Authored by Mike Shedlock via MishTalk,

M2 Money Supply is surging. Will gold follow? M2マネーサプライが急増している。ゴールドはこれを追従するだろうか?

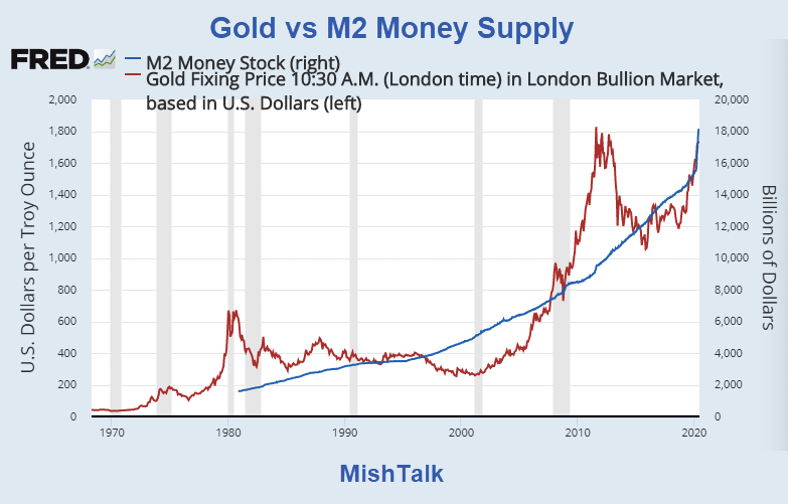

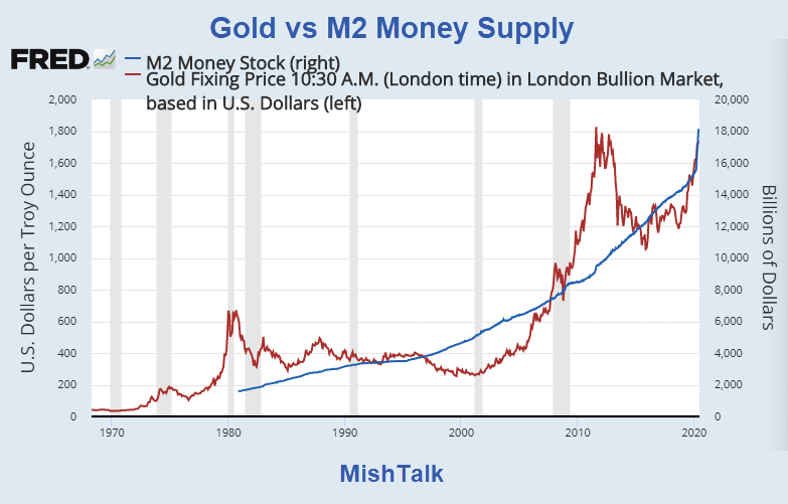

Let's investigate an alleged relationship between gold and M2, a measure of money supply in the US.

よく言われるM2(米国のマネーサプライ指標)とゴールドの関係について調べてみよう。

"There’s a clear correlation between the annual growth rate in M2 money supply and the price of the yellow metal. "

「M2の年率増加速度とゴールド価格の間には明らかな相関がある。」

Clear Correlation? 明らかな相関?

The Tweet claims something different than my lead chart depicts. So let's investigate the above idea in other time frames.

If we look at longer time frames, the rate of increase in M2 theory falls flat on its face.

もっと長期間を見ると、M2増加率理論は意味を成さないことが解る。

One can force a correlation starting in 2010 but that is purposeful

cherry-picking a timeframe. and even then, the time period in the box is

counter-trend.

Similarly, one can find times when gold is correlated to the dollar,

the Yen, and most likely the popularity of peanuts at Cub games in some

time frame.

The best correlation I can find to the price of gold is faith in

central banks. Gold collapsed from $850 to $250 under Greenspan's "Great

Moderation". Greenspan was viewed as the "Maestro" until the dot-com

bubble collapsed.

Gold went on a tear during the housing bubble, but put in a top when ECB president Mario Draghi gave his famous speech: "We will do whatever it takes to save the Euro, and believe me it will be enough."

Draghi did nothing. His speech was enough. Bond yields on Greek,

Portuguese, and Italian bonds started collapsing right after that

speech. It was not until years later the ECB resorted to negative

interest rates and QE.

Gold started rising again when the ECB went nuts with QE and the Fed

started talking about "normalization"that anyone in their right mind

knew was not coming.

The BIS did a historical study and found routine price deflation was not any problem at all.

BISは長年物価デフレを研究してきた、そこに何ら問題はないという。

"Deflation may actually boost output. Lower prices increase real

incomes and wealth. And they may also make export goods more competitive,” stated the study.

It’s asset bubble deflation that is damaging. When asset bubbles burst, debt deflation results.

資産バブルデフレは損失を生み出す。資産バブルが破裂すると、債務デフレが生み出される。

Central banks’ seriously misguided attempts to defeat routine

consumer price deflation is what fuels the destructive build up of

unproductive debt and asset bubbles that eventually collapse.

Amazonで買物をしてContrarianJを応援しよう Albert Edwards: This Was The Final Recessionary Shoe, And It Has Now Fallen by Tyler Durden Thu, 06/27/2019 - 12:45 Exactly three months ago, in late March, the 3 month-10 year spread inverted for the first time since 2007... ちょうど3か月前の3月遅くのことだ、3M10Yスプレッドが2007年以来初めて反転した・・・・ ... an event which sparked near-panic in the market as historically curve inversion has preceded the last 7 recessions. ・・・市場は準混乱状態になった、というのも歴史的に見てイールドカーブ反転が過去7回の景気後退の前兆となっているからだ。 However, while the inversion was certainly a memorable event, the question on everyone's lips is how do risk assets perform once the curve flattens and/or inverts. According to backtests from Goldman, since the mid-1980s, significant stock drawdowns (i.e. market crashes) began only when term slope started steepening after being inverted. ...

Powell Keeps The Bond Bull Kicking Written by Lance Roberts | Mar, 21, 2019 In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September. 多くの人が予想したとおり、FEDはFFR変更をしないだけでなく来年も不明とした。さらには、QTを9月末に終えると約束した。 The key language from yesterday’s announcement was: 昨日の発表の重要な部分はこういう具合だ: “ Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter . Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low. 「1月のFOMC以来の情報を分析すると、労働市場は強いがQ4に比べると経済成長は鈍化している。2月の雇用環境にほとんど変化がなかった、ここ数ヶ月確実に雇用は増えている、そして失業率は低いままだ。 Recent indicators point to s...

Amazonで買物をしてContrarianJを応援しよう "On The Precipice" by Tyler Durden Mon, 06/24/2019 - 14:30 Authored by Kevin Ludolph via Crescat Capital, Dear Investors: The US stock market is retesting its all-time highs at record valuations yet again. We strongly believe it is poised to fail. The problem for bullish late-cycle momentum investors trying to play a breakout to new highs here is the oncoming freight train of deteriorating macro-economic conditions. 米国株式は記録的バリエーションのもとで再度過去最高を試している。私どもはこれが失敗すると強く信じている。景気拡大終盤で強気のモメンタム投資家が新高値を試そうとしていることの問題は、マクロ経済条件の悪化にある。 US corporate profit growth, year-over-year, for the S&P 500 already fully evaporated in the first quarter of 2019 and is heading toward outright decline for the full year based on earnings estimate revision trends. Note the alligator jaws divergence in the chart be...