YCCがやってくる:FEDは衝撃的な株式ラリーを引き起こそうとしている

世の中にフリーランチはないですからね、米国も英国も金融抑圧の代償は通貨安でした。

Here Comes Yield Curve Control: The Fed Is About To Unleash A Mindblowing Stock Rally

With consensus growing that the Fed will unveil Yield Curve Control for the rates market, where it pins the short end somewhere just above 0% to avoid a spike in yields, some time around the September FOMC meeting if not sooner, it is worth recalling that this won't be the first time the US has implemented a monetary policy that was enacted by both Japan four years ago and most recently Australia.

金利市場でFEDがYCCを行うだろうというコンセンサスが醸成されている、短期金利を0%からほんの少し上にピン留めし金利急騰を防ぐのだ、すぐにではなくとも9月のFOMCで明らかになるだろう、日本はすでに4年前からこの政策を実行しておりつい最近オーストラリアも始めた、ただし米国ではこれが初めての経験で無いことを思い起こすのは大切だ。

We first discussed the original YCC episode back in 2012, reminding readers that the US first underwent a period of Yield Curve Control lasting 9 years between March 1942 and March 1951 to allow the US to keep rates low during WWII and its immediate aftermath, and which concluded with the Fed-Treasury Accord.

ZeroHedgeが最初にYCCを議論したのは2012年のことだ、読者に米国の最初のYCCを思い起こさせた、1942年3月から1951年3月まで9年間実行した、第二次世界大戦とその直後のにかけて米国は金利を低く抑えた、そしてこの制作はFEDと財務省の協定のもとに実行された。

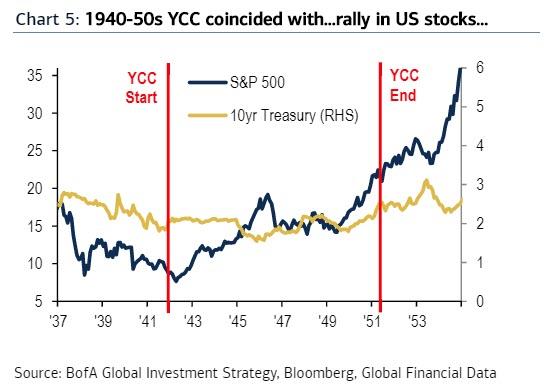

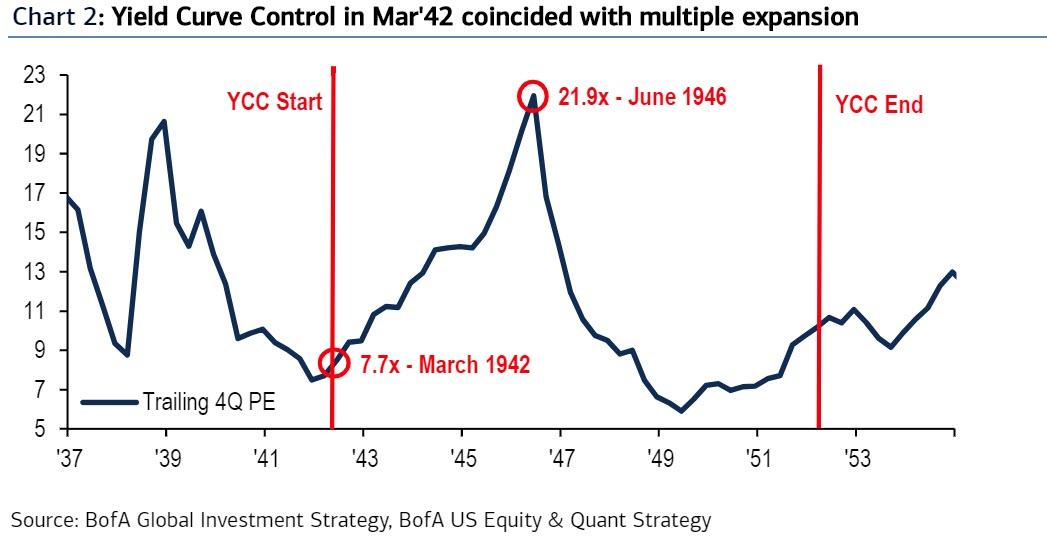

What is remarkable about this first YCC period - when the Fed capped yields at 2.5% to allow Treasury to fund cheap debt in WWII - is that as BofA's Michael Hartnett points out it coincided with start of a huge rally in US stocks...

この最初のYCCで顕著なことはーーFEDは金利を2.5%に抑え、財務省のWWIIの戦費調達費用を安くした結果ーーBoAのMichael Hartnettが指摘することだが、この制作で米国株に巨大なラリーを生み出した・・・・

... multiple expansion as PEs soared from 7.7x in March 1942 to 22x in 2 years, nearly tripling over a very short period of time...

PERは1942年3月には7.7xだったのが二年後には22xになった、とても短期間に株価は3倍になった・・・・

... and a sharp upward inflection point up in US home prices.

・・・そして米国住宅価格も急騰変節点となった。

BofA is not the only one to hint that the coming YCC could result in a massive rally for risk assets: Bloomberg does too, writing overnight that "should yield curve control go global, it would cement markets’ perception of central banks as the buyers of last resort, boosting risk appetite, lowering volatility and intensifying a broader hunt for yield."

これからのYCCがリスク資産に巨大なラリーを引き起こすのではないかと考えるのはBoAだけではない:ブルームバーグも同じ見方をしている、昨夜の記事では、「YCCは世界的な動きで、市場は世界の中央銀行がラストリゾート買い手になると確信している、これがリスク選好を引き起こし、ボラティリティを下げ、そして更に金利を引き下げる。

And while money managers caution that such an environment could fuel reckless investment already stoked by a flood of fiscal and monetary stimulus - an environment which Jay Powell recently said the Fed would carefully nurture now that the central bank is openly blowing asset price bubbles - "they nonetheless see benefits rippling across credit, equities, gold and emerging markets."

財政金融刺激策で資金が洪水のように溢れすでに見境のない投資がすでになされている環境で、マネーマネージャは注意喚起するがーー最近Jay Powellが言うには今は注意深くFEDがみまりながら公然と資産価格バブルを膨らませているーー「それにも関わらず、彼らは与信市場や株式、ゴールド、そして新興市場の変化を好ましいと見ている」。

"It depends on the form and the price but broadly speaking it’s the green light to carry on with the QE trade -- buy everything regardless of valuation,” Aberdeen's James Athey told Bloomberg.

その変化の様相と価格レベルに依存するもので、全般的に見ればこのQE環境は青信号だーーバリュエーショーンに無関係に何でも買え、」とAberdeen社のJames Athey はブルームバーグに告げた。

Perhaps the only question is just how powerful the surge in stocks will be once YCC is unveiled: the answer may depend on how much of the curve ends up being "locked out." Recall that two months ago Credit Suisse repo guru Zoltan Pozsar said that YCC would only be needed for maturities through 3 years. However, Societe Generale sees a case for focusing further out the curve, expecting that 5- and 7-year Treasuries may rally if the Fed looks to go beyond controlling just the front end.

多分唯一の疑念は一旦YCCが明らかになったとき株式がどの程度力強く上昇するかだ:その答えは、どの程度イールドカーブが「locked out」されるかによる。二ヶ月前にレポ市場の導師と言われるZoltan Pozsarが言ったことを思い起こすが良い、YCCが必要なのは満期が3年までの国債に対してだ。しかしながら、Societe Genraleはもっと長期の国債に注目している、FEDが制御するなら、5年物7年物国債のラリーになるかもしれないと期待している。

Yet while the question of just where on the curve central banks set their target is key, no matter the details it will likely spark a furious rally way. As Bloomberg notes, a 50-basis-point target on the 10-year Treasury yield would spark a bond rally and flatten the curve alongside a probable rise in equities. However, a full percentage point could see bonds bear steepen and trigger a sell-off in shares, said Aberdeen Standard’s Athey.

ただし、中央銀行が目的とするイールドカーブの位置が問題だが、その詳細に関わらず激しいラリーを引き起こすだろう。ブルームバーグによると、10年物債権の目標金利が50BPSとなると債権ラリーが勃発しイールドカーブは平坦化し株式上昇を引き起こしそうだ。しかしながら、確実なことは債権ベアとなるとイールドカーブは急峻化し株式下落を引き起こす、とアバディーンスタンダードのAtheyは言う。

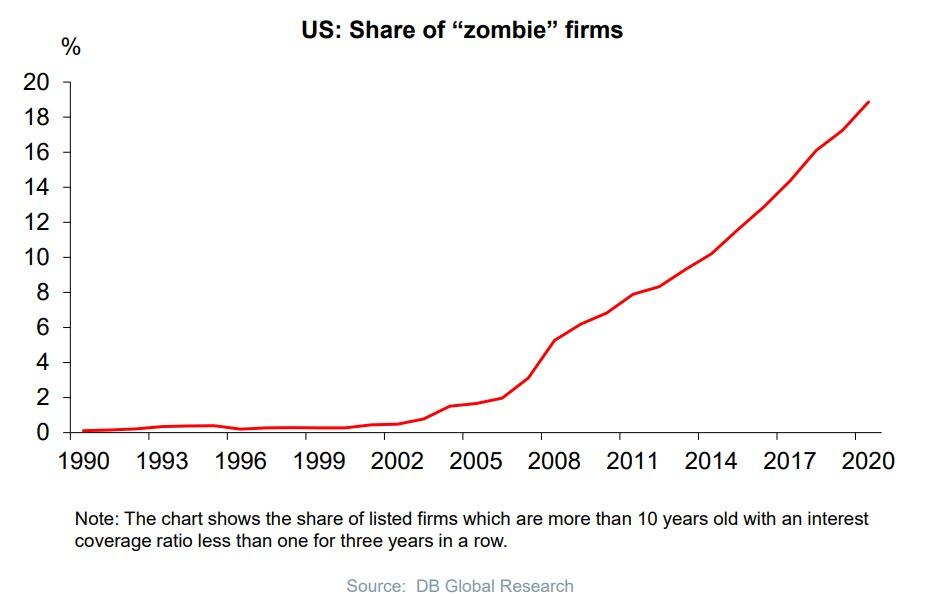

The flipside of the coming surge, is that it will once again come as a result of a dash for trash, as the worst of the worst companies, including most corporate zombies, surge.

これから起きる急騰の副作用は、またもや合理性を超えた行き過ぎを生み出すことだろう、最悪中の最悪と見られる会社、いわゆるゾンビ企業の株式も急騰する。

As if it wasn't enough that the Fed is now buying corporate debt, the capping of interest rates would also help by ensuring corporate borrowers continue to benefit from attractive financing rates, further detaching their fundamentals from their securities. Lower yields in longer maturities would assist investment-grade companies, which tend to issue longer-dated debt than lower-rated borrowers. Meanwhile, junk borrowers would reap the rewards of the general boost to market sentiment.

あたかも、FEDは企業債権を買うだけでは十分でないかのようだ、金利に上限を設けることで、魅了的な金利で企業は借金ができる、こういう会社の株価はますますファンダメンタルズから乖離する。長期債権の金利が下がることで、投資適格企業債権には有利だろう、安い金利で長期に渡る借り入れを行える。そうしている間に、ジャンク・ボンド発行者も市場心理改善の恩恵を受けるだろう。

Companies with high debt loads such as airlines and energy could get a lift, said Charles Diebel, who manages $2.6 billion at Mediolanum SpA in Dublin. U.K. banks could also gain as lenders will have escaped the crushing effect of negative interest rates.

“It will allow the whole rating spectrum of fixed income credits to borrow at incredibly cheap absolute levels during a time of much uncertainty and would certainly be very bullish,” said Azhar Hussain, head of global credit at Royal London Asset Management.

Meanwhile, the further decline in US yields would - in theory - also weaken the dollar and help riskier currencies like the rand and Mexican peso, while benefiting carry trades involving the Indonesian rupee and the Russian ruble according to Vasileios Gkionakis, head of FX strategy at Banque Lombard Odier & Cie SA in Geneva.

そうこうしている間に、米国の金利は更に低下するだろうーー理論的にはそうだーーそしてまたドルは弱くなり rand やメキシコpesoにとっては一息つける、インドネシアrupeeやロシアrubleのキャリートレーダーにとっては恩恵を受けるだろうと、Vasileios Gkionakisは言う、彼はジュネーブのBanque Lombard Odier &Cie SAのFXストラテジスト主任だ。

Of course, once the Fed launches YCC, it will only make the asset bubble - which has already resulted in 20-year-old Robinhood traders taking their lives when trades go wrong - even bigger, as assets becoming fully disconnected from underlying fundamentals. Meanwhile, 10-year yields are negative for nine of 25 developed markets tracked by Bloomberg, while the rest stand well below their one-year averages: "It’s a precarious bubble that could eventually burst, should the wall of stimulus spur inflation down the road and eat into investors’ profits" Bloomberg notes.

当然のことながら、一旦FEDがYCCを遂行すると、資産バブブルを引き起こすに過ぎないーーすでにわずか20歳程度のRobinhoodトレーダーがトレードを誤ったばかりに自らの命を断っているーー更に大きなバブルを引き起こすだろう、すでに株式は全くファンダメンタルズから乖離しているのだ。そうこうしている間に、すでに先進25カ国の市場の内9カ国で10年債はマイナス金利だ、他国もここ1年の平均金利を下回っている:「あまりに不用意なバブルでやがて破裂するだろう、壁の如き刺激策がインフレを引き起こし、投資家の利益も食いつぶすだろう」とブルームバーグは主張する。

Regardless of the risks, the notion that central banks are approaching some sort of curve control is here to stay, as is yet another milestone in central banks' takeover of the bond market, as YCC will further eliminate any information about future inflation the yield curve would otherwise convey, leaving precious metals such as gold the only true inflation hedge. Still, as Bloomberg concludes, the key lesson from the 2008 crisis was that policy makers need to intervene quickly, and investors now expect them to consider any weapon at their disposal.

リスクなど考慮せずに、世界の中央銀行がイールドカーブ・コントロールを行うというのはいわば、中央銀行による債権市場の乗っ取りとも言える、YCCを行うことで、将来のインフレに関する知見を得ることもできなくなるだろう、これまではイールドカーブを見ることでインフレの将来に関する知見を得ることができた、インフレヘッジとして残されるのはゴールドのような貴金属だけだ。それでもブルームバーグはこう結論づける、2008年の金融危機から得た重要な教訓は政策立案者の素早い介入だ、そして今や投資家は彼らの弾薬庫にまだ武器が残されていると期待している。

“Policy makers tightened up the banking system so much that the markets became too big to fail,” said Mark Nash, the head of fixed income at Merian Global Investors in London. "Now they have no choice but to keep them working."

「政策立案者が銀行システムを締め付けるが、市場はすでに too big to fail なのだ、」とMark Nashは言う、彼はロンドンMerian Global Investorsの固定金利部門の主任だ。「今や彼らは今の政策を持続するしか他に道はない。」

Indeed, as JPMorgan asked over the weekend, in a world where trillions are created out of thin air every month, why not just own anything? After all, at this point the Fed will never again allow the market to drop and the US central bank will keep doubling down to preserve risk asset prices until finally it loses control over everything.

たしかに、週末にJPMorganが尋ねられたとき、毎月無からトリリオンドルの資金が生み出される世界では、何かを買わないわけには行かないだろう?結局、この時点でFEDは決して再び市場の下落を許すことはないだろう、そして米国中央銀行はリスク資産を維持するために倍掛けを続ける、ただしそれもすべての制御を最終的に失うまでだ。