Authored by Alasdair Macleod via GoldMoney.com,

We are all used to the bullion banks covering their shorts on Comex

by waiting until the speculators are over-bullish and vulnerable to

mark-downs that trigger their stops. Algorithmic traders go from long to

short in a heartbeat as well, and they dump contracts into a falling

market, speeding up the decline. We should say at this juncture that the

Managed Money speculators are short-term, attracted by futures

leverage, and their gold position is often part of a wider risk strategy

deployed by hedge funds. They do not intend to stand for delivery. The

wider investment world taking strategic portfolio decisions does not

often get involved with gold, so the Comex gold contract has been a

secular play.

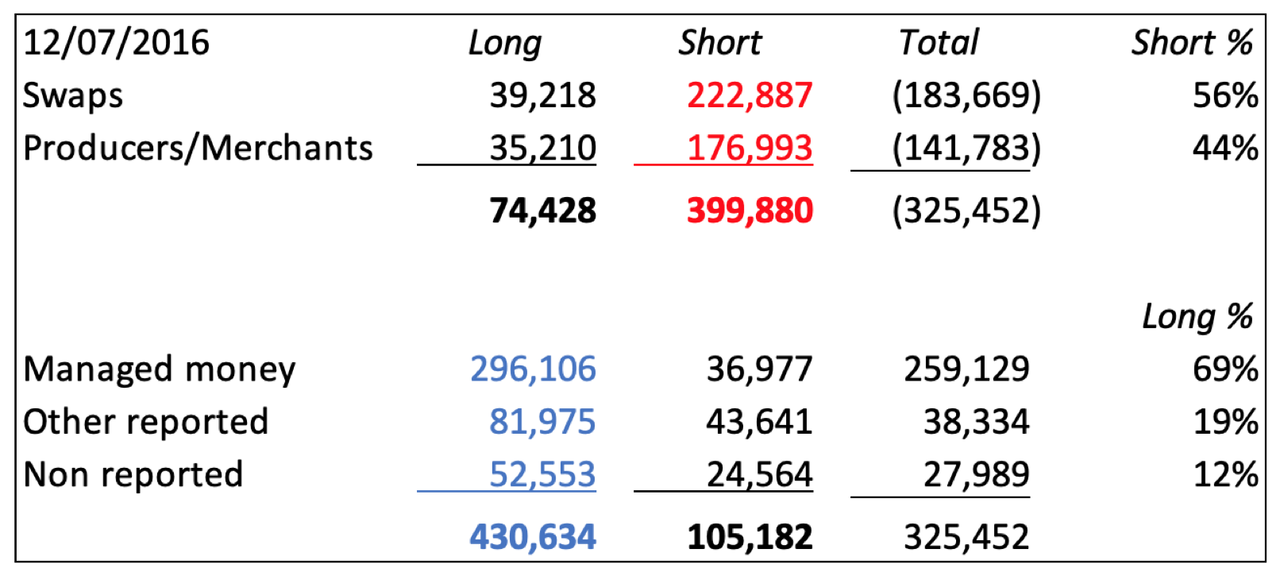

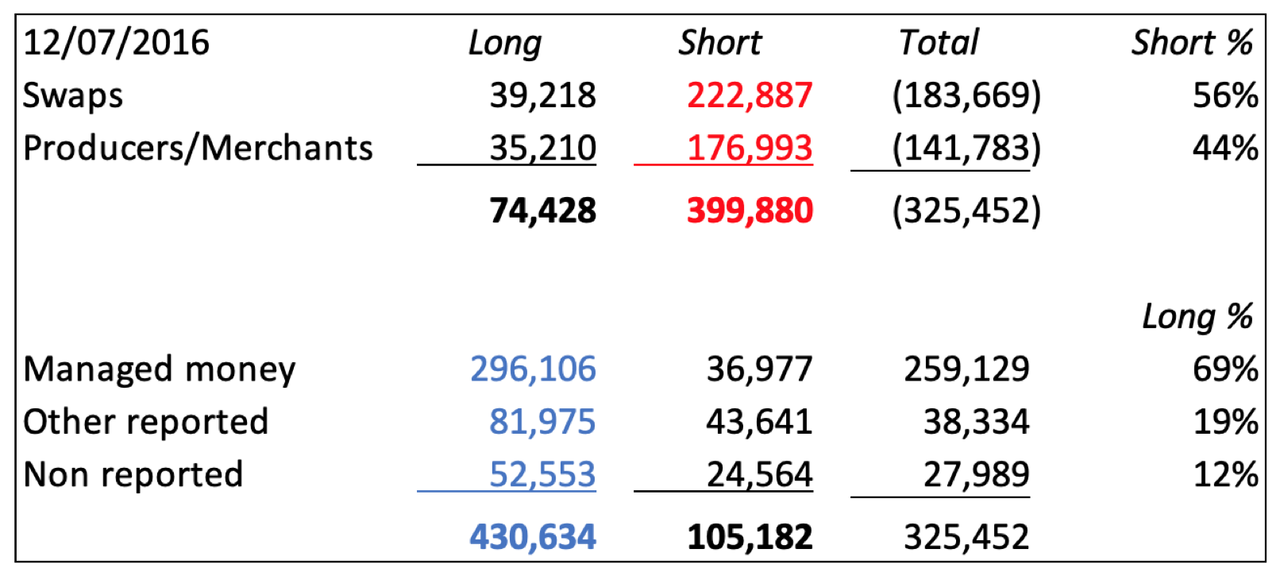

The table below shows a typical set-up, in this case July 2016. The

Managed Money category (296,106 — net 259,129 contracts) is close to

record long. Open interest was 633,000 contracts and the gold price was

at $1360, having run up from $1040 the previous December.

In the non-speculative category, the bullion banks (Swaps) had 56% of

the shorts and the Producer/Merchants 44%. Mark-to-market value of the

Swaps net short position was $25bn. Of the speculative longs, the

managed money category (hedge funds) held 69%, and at 296,106 long

contracts it was almost a record. There was a high level of bullishness;

easy pickings for the bullion banks, who by the following December

drove the price down to $1120, reducing their net shorts to under 50,000

contracts.

It was a game that evolved out of Comex futures being used simply to

offset long bullion positions at the LBMA. Over time, bullion bank

traders increased their trading position limits, as opposed to their

pure hedging activity, making easy money jobbing the other side of

Managed Money trades.

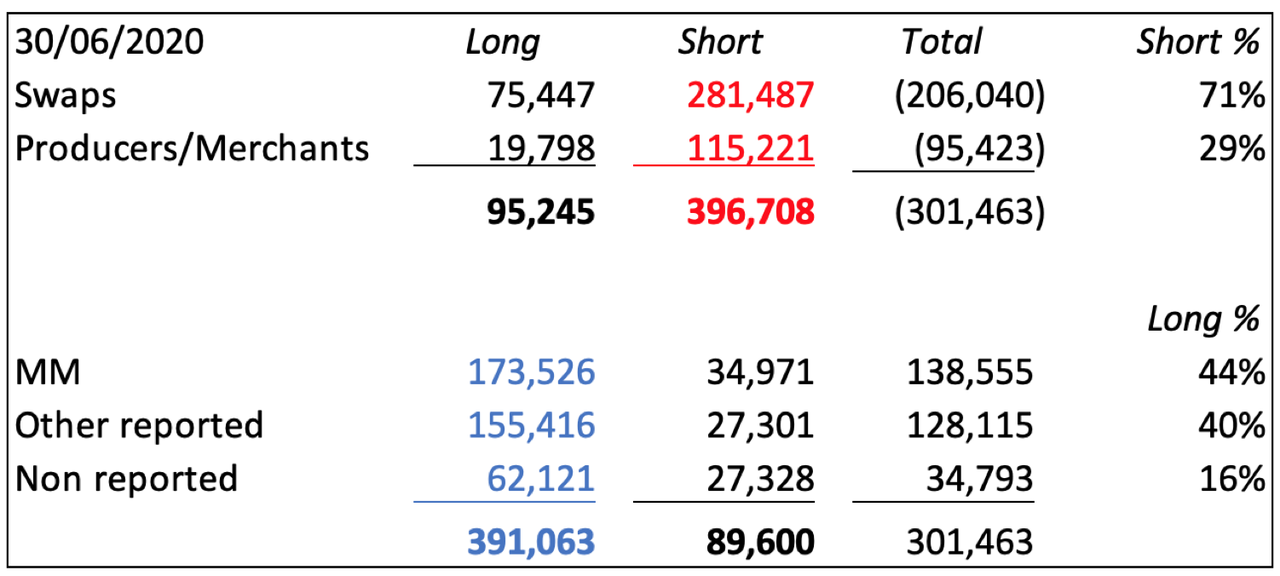

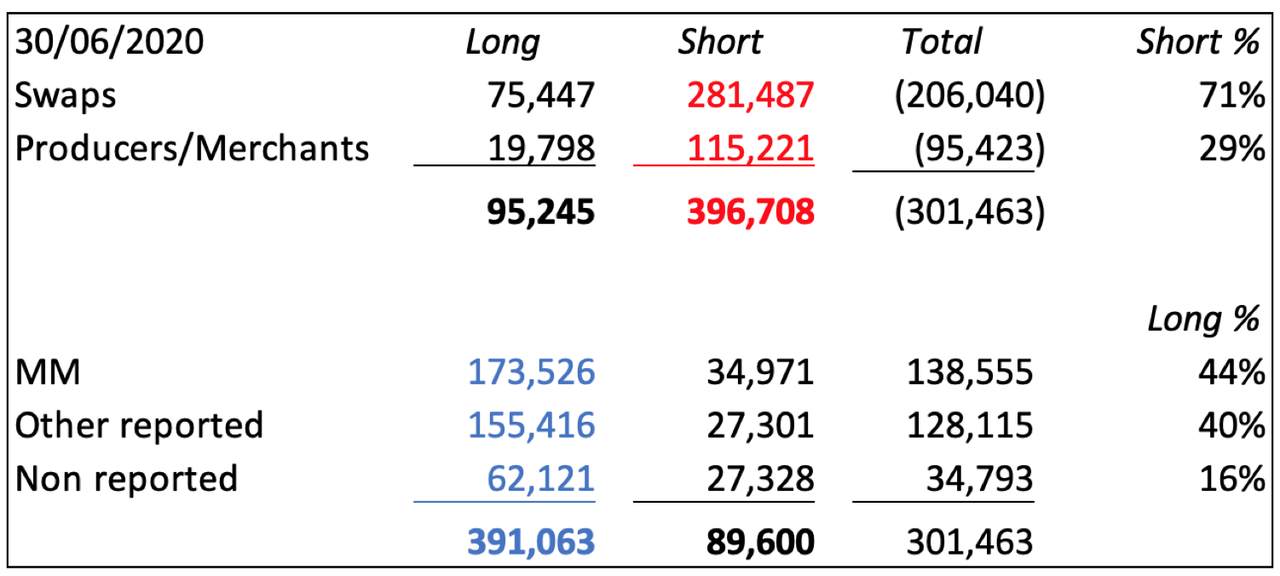

Now look at the current situation, with the gold price at decade highs ($1775) and open interest at 561,628 (30 June).

では、現在の状況を見てみよう、ゴールド価格は十年ぶりの高値($1775)になり、open interestは6月30日時点で561,628枚だ。

In the non-speculator category, the Swaps are more short than they

were in July 2016 despite open interest being 71,372 contracts lower.

The mark-to-market value is record net short at $36.6 billion. What has

happened is the Producer/Merchants have cut their positions, presumably

deciding that hedging mine output is less important in the current

inflationary environment. Consequently, the bullion banks are bearing

71% of the short exposure.

The speculator category makes this more interesting still. At 138,555

net long, hedge funds are only 25,000 contracts longer than average,

and compared with their bullishness in July 2016 have hardly got going.

It is the other categories, Other Reported and Non-reported have taken

56% of the long side, and they are not behaving like skittish hedge

funds at all. These include family offices, the ultra-wealthy and

foreigners through Globex who are standing for delivery as a means of

getting their hands on physical bullion —171 tonnes from the June

contract alone.

Bullion banks are between a rock and a hard place. For years they’ve

been playing the hedge funds as an angler hooks and plays a fish. That

game has ceased and there is no easy way for them to get level. For the

moment they are trying to put a lid on the price, but the cost has been

rising open interest, and therefore rising mark-to-market positions.

The August active contract runs off the board at the end of this

month and bullion banks are likely to be forced into large delivery

volumes again. Furthermore, the exchange for delivery arbitrage facility

between Comex and the LBMA is broken, allowing Comex premiums to London

spot to go unchallenged.

It is increasingly possible the gold contract is evolving into deep crisis, and that force majeure might have to be declared if, as seems increasingly inevitable, a wider banking crisis ensues.

Amazonで買物をしてContrarianJを応援しよう Silver Outperforming Gold 2 Adam Hamilton July 26, 2019 3232 Words Silver has blasted higher in the last couple weeks, far outperforming gold. This is certainly noteworthy, as silver has stunk up the precious-metals joint for years. This deeply-out-of-favor metal may be embarking on a sea-change sentiment shift, finally returning to amplifying gold’s upside. Silver is not only radically undervalued relative to gold, but investors are aggressively buying. Silver’s upside potential is massive. ここ2週シルバーは急騰した、ゴールドを遥かに凌ぐものだ。これは注目すべきことだ、もう何年もシルバーはひどいものだった。この極端に嫌われた金属が大きく心理を買えている、とうとうゴールド上昇を増幅するに至った。シルバーは対ゴールドで極端に過小評価されているだけでなく、投資家は積極的に買い進んでいる。シルバーの潜在上昇力は巨大なものだ。 Silver’s performance in recent years has been brutally bad, repelling all but the most fanatical contrarians. Historically silver prices have been mostly ...

Amazonで買物をしてContrarianJを応援しよう Junk Bond Bubble In Pictures: Deflation Up Next by Tyler Durden Fri, 07/19/2019 - 14:37 Authored by Mike Shedlock via MishTalk, The widely discussed "everything bubble" is, in reality, a corporate junk bond bubble on steroids sponsored by the Fed ... 幅広く議論されている「everything bubble」は実際に企業ジャンク・ボンドバブルにも言えることであり、これはFEDによりドーピング注入されている・・・ The highest grade AAA corporate bonds yield 2.75%. BBB-rated corporate bonds, just one step above junk, 3.5%. BB-rated bonds yield just 4.28%. 最高級ランクAAA企業債権の金利は2.75%だ。あとひとランク悪化でジャンク・ボンド入りするBBB債権金利は3.5%。BB格付け債権の金利でもわずか4.28%でしかない。 Corporate Bond Spreads 企業債権金利のスプレッド The spread between Prime AAA bonds and lower-medium grade bonds (see chart below) is just 0.77 percentage points. 最上位AAA債権と低中ランク債権のスプレッドがわずか0.77%しかない。 The spre...

結局、中国は隣国日本で20年前に起きたことを学んでいなかったということでしょう、というかどの国もどの政府も十分成熟するまでは「わかっちゃいるけどやめられない」ということでしょうね、きっと。 Spooked By Apple? Wait ‘Til China’s Bubble Bursts Written by Jesse Colombo | Jan, 3, 2019 Apple stock plunged nearly 10% on Thursday after the company cut its revenue forecast due to slowing iPhone sales in China. Apple’s woes dragged U.S. stock indices lower by more than 2% as fears of a more extensive China-driven slowdown spread. アップルの株価は火曜に約10%下落した、同社が中国でのiPhone売上原則を予想したためだ。アップルの弱さが米国株式指数を2%以上押し下げた、中国主導でさらなる原則が広がるのではという懸念からだ。 From the New York Times : ニューヨークタイムスによると: For years, no matter what was happening elsewhere, global companies bet billions upon billions of dollars that China’s consumers would keep spending money. 長年、他国で何が起きようとも多国籍企業は中国消費は巨額を維持することに賭けてきた。 Now, just when the world economy could use their financial firepower, they are no longer so quick to open their wallets. 今や、世界経済が金融弾薬を用いてももはや彼らの財布を緩めることはできない。 The latest sign of a slowdown in...

Gold Stocks Surge Higher Adam Hamilton February 22, 2019 2932 Words The gold miners’ stocks surged strongly this week, blasting to new upleg highs. The mounting gains are naturally driving more interest in this small contrarian sector, shifting sentiment towards bullish. Despite their accelerating rally, gold stocks still remain fairly low technically and deeply undervalued relative to gold. So their strengthening upleg likely has plenty of room to run considerably higher in coming months. 今週金鉱株は力強く上昇し新高値となった。上昇が積み上がりこの小さなコントラリアンセクターはさらに注目を集めている、これが心理を強気なものにする。ラリーが加速するが、金鉱株はテクニカル的にはまだ安値で、対ゴールドでとても過小評価されている。というわけで力強い上昇は今後数ヶ月まだかなりな上昇余地がある。 The gold miners’ stocks are ultimately leveraged plays on gold, which overwhelmingly drives their profits. The much-maligned yellow metal has enjoyed a strong upleg since mid-August, when record gold-futures s...

最後の2段落だけ訳をいれておきました。 Fed’s Risky QE4 Stock Ramp Adam Hamilton January 31, 2020 3567 Words The US stock markets dramatically surged mostly in a straight line since mid-October. This extraordinary rally started when the Federal Reserve announced it would resume expanding its balance sheet for the first time in years. The deluge of new liquidity from that quantitative-easing bond buying has again acted like rocket fuel for stock markets. After shooting vertically they are in real trouble when the Fed pulls back. In early October the flagship US S&P 500 stock index (SPX) slumped to 2888. That was a mild 4.6% pullback from late July’s latest record high. The SPX was still having a great year though, up 15.2% year-to-date at that point thanks to extreme Fed easing . After the SPX had plunged 19.8% mostly in Q4’18 in a severe near-bear cor...