A recent article by James Deporre at thestreet.com asked Will Powell’s Remarks Push the Algos to Make a Move? 最近のthestreet.comでのJames Deporreの記事ではこう問いかける、Powellの発言がアルゴリズム取引で市場を動かすか?

Deporre’s article is a recap of a day’s market events beginning with

Jerome Powell’s recent testimony to Congress. He suggests that what

matters are not Powell’s words, but whether computerized trading

programs, known as “algos,” would buy stocks as a result of Powell’s

testimony. Summarizing what ended up being an uneventful day of trading

activity, Deporre made the following absurd comment which caught our

attention:

“On the other hand, the mighty Apple (AAPL) is holding up and seems to function as a de facto money market account these days. It is a great place for some to park cash and that helps to keep the indices hovering near highs.”

While we currently hold Apple stock on behalf of some of our

clients, we do so with the full awareness that valuations for Apple and

many other stocks are extreme. A reversion back to or below

average historical valuations will result in a massive loss of wealth

for many investors. As such, we maintain a careful and balanced

investment posture and take nothing for granted. Most importantly, we

never confuse “parking” cash with owning a stock. Like a shovel and

hammer, stocks and cash are valuable tools, but neither is a perfect

substitute for the other.

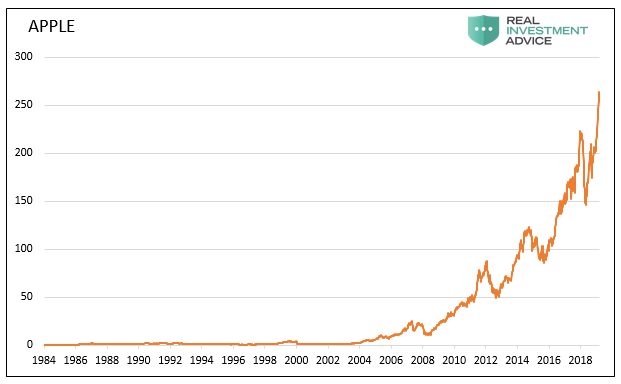

Apple is one of the world’s largest corporations, with innovative

products and a great growth trajectory. As reported in its third-quarter

2019 earnings release, the company has a war chest of $245 billion in

cash. These facts are not lost on investors. As shown below, Apple

shares have risen at a remarkable pace. Since its IPO in 1984, the stock

is up almost 70,000% or more than 20% annually. A $1500 investment in

1984 is now worth over a million dollars!

Data Courtesy Bloomberg

Money market mutual funds, also known as cash accounts, are vehicles

that allow investors to hold cash and earn the short term rate of

interest in the market. These funds invest in very short term, liquid,

and highly rated securities. The investments produce little to no price

volatility. Many money market mutual funds are governed by the SEC’s 2A7

rules, which greatly limit the credit and liquidity risk of these funds

and attempt to ensure investors in them do not have a risk of loss of

principal. Given the near riskless nature of money market mutual funds,

they offer meager returns.

As the Byrds sang, “there is a season- turn – turn- turn. Similarly,

there is a time to invest heavily in stocks and a time to scale back on

stock holdings and take less risk. It is all too popular for market

gurus, especially at market peaks when complacency is the highest, to

preach about buy and hold strategies. This advice is based on a

misconception that market drawdowns will be short-lived and investors

will quickly recoup any losses. Therefore, it is not surprising

that the popular investing view today insists that investors should

check their brains at the door and remain fully invested in stocks at

all times. Byrdsの歌にもあるように、「there is a season- turn - turn - turn、方針を変えるときがある、変えろ、変えろ、変えろ」。同様に、株式比重を大きくするときと株式露出を減らしリスクを抑えるときがある。市場になれた人にとってはあまりに一般的なことだ、特に安心感が高まり市場が頂点に達したときだ、buy &hold戦略が勧められなくなる。このアドバイスはこういう誤解に対するものだ、市場の下落は短期的なものであり投資家はどういう損失でもすぐに取り戻すことができる。しかるに驚くことではないが、現在の一般的な投資家はいつでも株式露出全開であり頭を冷やすべきだ。

As shown below, such logic flies in the face of history.

下のチャートを見れば、歴史的にそういう論理が的を得ていることが解る。

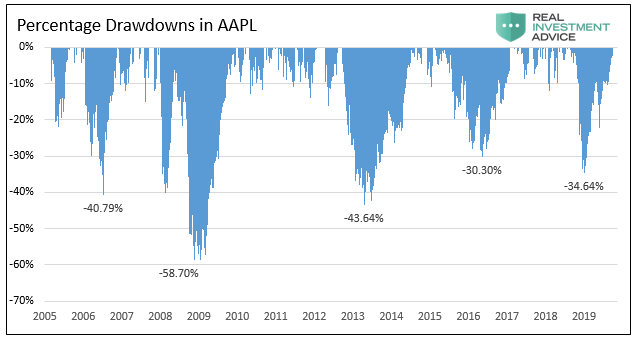

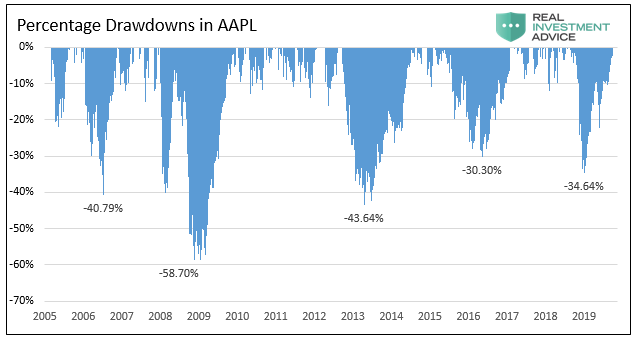

Over the long run, investors in Apple have fared better than the

market. As shown, drawdowns over the last decade have been relatively

short-lived. However, those setbacks have not been small. Since 2010,

Apple’s stock price has dropped by 35-45% on three different occasions

and by 20% on one other. So, can we treat Apple like a money market fund

and hold it with the certainty of knowing that it will never lose

value?

It is important to understand that, in the long run, stock prices are

regulated by the cash flows of the underlying corporation. We explained

this recently as follows:

“A Honus Wagner baseball card from 1909 was recently auctioned

for over $3 million. While that may seem like a lot of money, it is not

necessarily expensive. A baseball card is nothing more than paper and

ink with no real value. Its street value, or price, is based on the

whims of collectors. “Whim” is impossible to value.

Stocks are not baseball cards. Stocks represent ownership in a corporation, and therefore, their share prices are based on a series of future expected earnings

and cash flows. Further, there are many other types of investments that

serve not only as alternatives, but provide a means to assess relative

value.

Today, investors are trading stocks on a “whim,” with scant attention to their value. Unlike

a baseball card, when a stock’s market value rises much more than its

real value, an inevitable correction will occur. The only question is

not if, but when.”

There is an important distinction to be made here between “investing” vs. “speculating.”

そこには重要な違いがある、「投資」と「投機」だ。

Apple’s shares are priced at a historically steep premium to its

fundamentals, meaning “whim” is playing a role in recent price

appreciation. Whim is speculating. Here are a few fundamental data

points to consider, but as you do, keep in mind Apple has bought back a

third of their shares outstanding since 2012, making per share data when

adjusted for buybacks higher than that shown below.

Price to book value is the highest it has ever been since the IPO (12.90x)

PBRはIPO以来最高値だ、12.90x。

Price to earnings (trailing twelve months), price to sales, and price to free cash flow are at the highest levels since 2009

TTM PER、一株あたり売上、そして一株あたりフリーキャッシュは2009年以来最高だ

Regardless of whether Apple’s valuation may appear rich,

there is little doubt the valuation premium can still rise further in

the future. Earnings can grow faster than expected and justify

the current valuations. However, the premium can also revert back to

historical levels and earnings may disappoint in the future. Apple’s

stock price dropped 61% in 2008, and that was following the release of

the first iPhone. It is difficult to imagine a better time to have owned

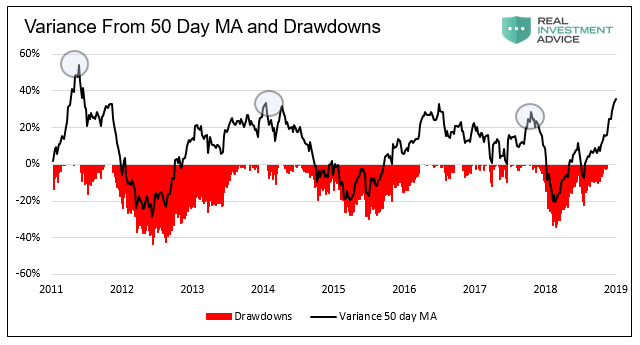

shares in the company. Apple also appears to be over extended on a technical basis.

The graph below shows the premium or discount of Apple stock price to

its 50 day moving average. As circled, three of the last four times that

the stock has been this far above the moving average, a drawdown of at

least 20% occurred.

Data Courtesy Bloomberg

Our simple conclusion is that Apple is a speculative investment with

zero guarantees and, therefore a poor substitute for a money market

fund.

Sorry Mr. Deporre, but Apple is not cash. When markets drop in

earnest, so will Apple, as suggested by its beta to the S&P 500 of

1.06. Holding Apple shares will not afford you the ability to

take advantage of lower prices when stocks go on sale. Therein lies an

important difference between the utilization of cash and stocks in a

portfolio. Mr. Deporreには申し訳ないが、Appleは現金とはわけが違う。相場が深刻な下落となると、Appleも同様だろう、S&P500に対するベータが1.06ということでも解るだろう。相場が下落した時Apple株を持っているからと言って有利なことは何も無い。現金ポジションを持つこととキャッシュを持つことの違いの重要性に関する嘘がまかり通っている。

The graph below shows the percentage drawdowns that occurred in Apple’s stock over the last fifteen years.

下のグラフはApple株の過去15年の下落割合を示す。

Data Courtesy Bloomberg

Summary 要約

There are two key points that Deporre’s article fails to consider. Deporreの記事が考慮していない重要な点が2つある。

First, an equity stake in any company – whether a boring utility or hot IPO – is speculative, especially when valuations are above fair value. Value is never guaranteed, but it is far less uncertain when the price paid is below fair value.

Second, cash is king when markets decline. Investors

that are fully invested with little cash as an insurance policy tend to

sell when markets decline rapidly. Quite often, a low is marked with a

massive amount of capitulation selling. Those who harvest gains when

markets are over-valued and hold a reasonable amount of their portfolio

in cash can buy stocks that trade at a discount to fair value from those

who are panicking.

第2、相場が下落するときは cash is king だ。ほとんど現金を持たつ全面露出の投資家は相場急落の時安全のために売る傾向にある。度々見られることだが、強制的な巨額の降伏的売りを引き起こす。市場が過剰なバリュエーションになったときに利益を確定し現金をかなり持つ投資家だけが皆がパニックになったときに割安のフェアバリューで株式を購入できる。

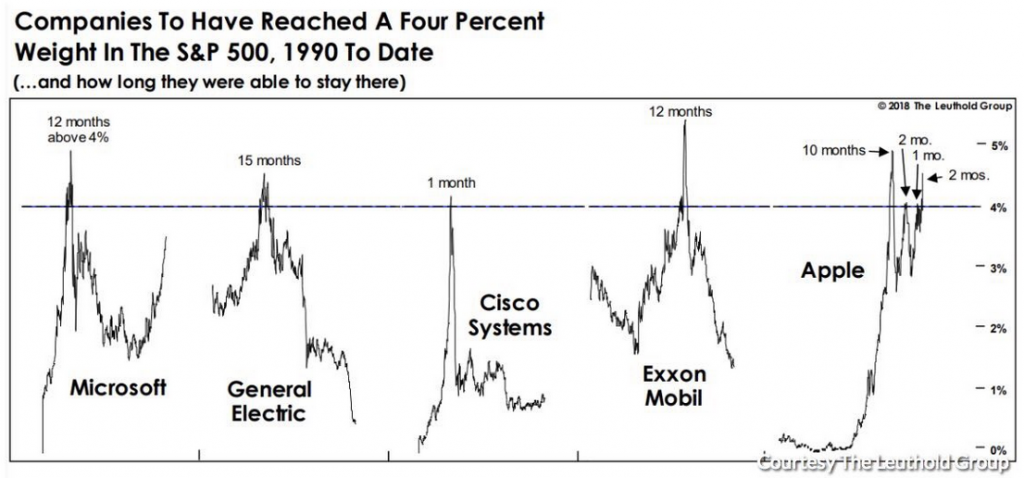

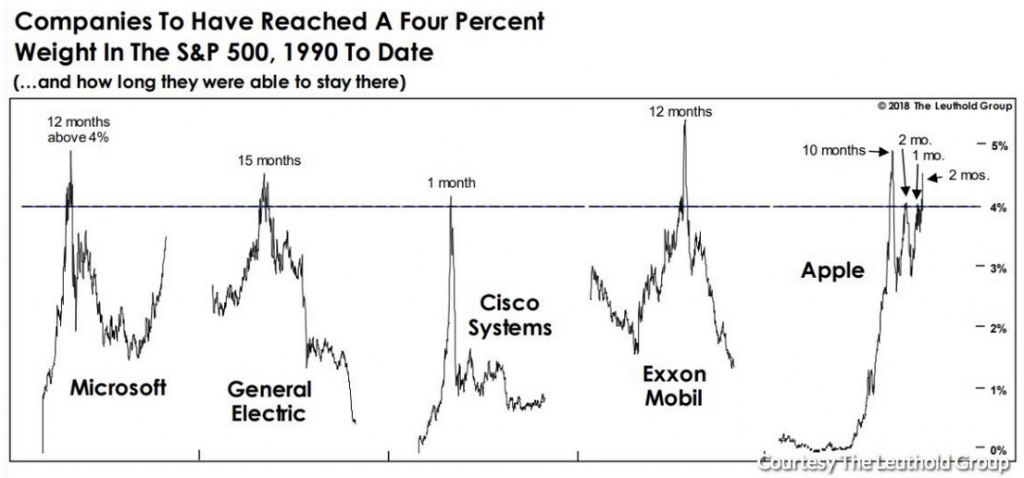

We leave you with an interesting graph from The Leuthold Group.

How Are Gold And Money Supply Related? by Tyler Durden Sun, 06/14/2020 - 13:00 Authored by Mike Shedlock via MishTalk, M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか? Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US. よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。 "There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. " 「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」 Clear Correlation? 明らかな相関? The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames. このツイートの主張は私が示す最初のチャートが示すものとは異なる。というわけでこのtweetの主張を別の時間フレームで見てみよう。 Gold vs Rate of Change in M2 Money Supply ゴールド vs M2マネーサプライの変化率 If we look at longer time frames, the rate of increase in M2 theory falls flat on its face....

Is The Stock Market As Confused As You Are About A Recession? Written by Lance Roberts | Apr, 1, 2019 Last week, Barron’s ran an article entitled “The Stock Market Is Just As Confused About A Potential Recession As You Are?” To wit: 先週バロンズにこういう記事が掲載された「株式市場は景気後退を予感させるほどに混乱しているだろうか?」見てみよう: “Investors have long used where we are in the economic cycle to decide which stocks to buy and sell. New research from Nomura’s Joseph Mezrich flips that on its head by showing how investors can use stock performance to help determine where we are in the cycle. Too bad the market is sending mixed messages right now.” 長らく投資家は現在景気サイクルのどこに居るかを見てこの株式を売るか買うかを判断してきた。野村證券のJoseph Mezrichの最近の研究では、これが逆さで、投資家は株式のパフォーマンスを見て今景気サイクルのどこにいるかを判断している。最悪なことに現在相場は悪化改善混在のメッセージを送っている。」 But let’s be clear here; no one wants the party to end. So, despite a struggling stock market over the last year, slowing economic growth, and a collapsing yield curve, there are s...