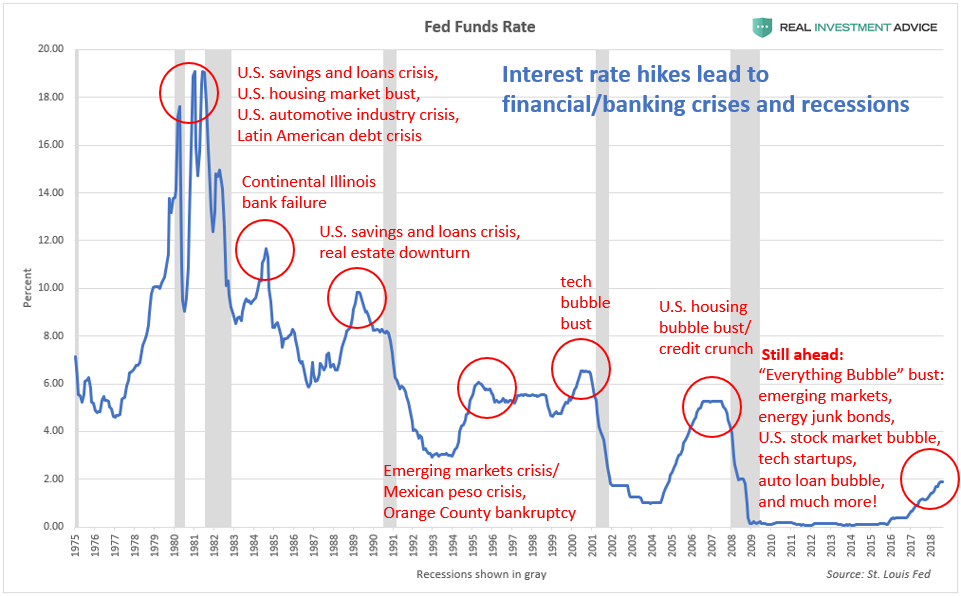

As I have explained

in the past, when central banks like the U.S. Federal Reserve cut

interest rates to low levels, they manage to create economic booms by

encouraging borrowing and higher asset prices. These economic booms are

often based on dangerous economic bubbles that burst and lead to

recessions when interest rates are normalized again. As the chart below

shows, financial crises and recessions (see the gray vertical bars)

occur after rate hike cycles, including the dot-com and U.S. housing

market crashes.

The false economic booms that occur when central banks interfere with

the business cycle trick investors and entrepreneurs into thinking that

they are organic and sustainable booms. When the booms inevitably turn

to busts, the bad investments that result are known as malinvestments – 中央銀行が景気サイクルに介入することで生み出される偽の景気ブームは投資家や起業家に誤解を引き起こす、この経済ブームは自然なもので持続的なものだと。ブームというものには必ず終焉がある、このとき、筋悪投資がはじめてmalinvestmentsとして認識されるーー

Malinvestment is a

mistaken investment in wrong lines of production, which inevitably lead

to wasted capital and economic losses, subsequently requiring the

reallocation of resources to more productive uses. “Wrong” in

this sense means incorrect or mistaken from the point of view of the

real long-term needs and demands of the economy, if those needs and

demands were expressed with the correct price signals in the free

market.

Malinvestmentとは wrong lines of production 方針を間違えた生産への誤解による投資だ、これは必ず資本の浪費となり経済的損失を伴う、その後もっと生産的な目的へと資本の再配分が必要となる。ここで言うところの「Wrong」とは長期的視点での実需を見誤ったという意味だ、自由市場ならばこのような需要には正しい(投資、債務)費用が示される。

Random, isolated entrepreneurial miscalculations and

mistaken investments occur in any market (resulting in standard

bankruptcies and business failures) but systematic, simultaneous

and widespread investment mistakes can only occur through

systematically distorted price signals, and these result in depressions

or recessions. Austrians believe systemic malinvestments occur

because of unnecessary and counterproductive intervention in the free

market, distorting price signals and misleading investors and

entrepreneurs.

For Austrians, prices are an essential information

channel through which market participants communicate their demands and

cause resources to be allocated to satisfy those demands appropriately.

If the government or banks distort, confuse or mislead

investors and market participants by not permitting the price mechanism

to work appropriately, unsustainable malinvestment will be the

inevitable result.

Because the current economic cycle has lasted for an unusually long

time due to the actions of central banks, an unprecedented amount of

malinvestment has built up globally that needs to be cleansed in the

coming recession. It’s similar to a night of drinking: the more you

drink and the later you stay out, the worse your hangover is going to

be. Globally speaking, the last decade has been the bender to

end all benders and the coming hangover is going to proportionally

severe.

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....